The impact of regulations on the disclosure of cross-border card payments to consumers.

Cross-border retail payments are becoming more frequent and significant in value around the world. However, understanding the magnitude and the meaning of fees applied on cross-border transactions can be complicated.

According to FXC Intelligence’s card pricing data on more than 700 issuers across 110 countries, the cost of a cross-border transaction can eclipse 10% of the transaction amount in certain countries and for certain card programs. While cross-border ecommerce has become mainstream, the lack of transparency and the uncertainty over the final cost of the payment can prevent customers from shopping cross-border or can cause unhappiness when the costs are uncovered.

Banks, payment companies and merchants implement various methods of charging consumers for purchases made abroad or paid in other currencies. These charges vary between exchange rate margins, percentage fees on the transaction amount and fixed fees for each transaction. In some cases, mixtures of these charges can be observed.

Due to the complexity of cross-border fees and their components, there is a growing need for card issuers to disclose the cost of such transactions to the final consumer. Regulators around the world are taking steps to ensure that card issuers comply with transparency rules.

The aim of this report is to investigate what measures various regulators have taken to control the fees arising from foreign exchange transactions and to investigate the relationship between regulation and disclosure of fees by card issuers. Finally, we identify issues that still need to be addressed so that consumers have a clear understanding of the fees that will be charged.

Cross-border card payment regulations: Key takeaways

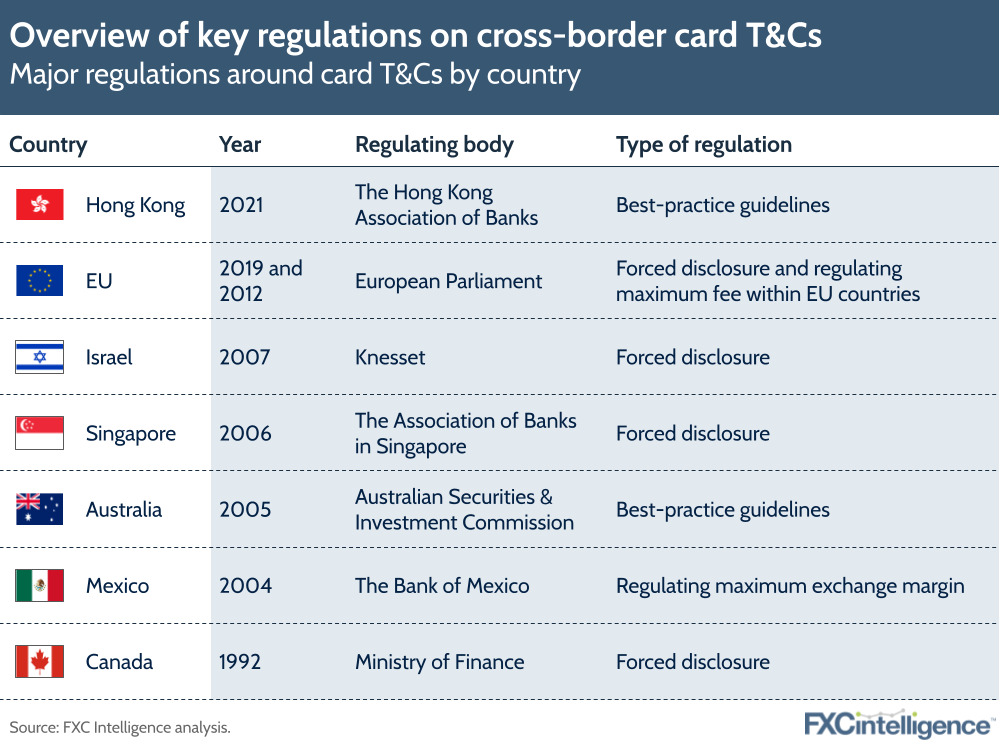

Regulators around the world are taking very different approaches when it comes to regulating the cost of cross-border transactions. While in some jurisdictions such as Mexico regulators establish caps on the amount that can be charged for cross-border transactions, other countries such as the EU, Singapore and Israel dictate standards of disclosure on cross-border payments’ costs that are binding for card issuers. Finally, there are countries where only best practices are published by regulators, or where transactions involving foreign exchange are not regulated at all.

