Although in the process of going private, MoneyGram has released its Q3 22 results, following recent announcements on crypto and an F1 sponsorship. We spoke to CEO Alex Holmes to find out how he’s thinking about the brand as it embarks upon a new era.

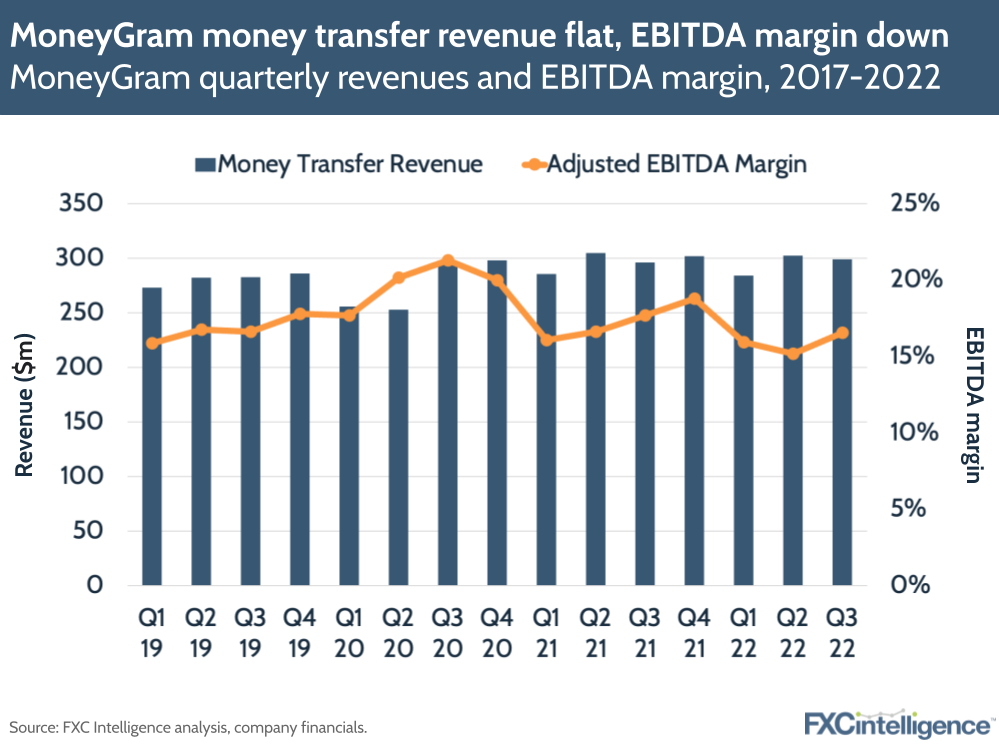

MoneyGram has announced its Q3 2022 results, and while there was no earnings call due to the company being in the process of going private, there were some positive signs for the money transfers major.

While total money transfer revenue grew just 1% year-on-year, to $2.9m, this was largely due to the ongoing strength of the dollar – on a constant currency basis the company saw money transfer revenue grow 7% and volume rise 11%.

