Money transfers player Paysend has grown significantly since its launch six years ago, including through an expansion beyond consumer into B2B payments and in offering an enterprise platform. We hear from key senior management about Paysend’s ongoing strategy and vision.

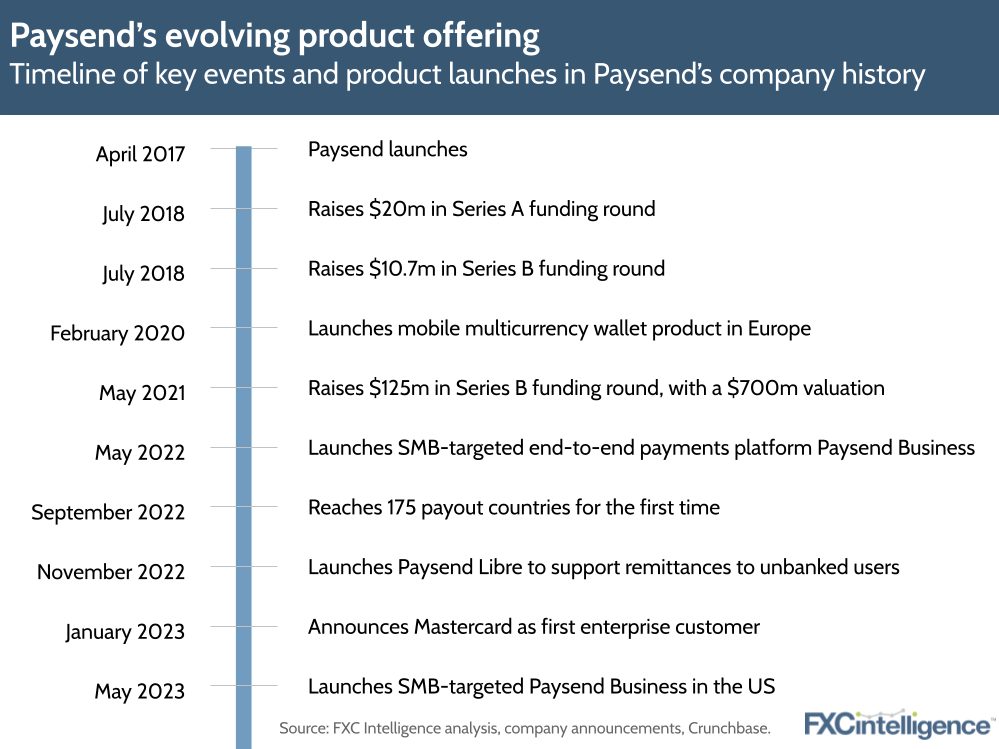

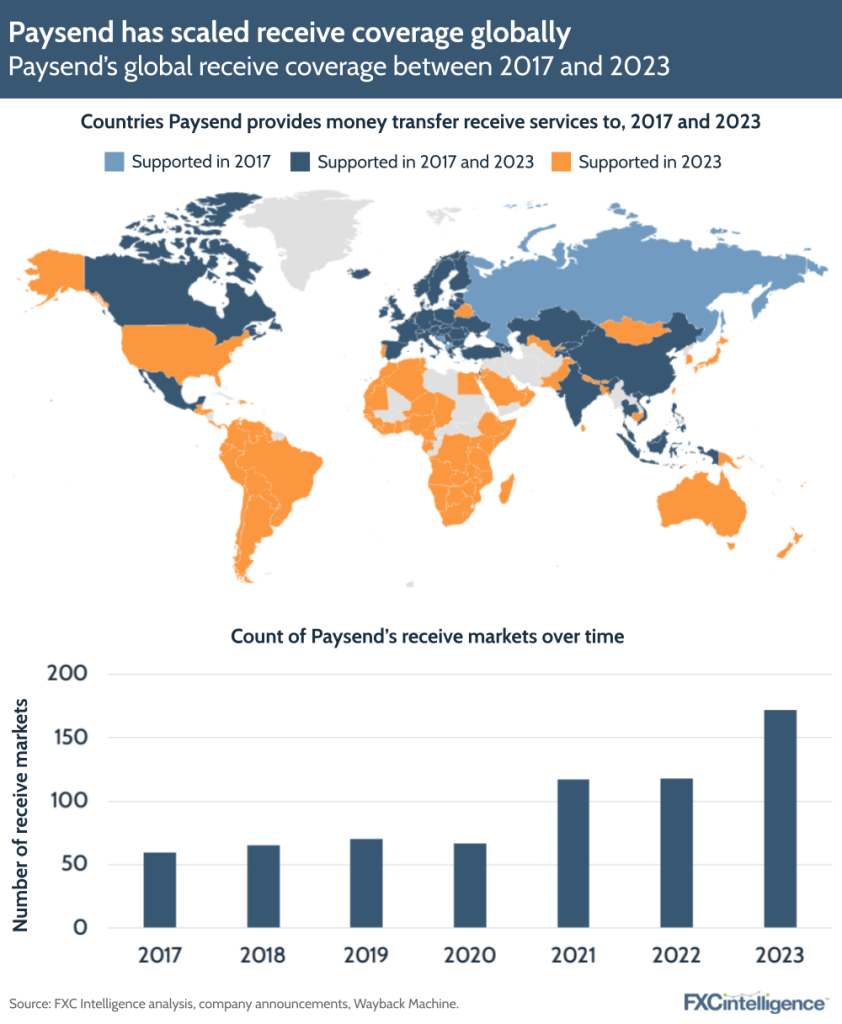

Founded in 2017, Paysend has grown from a money transfers player focused on certain regions to a significant contender around the world, operating in over 170 receive markets across six continents.

While initially focused on card-to-card transfers, the company also has expanded to support several other send and receive types, and has secured a wide variety of partnerships with both local players and key networks, including becoming direct members of Mastercard, Visa and China UnionPay.

It has also broadened its offering during this period. In 2020, Paysend launched a consumer multicurrency account and in 2022 it expanded its services to business customers, covering both small and medium-sized businesses (SMBs) – as well as larger enterprise clients.

As it has grown, the company has increasingly focused on infrastructure, while also evolving its go-to-market offering to meet the needs of the diverse range of markets it now caters to.

But how has its strategy underpinned this approach, and how does Paysend plan to evolve its plans over the coming years? We speak to key members of the company’s senior management to find out.

Positioning Paysend: Evolving strategy

Built on the core values of simple, instant and inclusive, Paysend has evolved its proposition over the past few years to broaden its customer base.

“Our goal is to deliver the world’s simplest money transfer, and that goes across the consumer side of the business, as well as the business side, small and medium-size firms, and more recently also our enterprise solution,” says Jairo Riveros, Chief Strategy Officer and MD of North America LATAM, Paysend.

