An extensive teardown of Wise’s pre-IPO financials and its place in the wider money transfer industry.

Introduction

On 17 June 2021, Wise announced that it would be going public via a direct listing on the London Stock Exchange, which is expected to happen in early July.

The announcement, which was published in a blog post by CEO Kristo Käärmann a few months after the company rebranded from TransferWise, put an end to months of speculation about the company’s plans. These had included suggestions of listings on both sides of the Atlantic, and routes to market that included an IPO or a SPAC.

Alongside the announcement, Wise published a registration document for its public listing, which provides the greatest insight into the company’s financials that have ever been published.

In this report, we take a deep dive into these financials, as well as Wise’s history and product offerings, and compare them to those of its competitors in order to get a full picture of where Wise sits in the wider industry.

Contents

The road to Wise’s direct listing

History of Wise

Wise was founded in 2011 as TransferWise by Kristo Käärmann (left) and Taavet Hinrikus.

Taavet Hinrikus was Skype’s first employee, who was working for the company in Estonia while living in London. His friend Kristo Käärmann was also living in London and working for Deloitte, but paying for a mortgage in Euros. The two had an informal arrangement to transfer money to each other when the mid-market rate was favourable to cover their cross-currency expenses. This gave rise to the idea of TransferWise.

The company began with its core money transfer product, and by 2014 customers had transferred over £1bn using the platform. In 2015, it expanded to the US and Australia, and in 2016 it added its first business products.

In 2017 the company opened it Asia-Pacific hub in Singapore, and launched multicurrency business bank accounts, with consumer multicurrency accounts and debit cards following in 2018.

In 2020, TransferWise announced that customers were holding over £2bn in deposits in its multicurrency accounts. That same year, it was also licenced by the UK’s FCA to offer regulated investment products. In 2021, the company rebranded to Wise.

Funding

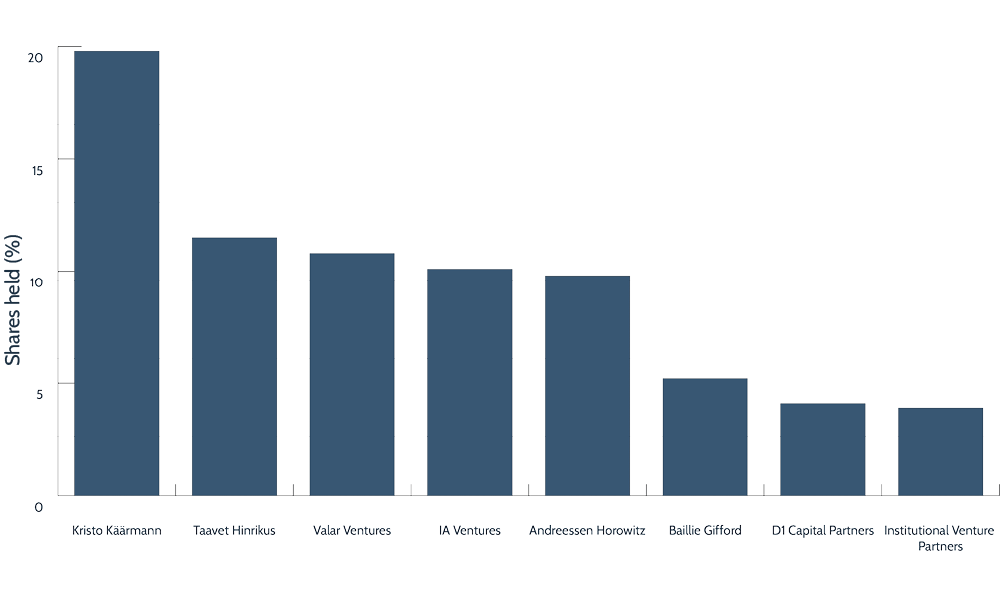

Wise has consistently raised additional funds every year since it was founded in 2011. Of the organisations that still hold notable shares in Wise, the vast majority invested in the company within its first five years of development. Co-founders Käärmann and Hinrikus remain the biggest shareholders, together holding just below a third of Wise shares.

Figure 1

Wise’s main funding rounds and lead investors

Figure 2

Shareholdings at time of Wise’s direct listing

Summary of Coverage

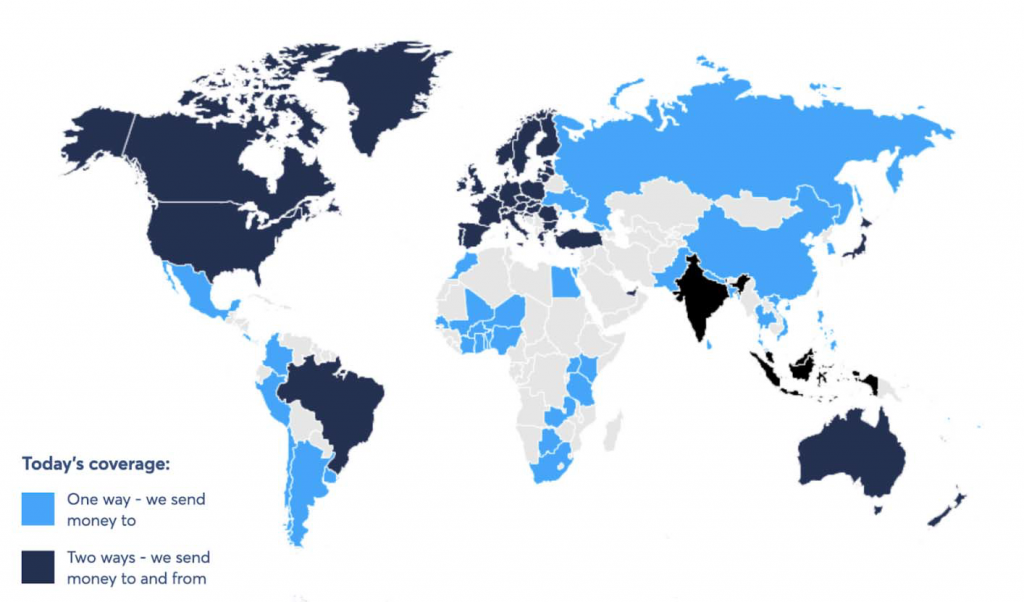

Wise supports the sending of money to over 80 countries, with over 85% of bank accounts worldwide supported by its service. Its multicurrency account allows customers to add money in 19 different currencies, receive money in ten currencies and hold money in 56 currencies. It also supports local payments in 30 countries. Its debit card can be used in over 176 countries. Wise’s platform business (powering banks and fintechs) had an annualised volume of £1bn as of 31 March 2021.

