Our latest cards report, ‘Understanding the economics of cross-border card payments’, takes a deep dive into the costs and complex economics.

Credit and debit cards are used for everyday purchases, both online and in physical stores, in home countries or abroad. When it comes to cross-border purchases, however, the process can be quite complicated – there are a large number of players involved, and the additional fees and costs are not always straightforward.

In this report, we will guide you through the process and economics of cross-border card transactions and the distinctions between payments made in a foreign currency and in the home, card currency.

We will explain the different fees and costs involved and present some analysis of the variation of these costs across countries and issuers based on FXC Intelligence card pricing data. This report will also highlight the benefits of providing local currency payments and opportunities for merchants and payment processors.

Contents:

- The process of a cross-border card transaction

- The economics of a cross-border card transaction

- Variations in cross-border card fees

- Conclusions

The process of a cross-border card transaction

Processing cross-border card transactions involves a number of different players including merchants, payment gateways (for online transactions), payment processors, card networks and banks. Depending on the currencies a merchant allows customers to pay with, there are generally two types of cross-border payments:

- Foreign currency transactions – cardholder pays in a foreign currency which is converted through the card network (e.g. Visa, Mastercard).

- Home, card currency transactions – cardholder pays in the currency of their card, the foreign currency conversion component of the transaction is handled by the merchant’s payment processor or FX partner bank.

Players involved in processing card transactions benefit from the fees and margins they can charge. Depending on which of the two types of transaction it is, different players have the opportunity to reap the gains from the FX conversion component of the transaction. In a foreign currency transaction, the card issuer and card network split the margins; in a home, card currency transaction – the merchant and its FX partner reap the FX revenues.

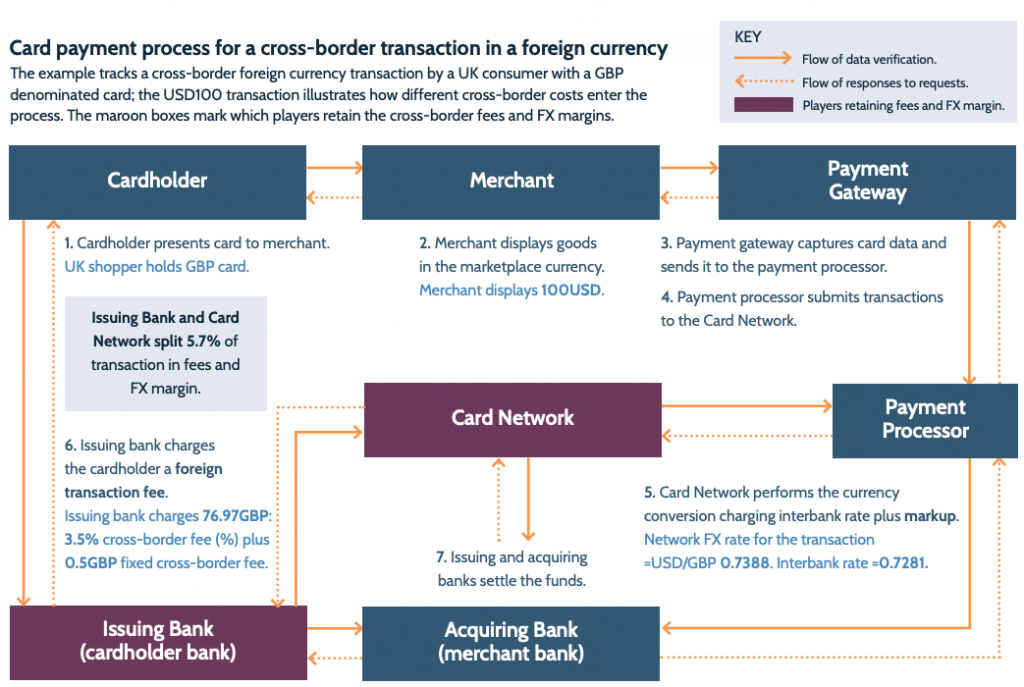

The process: Foreign currency transactions

Figure 1 walks through a cross-border transaction process where the customer pays in foreign currency (USD). The process starts with a merchant charging a customer for a purchase (in foreign currency). The payment gateway acts as an online equivalent of a point-of-sale terminal – it captures the card data and sends information to the payment processor.