“We allow 12 billion cards that exist worldwide to connect to each other and send payments from one to the other.”

However, this broadening approach follows a period where the company was tightly focused on its consumer offering, and developing to more effectively deliver that.

“We were initially incredibly focused on the consumer money transfer side and building out the global platform in a way where we owned the value chain ourselves,” says Ronald Millar, Co-founder and CEO of Paysend. “We did that very successfully over a number of years.”

This saw the company build out its consumer services, as well as add some ancillary services for the business marketplace; however, in 2021 the company reviewed this and determined that its approach wasn’t fully aligned with its core focuses.

“Looking at the marketplace and what we’d created in terms of our ownership of the value chain and the technology we had behind it, we came to realise that actually wasn’t really building to our best strengths,” says Millar, adding that these strengths were to “focus incredibly well on the payments piece, regardless of the end customer, be it a consumer, be it a small business or be it a very large corporation”.

“That really led us to launch the three business divisions at the start of 2022: the consumer division, what we call the B2B or direct business division and then the enterprise division.”

For Millar, this has been a “fundamental transition” in how Paysend is building its business, and has changed not only how it is continuing its strategy and development, but also how it sees itself sitting within the market.

“We really homed in on the payments piece, with the ancillary services that we offer being correlated to the fundamental underlying mechanisms of money transfer itself,” he explains.