Figure 3

Wise’s transfer network

Wise’s network includes:

- Local processing in 88 countries

- Partnerships with 85 local financial institutions

- Local account details in 10 currencies

- Card issuance partnerships with Mastercard and Visa

- Cloud-based global connection with VisaNet

Regulatory

As of June 2021, Wise holds 62 licences across 11 different countries, supporting 2,500 foreign exchange routes.

User Experience

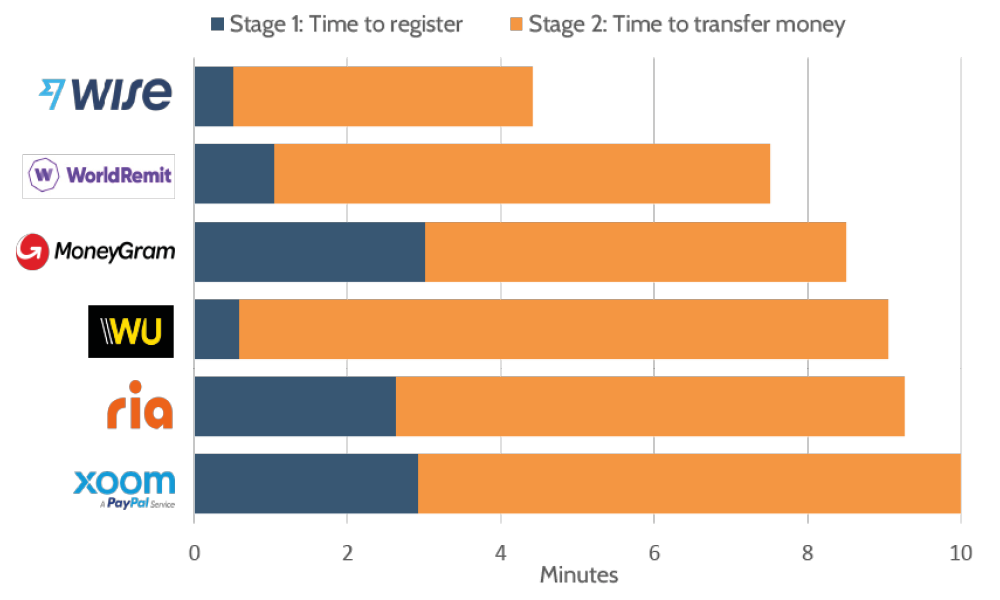

User experience is a core focus of Wise’s offering, and our own Benchmarking Remittance Apps series found that the company’s money transfer product outperforms competitors on a number of useability benchmarks.

Figure 4

Time to register and complete first transfer

How Wise’s app compares to competitors

Fastest to sign up and transfer money:

- Wise

- WorldRemit

- MoneyGram

Least amount of signup information to make a transfer:

- Wise

- Xoom

- WorldRemit

Least amount of recipient information to make a transfer:

- Wise

- Western Union

- Xoom / Ria

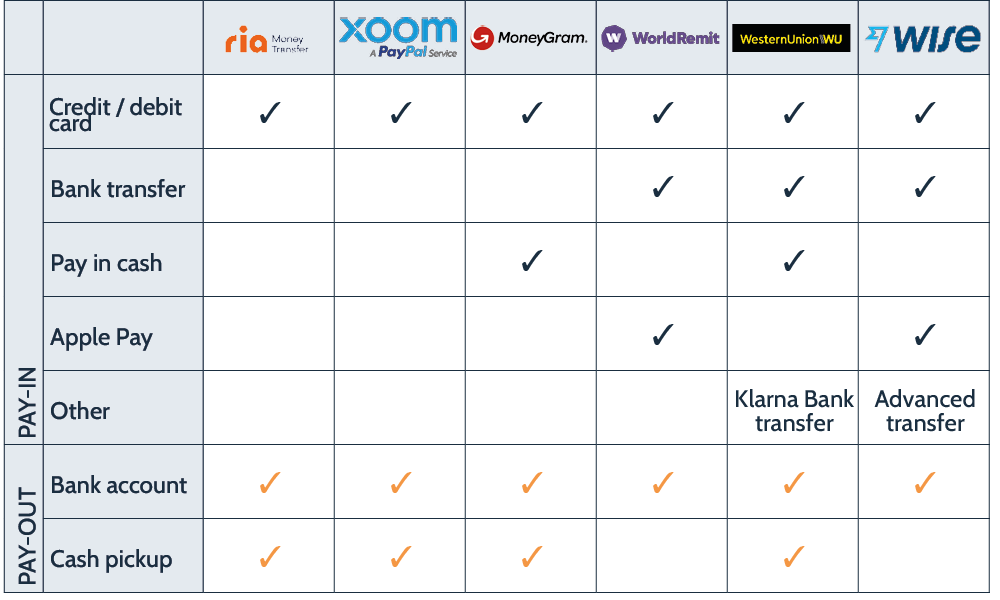

In terms of pay-in and pay-out options, our research found that Wise has some of the broadest coverage of options, with the big exception that it does not support cash.

Figure 5

Pay-in and pay-out options offered by remittance apps for example of UK to France

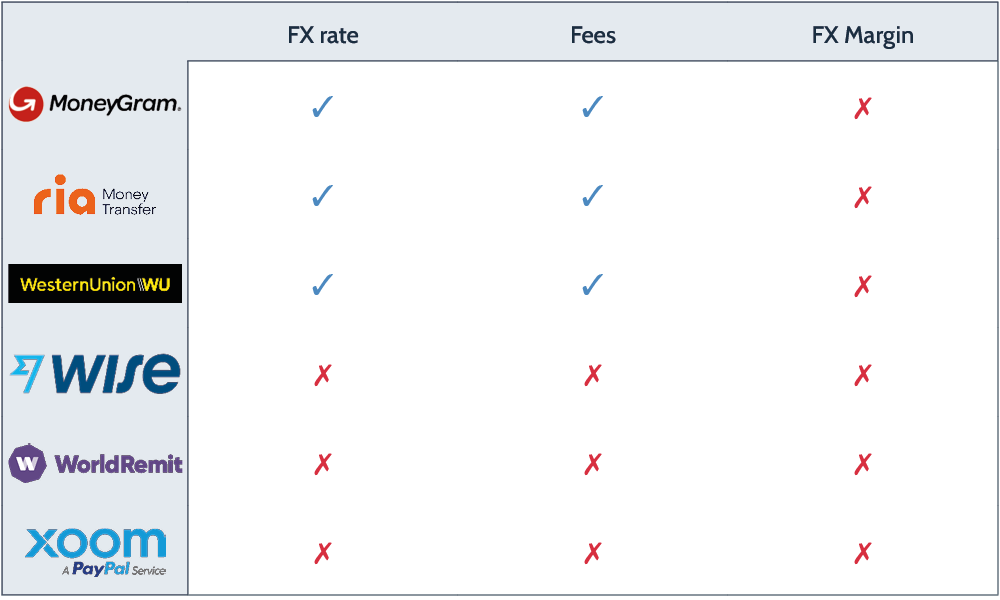

The company also includes transparency-focused features, such as alerting customers when a competitor is cheaper for a particular corridor. However, it does require customers to sign up in order to check FX rates and fees, unlike some competitors.