The payment processor submits payment details to the relevant card network and acts as a mediator between all players. The card network then performs the currency conversion, makes authorisation requests, and communicates information between the issuing and acquiring banks.

Authorisation and subsequent settlement procedures for cross-border transactions can be lengthy and usually takes several days compared to instant, local transactions.

In a foreign currency transaction the card network does the FX conversion and the markup passes through to the customer via the card issuer.

Finally, the issuing bank charges the customer an overall fee for processing a cross-border foreign currency transaction. In this type of transaction, the card network and card issuer benefit from all the cross-border fees.

Figure 1

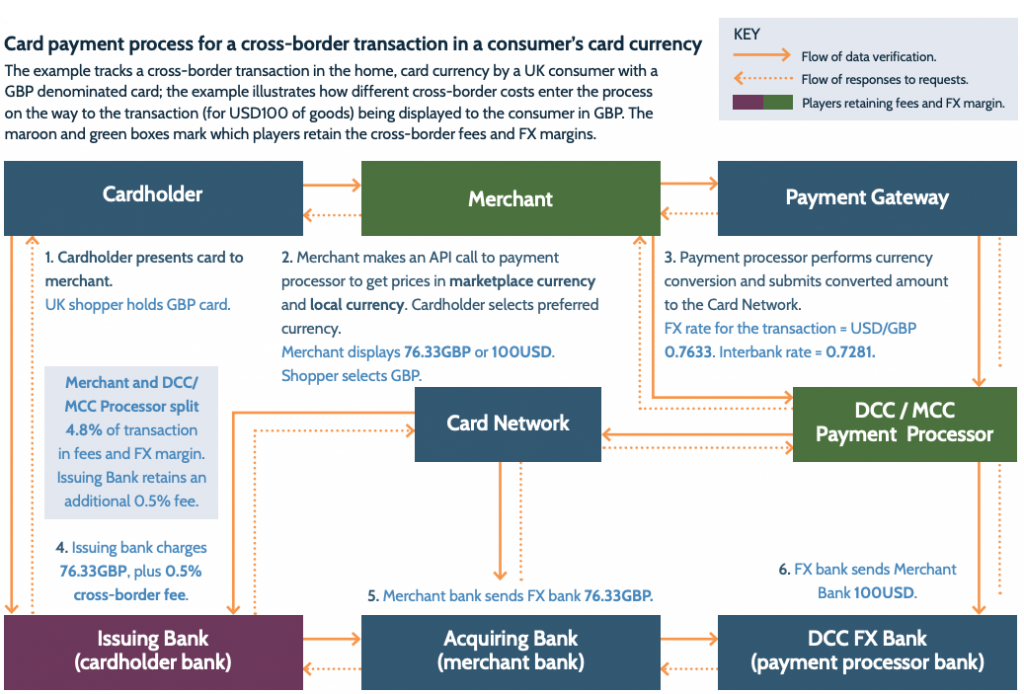

Cross-border card currency transactions

Figure 2 walks through a cross-border transaction where the customer pays in their home, card currency (GBP). The process largely involves the same players as a foreign currency transaction; however, there are additional participants in the process who help the merchant to perform the currency conversion and allow the customer to shop in their card currency.

In a cross-border card currency transaction the payment processor performs the conversion and will share some of the FX margin with the merchant; unlike a foreign currency transaction, the FX conversion margins do not go through the card network nor are they passed on to the customer through the card issuer.