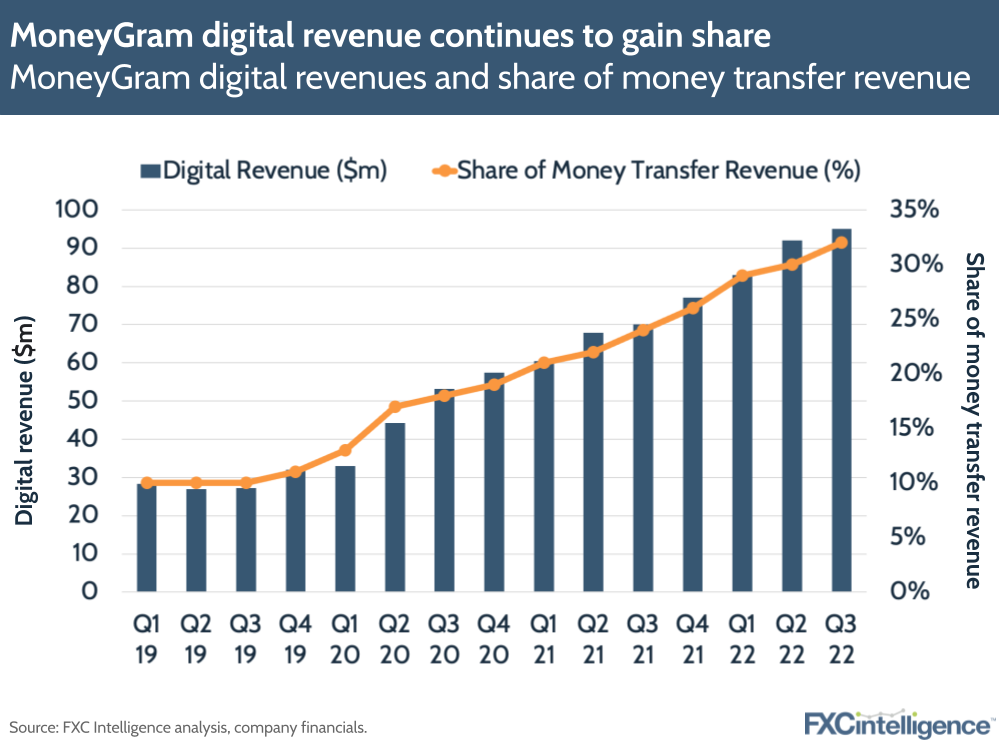

However, this masked a strong performance from MoneyGram’s digital segment, with MoneyGram Online growing 13% YoY to $52.9m, as well as a 15% rise in transactions and a 17% increase in cross-border revenue. Total digital – which includes MoneyGram Online, digital partners and digital receives – performed particularly well, with revenue increasing 36% YoY to $95m, while transactions grew 39%.

The earnings follow two recent key announcements from MoneyGram. At the start of November, it added the ability for US customers to buy, sell and hold major cryptocurrencies via its app, building on an existing partnership with blockchain provider Stellar using Circle’s USDC stablecoin. In late October, it also announced that it would become the title sponsor of Formula 1 team Haas in a multi-year deal.

With the company set to go fully private by the end of 2022, what is driving these decisions and how does it plan to build on its current success in digital and beyond? Daniel Webber spoke to CEO Alex Holmes to find out more.

Branding: MoneyGram’s F1 sponsorship and beyond

Daniel Webber:

Let’s start with your Formula 1 title sponsorship with Haas. Why did you choose this sponsorship, and how do you anticipate it impacting the business?

Alex Holmes:

Absolutely. First and foremost, in many respects people have seen us pulling away from global brand marketing over the last several years as we’ve pivoted the story to the digital and the moneygram.com business and focused a lot on consumer direct acquisition strategies.

As we transition to a private company and begin to really message and change the story around our capabilities – we’ve added so many new use cases, so much more functionality to the system as we’ve digitised – we felt it was important to get back out there and get on the front foot and really start thinking about we get the message out to consumers who may not realise that MoneyGram now has so many different opportunities to transact digitally, in addition to our great cash network.

We thought about how to do that; how you do that on a global scale and how you do that across 200 countries and territories and really get the message across. There’s a lot of opportunities for sponsorships in the world around sports. Sports has a very attractive appeal to many people and it’s a unifying thing, if not also a divisive thing, but it creates a unification, the competition of sport.

When you break it down, there’s a lot of global sport, but there’s really only one in that sense that’s unique, that travels, that goes from country to country, that creates sort of that World Cup, Super Bowl environment everywhere it goes. And that’s Formula 1.

For us, the uniqueness of the sport is it moves across so many continents – across 21 countries next year – and covers about 80% of our global revenue. So we think it’s a great way to put some sizzle into the brand and really excite people about MoneyGram, what we’re doing. It’s a wonderful platform to drive the future growth of the company.

In addition to that, Formula 1 has just been on a tear globally, setting records at racetracks. The Drive to Survive Netflix series has been instrumental in pushing that forward. And we love the Haas team. The Haas team is an underdog, scrappy. They’re new. They’re coming out right now. I think it fits our brand profile really well.

It’s exciting for people. It’s going to be amazing for us from an activation perspective around the world and the ability to transcend the traditional view of our business model and really begin to think of it as a much more upbeat, fast and, for lack of a better word, sexy opportunity to really think about the business and the company differently.

Figure 1

Daniel Webber:

How does the Formula 1 sponsorship fit into your broader plans for marketing and branding as you reposition the company?