Figure 6

Ability to check the FX rate and fees prior to signup

Figure 7

The ‘How Wise Compares’ feature

Key User Experience Questions

How will Wise be able to maintain a lead over competitors for its user experience, or will the gap continue to narrow?

Will Wise need to broaden its pay-in or pay-out offerings to drive growth?

What will be the next big innovations in improving the cross-border payments customer experience?

Speed

The speed of its money transfers is a key part of Wise’s user experience, with over a third of transfers arriving instantly, and over 80% arriving within a day. The company’s own data shows it has made steady improvements in this area, and our benchmarking suggests that it offers an edge over its competitors on speed.

Figure 8

Time for funds to arrive in the beneficiary account (debit card pay-in method to bank account pay-out) for UK to France corridor

Figure 9

Time taken for money transfers to arrive, 2018 – 2021

Key Speed Questions

Will speed become more important than price as a differentiator?

How far will Wise be willing to go and what will it be prepared to invest to deliver instant payments globally?

Will its speed offering drive the growth in Wise for Banks?

Key Wise Financial Metrics

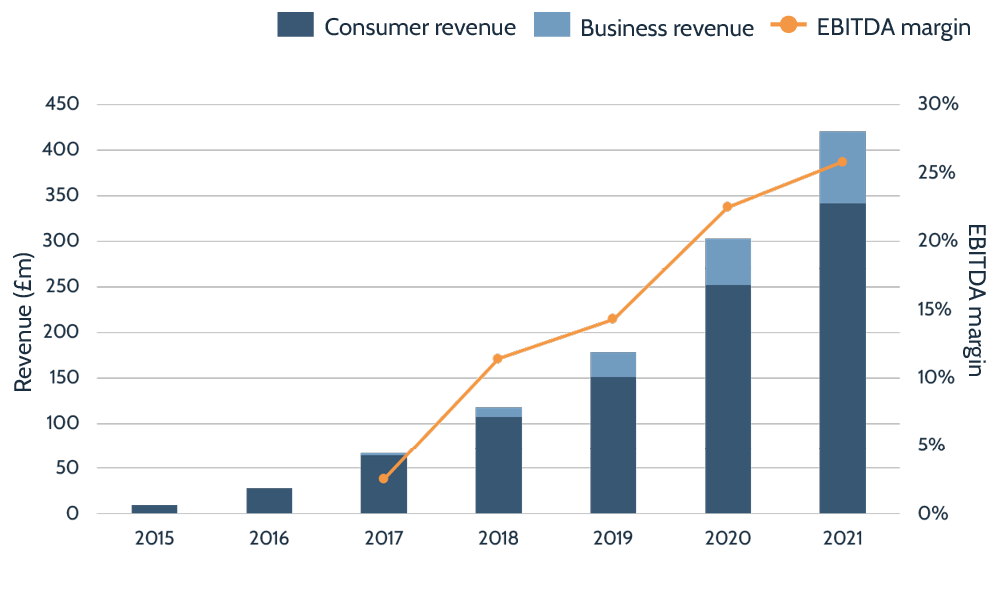

Wise sees consistent strong growth, although growth rates slowing

This is the path that has led the company to being able to do a direct listing – it has been profitable for several years, has grown since and is now building strong positions in both consumer and business.

Figure 10

Wise Historical Revenues

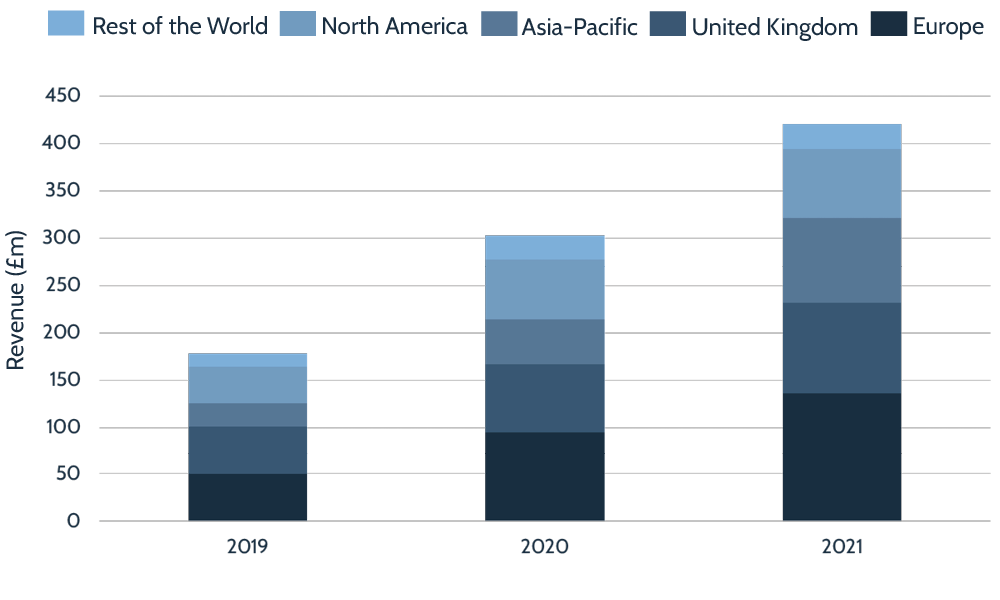

Wise has diversified its geographic revenue

Starting from a UK base in its early years, Europe and the US came next with Asia-Pacific now the fastest growing part of the business.