“Whereas before, [our proposition] would have sounded a lot more similar to a Revolut or a Wise.”

Paysend is not the only company to have shifted to increasingly focus on the B2B and enterprise market. The pandemic prompted many players in the space to look to this highly fragmented market for growth, however Millar sees the company’s cross-scheme card offering as giving it an edge over its competitors.

“We still are today the only people that can do cross-scheme on a global basis,” he says, pointing to the company’s integrations with Visa, Mastercard and China Union Pay, as well as its support for wallets, including Alipay and WeChat, and bank account integrations, including SEPA.

“It doesn’t matter where it’s coming from, it doesn’t matter where it’s going to, we can do that on a global basis. At the end of the day, it’s about giving the end customer the choice as to how they want to receive the money and making sure we have the infrastructure to do it to the same quality, same effectiveness and same speed of transfer.

“That’s the bit that still remains unique for us. It was unique when we first launched it six years ago, and still no one’s come at it in exactly the same way that we have.”

Building Paysend’s infrastructure

This broad offering in terms of pay-in and pay-out types has seen Paysend put a strong focus on developing its own infrastructure over the past six years.

“We evolved as an organisation that built interoperability of the three major networks, enabling consumers to make easy cross-border transfers,” says Abdul Abdulkerimov, Founder and Executive Chairman of Paysend.

“Then we moved to be an organisation that literally built our own infrastructure, enabling not just the consumer or businesses directly, but enterprises, leveraging the infrastructure we built.”

Critical to this has been and continues to be the ability to enable these various networks to interoperate.

“The company will build this technology stack that enables the networks to talk to each other, to transact with each other,” says Abdulkerimov.

“We will enhance this network by adding global instant payment systems (IPS), like SEPA in Europe, Faster Payment in the UK and ACH Instant in the US. That is our goal: the combination of the network infrastructure and the IPSs that allow customers to have frictionless transactions where messaging and settlements happen instantly.”

This is also seeing the company take on the challenge of settlement, which unlike messaging remains “very complex”, according to Abdulkerimov.

“In many cases, traditional money transfer organisations have partners in different countries. They deposit the money with these partners who pay our partners, and they settle this afterwards as soon as the transactions are executed,” he explains, adding that through SWIFT the involvement of multiple banking organisations “causes high cost, friction and timing”.

“What we’re building is open, where the messaging and settlement occurs instantly. Whenever you send the money to your counterpart in a different country, you get the instant messaging and we settle the funds immediately as well, leveraging the existing infrastructure of the payment network like Visa, Mastercard and UnionPay. “

Infrastructure development is an ongoing project for Paysend, which only launched its SMB business offering in the US in May of this year. As a result, while the company has moved past startup into scale-up territory in terms of reach and size, Millar argues that the company in some ways still needs to have the approach of an emerging business.

“The people you’re bringing on board have got to have that startup mentality because you are starting new in each of those things which you do,” he explains. “You’re still starting new in new markets, we’re starting new in North America, starting new in the US with our own licence. On each and every thing, it is completely from scratch.

“That’s what, to me, brings the excitement of the day-to-day for Paysend and also keeps everybody focused on what they need to achieve and how quickly they need to achieve it. Because you can’t achieve it at corporate rates of development and speed; you have to achieve it at startup speeds of development.”

Paysend’s enterprise play: The importance of owning the network

Launched in 2022, the B2B and enterprise divisions saw Paysend develop entirely new teams and products, and attract new customers.

“It’s like doing another complete startup again,” says Millar.

Paysend’s first enterprise customer was Mastercard, which was announced during the issuer’s Q4 22 earnings call in January of this year, with CEO Micheal Miebach saying the partnership with Paysend would “broaden [Mastercard’s] global reach and expand the ability to send international payments across card brands”.

“We have made a Mastercard super network where we provide our solution via API. Now Mastercard’s clients can send money not just to Mastercard but can send Visa, China UnionPay, AliPay, WeChat accounts,” says Abdulkerimov. “That enhances the network capabilities of Mastercard and provides a richer proposition.”

