Rapyd’s acquisition of PayU GPO for $610m sees it move further towards its goal of “creating the world’s largest global fintech”. We spoke to CEO Arik Shtilman to find out more about the acquisition and how it feeds into Rapyd’s wider strategy.

At the start of August, B2B-focused fintech-as-a-service player Rapyd announced that it was acquiring PayU’s Global Payments Organisation (GPO) unit for $610m.

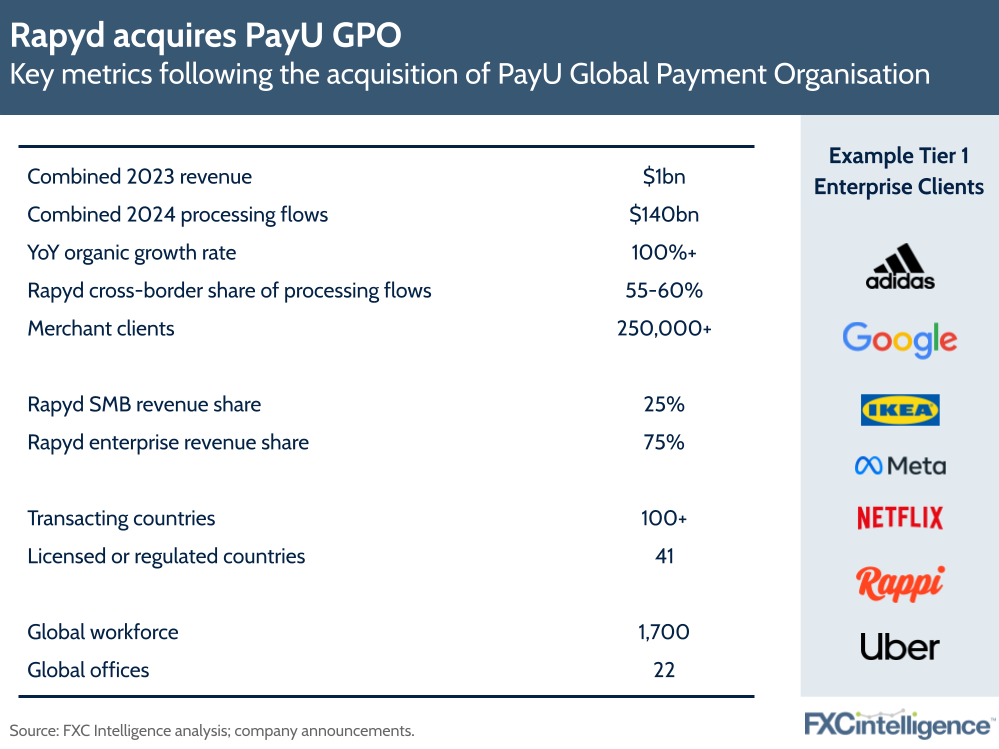

This sees Rapyd acquire the payments fintech business of global consumer internet group Prosus, excluding its operations in India, Turkey, and Southeast Asia, which provides SMB and enterprise payment solutions in over 30 countries globally.

For Rapyd, the emerging markets-focused PayU GPO provides key strategic additions globally, particularly in Central and Eastern Europe, as well as Latin America. With the acquisition, the company will cover more than 100 transacting countries and over 250,000 merchant clients worldwide.

It’s a key step towards Rapyd’s stated target of “creating the world’s largest global fintech”, as well as enacting an IPO. But how is the acquisition of PayU GPO set to contribute to Rapyd’s growth, and what other steps is the company planning to take as it continues to develop? We caught up with CEO Arik Shtilman to find out.

Rapyd’s market position

Daniel Webber:

Before we get onto the acquisition, let’s talk about Rapyd’s position in the market. Where is it at present and where do you want it to get to?

Arik Shtilman:

We want to be the platform for fintech-as-a-service. So we’re trying to position ourselves as an Amazon AWS for the fintech space: an infrastructure platform that provides clients with the ability to build – on top of us – services for either consumers or businesses for collection, disbursements, issuing of cards and storing funds in individual accounts or wallets.

Basically a platform – not an acquirer, not an issuer, not a disbursement platform – but a much bigger platform for companies that are trying to build use cases that are more than collecting a payment from a card.

For example, a company in the payroll space that is trying to solve a problem for seafarers, people that work on ships. They come from a lot of different countries and the company created a product that is literally a new mobile app. The seafarers can download the app, create a virtual bank account inside it, receive their salary and issue a card that is linked to the app. From the app, they can also pay their relatives the money via wire transfers, buy airtime or pay utility bills.

