Wise’s continued investment in infrastructure and active customer growth drove revenue and profit in its H1 2025 results. We spoke to the company’s CFO Emmanuel Thomassin and Director of Finance Martin Adams to explore what’s driving the company’s growth and how it plans to capture more of the market going forward.

This week, money transfer provider Wise released its results for H1 2025 (spanning calendar Q2 2024 and Q3 2024), in which the company once again saw solid growth on the back of customer increases and network expansion.

Revenue grew 19% to £591.9m, while the company’s profit before tax was also up 57% to £147.1m. Wise’s share price continued to climb after its results, having already seen a boost from the announcement of a Wise Platform partnership with Tier 1 bank Standard Chartered earlier this week.

Wise has expanded its customer base through word-of-mouth marketing and acquiring licences in new regions, with a network that now serves more than 160 countries and more than 40 currencies. As a result, active customers during the half grew by 25% to include 11.4 million people and businesses, with total volume sent across borders increasing by 19% to £68.4bn. Of this figure, Personal volumes grew 20% to £50.6bn while Business volumes grew 18% to £17.7bn.

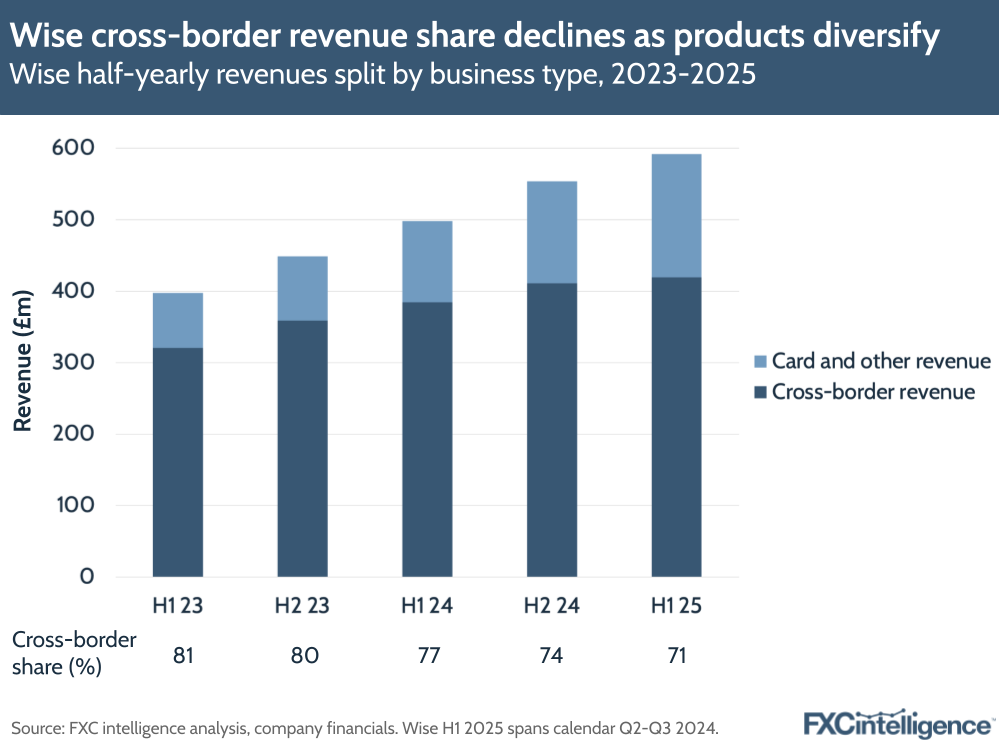

As the company has grown its number of Wise Account customers, it has also received a boost from interest income. Account holders are also driving the growth of Wise’s card business. While cross-border revenues rose 9% to £419.1m, card and other revenues rose 52% in H1 2025 and accounted for 29% of revenues against 23% last year.

This half saw a strong focus on infrastructure, with the company receiving approval to directly connect with local instant payments infrastructure in the Philippines, Japan and Brazil, in addition to new licence developments that will boost the company’s products in India and Australia.

To find out more about the company’s strategy moving forward, we spoke to the company’s CFO Emmanuel Thomassin and Director of Finance (FP&A, IR) Martin Adams.

