Spend management has seen a transformation during and after the coronavirus pandemic, spurred on by a rapid change in businesses’ payments needs.

The Covid-19 pandemic has changed the world of work, significantly shifting the expectations and behaviors of the workplace. This has had a knock-on impact on many supporting industries, not least of all spend management.

Designed to take the pain out of employee and departmental spending, spend management has traditionally been focused around the reimbursement of employee receipts for both domestic and cross-border purchases. However, changes in how and where spending is occurring has had a significant impact on the business needs the space is responding to.

“Even though it sounds like it was here forever, there was a huge evolution in spend management in the last few years,” explains Oded Zehavi, CEO and co-founder of Mesh Payments.

“One of the most important milestones for the spend management space was Covid.”

In the process, the pandemic has sparked the rise of a new breed of company harnessing payment technologies to better meet the spend management needs of post-pandemic businesses, and with a vast potential market and ongoing evolution, there remains significant potential for the future industry.

Covid’s transformation of spend management

Prior to the pandemic, the primary focus of spend management was travel and entertainment (T&E), which led to finance teams citing collections of receipts as their biggest concern. However, Zehavi argues that this was largely “noise” that could be solved by additional staff.

“When Covid happened, overnight that noise was eliminated: no more T&E,” says Zehavi.

“That’s really enabled the finance team to start looking at things that are, in my mind, bigger pains than receipt collection.”

This happened as businesses were also seeing other shifts in payments, led by a mixture of Covid-prompted transformations and wider changes in industry practices. For example, the shift to remote had a knock-on effect on the use of company cards.

While previously, these had often lived in a desk drawer in the office, or in the hands of certain salespeople, within easy reach when needed. However, the pandemic led many to be either canceled or not in the locations they needed to be used.

“Companies were left with very few corporate cards and with a lot of employees all around the country or the world that needed to pay, and they started sharing the numbers all across the company, which created even more complexity and lack of visibility,” says Zehavi.

Compounding this challenge was the shift from one-off large purchases for software to SaaS-based services.

“Now you need to pay a lot on a monthly basis for your LinkedIn subscription, for your MailChimp subscription, for online media, for all the things that are recurring by nature,” he explains.

“You cannot expect the employee to pay for such expenses and to be reimbursed, because you cannot expect the employee to pay $40,000 for LinkedIn ads or for Facebook ads, even though it still happens.”

This mix of factors created a business payments landscape with quite different challenges and pain points compared to before the pandemic, creating what Zehavi describes as “the triggers for the rise of spend management players”.

These companies harness payments technologies such as virtual cards to tackle new business needs, while typically employing a highly appealing business model for would-be customers.

“You don’t charge this client anything; you don’t need him to negotiate pricing,” he says.

“Not only he doesn’t need to pay you anything, you pay him back part of the revenue you collect from interchange. So you pay him to use your product.”

Market landscape: The emerging spend management players

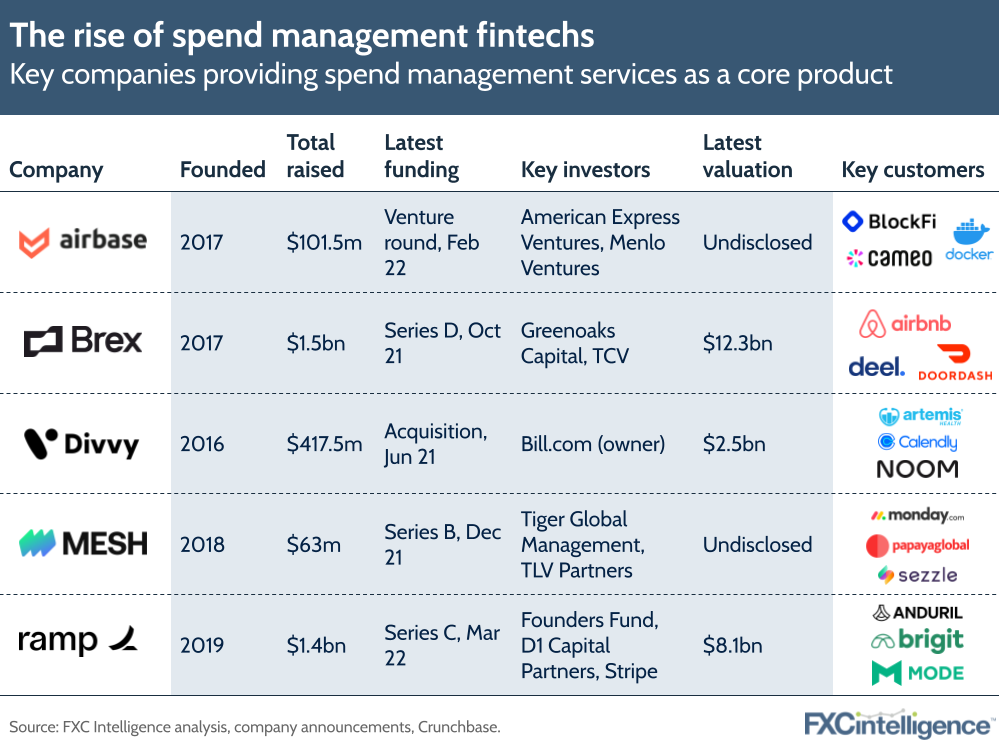

While traditional players are still responsible for much of card purchase volume, a number of key names are waving waves in the space. These spend management fintechs include Zehavi’s Mesh, alongside Divvy, Ramp, Airbase and Brex, which have typically catered to the needs of fast-growth, tech-savvy startups. According to Mesh’s analysis of data published by Nilson Report, they together accounted for between 1-3% of all commercial US card purchase volume in 2020.