Figure 11

Wise revenue by region

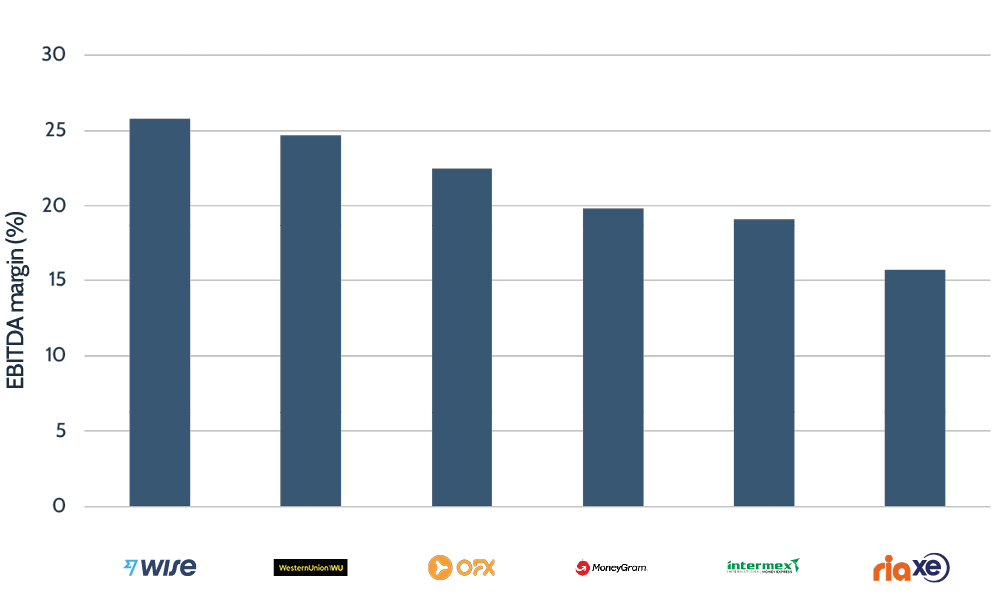

Wise leads on EBITDA margin

Wise’s EBITDA margin compares favourably to established money transfer players, ahead of leading incumbents including Western Union and MoneyGram.

Figure 12

EBITDA Margin

Key Financial Metrics Questions

Will Wise need to spend more on marketing to drive more growth?

Which regions will Wise’s next 100% of growth come from?

How will competitors respond in the second 10 years of Wise’s development?

Wise’s Consumer Offering

Wise has gained a large share of the consumer market

Wise has seen consistently strong revenue growth in its consumer segment over the past few years, which has outstripped most of the competition. Wise is forecasting growth of c.20% going forward as its scale makes it harder to grow share.