The merchant and its payment partners benefit from the margin on the FX conversion. This FX margin can be sizeable (see Figure 2 and Table 1). In addition to this FX margin, the card issuer may apply a fee, even on cross-border transactions in the card currency, which the customer will see on their card statement.

Figure 2

The economics of a cross-border card transaction

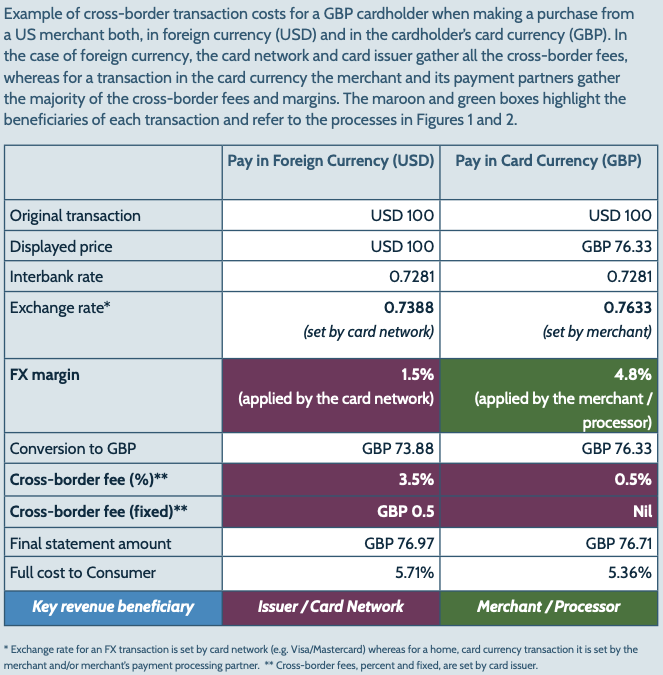

Teasing out the different fees and costs associated with the different types of cross-border transactions is challenging. To dissect these, we extend the example above (Figures 1 and 2) and align the fees and FX margins applied to a cross-border transaction made in a foreign currency side by side with one made in the card currency (Table 1).

Table 1

FX margins

This is the margin between the mid-market rate (or interbank rate) and the rate charged to consumers to make the conversion to the cardholder’s card currency (see Table 1 Exchange rate).

For a foreign currency transaction, the conversion rate is set by the card network (e.g. Visa, Mastercard, American Express, etc). In the example in Table 1, the card network applies an FX margin of 1.5%.

For a transaction in a customer’s home card currency, the FX margin is applied by the merchant or the merchant’s processor when they convert the price from the foreign currency to the cardholder’s home currency – the FX conversion is where the merchant and the merchant’s processor make the bulk of their margin. In the example in Table 1, the merchant’s processor applies a FX margin of 4.8%.

Cross-border issuer fees

The issuer will often apply one or more additional charges to a cross border transaction. This is usually a percentage and/or a fixed fee. These fees are most commonly applied when the transaction is in foreign currency. In the Table 1 example, for a foreign exchange transaction the issuer charges an additional 3.5% of the amount (after it is converted to GBP by the card network) plus another cross-border fixed fee of GBP0.5.

Some issuers also apply such charges to transactions placed in a cardholder’s card currency. In the Table 1 example, for the transaction in the customer’s home currency (GBP) the issuer charges an additional 0.5% of the amount (after it is converted to GBP by the merchant’s processing partner).

Identifying these fees from a card programme’s terms and conditions can prove difficult. Few issuers explicitly break out the fees for cross-border transactions in foreign and home, card currency. Often, a generic term such as ‘cross-border fees’ is used which may include either types of fees or both.

Credit card processing fees

Card processing comes with three types of fees for the merchant: processing fees, card scheme fees, and interchange fees – interchange fees being the largest component. These fees are incurred by merchants and are not directly charged to the consumers. However, these are usually passed on through other margins, such as FX margins for example.

- Processing fee – charged by the payment provider (processor) for processing the transaction.

- Card scheme fee – charged by the card schemes for using their network.