From our analysis, regulation alone is not a good proxy to determine how transparent issuers in a given country are when it comes to the cost of cross-border transactions. While the disclosure of terms and conditions (T&Cs) for cross-border card transactions is higher in countries where binding regulations exist, there are also cases such as Hong Kong and Australia – where no binding regulations on cost disclosure exists – that still have a high proportion of card issuers presenting clear-cut costs to their customers.

Our data comparing costs from real cross-border card transactions and costs disclosed in the T&Cs also shows that T&Cs tend to either underestimate or overestimate the cost of real transactions. This means that consumers are still going to be faced with unexpected costs, which might come from card networks, the government via taxes or through hidden fees that are unreported by the card issuer itself.

Helping consumers understand the economics behind cross-border card payments is essential for card issuers and card networks. Breaking down the components of the final cost charged beyond the scope of existing regulations, if any, only provides benefits. The number of customer complaints will decrease. Usage of cards for cross-border payments will also increase if consumers are aware of any costs beforehand and so are not scared of being charged excessively. This provides the card issuers and networks with incremental revenue opportunities.

Figure 1

Foreign exchange legislation and the impact on the availability of T&Cs

To avoid transparency issues and improve customers’ protection, countries have introduced a variety of measures, which range from formal regulations to guidelines. In some cases, coercing regulations, which force issuers to disclose certain information regarding foreign exchange fees are implemented.

Other countries have issued suggestions for issuers to guide them on which information they should publish in order to boost transparency for their customers, while many countries still have no regulation regarding the disclosure of FX fees.

In the following sections, we’re going to explore what these various levels of FX fee regulations mean, and in which countries these are applied.

Regulating fee amounts

The most direct way of influencing the ability of institutions to set fees is by directly regulating how high they can be. This can either be done by setting a numerical limit to how high fees or margins can be or by limiting the fee through another benchmark. We have found two examples of this sort of regulation, namely in Mexico and the EU.

In Mexico, most issuers have no fixed or percentage fees, but rather charge a margin on the exchange rate. Paragraph 13 of the rules for banking institutions and limited purpose financial companies issued by The Bank of Mexico states that when conducting the conversion, the card issuer must not charge an exchange rate that is more than 1.01% above the daily exchange rate between the USD and Mexican Peso set by the Bank of Mexico. For the bank to have the right to charge a fee, that fee needs to have been disclosed in advance when signing the contract in the T&Cs.

In the EU, Regulation (EU) 2019/518 does not put a numerical limit on the costs of transactions but they do, within the EU, force issuers to charge the same fees domestically and internationally within other EU countries. This applies to all foreign transactions within the EU in Euro, as well as transactions in currencies of member states that have extended the application of the regulation to their national currencies. Fees for card transactions outside of the EU do not fall under the EU’s regulations.

Regulating disclosure obligations

Another form of regulation that is frequently implemented concerns what information must be made available to customers when signing contracts with the card issuer. While customers are not protected by regulation from high exchange rates, they have the ability to gauge the fees beforehand and decide whether incurring them is acceptable.

EU regulations require card issuers to inform their customers of any fees they will encounter when performing FX transactions or paying in their card currency while abroad as part of their T&Cs. Card issuers usually provide this information in T&C documents that are publicly available, but also disclose this in their contracts when accounts are created or cards are requested.

In Singapore banks must inform customers of the following fees relating to FX transactions when dispatching payment cards: how fees are calculated and whether they are imposed by the bank or by the card network, administrative fees, commission fees and any other charges relating to FX transactions.

Similarly, banks in Canada must display all charges relating to banking accounts online and upon request. Although not specifically stated, this may also apply to bank account maintenance fees as well as card fees.

In Israel, banks must disclose all card fees that are applied in various cases to the user of the card. This includes fees applied when using the card abroad, paying in either card or foreign currencies, as well as fees on international withdrawals at ATMs and other fees, such as account maintenance expenses. While The Supervisor of Prices at the Ministry of Industry, Trade and Labor has the right to supervise certain bank commissions, fees on cross-border transactions do not fall under this category and the government has no control over how high the charged fees are.