Figure 13

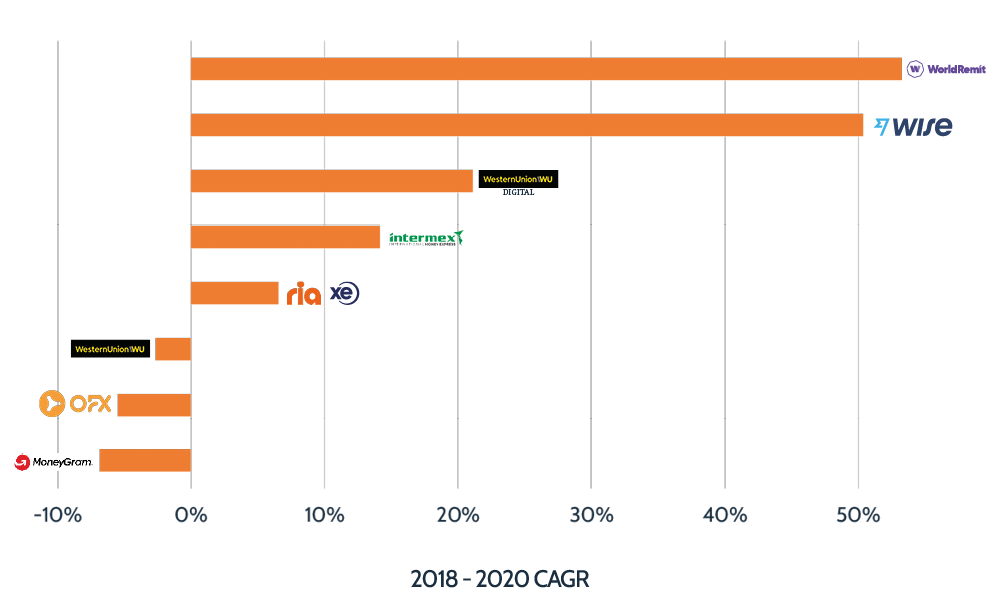

Growth rates – consumer: 2018 to 2020 CAGR

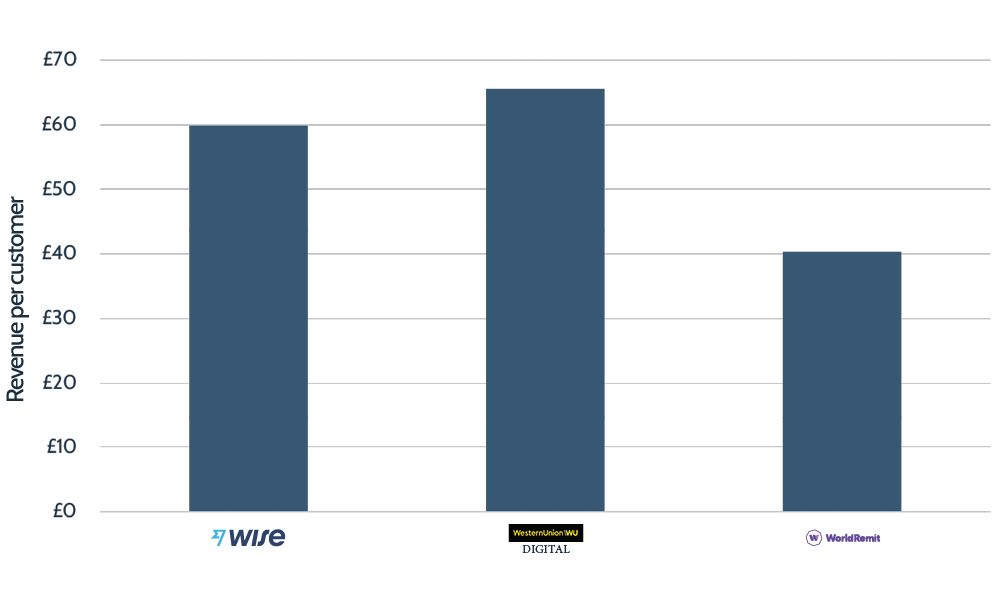

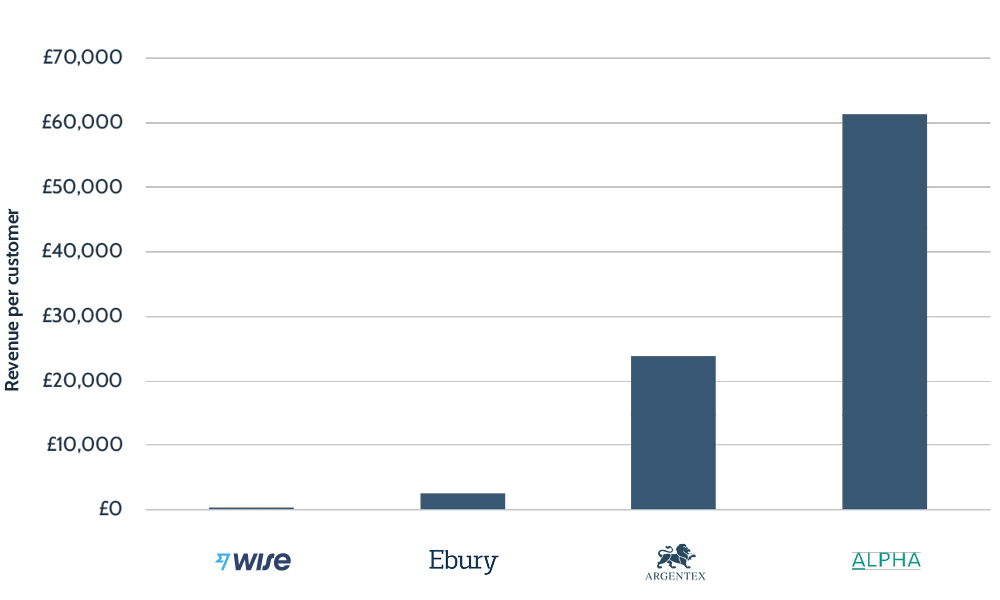

Wise has strong per consumer revenue metrics

Despite having a significantly lower take rate than its consumer competition, Wise’s revenue per consumer customer is in line with other players in the market, indicating it is transferring a higher average transaction value than some of its rivals with much higher take rates.

Wise’s multicurrency wallet offering called its Borderless account has helped support this customer growth with. Wise has issued more than 1.6 million debit cards and customers held £3.7bn in deposits as at 31 March 2021.

Figure 14

Annual revenue per customer – consumer

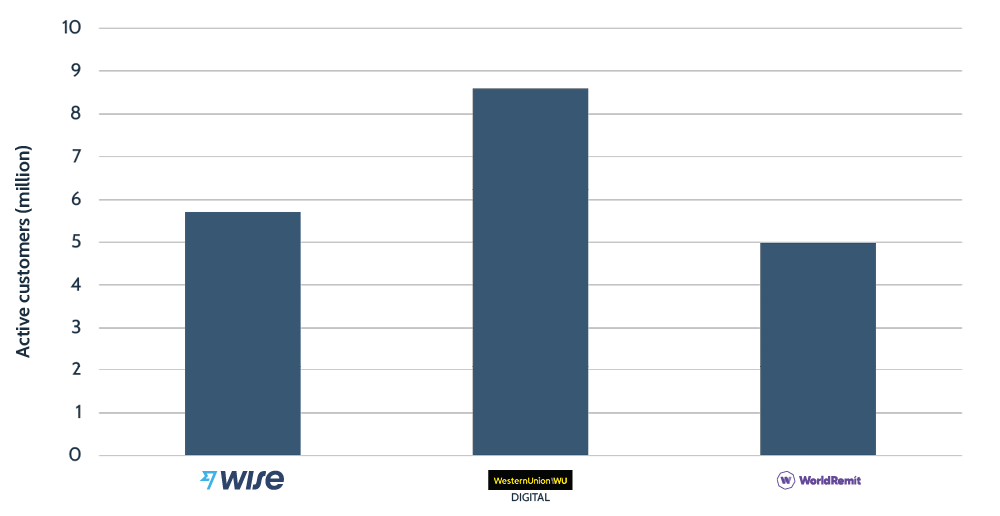

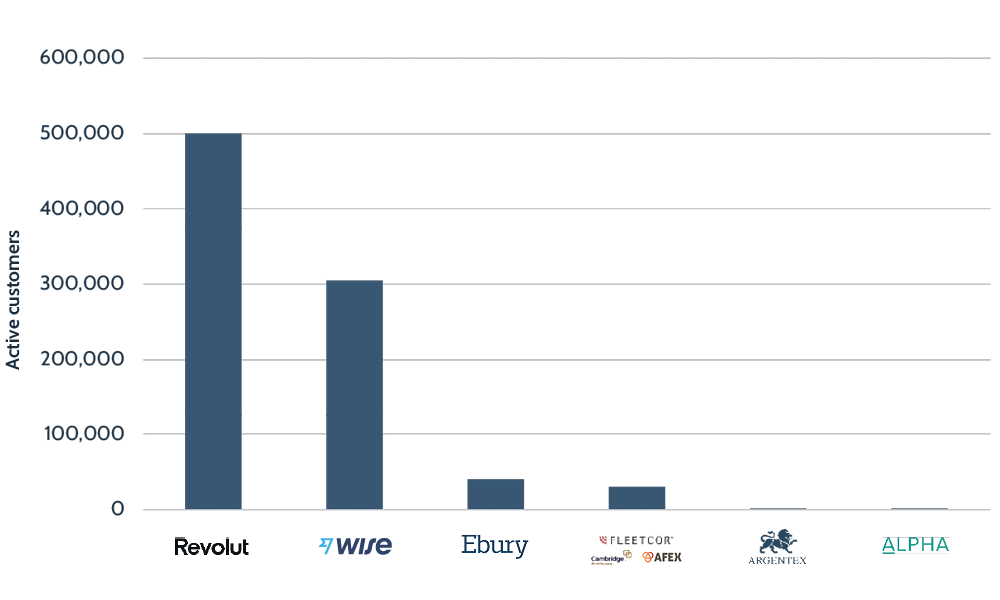

Active customer numbers challenge but don’t lead the sector

Wise is not yet the biggest player in digital money transfers, with Western Union’s digital business remaining bigger. However, it is a strong presence in the market.