- Interchange fees – transaction fees that the acquiring bank (merchant bank) must pay whenever a customer uses a credit/debit card to make a purchase from their store. The fees are paid to the issuing bank (cardholder bank) to cover handling costs, fraud and bad debt costs and the risk involved in approving the payment.

Government taxes

Taxes are further costs that are often involved in cross-border transactions. In some countries, governments levy taxes for online purchases of goods and services. These taxes are added on top of any fees applied by card issuers for cross-border transactions and can span the range of 1-35% of the transaction amount. It is therefore important for cross-border merchants, payment processors, and card issuers to be aware of local regulations to understand the entire costs consumers will face in order to adjust their pricing strategies accordingly. For detailed information, see our report on cross-border taxes for ecommerce sellers and payment companies.

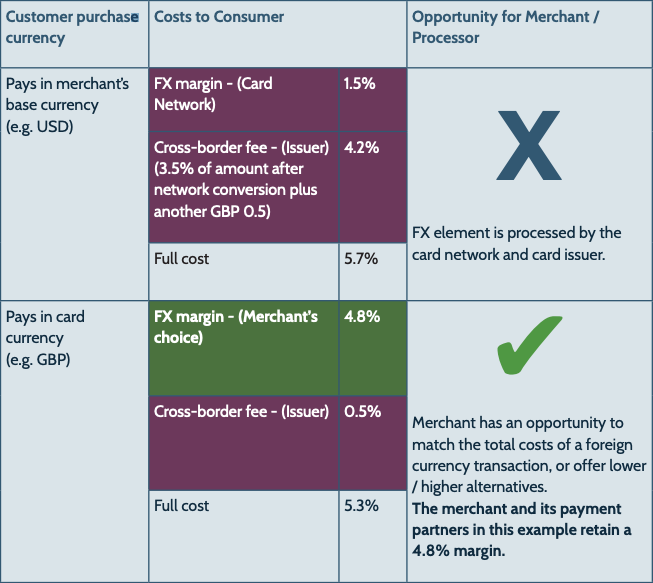

Opportunity for merchant and payment processors

The merchant and its payment partners benefit from the FX margin on the FX conversion. Depending on how the merchant and processor decide to set their pricing for the FX conversion – this FX margin can be sizeable.

Based on the examples we walked through above, Table 2 highlights the opportunity for merchants and payment processors in the FX space.

Table 2

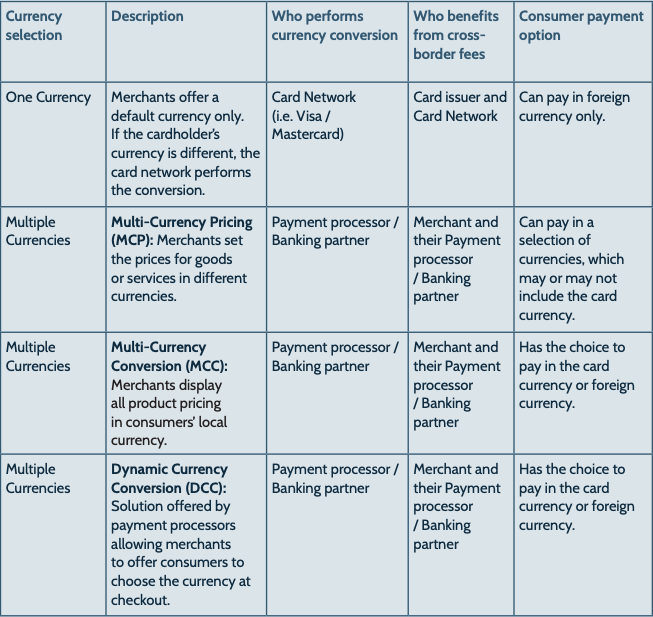

Checkout experience and different types of merchant pricing

Merchants initially price products in their base currency – for instance a US merchant will price in USD (as in the examples above). Then, depending on their preferred way of handling cross-border transactions – merchants can offer several different checkout experiences:

- Consumer can pay only in merchant’s default currency

- Consumer can pay in one of several currencies (e.g. USD, EUR, GBP but not necessarily their card currency)

- Consumer can pay in either merchant’s or their own card currency (e.g. NOK, SEK, CHF, MXN, PEN)

These different experiences are underpinned by different merchant and payment processor solutions (Table 3). Depending on the solution, either the card network or the merchant and its FX partner will perform the FX conversion and benefit from the FX margin.

