Western Union spoke more about its stablecoin strategy in its latest earnings results for Q2 2025, in which difficult macroeconomic conditions saw the company’s total revenue fall by -4% to $1.03bn, while its operating margin remained flat at 19%.

The company is now doubling down on its digital transformation, while its travel money business continues to grow its share of Western Union’s overall business as transactions falter across some core markets.

Western Union headline financial figures for Q2 2025

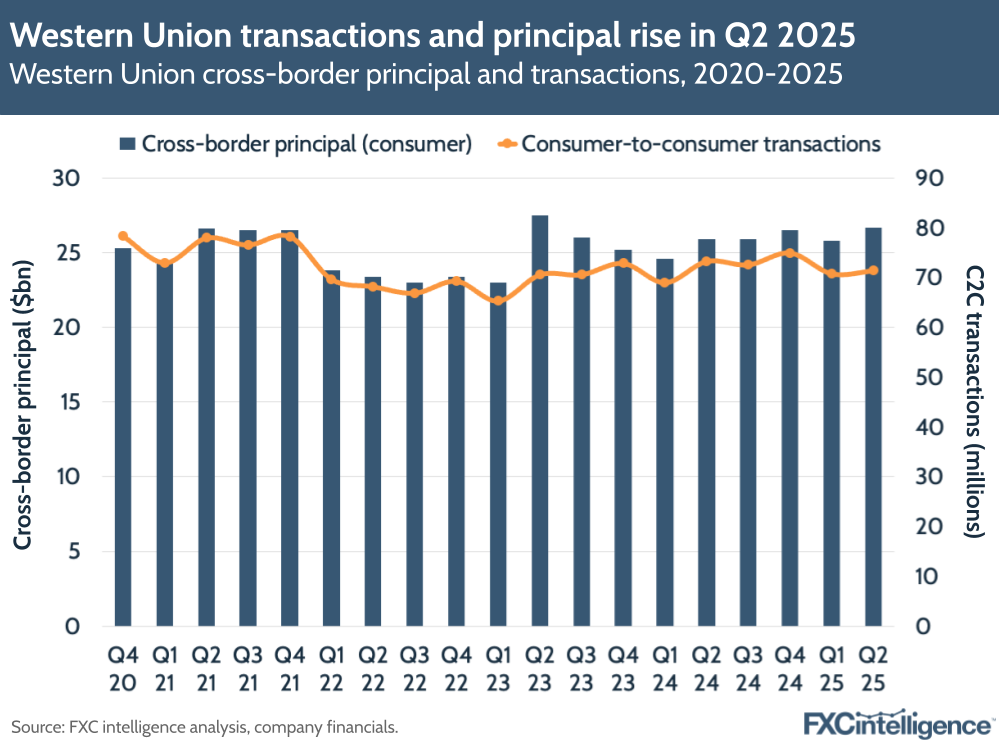

Consumer Money Transfer (CMT) revenue fell by -6% (adjusted to exclude revenues from Iraq, where the company has seen reduced contributions after suspending services). Transactions declined by -3% – the first time this metric has fallen since Q1 2023 – on the back of uncertainty around immigration policies, particularly in the US. However, the company’s total cross-border principal grew 3% to $26.7bn, which drove principal per transaction up by 6% for the quarter excluding Iraq.