Best-practice guidelines

Some countries do not regulate the fees or what banks need to disclose, but their governing bodies provide best-practice guidelines that issuers seem to, at least to some extent, follow.

In Australia, the Australian Securities and Investments Commission (ASIC) provides an elaborate report, which includes suggestions when customers should be made aware of any fees. This includes informing the customer of fees when the account is opened, when there are any changes to fee levels, before transactions are concluded and whenever the customer requests this information.

In Hong Kong, the Hong Kong Association of Banks provides a document with best-practice guidelines. They suggest that issuers should make the details of the fees and charges associated with services readily available and provided upon request. They also suggest that fees should be of reasonable amounts, however do not provide any indication of what a reasonable amount is.

No regulation for FX

In many other countries there is no regulation regarding foreign exchange transactions. In some countries, such as Argentina, governing bodies do regulate some fees, but do not regulate FX fees themselves. Similarly, in China, while ATM fees, agency fees and maximum interbank fees are defined, there is no regulation surrounding foreign exchange fees.

In other countries such as Russia there is no regulation that discusses how banks should disclose fees.

A look at the data: The impact of regulations on cross-border card payment T&Cs

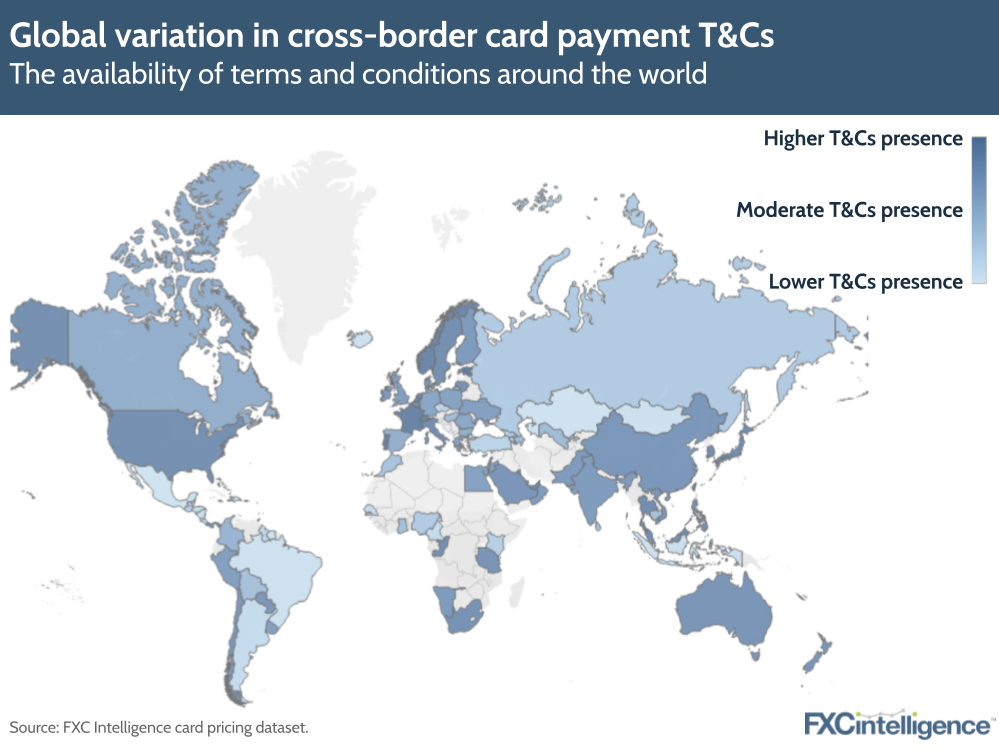

Do regulations really boost T&Cs presence?

As can be seen from the figure below, countries where regulation exists generally have high to moderate availability of online issuers’ T&Cs. EU countries have high availability of T&C documents, as do New Zealand and Israel. Canada has moderate availability of T&Cs.

Regulation, however, does not seem to be a requirement for high T&Cs availability. Countries such as India, USA, Japan and China, where we were unable to find relevant regulation, still maintain high rates of online T&Cs. Additionally, in Australia and Hong Kong, where there are only best-practice guidelines, online T&Cs availability remains high. In Russia most banks do not disclose fees and charge exchange margins on transactions.