Figure 15

Active customers – consumer

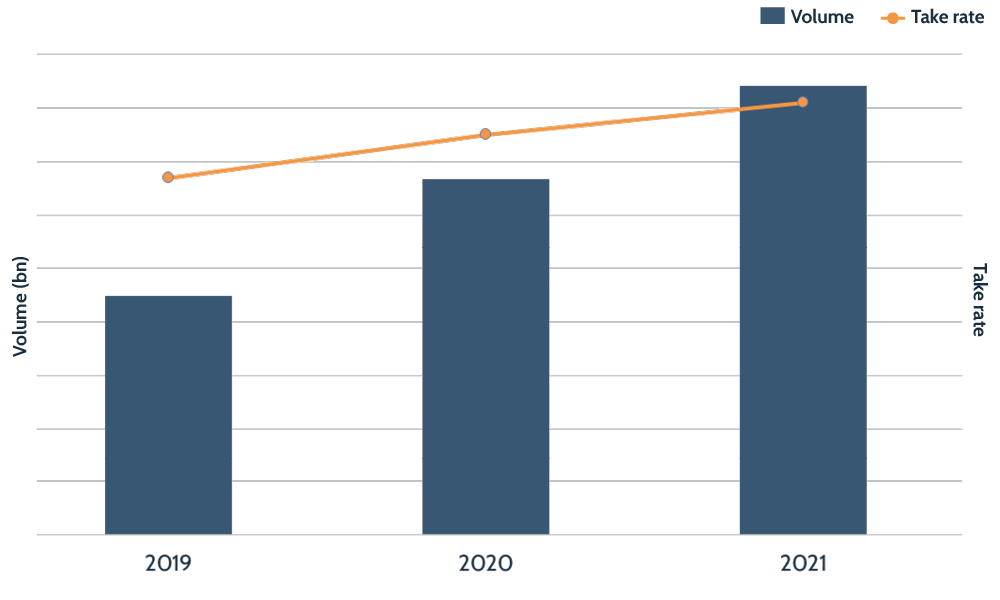

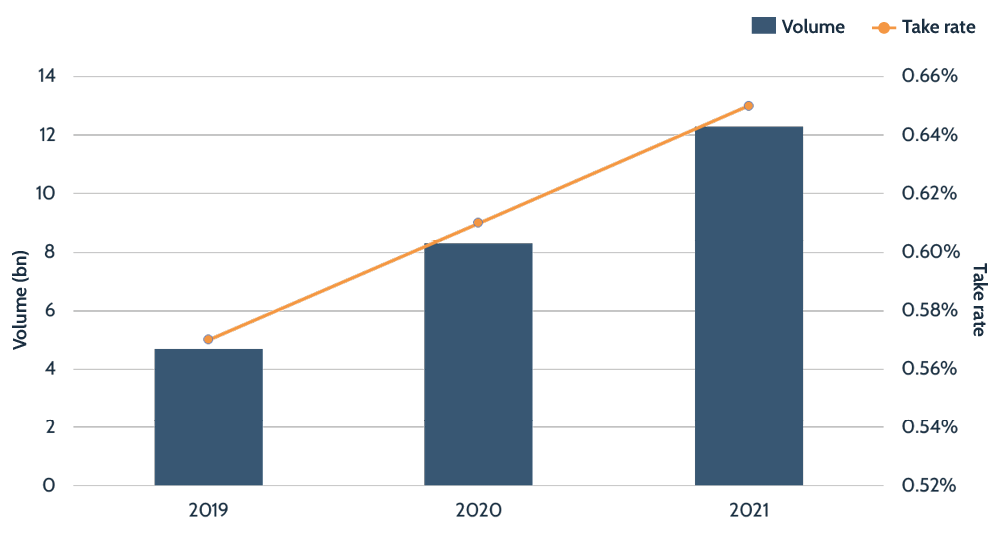

Wise’s take rates have been steadily climbing

Expansion into more exotic corridors plus a desire to make a profit have lead to the overall take rate rising.

Figure 16

Take rate and volume growth by year – consumer

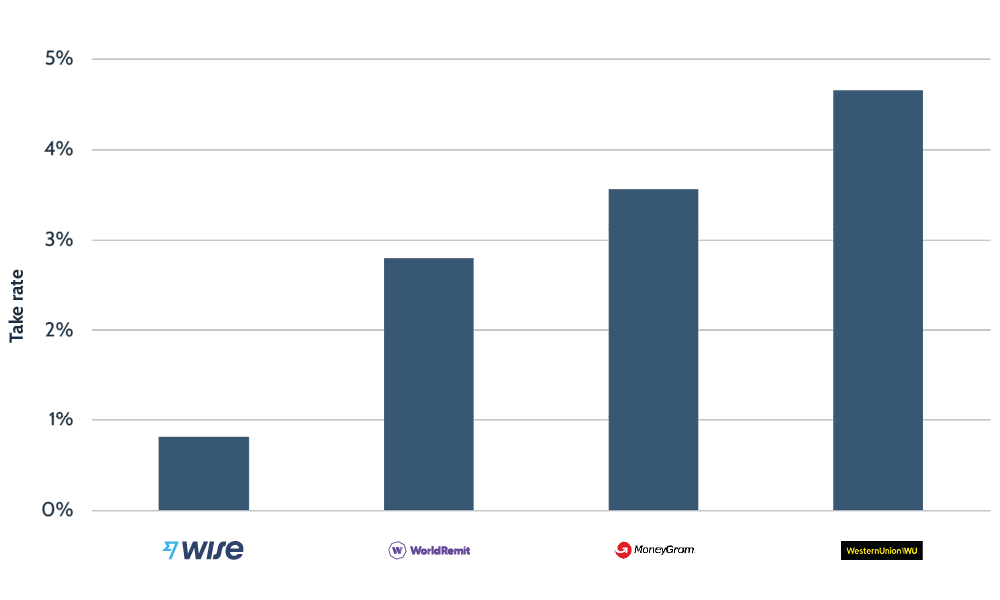

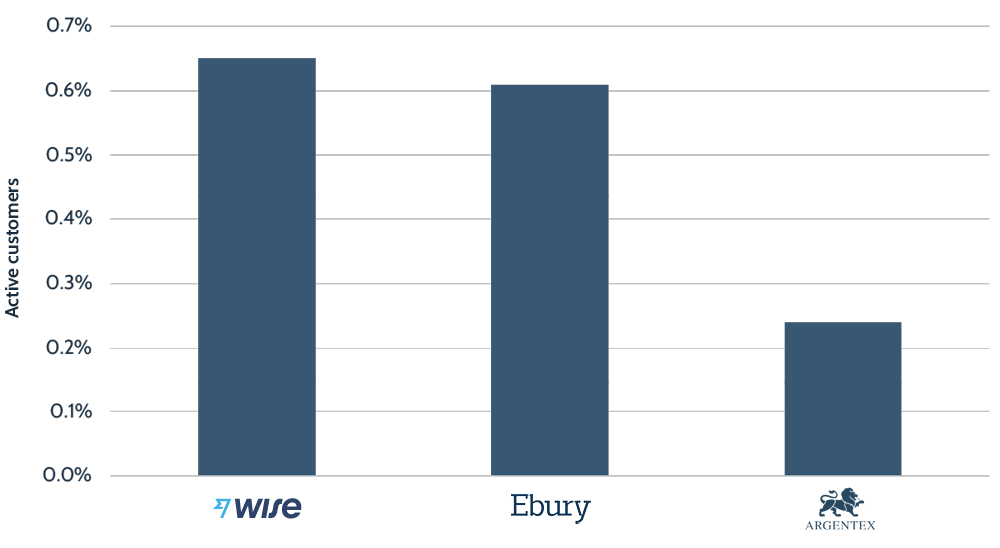

Wise’s low take rate (low price) has been a pillar of its strategy since the beginning, aiming to be 8-10x cheaper than the banks

Wise has won market share with its low pricing and in the early days splashy PR and marketing campaigns highlighting differences to the banks. Whilst it’s take rates are much lower than the traditional remittance players, its is also targeting a different customer with a much higher average transaction size.