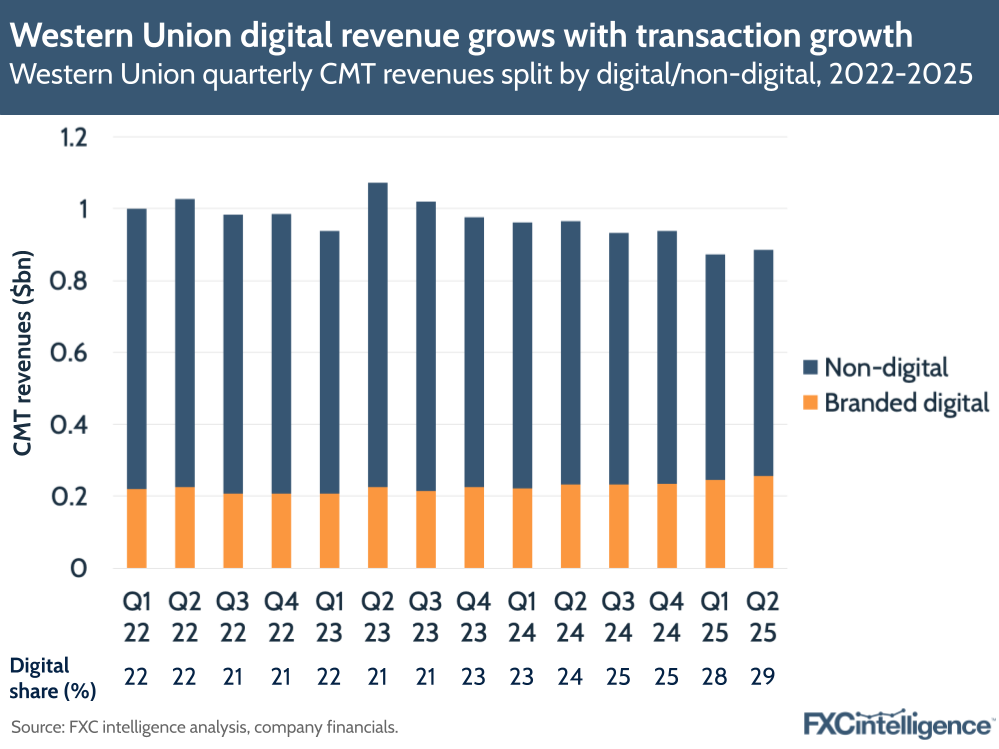

Though transfers are down overall, Western Union continues to see traction in digital, with branded digital transactions rising 9% (adjusted) and accounting for 29% of CMT revenue (around $257m).

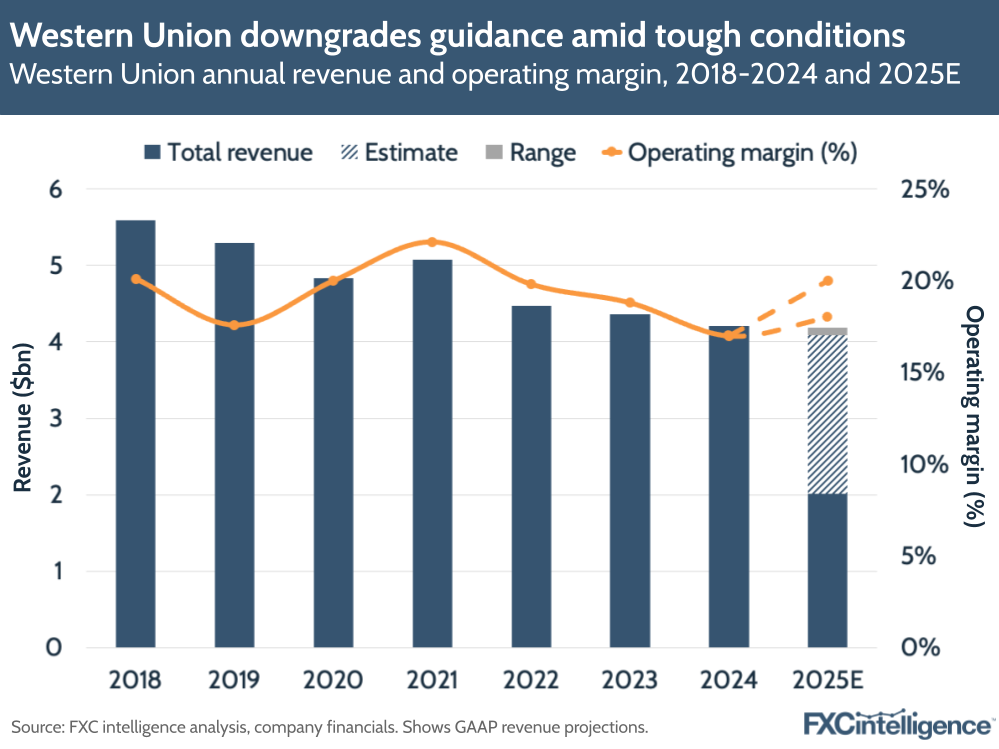

After another tough quarter, Western Union has decided to amend its guidance and now expects the company to deliver adjusted revenue in the range of $4.04bn-4.14bn – down from $4.12bn-4.22bn previously – with an operating margin between 19% and 21%.

This new revenue range would equate to a -2 to -4% decline in FY 2025, which would miss the 2% revenue growth projection for 2025 originally set out in Western Union’s Evolve 2025 strategy back in 2022. However, the company said it continues to implement this strategy, which is “focused on returning Western Union to sustainable, profitable revenue growth”.

On the plus side, the company did note that it is continuing to see significant productivity gains and cost savings as a result of using AI, with a 50% reduction in customer service handling time and improved call sampling. This brings Western Union in line with other players in the cross-border space who are seeing tangible benefits from AI.