For Paysend, the addition of an enterprise product has been a significant shift in offering, and signals how the company is set to develop in the coming years. However, Millar says that the division “in essence came about by accident”.

“The B2B business, first of all, was designed for the SME online market. Some of them were doing cross-border payments and saying, ‘Why can’t we do those in more bulk?’. That ultimately led to us realising that there’s actually a completely different market segment here that initially we hadn’t thought about,” he explains.

Now that the company is broadening its customer base for its enterprise product, it is positioning it largely on two main points, the first of which is geographical coverage.

“For a business of our size – we’ve been going for six years – we have tremendous global penetration. We can currently transfer into just short of 180 countries,” says Millar, adding that the second point is the company’s control of the value chain.

“We are direct members of Mastercard, Visa, China UnionPay; we are our own third party processor, we do our own processing; we are also a certified acquirer, we’re a card issuer. So we own each individual element of a payments value chain in-house and on a single platform.”

This gives Paysend visibility into a payment’s progress through the system – something that Millar argues gives it an edge over correspondent bank systems where payments can get lost.

“You spend days, maybe a couple of weeks, to actually physically chase down money. It happens because of the way they’ve structured and are using the global payments mechanism,” he says.

“By owning the entire value chain and controlling that ourselves, we take that element of it out. So the combination of that element and the global coverage is what allows us to really deliver a single, reliable, trustworthy, enterprise-level service compared to how the vast majority of cross-border payments get made.”

This approach sees Paysend own the full value chain for all 180 countries it serves, including on the regulatory and legal side, although in some cases the company does work with partners.

“It’s not that you can’t do things through partners, and clearly we do work with partners in some areas because it does bring you more speedily to market,” he says. “If you want to do business out of New York, finding a partner so you can do business is a lot quicker.”

Catering to enterprise customers

Within the enterprise category, Paysend caters to a relatively broad range of companies, however most are looking to solve two common issues they face when regularly using correspondent banking solutions: certainty over both arrival time and the amount that will arrive.

“When you’re shifting money across borders through multiple correspondent banks, ultimately you actually don’t know how much money will arrive at the end destination in many cases,” says Millar, pointing to the fact that the amount charged by correspondent banks varies significantly, with some charging nothing, others charging a fixed fee and some charging a variable fee.

“If you’re dealing with very large corporations who are just doing corporation-to-corporation transfers, then sometimes they view that as a cost they have to bear. But if you’re using an enterprise solution where your end recipient is a consumer or consumer-level transfer, the end recipient is in quite a different position and these sums of money are quite significant to them.”

This is a particular concern for global cross-border payroll companies, who need to be sure of the exact amount that arrives in the recipient’s bank account, as well as when it appears. This includes provider Deel, which is a customer of Paysend.

“You’ll be able to provide certainty of what is actually going to arrive, on a cost basis that matches the amount of money you’re transferring, and with the certainty as to arrival,” says Millar.

Remittance companies also have similar needs, with Paysend increasingly looking to cater to this group.

“We’re enhancing their capabilities with a single API, reaching 192 countries,” explains Abdulkerimov.

“We send money to accounts, cards, wallets. They don’t need to develop that network-by-network, certify the product and spend months and millions to build the network: via a single API, they can get this access immediately.”

The company is also developing a new product for B2B transactions that will pay out to any mix of digital bank account, mobile wallet or card.

“When you travel with your personal card to another country and pay for a coffee, with a UK issued card you’re to pay the merchant and your issuer, Visa or Mastercard, settles this locally and charges your issuer in the country where the card was issued. This is a standard operation,” says Abdulkerimov.

“We’re building a solution to use this relationship and infrastructure and use this for B2B transactions below $100,000 in exactly the same way. Combining our technology with that infrastructure creates a breakthrough solution that can provide customers with greater value than any existing solution.”

Evolving products: Virtual cards and Latin America

While much of Paysend’s recent business development has been on the B2B and enterprise side, the company has also expanded its consumer offering geographically.