Drivers of Wise’s H1 2025 results

Daniel Webber:

Let’s take it from the top: another really excellent set of results. What drove growth in H1?

Emmanuel Thomassin:

This is based on the activity of our customers, right? We saw their activity grow by 25%, which is a prerequisite for growth of our business. This is coming from our new customers and our existing customers.

From the new customers that are coming on the platform, 70% of them are coming because other customers are happy about it, because they’re recommenders. That continues to be one of the number one acquisition channels, which is very nice.

As a CFO, you like it because basically it doesn’t cost you anything. But it’s also a good barometer to measure the satisfaction of your customers. Because once you seem to see maybe an opposite trend, then you have to ask, “Do I provide the right services?”

Today I can say, “70% is really good feedback to get.” This is the best NPS score that you can get from customers at this point.

Martin Adams:

In terms of the numbers, as Emmanuel was saying, we’ve seen strong growth across the Personal side, which grew 25% year-on-year, H1 to H1, and 11% on the business side of things.

From a cross-border perspective, actually the business side grew 18% to £17.7bn of cross-border volume. On the personal side of things, this grew by 20% year-on-year to about £51bn. So in total, we moved £68.4bn in the first half of the year. It’s up 19% year-on-year, 21% on a constant currency basis.

As you’ve heard before from us, the main driver of this is the growth in customer numbers. There’s been chat in the past in terms of things like the volume per customer (VPC), but as you know, as a business, we’re trying to grow the number of customers – we’re trying to grow the volume in absolute terms – so VPC is less relevant for us.

Then all of these customers that are joining us and using the Wise Account now on the personal side of things and on the business side, we see them holding even more money with us either in their account or in the assets product. In aggregate, this grew by 31% year-on-year. We’re now holding either assets under custody or assets in the account totalling £18.5bn of our customers’ money, so an important sign of actually how much they trust us as an organisation.

Emmanuel Thomassin:

It’s a bit of a second confirmation to the 70%. Not only are they happy with you – they’re happy with the application, they’re finding it seamless, their experience is great – but then on top of that, they trust you with more money. So if you want a second NPS score, here we go.