When you have Rapyd, you can use the Rapyd wallet infrastructure to create the wallet to KYC the seafarer. This opens your virtual bank account. You can receive the incoming money as a salary from your employer, and then Rapyd can issue a card for you, both virtual and physical, and also Apple Pay, Google Pay, so you can actually spend the money from the wallet.

Rapyd provides you disbursement capabilities and airtime top-up capabilities so you can move the money out. This is a full infrastructure play and it’s a great example of one of the clients that we have. If we didn’t exist, this client would have to go and partner with five to ten different companies in order to build this entire solution.

Daniel Webber:

How central are cross-border payments to what Rapyd is doing?

Arik Shtilman:

It’s a big piece of it because, first of all, to continue with the example, the shipping company pays in a specific currency and the seafarer wants to have the money, typically, in euro, dollar or pound. They don’t want to convert it to Myanmar’s currency or Philippine peso, whatever it is.

We allow them, first of all, to have the money in the currency that they prefer. Then, when they do the payouts, it’s a typical cross-border situation because the money moves to different countries in different currencies.

Even the card that we issue is a cross-border transaction because the seafarer is travelling with the ship all over the world and they spend the money in all different places. Everything is cross-border trade there.

One of the best things about our platform is that we are not only providing technology, but we also provide the licensing and the money movement capability.

Rapyd’s acquisition strategy

Daniel Webber:

You’ve made a number of acquisitions now, including your most recent PayU GPO announcement. How are you thinking about acquisitions as a big picture?

Arik Shtilman:

First of all, organic growth is more than 100% year-over-year. But we strongly believe that if there is the right M&A opportunity, non-organic growth is the right choice. We believe that we can accelerate the company by two, three and sometimes even a five-year timeframe by doing the right acquisition.

I know that there are a lot of companies that prefer only organic growth and, yes, it’s much more simple when you focus only on organic. But on the other hand, if you have the secret button that you can push for nitro, that will push you faster and get you accelerated by two to five years, sometimes it makes a lot of sense and that is why we’ve done these acquisitions.

The benefits of Rapyd’s PayU GPO acquisition

Daniel Webber:

Let’s talk about the PayU GPO acquisition. How does that add to what you have at the moment?

Arik Shtilman:

The PayU acquisition is a perfect match for the Rapyd puzzle. Today, we operate all over the world – in more than 100 countries. But if you look at our European business for example, we’re very strong in Western Europe and in the Nordics, but we don’t have any central or Eastern Europe presence. They [PayU] have only Eastern Europe and Central Europe, so it’s a perfect match.

Then you go to Latin America, we have a significant business in Brazil and Mexico. They have a huge business in Colombia where we don’t exist. We do not exist in Africa. They have a business in Africa.

When you really put all these pieces of the puzzle together, they provide us with a lot of things that we don’t have today and that we can grow into organically. But it would take us at least three to five years to build and maybe even more to scale to the level of revenue that they have from these countries. It basically accelerates us by at least five years in our plan.

Daniel Webber:

What do your consolidated overall revenues and processing flows look like together with PayU GPO?

Arik Shtilman:

With revenue, together it’s more than a billion dollars. For processing flows next year, taken together with PayU, you’re talking about $120bn.

Rapyd will probably see around $70bn in processing flows next year and around 55-60% is cross-border. Around 25% of our revenue is coming from small businesses and 75% is coming from medium and large-scale enterprises.

Competitors to Rapyd

Daniel Webber:

Who do you see as your main competitors?

Arik Shtilman:

It depends on the use case. If it is a very narrow use case, then you might find a company like Adyen as a competitor, and Ebanx, dLocal, 2C2P and Payoneer for disbursement, Marqeta for issuing.

It depends on the use case, but if somebody’s trying to build this seafarer solution that we talked about, it has to be a combination between five to seven companies. Nobody can provide it alone.

It’s a huge competitive differentiator because not providing the regulatory and money movement capabilities means that it’s not worth anything, because the number of companies that are regulated is very low. 99.9% of the companies are not regulated.

Rapyd’s future roadmap

Daniel Webber:

Where does Rapyd go next? What’s next in terms of the roadmap and strategy?

Arik Shtilman:

Regarding our roadmap, one of the new things that we’re going to introduce early in 2024 is a new product for working capital lending to our merchants.