Figure 17

Take rates: Wise versus consumer competitors

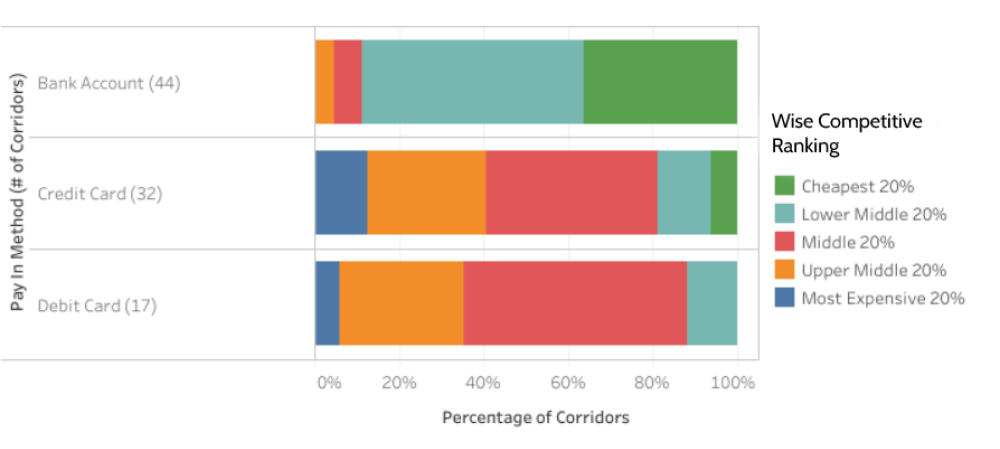

Competition is fierce in the sector. Whilst Wise is often one of the cheapest for bank to bank account transfers, for card-based pay-in methods, others are more competitive

Every pay-in and pay-out method requires infrastructure and investment to be the cheapest and fastest offering. Wise is typically very competitive on bank to bank transfers but cards can be much more costly and others players are more competitive. The example below for Singapore shows how challenging the market is.

Figure 18

Wise’s Market Positioning for Singapore

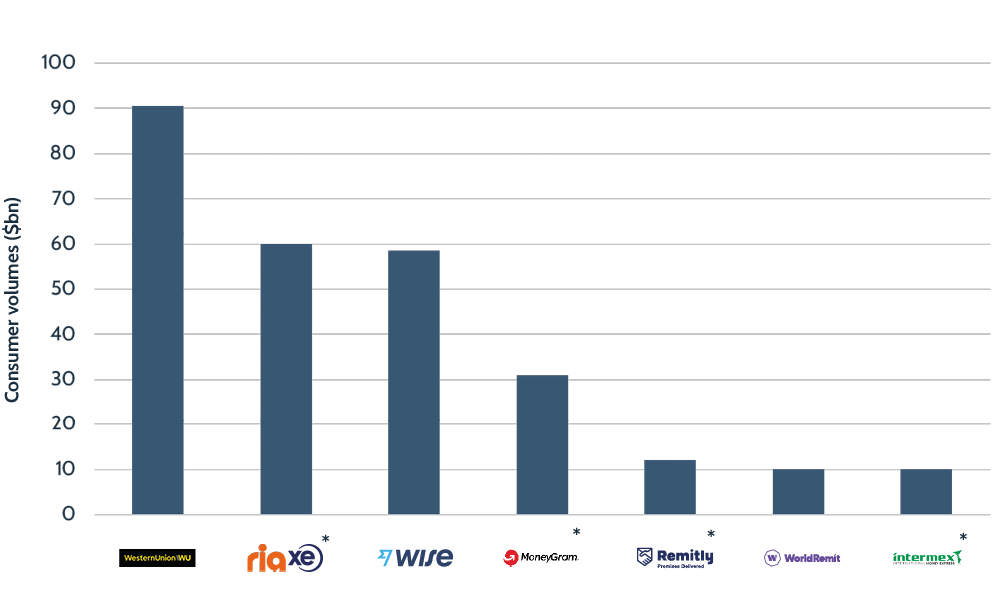

Wise has built up significant consumer volumes

Wise has one of the highest volumes among its competitors, but it isn’t the leader, with both Western and Euronet’s Ria and XE seeing higher. However, its volumes are significantly higher than other digital-first competitors.

Figure 19

Consumer cross-border volumes by competitor

Key Consumer Questions

How will Wise balance low-customer pricing versus driving profits as a public company?

How important is the borderless account in driving customer growth?

What additional products will be needed to continue to drive customer growth?

Wise’s Business Offering

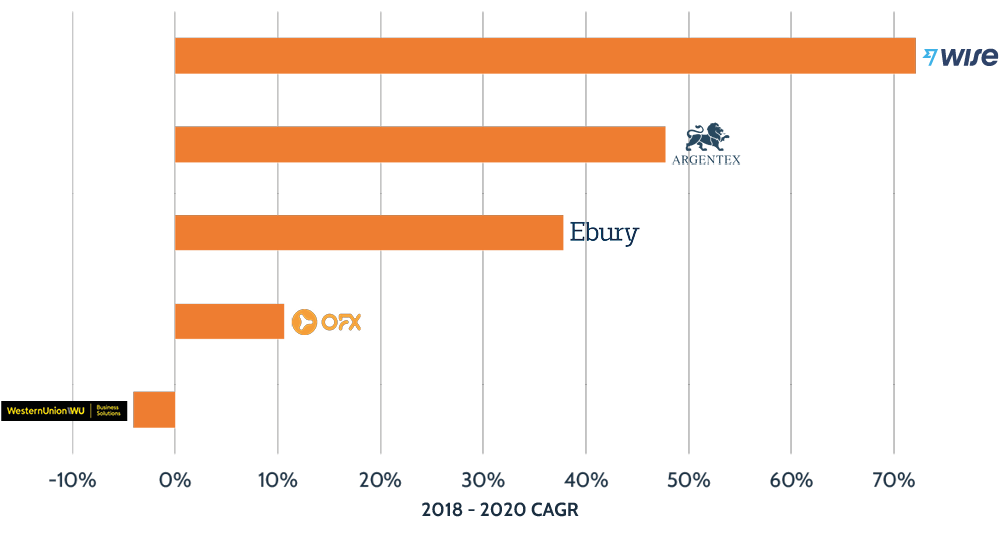

Wise has quickly built a business presence

Although still a relatively small part of its overall business, Wise’s business revenue has grown significantly over the past few years, outstripping its competitors and growing at a faster rate than its consumer segment.