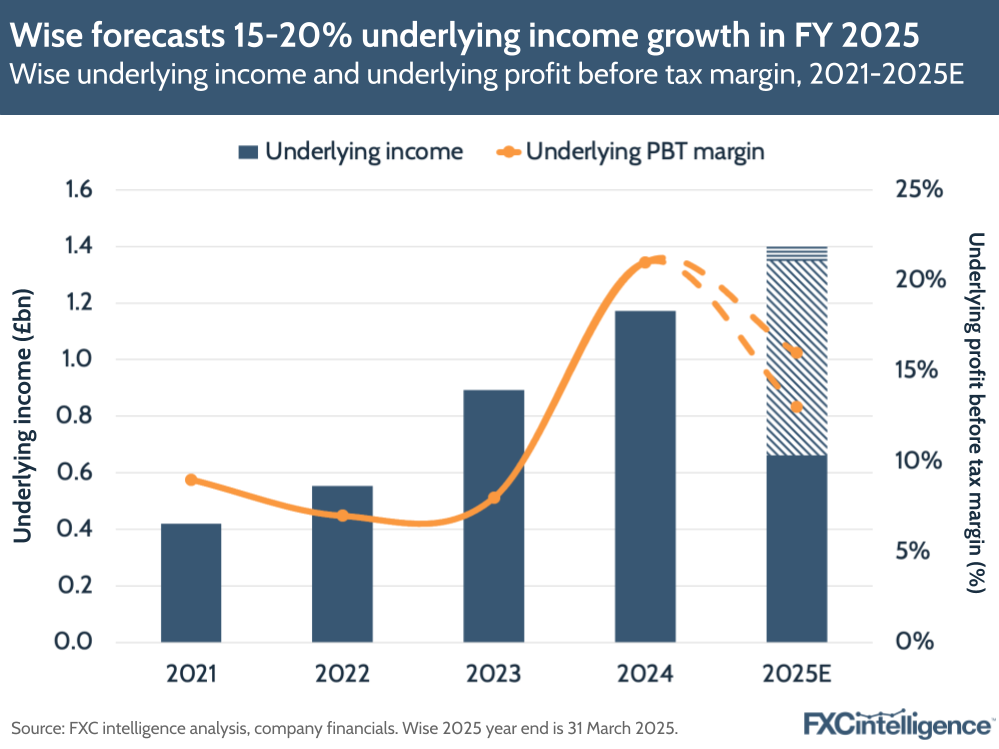

Wise maintains forecast on underlying income

In its FY 2024 results, Wise had shifted its financial projections to focus on underlying income growth – which captures revenue plus the first 1% gross yield – alongside underlying profit before tax (i.e. PBT against this income). This was to reflect the growing impact of interest rates and customers holding balances at the company (discussed in more detail below).

On a quarterly basis, Wise’s underlying income grew 17% to £337m, bringing its H1 underlying income to £662.4m. Based on these results, the company has opted to maintain its previous guidance of 15-20% underlying income growth for 2025 and in the medium term, as well as an underlying PBT of 13-16%.

Segmenting Wise’s Personal customers

Daniel Webber:

You’ve traditionally focused on the expat customer in corridors such as UK to US, but if you’re doing UK to India, for example, that’s a different type of customer. How are you thinking about your Personal customer segments?

Martin Adams:

The first point to make is that, as you know, there are other providers of this service that are very focused on particular verticals like healthcare and education, etc. But because of the strategy that we’re working towards in terms of enormous scale over the longer term, what we do is we approach this from the perspective of the common factors across different use cases that are valuable to customers.

We know the problems that they face when they use the banks and some other providers are that it’s expensive, it’s slow, it’s inconvenient. They don’t actually know what they’re paying.

When we develop the products, we’re trying to solve for these problems. It doesn’t really matter from our perspective whether you’re moving money to purchase a house or to pay for a healthcare bill or to send money home each month. The common factors are you want it to be quick and reliable, convenient, as cheap as possible and you want to know what you’re actually paying.

So this is actually how we approach it and it doesn’t matter what the use case is: these are the common principles across all of our customer base. So when we go to market, this is really what we’re leading on. We’re leading on these factors rather than trying to focus on particular use cases.

Wise’s revenue split and diversification

Looking specifically at the company’s revenue breakdown highlights the extent to which Wise is diversifying its revenue streams. Card-related and other revenues rose by 52% in H1 2025, and accounted for 29% of revenues (versus 23% in H1 2024).

This is being driven by a growing number of customers holding accounts with Wise. Customer balances held in accounts rose by 20% to £14.7bn, with Personal balances rising 29% to £9bn while Business balances rose 8% to £5.7bn.

Wise’s cash-free approach

Daniel Webber:

What has driven your decision to not do cash? It seems that the user experience you want to give – the customer experience, the speed, the transparency – is not possible with a cash funding or pay-out experience.

Martin Adams:

Price is important for everybody. But when we consider the demographic of the customers that are typically using some of those traditional players like Western Union, those customers are becoming increasingly digital in terms of how they send money.

There is this increasing digitalisation. There is a question over how quickly that happens, but we also think the better we can do our job in terms of reducing prices, the more compelling it will be for people to actually go digital and save a lot of money when they remit these funds each month.

With Wise, we are looking over the longer term.The opportunity here is enormous and we have to choose what we spend our time on. We think that having the engineers and the product specialists spending their time on things like the connections into these domestic payment systems is the fastest route really to achieving our mission and getting the price down.

In time that will make it even more compelling for those customers that are remitting cash today to switch and go digital, hopefully through Wise.