Alex Holmes:

There’s two ways to look at a business. One is obviously from a customer perspective. And from a customer perspective, we want them to think about the company as being digital-first. Clearly, with our MGO business in about 38 markets, with over 100+ countries digitised, and with changing dynamics in markets across Asia, the Middle East, South America and Africa, we really want consumers to begin to think about that new angle on us. Wallets and telcos are coming into the game and we’re really thinking about how to acquire customers on the front-end and the ability for us to disperse payments and push them through all of our dynamic rails.

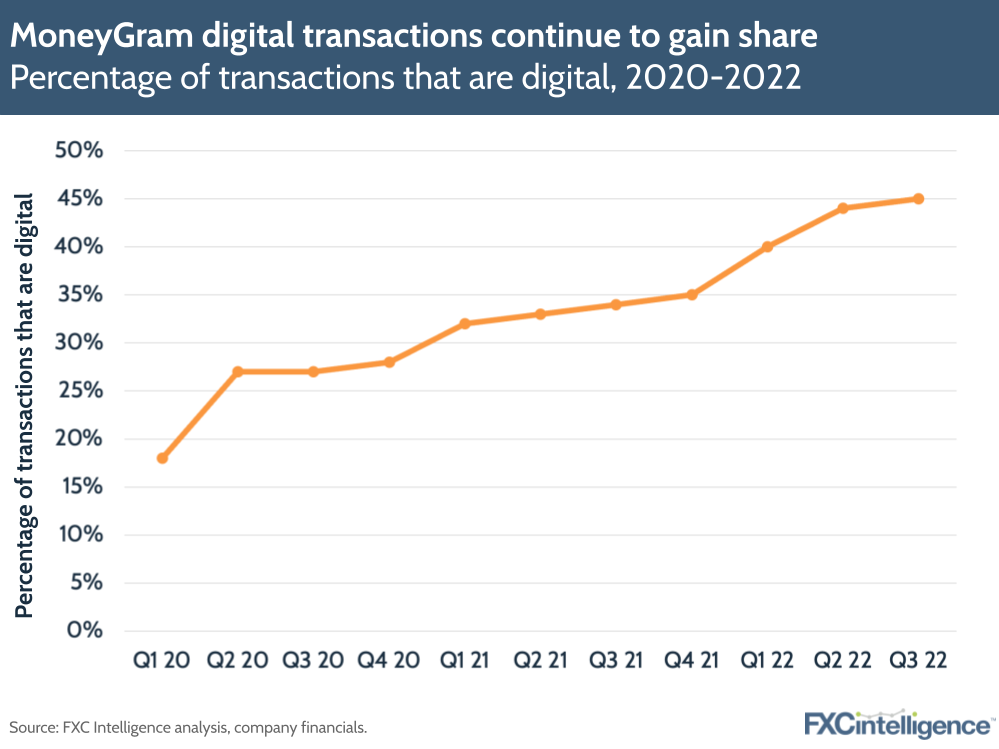

Cash is still king in many respects, but we want that to be seen as something that we do, not something that is all we do. 45% of our transactions in our third quarter were digital. That speaks volumes about the transformation not only of our business but also of the market itself and also what consumers are looking for.

The customer demographics when you go digital are trending much younger. The walk-in business, the cash business, while still incredibly relevant in so many markets and in such a need for so many people, is ageing. That demographic is shifting and ageing and new customers coming into the market every day.

Migrants are still as active as they’ve ever been, yet they’re leading with mobile. They’re leading with digital. They’re leading with these new types of apps and platforms. When you blend that through with Formula 1, for example, the age demographic for that sport continues to trend younger as well.

So there’s a perfect relationship there between new customers coming into the market and the brand perception and persona that we want to push and achieve.

The other side of that, then, is obviously your investor and shareholder base. As we go private, one of the things that we want to do over the next several years before we take the company public again and try to monetise it is we’ve got to change the perception of the investor base and what we do.

The more you talk about digital, the more you lead as a digital company and the more corporate see you doing things like Formula 1, the more they see that name and that brand, the more attraction there’s going to be for people to go see what that’s all about. “Oh, where have I heard of you before today?”

Someone might say in the US, “Oh, aren’t they at Walmart and check cashers?”. In five years, I want them to be saying, “Oh, I’ve seen them on Drive to Survive and Formula 1,” and like, “Oh, yeah. I love their app. It’s digital”.

We’ve got to expand the multiple. We’ve got to create value. And the way to do that is to make your company more valuable.