In Mexico, on the other hand, while the exchange margin is regulated, there is no requirement for issuers to publish fees on FX and cross-border transactions, and this reflects in the low availability of T&Cs.

In areas of Latin America, Central Africa and Central Asia the availability of T&Cs is lower compared to the rest of the world.

Figure 2

Find out how FXC Intelligence’s card pricing data can help your business

Comparing issuers’ T&Cs with the real cost of FX transaction

T&Cs do not necessarily convey the full picture when it comes to the cost of FX transactions. The cost of such transactions is made up of several components, only one of which is the FX fee that is usually disclosed in the T&Cs of a bank.

In addition to the FX fee, customers may also be charged a margin on the exchange rate by the card network (Mastercard, Visa, Amex etc.), by the bank or through taxes applied by the government. While T&Cs sometimes break down these additional costs, most of the times they are not stated and may surprise customers.

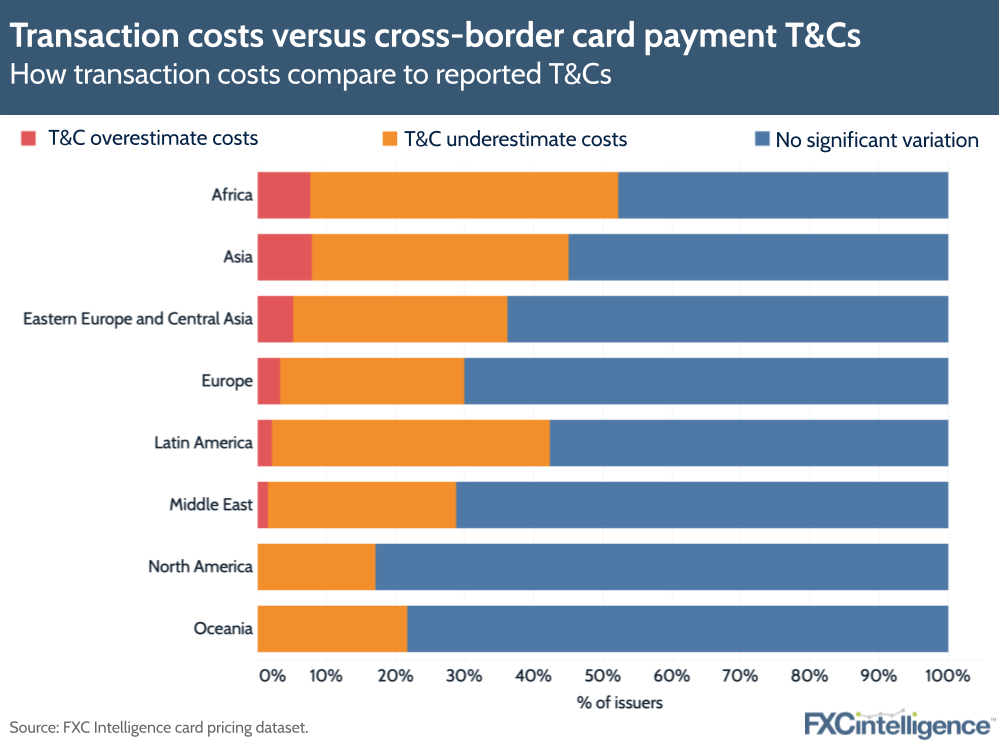

Figure 3

When comparing the data collected through T&Cs and from real transactions, we have concluded that while for 53% of issuers in our dataset there is no significant difference between the cost from real transactions and T&Cs, for 38% of issuers real transactions showed significantly higher fees than what was reported in the T&Cs.

Only 8% of issuers’ real time transactions have lower fees than what the T&Cs suggested. The average transaction was 0.68% higher than what was expected according to the T&Cs.

The regional perspective

The T&Cs are most precise in North America and Oceania, where 75-80% of T&Cs accurately convey total fees, while only around 20% of cases are transactions higher than what is stated on T&Cs. In Oceania, 4% of issuers overestimate total fees in their T&Cs, however we have not found such cases in North American issuers.

In Europe and the Middle East, around 60% of issuers have no significant variation between T&Cs and transactions. 33-36% of transactions are higher than what T&Cs suggest and in 3-5% of transactions T&Cs have indicated higher fees.