This is not from our balance sheet, so it’s going to be a marketplace that will allow other lenders to plug into our merchant base and our data in order to provide the working capital lending and we will be part of the revenue share.

This is, from our perspective, one of the more exciting products that will come out next year. But the majority of the focus now is really on optimising the platform and really upselling the different capabilities that we have to the client base in jurisdictions where they don’t use them yet.

The changing cross-border landscape

Daniel Webber:

How have you seen the sector change in the last four to five years, particularly in terms of cross-border payments?

Arik Shtilman:

The cross-border element grows year over year, because most of the trade becomes more and more international. The majority of the companies understand that they cannot do business only inside their own country and they’re trying to expand.

But the regulatory requirements are becoming harder and harder every year. We see it with the banking partners and with the regulators that we work with, that cross-border trade is a big focus from a money laundering perspective. There are a lot of barriers to entry because of that, because you need to really have a strong compliance and an AML program in order to operate successfully in global cross-border trade.

We have local people regionally, not in every single country, but we have offices in 12 different countries. These are the countries where the majority of the business is done, and we have these people managing their local and regional regulation from these hubs.

Daniel Webber:

Where do you think cross-border trade still needs to be solved?

Arik Shtilman:

This is what people don’t understand. The only people that solve cross-border trade are Visa and Mastercard, because you provide a 16-digit number and the money moves to the other side of the world and you don’t think about it. But that’s also temporary: the regulators are going to start putting their eyes on that too because there’s quite a lot of money laundering that is going on in this type of cross-border trade.

Cross-border trade becomes much more complicated every year that passes by because, first of all, there are new payment methods and payout methods that exist in every country.

SWIFT is not really the solution for the majority of cross-border trade. The regulatory requirements are very complicated and the demand from the banks and the correspondent banks is growing all the time because of the regulatory scrutiny, so it becomes more complicated every year.

Building networks and partnerships

Daniel Webber:

How are you building out your network? Do you try and do all the connections yourself or do you have partners?

Arik Shtilman:

Like everybody else, at the end of the day we partner with a lot of banks and also with some fintechs. You have to be in a situation where you are building a network that is flexible enough to support the majority of the use cases that you need and that you have redundancy.

Success is to have as many local connections as possible for near real-time movement capabilities, but also to be able to manage the FX risk and liquidity in the best way possible because you can gain losses just because of the fluctuation of currency exchange.

We’re focused a lot on hedging and on the right partnerships. We don’t provide our clients the ability to hedge, but we do a lot of hedging in the background.

Speed and coverage in cross-border transactions

Daniel Webber:

Many people are currently competing on instant payments and speed. How important do you see instant payments being to cross-border transactions?

Arik Shtilman:

Generally speaking, the number one question that exists in every support organisation of a cross-border trade company is ‘where is the money?’. Around 30-40% of the support tickets are ‘where is the money?’. The reason why is because the money always gets stuck.

The way to get around it, and to reduce the operational overhead and the FX risk, is to get as many local connections as we can, which will allow real-time or almost real-time payouts. That’s what can improve margins and reduce FX exposure.

Nobody knows if the money has arrived or not except the consumer or the business, unfortunately. But at the end of the day, you dramatically reduce the overhead if you have the local capabilities.

Daniel Webber:

Beyond speed, what else are you finding to be a good differentiator?

Arik Shtilman:

It’s coverage. For example, Google selected us to provide them Play Store payments in Southeast Asia because we can provide them with coverage across seven countries.

The second reason is exactly like the seafarer example I gave: they needed multiple capabilities and it’s a headache to go and find multiple providers.

The third is simplicity: you don’t need to deal with the regulation, with the licensing, with the money movement. You just need to write code and the money will move.

A lot of companies are only tech providers. A lot of companies are only finance providers with no tech, and the number of actual companies that do fin and tech together well is very small.

Rapyd’s road to an IPO

Daniel Webber:

How are you thinking about the future of the company in terms of capital? Are you aiming for a path towards an IPO?