MoneyGram’s digital growth

Daniel Webber:

Your growth in digital is faster than some of your peers. How are you managing that?

Alex Holmes:

For us it’s really about the front end and the back end. When you think about the digitisation of the network, a lot of that has been these efforts on our part to improve distribution on the receive side. Adding account deposit globally; adding new wallet functionality and capabilities to deliver funds directly into those wallets.

One of the things that’s amazing about that is it begins to shift the paradigm about who your customer is. It changes the use cases. People sending to wallet, for example, are typically sending smaller dollar amounts to more people. Those are more payment-oriented type movements; that non-traditional remittance.

When you think about people moving money into a bank account, sure, sometimes I am sending it to another party. Oftentimes, though, I’m sending to myself and I’m saving so that when I get back home, I have money.

So you’re changing the use cases and you’re shifting the paradigm around what your brand is and who it’s relevant to. That’s pretty important.

We’re going to continue to drive moneygram.com. Obviously, we want to lead with that. We’re going to develop that into a more fulsome financial service app. We saw the launch of buy, sell crypto this fourth quarter. But then we’re going to continue to focus on expanding that, making it a more dynamic wallet. We’ve done a considerable amount to change our agent partners around the world to focus on adding digital send partners as well, thinking very differently about that.

When you look at the shift in Asia-Pacific, across the Middle East, even down into parts of Africa and South America, many consumers are now leading with sending money but they’re doing that from their phone, from apps, from local providers that have some sort of fintech service app.

In many countries, it’s very difficult to get a licence to actually be a money transfer service provider because sometimes you have to be a bank or you have to have a special licence. It can be expensive. So we’re looking at how we can plug into those partners so that we can hit the distribution side of it.

Many of our competitors aren’t thinking that dynamically. Many of them are leading with their own app and then they want to go market-by-market, which is fine, but in so many countries, somebody else’s app means more. Their brand name means a lot more than what a local money transfer or a global money transfer could mean versus a global provider.

So thinking about someone else having the front end and you running the back end rails is an important part of that mix. That’s played really, really well for us as we’ve thought about how to more dynamically focus on partnerships around the world.

Figure 2

The growth of digital receive

Daniel Webber:

I assume that digital receive has grown. What proportion is now digital receive?

Alex Holmes:

It’s a difficult question to answer in some respects because it really depends on where you are in the world. I’ve used some examples in the past where in India, for example, over 80% of our transactions now go directly into bank accounts and the cash side of the business in India, while still existing and still doing fine, is just becoming a much smaller piece of that business.

Clearly, there’s a higher propensity of people sending digitally to also have that money received digitally than there are the opposite, people walking in to do cash and sending to bank account is important, but you tend to see more cash-to-cash in that sense and you tend to see a much higher percentage of digital-to-digital.

So digital receives for us continues to improve. When you have a digital send, it outpaces the cash pickup. Digital receive is starting to outpace the cash pickup side from a growth perspective. But it’s a market-by-market dynamic and it depends on where you are in the world.

Approaching MoneyGram’s cash-to-cash business

Daniel Webber:

How are you thinking about the cash-to-cash side of the business now you’re increasingly focusing on digital?

Alex Holmes:

I will say, profitable growth tends to cure all ills. But when you’re not in the G20, cash sends, cash receives are still as important as they’ve ever been. Where we’re seeing the slowdown and the drop off in the business has really been in the G20 and even a little bit beyond that.

Even across the Middle East, for example, you’re seeing this massive switch from, typically, foreign exchange houses and walk-in business to digital sending. But when you go to Europe, when you go to the US, when you’re down in Australia, Canada, etc, the bigger stores – the big post offices, retailers, big boxes – we’re seeing slowdowns in those and you’re just not seeing customers come back the way that they used to.

That was a trend that we saw before the pandemic, but since the pandemic and after, you just have not seen a lot of those big box retailers and post offices, banks, etc come back in popularity from a walk-in perspective. So many people switched to digital. That’s where that’s trending. But on the mom-and-pop retail side of it, when you get down into ethnic grocers, that is still doing really, really well.

My view is that over the next several years, we’re going to continue to see a transition away from the walk-in business as demographics age and as popularity of digital continues to grow. People will continue to do cash sends, but they’re going to do that at more of their local street corner store and not necessarily at a vast post office or a big box retailer.