Wise’s consumer revenues grow faster than business

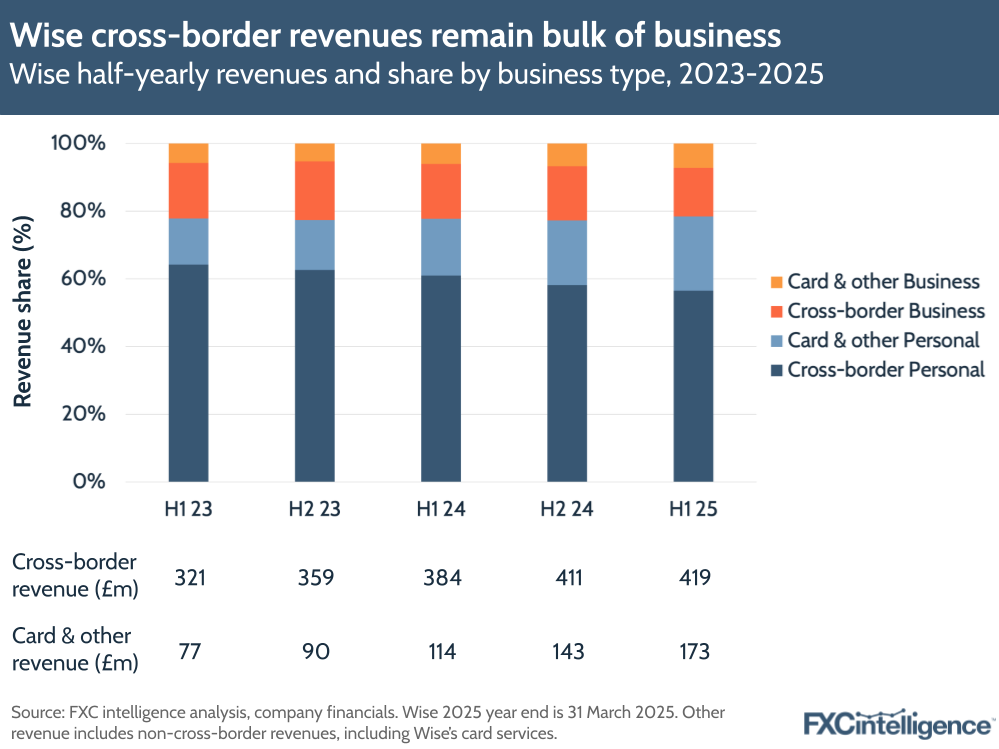

Consumers are still driving Wise’s bottom line, accounting for 80% of cross-border revenues in H1 2025 and 75% of card and other revenues.

Personal revenues accounted for £464m of Wise’s total revenues in H1 2025, equivalent to 78% of its total revenues, against £128m from Business customers. Personal growth outstripped Business growth this half, with cross-border revenues rising 10% for the Personal segment against 5% growth for the Business segment.

Personal active customers grew 25% to 10.8 million versus 11% growth in businesses to 523,000 (though this reflects a longer pipeline for adding Business customers). Underlying income rose 21% for the Personal segment, versus 14% growth in the Business segment.

Strategies around Wise Platform

Daniel Webber:

Let’s talk about Wise Platform, which is reported across Personal and Business rather than broken out separately. You had a great partnership announcement earlier this week with Standard Chartered. Talk us through that announcement and how you’re thinking about Wise Platform.

Martin Adams:

As you can imagine, we were really pleased. We’re pleased with all of the partnerships that we’re able to announce. Earlier this year, we announced Nubank, which was fantastic, Quonto, growing so quickly in Europe for small businesses, and now Standard Chartered, a Tier 1 bank.

The signal that it sends in terms of how compelling it is to use the Wise infrastructure via Wise Platform is there for everyone to see, and it’s also a demonstration of how we can grow a relationship.

We started off this relationship by providing Standard Chartered’s neo-bank Mox out in Hong Kong with access to the infrastructure. And now we’ve announced this expansion of that relationship as well. No relationship is going to start with 100% of everything from day one.

This is the same when we talk about Wise Platform, Wise for business or Wise for individuals, but fundamentally, these three products are ways for people, businesses and banks to access our infrastructure.

Then it’s the question of what is it that people like about this infrastructure?

It’s the fact that it spans 160 countries. We’ve got the capacity across 40 currencies to be held within accounts. 63% of payments are instant. The average price is below 59 basis points now. The reliability is there. We’ve got the customer support if platform partners want this as well. We’ve got 24/7 support again for those that want this.

So it’s really the infrastructure that they’re buying into and these stats around how quick and low-cost the infrastructure is as well as the coverage. This is fundamentally what sells Wise Platform.

Daniel Webber:

Is there any colour that you can provide on Wise pricing dynamics, given that it’s a blended number between Platform and your direct customers?

Martin Adams:

Fundamentally, whether it’s through Wise Platform or any of the other products, we’re fundamentally pricing on a cost plus margin basis. To the extent that there are different costs involved, there will be different prices involved and different economics within these things.