Table 3

Variations in cross-border card fees

At FXC Intelligence, we have built up a dataset of pricing and transaction data for around 900 card issuers and over 12,000 card programmes in more than 120 countries. We collect and analyse terms and conditions for card issuers across the world to compare the indicated rates for cross-border transactions against the fees recorded on our own database of actual transactions. In this section we will present some country-level data as well as fees charged by individual issuers.

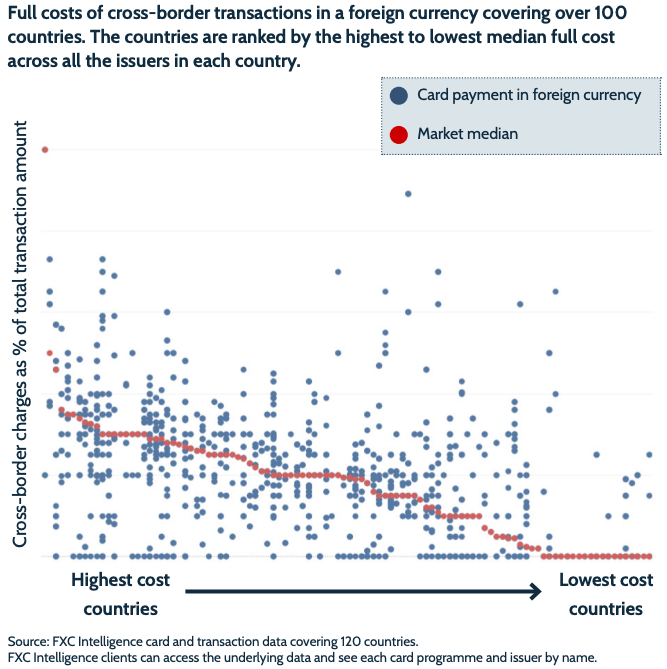

Figure 3 presents cross-border charges as a percentage of the total transaction amount across different countries and issuers. A key takeaway highlighted here is that the full costs incurred by consumers vary significantly across countries – this is illustrated by the market medians of the costs of foreign currency transactions. Another important finding is that there is considerable variation amongst the fees charged by issuers within each country as indicated by the range of blue marks.