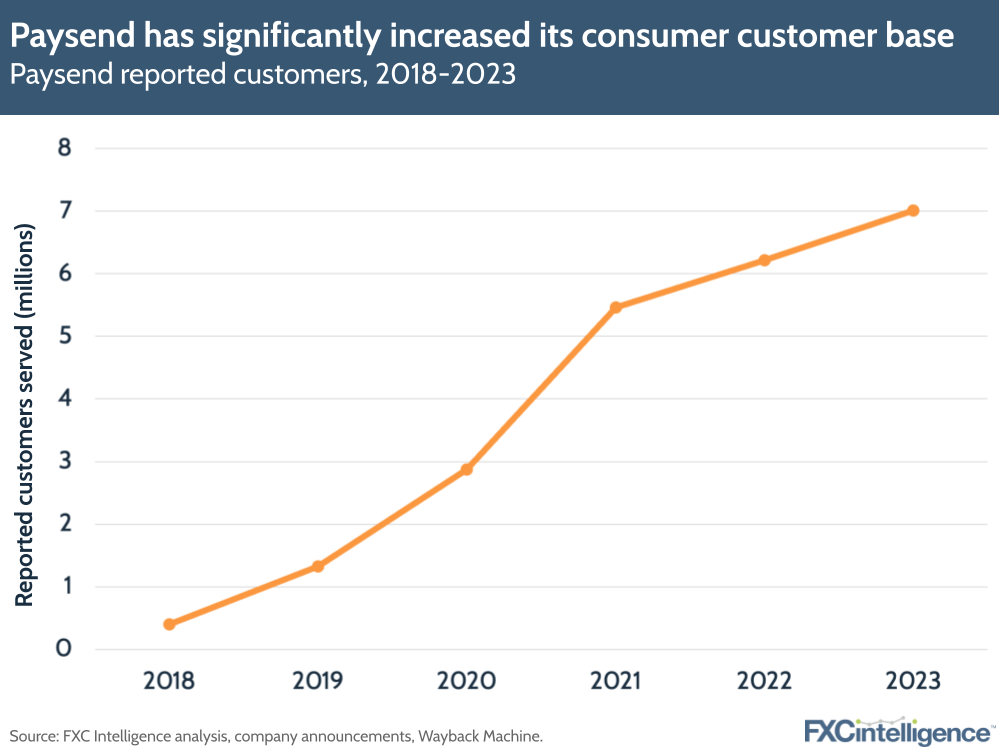

“We have more than six million customers who use the card-to-card payments today. They are focusing on sending from the US to Europe, Europe to Eastern Europe and the US to Asia,” says Riveros, adding that the company also sees a significant domestic consumer business within the US, Canada and Europe.

However, the company has recently increased its focus on Latin America, including with the launch of virtual card product Paysend Libre.

“$130bn is sent from the US to LatAm every year, and most of that is cash,” says Riveros, adding that while the volume meant that it was “definitely a market” for Paysend to enter, the cash focus presented a potential challenge.

“We have grown in Europe fantastically: there is a lot more card penetration within Europe, so our model was working fantastically. But when we came to the Americas a year ago, we saw that our volume continues to be strong from the Americas, from the US and Canada to Europe, but to LatAm, we were finding that most recipients do not have a card.”

Paysend Libre is designed to tackle this. Developed in partnership with Mastercard, and already the subject of a BBC Storyworks documentary, it is designed to provide a digital receive solution for recipients who do not have access to a bank account.

Through this system, the sender remits money to their friend or relative as normal, via the Paysend app using their phone number. The recipient then receives a text message to download the app, after which they can opt to transfer the money to a bank account if they have one, or alternatively accept it as a Paysend Libre virtual card.

“She’s going to immediately have the money right there, without leaving home, without having to expose herself,” says Riveros, adding that the company selected Guatemala as the first market – with Mexico, Colombia, Argentina and Brazil to follow – due to its position as the second-largest receive market in LatAm, as well as its high levels of smartphone penetration.

“The transit in Guatemala accepts contactless payments, so she can take the bus to work. She can also order online groceries, food, medicine, because it will be deliverable. She can also go to certain merchants and use her Google Wallet or Apple Wallet, and she can go to an ATM network – not all of them, but a good number of them – and take cash out.”