Many of these players existed before the pandemic, although did not see as strong success. Divvy, for example, struggled to attract investor support in the US before Covid-19, and ultimately raised funds in Israel. However, the pandemic has provided a rich environment for growth.

“Everybody that had any type of spend management platform has grown,” says Zehavi.

This has also seen some refocus their efforts in an attempt to better equip themselves for future growth. For example, Brex, the biggest player in the group, recently took the decision to refocus on its core customers, many of whom are SMBs, rather than also support microbusinesses with very small numbers of employees. This announcement was initially misunderstood, with many wrongly interpreting it as impacting all SMBs, although the company has since clarified its position.

“We’re focused on the core customers that get more value from Brex. Those who are closer to scaling, so they need things like international hiring, expense management, cash management,” explains Henrique Dubugras, CEO of Brex.

“The technology world, in which companies grow from a few employees to a lot of employees, need those things more than small design studios that have one, two, three people and might not even need expense management.

“Those customers have a bunch of different needs that we weren’t going to build for, so we decided to focus and say ‘we’re not going to serve your needs, so we suggest you move to a different provider’.”

There are also those that have pivoted into the space in response to changing market conditions in their core areas, such as TripActions, a travel company that used its expertise to build a spend management offering during the drop in travel. Now that the corporate trip has returned, its core business has too, but the company now also has a supporting spend management solution for those that need.

Mesh, meanwhile, first developed its product during the pandemic, which Zehavi sees as an advantage as the company “really didn’t need to think about T&E”.

“When we built everything from scratch, we focused on the pain that the finance team had been trying to solve at that specific moment,” he says.

“A lot of our initial traction came from what we built, maybe the most sophisticated product recurring SaaS payments, and we built a lot of technology around the insights and leveraging the data that you can collect from the payment.”

This focus on payment data is key for Mesh, with the company combining data it sources from payments with those from external sources.

“We connect more and more into organizational infrastructure,” he says. “That enables us to converge between the organizational data and the payment data and get better insights about the usage of the product.”

Future developments and untapped opportunities

Looking forward, there is a far greater potential market for the spend management industry to address.

“It’s such an untapped business,” says Zehavi. “There’s not going to be one winner takes all, that’s for sure. It’s still such early days for the entire space.”

While he does anticipate some consolidation in the industry, he also sees a greater shift from banks providing these services to spend management fintechs.

“The coming few years are going to redefine the way that companies choose their corporate spend partner,” he says.

The opportunities for the banks to win is much lower compared to other spaces, because in other spaces you talking about margins and pressure, etc., but here, it’s mostly about technology, integration and reconciliation. There banks will have tough time competing with companies that come from the technology space.”

Meanwhile, travel is returning, but not in the way it was commonplace before. Instead of small numbers of staff, such as salespeople, traveling frequently, Zehavi says that “now almost everybody travels, but much less”. As a result, these expenses are less commonplace, making a 2% FX margin not a matter of concern. This reopening of travel is creating new opportunities for the key spend management players, all of whom are “now launching products that are more tuned to T&E”.

There are potential cross-border concerns, however, around where a major international provider might process a transaction. This is something that companies are beginning to to take notice of as it can be different on different occasions, with different tax implications as a result.

“More and more clients, especially the bigger ones, are sophisticated enough to have these questions and try to optimize that for the benefits,” he says.

“For us and the vendor, a lot of the engine we’ve built is around optimizing that as much as we can, or at least understand what the implication of each transaction is on our core structure, which we need to manage carefully.”

As with much of the rest of the payments space, there is increased interest in partnering with other players, with Mesh recently announcing a partnership with Papaya Global, whilst others have partnered with Stripe. However, the unifying focus for the space is on increased sophistication, driven by more complex client demands and increasing capabilities.

“Companies are becoming more sophisticated and now they are comparing products based on the capabilities of the workflow engine, about integration to the accounting system, their ability to get notifications about different spend behaviors, etc.,” he says.

“It’s less about traditional banking and more about the technology and the integration. That’s a trend that is going to increase even more.”

And with it, spend management is seeing its adoption move beyond tech-led startups.

“We are seeing adoption of spend management platforms even in non-tech verticals; healthcare, NGOs, manufacturing, they’re now starting to adopt,” he says.

“Historically, it was only startups. Now a lot of our biggest clients are companies that don’t have any links to software development.”