Figure 20

Growth rates – business: 2018 to 2020 CAGR

Relatively low revenue per customer speaks to the micro and small businesses being targeted

Wise’s revenue per business customer is only a very small fraction of its competitors, despite it seeing strong revenue growth in this segment. Competitors in the corporate space typically have much deeper product offerings, ranging from hedging services to credit-based products and targeting bigger business customers.

Figure 21

Annual revenue per customer – business

Wise has large numbers of small business clients

Despite having relatively low revenue per customer in its business segment, Wise is one of the biggest in terms of active business customers, outstripped only by Revolut. It is similarly targeting the needs of smaller businesses who also have simple requirements and require far less direct account management.

Figure 22

Active customers – business

Wise’s take rates have been steadily climbing

As with consumer, expansion into more exotic corridors plus desire to make a profit have lead to the overall take rate rising.

Figure 23

Take rate and volume growth by year – business

Wise’s pricing for businesses is much more in line with the competition

Wise (like many other corporate-focused players) focuses on being much cheaper than the banks. This and its user experience help it win business customers – although for now, Wise is very much focused on the smaller end of the market.

Figure 24

Take rates: Wise versus business competitors

Key Business Questions

Will the unit economics continue to make sense targeting micro and small businesses?

Will Wise be able to attract significant numbers of larger corporates?

What changes to Wise’s product and account management/sales offering would be required to onboard larger corporate customers?

Wise’s Valuation and Revenue Multiples at the Time of its Direct Listing

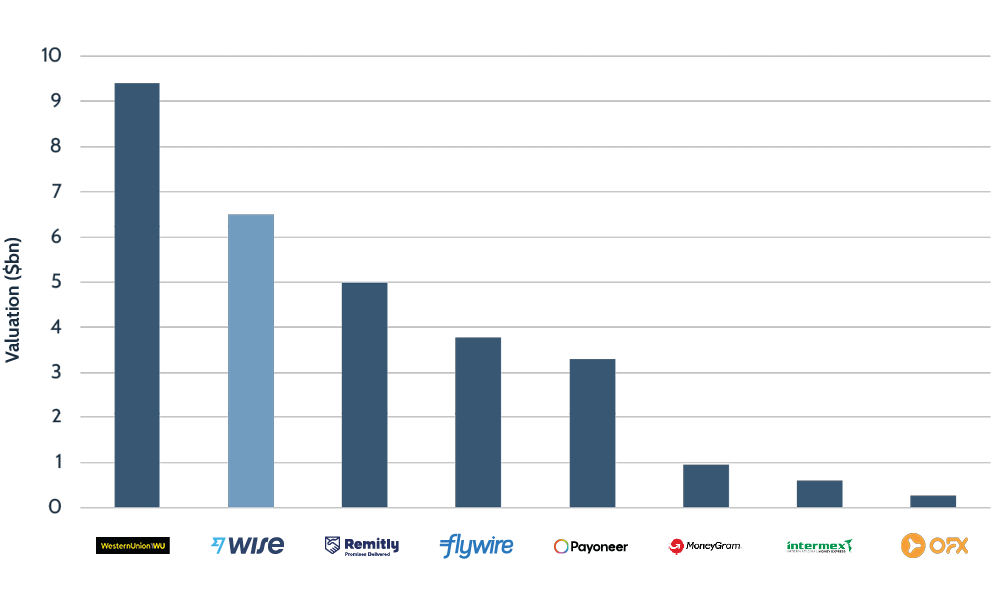

Wise’s direct listing will see it become one of money transfers’ most valuable companies

The reported £6-7bn direct listing will make Wise a more valuable company than even Western Union, despite it having lower revenue and customer numbers. This reflects the value the market is placing on growth in the market.

Figure 25

Public company valuation versus competitors

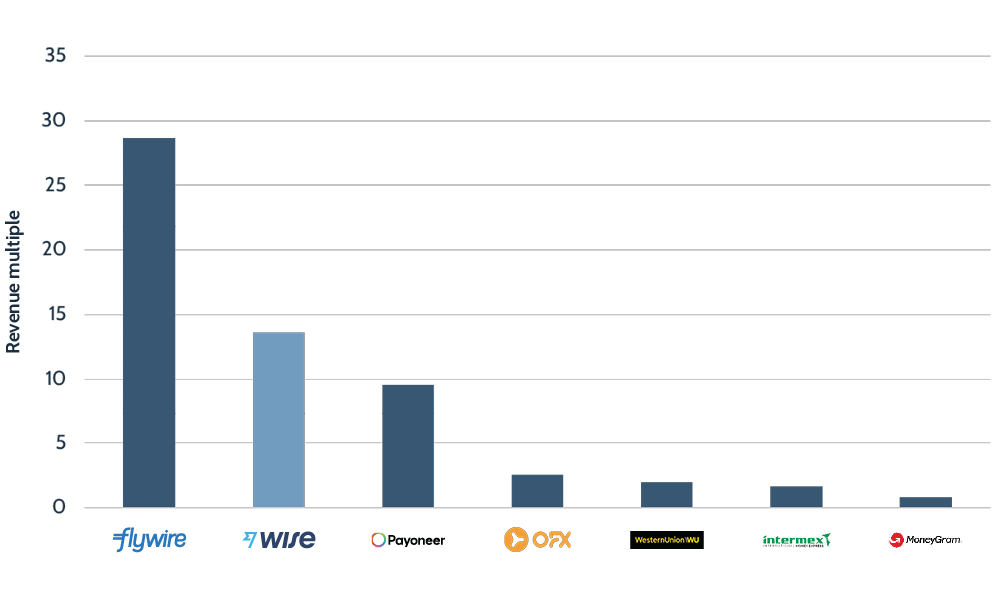

Wise’s position among fintechs on revenue multiples

When it comes to revenue multiples, the money transfer industry is clearly divided between incumbents and fintechs, the latter of which has a much higher, double-digit revenue multiple than its more traditional counterparts. Wise is no different, with strong revenue multiples but below the B2B-focused players such as Flywire and Payoneer.

Figure 26

Current year revenue multiple versus competitors

Key Direct Listing Questions

How will Wise’s direct listing be received by the market?

How will Wise’s Platform business be valued by the market?

What growth and profit rates will Wise have to continue to deliver to grow its valuation?

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.