Inside Western Union’s stablecoin strategy

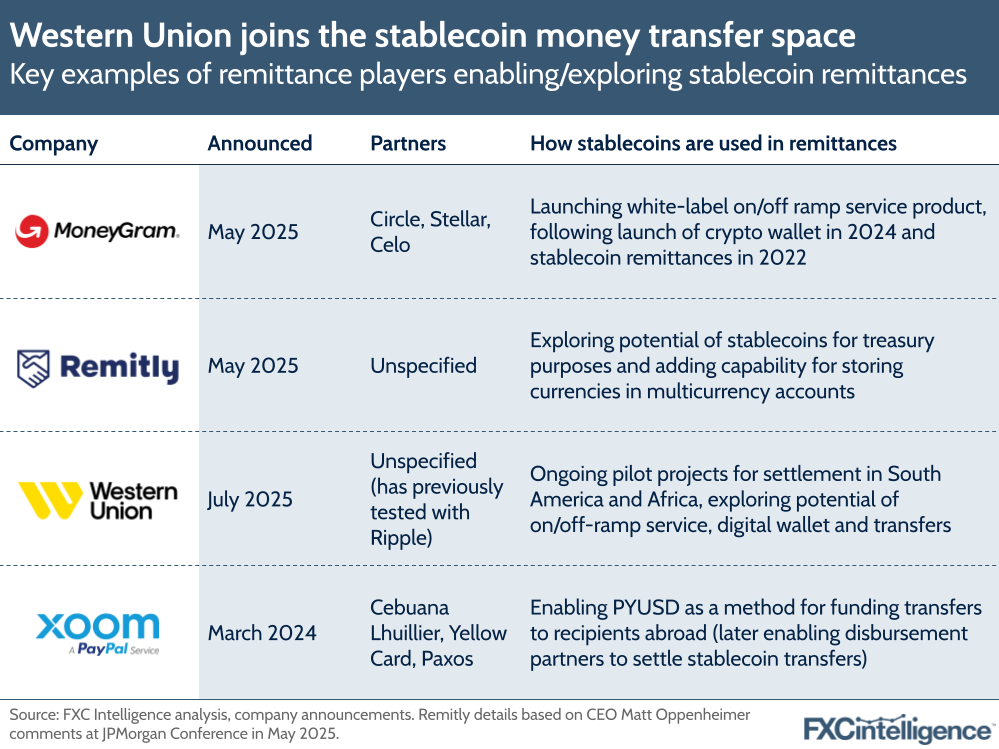

Having historically steered clear of crypto, Western Union is now one of several cross-border payments companies to emerge with a stablecoin strategy in the wake of the US GENIUS Act, which has given clarity to many players around the use of USD-pegged digital currencies.

The transfer provider has identified several opportunities for stablecoins, particularly in its potential for treasury operations, enabling faster settlement speeds and lowering the requirements for partner funding. It has already begun testing programmes to leverage stablecoin settlement in South American and African markets.

Specifically, Western Union is exploring how its network could be used to create an on/off-ramp for digital assets in emerging markets. It’s also looking at enabling customers to make global payments with stablecoins, as well as buy, sell and hold cryptocurrencies in their digital wallets.

“The goal is to reduce dependency on legacy correspondent banking systems, shortened settlement windows and improved capital efficiency, all without compromising compliance, transparency or customer experience,” said Western Union CEO Devin McGranahan during the earnings call.

“These innovations align closely with our broader strategy to modernise the movement of money and we believe they could ultimately improve our ability to manage our global liquidity.”

McGranahan added that a key challenge (and opportunity) is off-ramping to local fiat currencies in various countries worldwide, noting that there is a particular opportunity for this in Asia, Central America, South America and Africa.

“We see it as a natural evolution for us, given what our capabilities are around the world and the value we can provide as the payments world digitises towards blockchain-based platforms,” he said.

Western Union’s move into stablecoins comes well after MoneyGram, which first began offering the ability to send remittances in USDC in 2022 and has since expanded to offer a white-label on-ramping and off-ramping solution based on its network.

However, given Western Union’s size and scale across the industry – serving more than 150 million retail customers across 200 countries – the commitment to stablecoins remains a significant marker for the remittances space.

Digital drives transactions despite slowdown in key corridors

Aligning with stablecoin developments, Western Union is continuing its push into the digital money transfer space. Branded digital transaction volumes grew 9% YoY in Q2 2025, with revenue growing 6%, marking the eighth consecutive quarter of growth.

The company also noted that payouts to accounts grew by nearly 30% YoY and represent around 40% of digital volumes – Western Union is trying to grow the number of payments directed to accounts, having negotiated lower account payout rates during Q2, as these payouts come with “higher margins and a much stickier customer relationship”.

Having said this, it did see a slowdown in payout-to-account volumes across a number of corridors, including Mexico, Venezuela, Haiti, Dominican Republic, Colombia and Ecuador.

Digital transactions grew well in the Middle East and APAC, but Western Union is seeing a slowdown from the US to Latin America, led by the US to Mexico corridor (which was also seen in its retail business). During the call, the company noted that policies to crack down on immigration to the US are creating short-term headwinds in this core market, speculating that the moves can lead to reduced transactions and even shifts to less formal remittance channels.