In Asia and Latin America 54% of transactions have no significant variation, while 38-44% have higher transaction costs than what T&Cs suggest. In Asia around 8% of transactions have lower costs than the T&Cs, while in Latin America that number is only around 2%.

Finally, the lowest percentage of accurate T&Cs is in Africa, where only 46% of T&Cs accurately convey transaction costs, while another 46% are issuers where costs of transaction exceed what T&Cs suggest. The remaining 8% are transactions which are lower than what is stated in their T&Cs.

The example of Mexico

Are fees compliant with regulations?

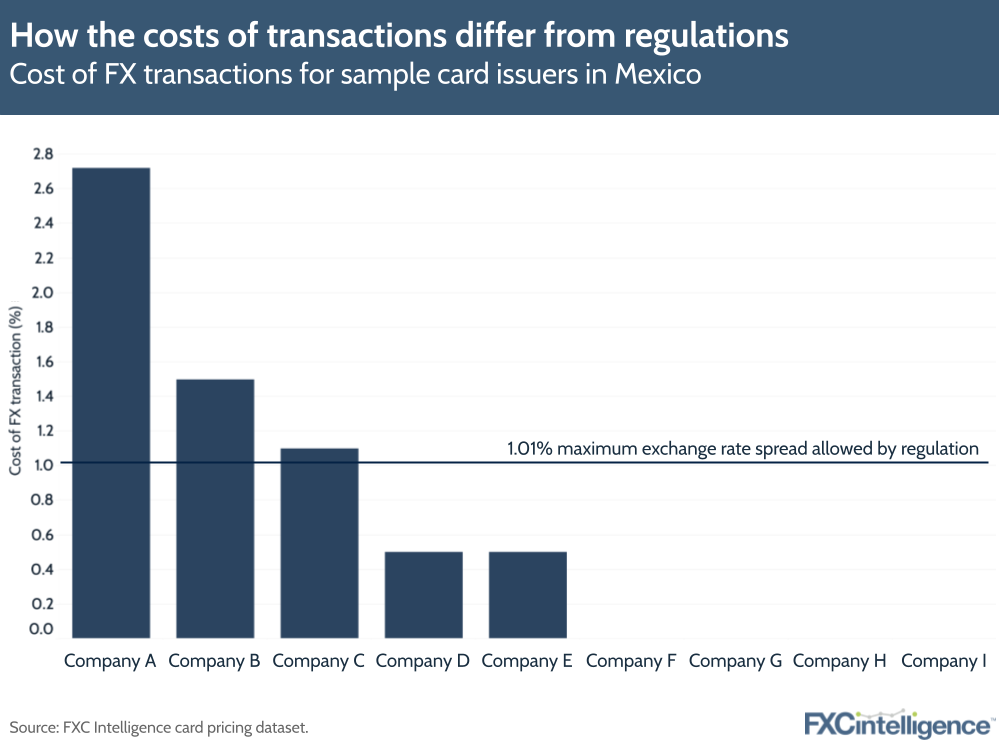

Mexico is one of the few countries in the world that provides a clear cut number for the maximum exchange rate spread that issuers are allowed to apply. However, as the example below shows, even regulations providing Regulating Fee amounts might not be enough to put a real cap on cross-border transaction costs.

In addition, the need for the card issuer to disclose the cost of cross-border transactions is not mentioned in the regulation. This provides room for additional costs to be charged on top of the amount stated in the regulations, on the part of both the card issuer and other parties involved in the processing of the transaction such as the card network.

Figure 4

Of the nine issuers that we have collected in our card pricing dataset, three apply charges that are higher than the 1.01% threshold indicated in the regulation. What this means is that there are definitely alternative sources of costs for cross-border transactions. T&Cs or regulations alone cannot explain the final cost charged to the consumer.