Arik Shtilman:

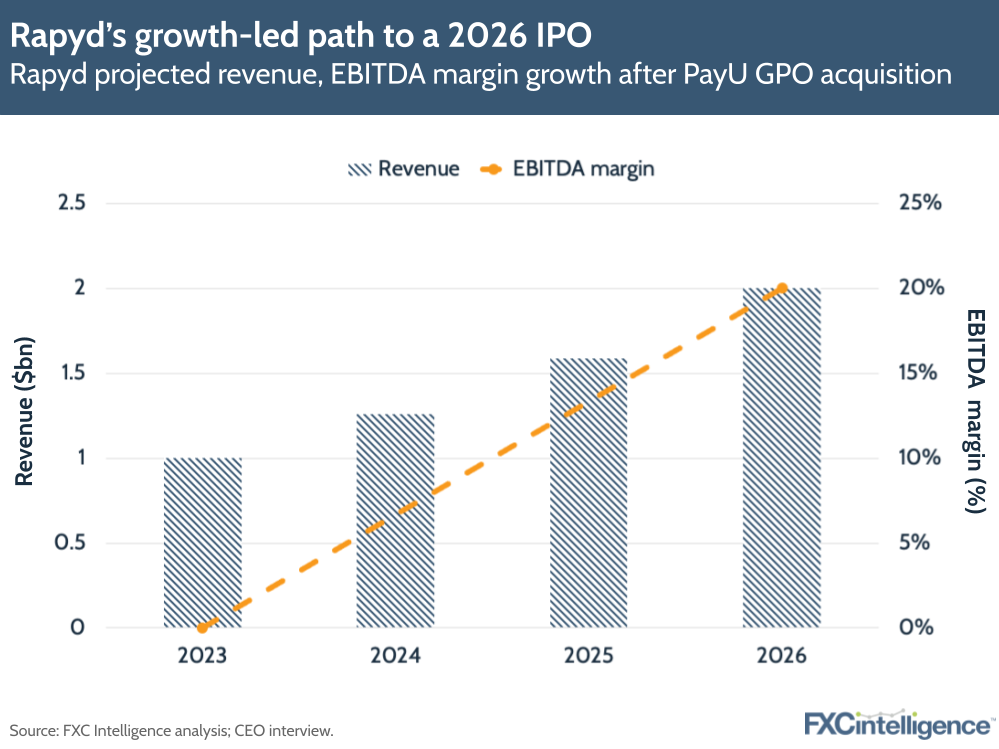

We’re aiming for an IPO because we understand that at the end of the day, if you really want to be a very big company, you have to go public at a certain stage. This is also why we are doing this acquisition of PayU GPO, and we believe that it’ll take us three years from now to go public.

We need to hit profitability. If we look three years down the road, we believe that we’ll be at around $2bn in revenue, with a positive EBITDA of $400m. EBITDA at our current stage is around zero, so we’re almost at breakeven.

Profitability is the fact that at a certain stage, your product and your technology platform gets to a point where it doesn’t need to grow significantly in order to grow revenue.

This is something that happens in the very early to medium stages of life of a company. The operational overhead, the engineering and product overhead, and the cost of processing basically starts to stabilise at a certain stage where the revenue will continue to grow and this is what’s creating the profitability.

Differing approaches to recruitment

Daniel Webber:

You’ve taken some very different approaches to bringing attention to the company and attracting talent. You’ve hosted some great parties. You’ve sent someone into space. Give us some colour on that approach.

Arik Shtilman:

It works extremely well, and the rationale is very simple. If you go back in time to around May 2021, which is only two years ago, Rapyd was not a brand. Rapyd had a very hard time recruiting employees, getting clients and basically fighting for recognition and brand awareness around the tech and the fintech space.

We were looking for different ways to do it. Going to a conference and having a booth is not the way to do it. We basically tried to do things a little bit differently. It was a very big gamble from our perspective, but we went down the path of having these hackathons with large prizes like sending somebody to space.

We had some very large events and parties that were related to recruitment of new employees that created a lot of noise and social media awareness. Basically we were able to build in a very short timeframe – literally less than a year – significant brand awareness.

At the end of the day, we invested the same amount of money that people will invest in conferences or Google, Facebook or Instagram advertisements. We just invested them in a different place, but the result was 100x better.

If you measure our output from Google Ads, Facebook and Instagram versus what we did with one party that David Guetta played in Lisbon during the event, the party generated 100x more business. It’s insane.

Daniel Webber:

Anything else that you’d like to share about Rapyd that we haven’t covered?

Arik Shtilman:

We want to be one of the top three fintech platforms in the world. We are on the right path to become one of the biggest three players that exist.

The goal is really to build a long-term sustainable company that will be worth $50bn+.

Daniel Webber:

Arik, thank you.

Arik Shtilman:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.