As part of this, the company also referenced the new 1% tax on remittances, effective on cash-based retail transfers from the US from 2026. It said that around 50% of Western Union’s US CMT transactions are funded digitally or through cards, leaving less than 20% of the company’s revenues exposed to retail-based transactions – and this could drop to 15% or less as debit card adoption increases in the US.

The company is building infrastructure to collect and remit the tax, as well as giving customers non-cash remittance options at checkout (i.e. through the Vigo Money wallet). However, it said the tax is “not likely to have a meaningful impact on our business going forward”. If anything, McGranahan says it is an “incentive”.

“We’re hoping to spur people to want to open Vigo wallet accounts, which will help us build that product without having to spend an enormous amount on marketing,” he said.

Western Union sees faster growth in non-core markets

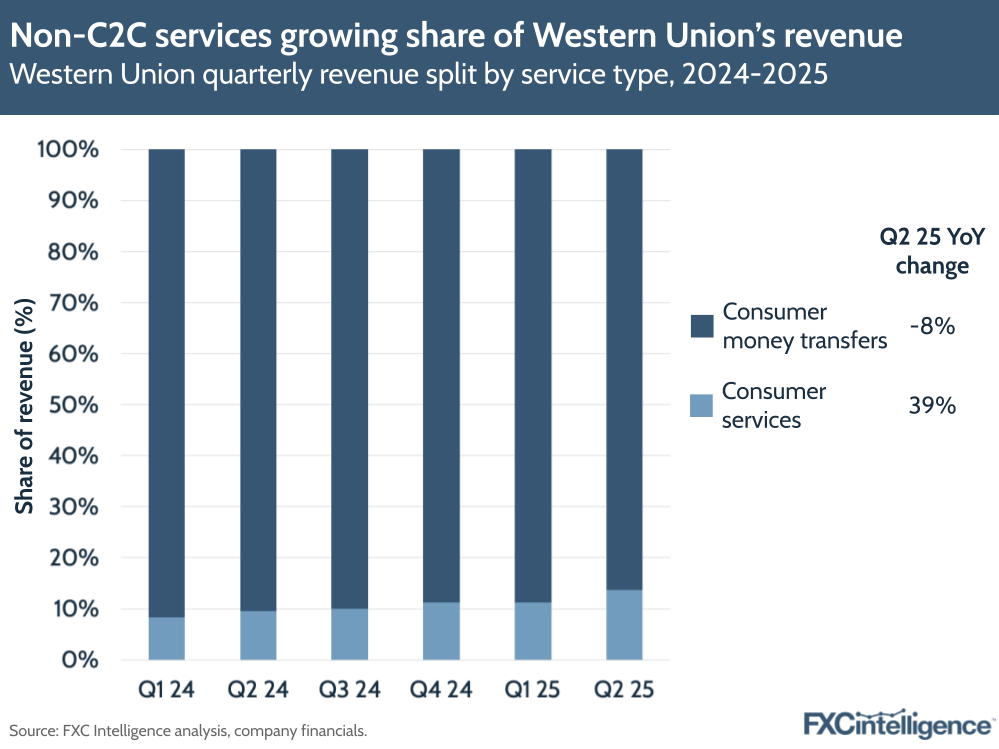

While transactions are down, Western Union is continuing to see traction in its non-C2C transfer segment, Consumer Services, which grew 41% on an adjusted basis during Q2. It accounted for 14% of the company’s revenue, up from 10% in Q2 2024.

This segment is being driven by the company’s Travel Money business, with more than half of the growth being due to the company’s acquisition of foreign currency provider Eurochange at the start of April 2025. Other drivers included Western Union’s bill-pay and media network businesses.

On geographies, Western Union’s biggest market, North America, accounted for 39% of Q2 CMT revenues, followed by the EU and the Commonwealth of Independent States (CIS) at 29%; Middle East, Africa and South Asia (MEASA) at 15%; Latin America and the Caribbean (LACA) at 11%; and Asia-Pacific (APAC) at 6%.

However, the growth figures tell a different story, with North America down -11% YoY, while MEASA down -23%, LACA down -13% and APAC down -2%. However, EU & CIS grew 6%, with Western Union noting 15% retail revenue growth across Spain and the UK. During the call, the company even mentioned that it was hoping to transfer its European model to the US to improve its coordination in payout markets.

The changes in Western Union’s revenue mix signal a company that has faced significant challenges and disruption in its core markets, but also one that is striving to capture new opportunities and continue its advance into digital. The movement of the long-established money transfer player into the stablecoins market could have ripples across the remittances space this year.

How can I track the use of stablecoins in cross-border payments?