Disaggregating cross-border charges

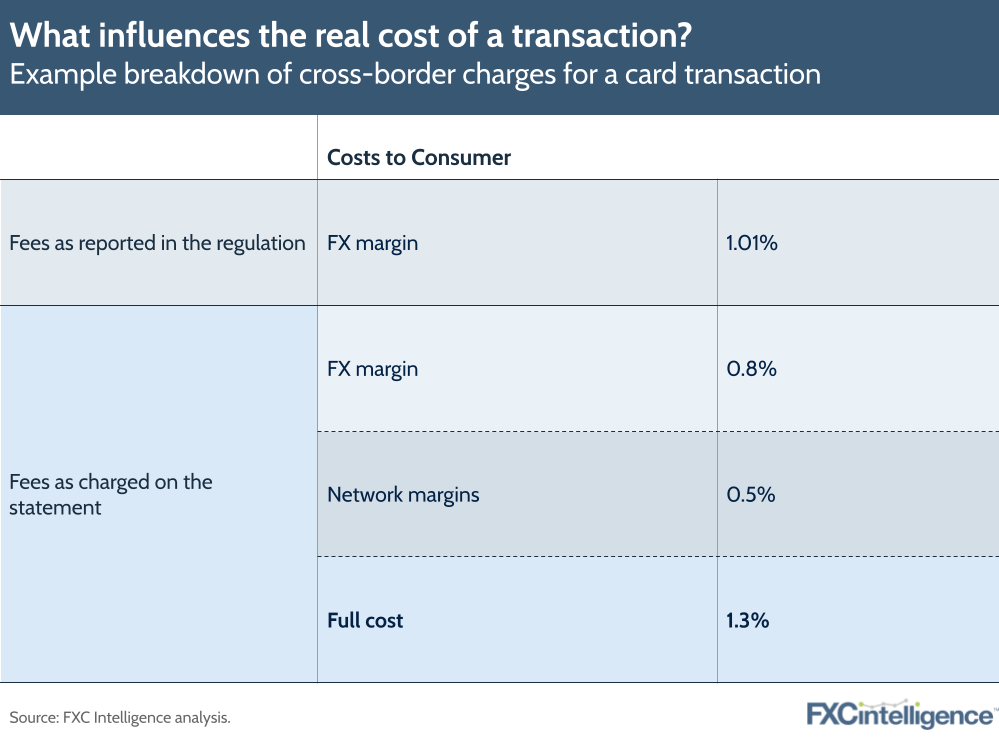

This example illustrates what are the components of cross-border charges. The card issuer reported in this example does not publish T&Cs publicly. The total fee for this transaction was 1.3%, which exceeds the 1.01% margin regulated by the government.

Figure 5

However, when we break the transaction down we can see that the transaction margin at the point of transaction was only 0.8%, which is in line with the regulation and that a further 0.5% was charged by the network provider.

In this case, while the bank is both in line with government regulation and can claim not to charge “additional” fees to customers, the cost of the transaction is still fully passed onto the customer and they have to pay a charge 1.3% for the service.

Conclusion

Our research has shown that the degree of regulation on cross-border payments around countries varies widely and that, where existent, regulations influence transparency and transaction costs in several ways.

While regulation is not mandatory to have a high degree of T&C availability in a country, having regulation drives the availability of T&Cs upward and allows customers to be better informed about the costs that they will incur. However, since there are several components to each foreign transaction fee applied by different players such as the card issuer, card networks and the government, regulating just one aspect may not be enough to avoid high charges and confusion for the end consumer.

This implies that simply looking at the T&Cs is often not enough to accurately gauge how high the total fees will be in the end. Our data comparing the real cross-border card transactions and costs disclosed in the card issuer’s T&Cs shows that T&Cs tend to either underestimate or overestimate the cost of real transactions.

Our example on Mexico reinforces the fact that card issuers’ T&Cs and regulations aimed at the fees charged by the card issuer alone are not enough to describe the real, final cost of a cross-border transaction. There are other players and several steps involved in the processing of a card transaction, which might have a significant impact on the final cost.

Presenting customers with a clear description of the economics behind cross-border card payments comes at a cost for card issuers and card networks. However, the benefits are likely to overcome such costs.

The number of customer complaints will decrease while the usage of cards for cross-border payments will increase if consumers feel more informed and safer about the costs they’re going to be charged. This provides the card issuers and the networks with incremental revenue opportunities, making increased clarity a key opportunity.

Find out how the card pricing data used in this report can help your business