This approach is designed to serve as a bridge between the recipients’ usual cash-based approach and the digital capabilities offered by a card-based product, with the ATM support in particular being key to ensuring the product is well received.

“These are mostly cash-driven countries, and we want to still give them something which they are familiar with. But at the same time, we want to bring this customer to financial services as a client because they are outside of the system,” says Abdulkerimov.

“We believe it’s an amazing product that’s creating great impact for the people who are unbanked and making sure they can benefit from financial systems as any one of us can.”

The company expects that the simplicity of the process will encourage recipients to request this method again, and through its partnership with Mastercard Paysend will continue to build digital payments literacy.

“We’re beginning to educate that customer about how they can become digital instead of having cash. We will be able to say: this card is actually quite powerful, it can give me access to things I didn’t know about,” says Riveros.

This approach has also included the use of ambassadors both in the US and Latin America who can introduce the technology to the communities in question and so bridge the understanding gap about its utility and benefits. In the US, this has included the hosting of a soccer tournament for the Hondouran community in Miami, while in Guatemala this has included meeting locals at a handicraft fair.

“By planting seeds, we want to spread the message of ‘this is how we can do it, this is what it can do’,” says Riveros. “[We’re planning] more events locally in the US, certain communities – California, Texas, Illinois, New York, Florida – and country by country, going as local as possible.”

In the long term, the company hopes to extend the service beyond LatAm.

“Once this works quite well, we want to take it to Africa, we want to take it to Asia as well. But we have started with Latin America with Paysend Libre,” says Riveros, adding that smartphone and internet penetration, as well as flows, will be key to selecting future markets.

Paysend, strategy and the future of cross-border payments

With evolving foundations in place across both the consumer and B2B sides of the business, Paysend is now looking at how these will feed into the company’s ongoing development.

“The strategy for the next five years is to make sure we are the network provider for big players, including the networks themselves, and that we still have a strong direct-to-market position in consumer and business that give us the opportunity to continuously learn about our customers,” says Abdulkerimov.

“Paysend will have this diversified revenue stream, but mainly it will be enterprise–driven from providing access to the Paysend payment network and open payment network.”

Within this, the company is also likely to look to broaden who is taking up its enterprise offering.

“We believe there is a demand for banks that want to modernise their cross-border payments,” says Riveros. “Not the Bank of Americas, Citis or RBCs, but the second tier, third-tier banks, community banks, who are not members of SWIFT, so by definition they have to connect via correspondent banks.”

Meanwhile, the company expects the cross-border payments market to continue to present a variety of opportunities over the next few years.

“The consumer money remittance market is still dominated by cash transfer; the majority of that market is still cash. Therefore, from our perspective, it’s still an incredibly attractive market to play in in terms of the opportunities to go forward,” says Millar.

“Looking at the broader market of cross-border payments, then the market in which our enterprise and B2B products are in is a vast multiple of the consumer money transfer market, given the significance of the volumes that are coming out from enterprise-size businesses. So the opportunity we’ve created for ourselves over the next few years is actually on a different level to where we were before.”

Ultimately, the company expects its business divisions to become the primary driver of revenue.

“I can’t say whether it’s two years, three years, but if we’re looking forward over a number of years, then I would clearly expect the enterprise and business parts of our business to become more dominant, to ultimately become the majority of our business because they are bigger marketplaces. And by being successful in those marketplaces, they would become the majority of our business automatically,” says Millar.

However, the company is mindful of the fact that while it has laid strong foundations, there is a tough economic climate ahead.

“This is a very tough time for startups, particularly in regulated areas. The major challenge today is how to not lose what was invented and how to re-emerge stronger within the next couple of years and still be an innovation-driven company. That is a big challenge for every player on the market, including Paysend,” says Abdulkerimov.

“But at the same time, we don’t want to become just a simple money transfers organisation. Instead, we want to continue being a leader in payment technologies, infrastructure and network technologies. That is the challenge for everyone and the challenge for us, and this is what we are doing at Paysend.”