We love the distribution that those service providers bring. We love being partnered with them, but I just don’t think you’re going to see the growth from that over the long-term. That means a lot. When you’re going through a transition to digital, that doesn’t mean that everything is digital today and no longer cash. You’ve got to work through that and maintain that.

We’re seeing a lot of our partners that have seen some of the slowdown and drop-off, turn around and say, “Okay. We want to be more digital. How do we get the app? How do we get plugged in?” So I think you’re going to kind of see that transition.

The Middle East is a good example where banks and others have said, “Okay. Customers aren’t going to walk in. So let’s put the investment into a new app on the send side of it, so that we can give people the same service but in a different way”.

Figure 3

MoneyGram’s moves into crypto

Daniel Webber:

Given the current crypto environment, some people are probably asking why you’ve chosen now to launch products in the crypto space. Give us some colour on that decision.

Alex Holmes:

People need to be very cautious in understanding where the market is. There’s an old saying: “To get from zero to 10% takes 10 years and then to go from 10 to 100 takes about 10 years.”

That’s happened with crypto, it’s had this astronomical skyrocket and probably overextended because of the pandemic. So many people at home sitting there focusing on it and thinking about it drove up valuations probably way beyond where they should be, a little bit like the early dotcom age. It’s hard to go back and say the internet didn’t work. It’s hard to go back and say that the dotcom era blew up and that we’re not better off for it now. And I think you’re going to see the same thing across crypto.

I mean, clearly what happened with FTX is a tragedy in many respects, but it’s irresponsible management and you got margin calls going in. It’s the same wheeling and dealing that you see in Wall Street on occasion, and I don’t think that’s isolated.

That’s not a crypto problem. That’s a new market, unregulated issue that’s lack of oversight, lack of discipline. When you think about FTX, the exchange is fine, it was this hedge fund in the backside that caused a lot of the problems.

Does that lead to losses? Sure. Is the crypto market down? Absolutely. But are there more and more applications coming out every day? Is there more utilisation of blockchain? Are there more and more people looking at it for everyday needs? I think the answer to that is yes.

What’s going to be the winner in crypto? I don’t know. How’s it going to play out? It’s hard to say. We need some regulation. We need some controls on it. But the things we’re doing with Stellar and stablecoin with Circle and USDC, as long as that coin is stable, there’s an amazing amount of things you can do from a transfer of money and thinking differently about how the markets work.

But when you get into speculation and you buy crypto because you think it’s going to perpetually increase in value, that’s just not how any market works and it’s not how people should be looking at it. These things need to get sorted through and I do think you learn a lot from failure and I think that they’ll grow through.

At the same time, before the pandemic there were very few people [using crypto]. It was starting to creep up. There’s now much more awareness of crypto, many more people focused on it.

We thought it was an important part of the business to get into. Over the next decade, as crypto becomes more regulated, more mainstream, more understandable for everyday consumers, we want to be able to participate in that space.

Clearly, protecting consumers against losses and all that is an important aspect of it. We’re going to do the right things there. That’s why we’re not rushing into it. We’re dipping the toe in the water and slowly going in it.

We have a partner on the back end that’s doing the custody of the coins and that is securing those assets for consumers. You can’t take away from market volatility, but you can protect assets. So I think it’ll be interesting.

I’m not saying the entire future is blockchain, fiat’s going to be around for forever and there’s tons of benefits to the current financial systems. This is supplemental to it and it’s going to enable us to do some very interesting things over time. So it’s important to be a participant, but obviously not in a way that creates risk or volatility.

We’re taking crypto and we’re applying the KYC standards, the AML standards and the other standards of the fiat world and we’re applying that to the crypto space.

People in crypto say there’s no regulation. Sure there’s regulation. You can take everything that they do today and you can apply it to the crypto space, there’s just a lot of people that don’t want to. There’s a difference between not wanting to and not having something to base your skill sets on.

Daniel Webber:

Is there anything else you want to mention that we haven’t covered?

Alex Holmes:

I think we covered a lot of things. We had a very nice quarter. The company’s doing great. Digitisation has been going quite well. And it’s always a pleasure to talk to you.

There’s going to be a lot of exciting things coming out with MoneyGram even as we’re private. So I look forward to talking more about that, and always appreciate it.

Daniel Webber:

Alex, thank you.

Alex Holmes:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.