Figure 3

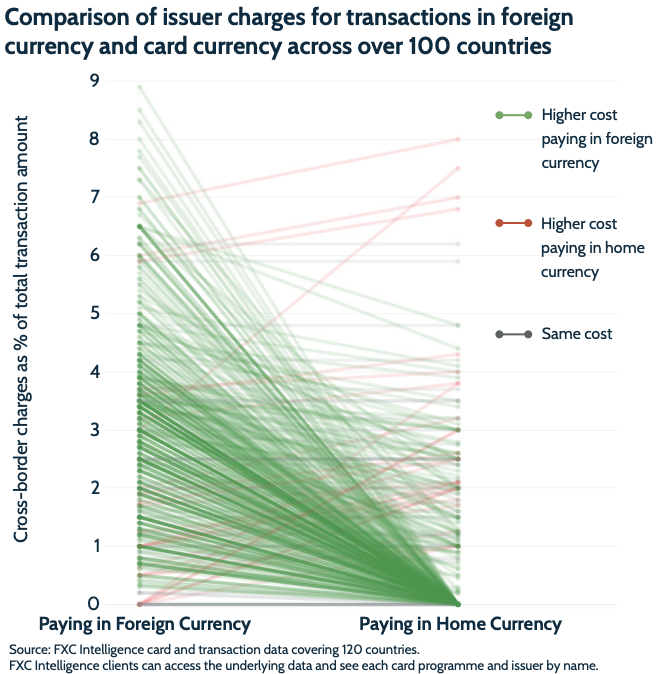

In the chart illustrated in Figure 4, we look at the fees for cross-border foreign and home currency transactions across more than 100 countries. Consumers by and large face higher issuer charges for FX transactions. The full cost of a foreign currency transaction incorporates the FX markup and any additional fees charged by card issuers.

For home currency transactions in Figure 4, the data includes the fees charged by the card issuer only and excludes the FX markups which are attributed to the merchant and its payment or bank partner. By removing the merchant component of the costs, we are able to look exclusively at the costs imposed by the issuer when consumers pay in foreign and card currency. However, it is worth noting that merchant markups –- DCC / MCC / MCP conversion margins – can be sizeable.

Figure 4

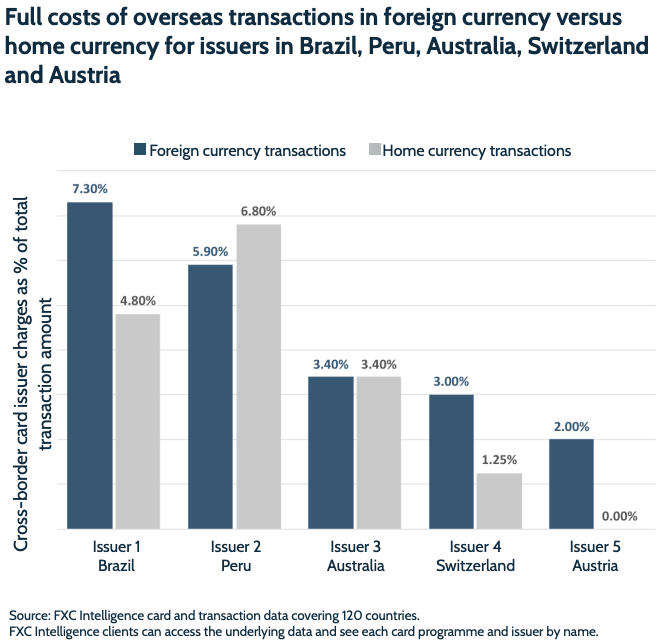

To illustrate some examples of the different types of fees for individual issuers, we will present charges from a card issuer in the following countries: Brazil, Peru, Australia, Switzerland and Austria.

Figure 5 shows the full cost of cross-border transactions for a bank within each of the five aforementioned countries – the blue bars represent the full cost of transactions in foreign currencies and the grey bars represent the full cost of transactions in the local, card currency.

Figure 5

Figure 5 again illustrates that fees charged by card issuers for cross-border transactions vary across countries and across issuers – for example, Issuer 1 in Brazil charges 7.3% whereas Issue 5 in Austria charges only 2.0%. It is also more common for card issuers to charge customers lower fees, or no fees at all, for cross-border transactions in local currency than in foreign currency.

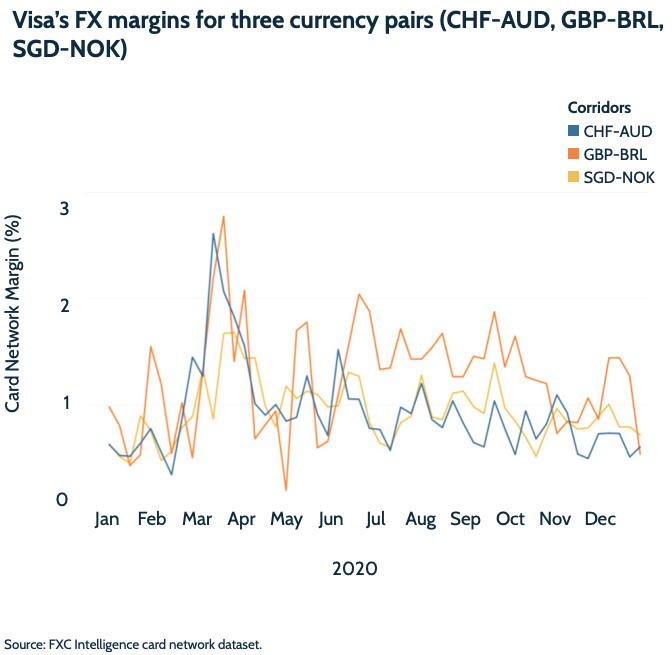

Overall, there is great unpredictability for the consumer, particularly in some countries, when it comes to the fees they’re charged for FX transactions. One reason for these fluctuations is the fact that the full costs also include FX markups as discussed in the section above. The card networks (e.g. Visa, Mastercard etc) can vary their FX rates and FX margins substantially on a day-to-day basis for any given currency pair (Figure 6).

Figure 6 shows the weekly average FX margin for three currency pairs charged by Visa for the duration of 2020. The margin fluctuates considerably for each currency pair. This adds uncertainty as to the full cost of a transaction for consumers as they do not usually know these network rates until they see them after the fact on their bank statements.

Figure 6

Conclusions

The analysis presented in this report casts a light on cross-border card transactions and the technicalities of the process, fees, and costs involved.

The players involved in processing cross-border transactions in both foreign currency and a customer’s card currency are largely similar. The main difference is who performs the currency conversion and therefore reaps the revenues associated with it. In the case of a foreign currency transaction, the card network performs the currency exchange and retains a FX margin and the card issuer charges a fee for processing the cross-border transaction. Whereas, in the case of a cross-border transaction made in the card currency, the merchant and payment processor set the FX rate and therefore have the opportunity to earn the FX margin.

The opportunity for a merchant and payment processor to allow the customer to pay in their home, card currency can be considerable.

Looking at fees and charges for cross-border transactions across over 100 countries – we have seen that these vary considerably both across countries and across issuers within any country.

This variability and the relatively higher costs applied by the card network and card issuer for FX transactions presents a sizeable opportunity for merchants and their processing partners to allow the consumer to shop in their home currency.

In addition, when the card networks make the FX conversion this can add further uncertainty for the consumer given that these rates are usually known after the fact and that the FX margin on the rates for any given corridor can fluctuate considerably day-to-day, week-to-week. Combined, the issuer fees and FX margins can lead to significant cost uncertainties for the consumer.

Some parallels can be drawn between cross-border card transactions and cross-border money transfers. The commission for both will depend on the currency being transferred or paid into, the country of the transfer or payment, and whether the money is being transferred from a bank account or credit/debit card. However, money transfer services usually state upfront the exact fees and exchange rate that will be charged to transfer the money.

The EU has taken steps to help limit the cost uncertainties to consumers when making cross-border transactions. In 2020 it introduced new regulations to bring about full disclosure of fees and conversion costs. However, this still remains a challenge for many providers.

Why is there so much uncertainty when it comes to charges for cross-border card transactions? Some potential factors contributing to the variability and uncertainty of cross-border card transaction fees include:

- There are a large number of players involved at different stages of processing cross-border card transactions, each charging a small fee for the services provided.

- The FX margins vary significantly across card networks, across different currencies, and across the same currency on different calendar days.

- The fees and charges stated in card issuers’ terms and conditions often understate the costs consumers will ultimately face.

Providing consumers the option to pay in their home currency is a good opportunity to reduce uncertainty for consumers as they are able to see the cost of purchases imposed by the merchant and its payment partners in advance. Furthermore, understanding all costs consumers face in cross-border transactions help merchants, payment processors, and FX partners optimise their pricing strategies and benefit from a potential FX margin.