To the question around what role is this playing within the overall price, we talk about it a lot for Wise Platform because the long-term potential of this is huge. In the short term, it’s still a very small part of our overall volumes and therefore, it’s not having a significant impact in terms of mix within our broader financials.

Wise’s cross-border pricing strategy

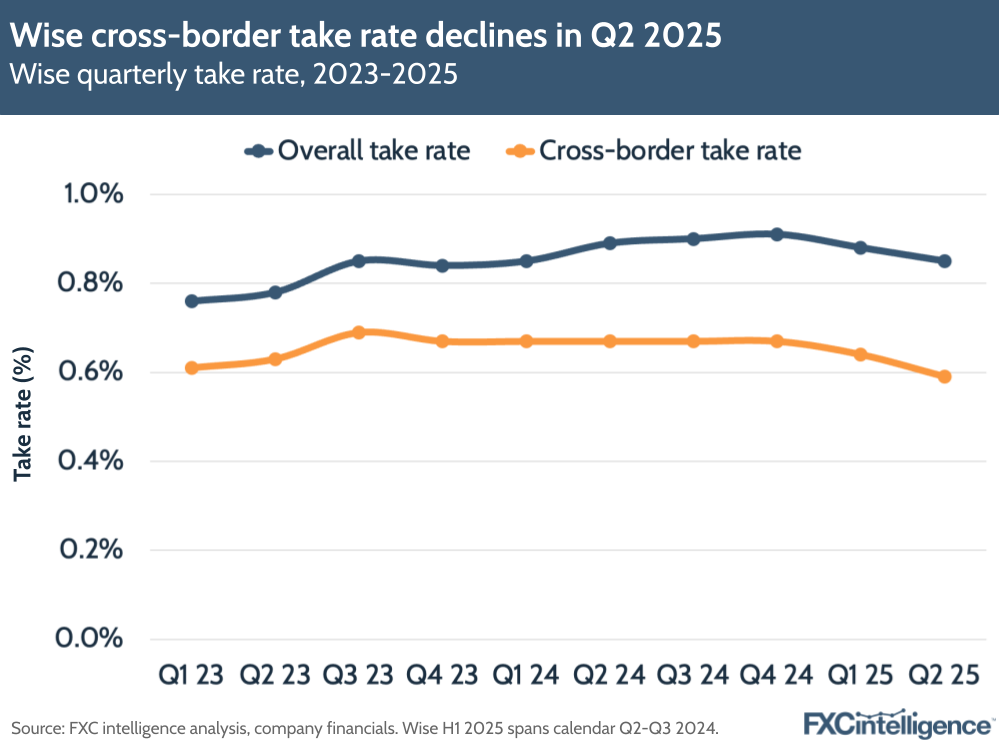

Wise reduced its pricing earlier this year, part of its strategy to boost its appeal to consumers, and this has been reflected in its take rate. On a quarterly basis, the company’s cross-border take rate declined by 8 bps to 0.59% in Q2 2025, while in H1 2025, it declined 5 bps to 0.61% compared to H1 2024’s 0.67%.

The company said that its investments in pricing in the first half of FY 2025 are expected to help it move closer to achieving its target underlying PBT of 13-16% in H2 2025 from an elevated position of 22% in H1. As well as making cross-border payments cheaper, Wise aims to make them faster, with 63% of transfers being instant on the company’s network, versus 60% this time last year.

Wise’s India outbound play

Daniel Webber:

You’ve been developing your offering in India outbound, including expanding your licence there. How do you see the India opportunity?

Martin Adams:

India is a great example of how we approach this, like we do everywhere, on an incremental basis. We launch and we get a licence and then we take the next licence. And as part of this release, we were talking about how we’ve now gotten an authorised dealer II (AD-II) licence which allows us to remove the $5,000 cap on sending out of India.

It’s all incremental: none of this stuff happens overnight, but it’s about doing what we can to expand our operations and our licensing and our customer base bit by bit in India. Then, over time, just as in every other country, as we develop what we have there, our infrastructure, this allows us to begin to scale our unit costs and become more competitive on price and the service that we provide.

Fundamentally, this is the approach that we’re taking in India, just as we have in every other country.

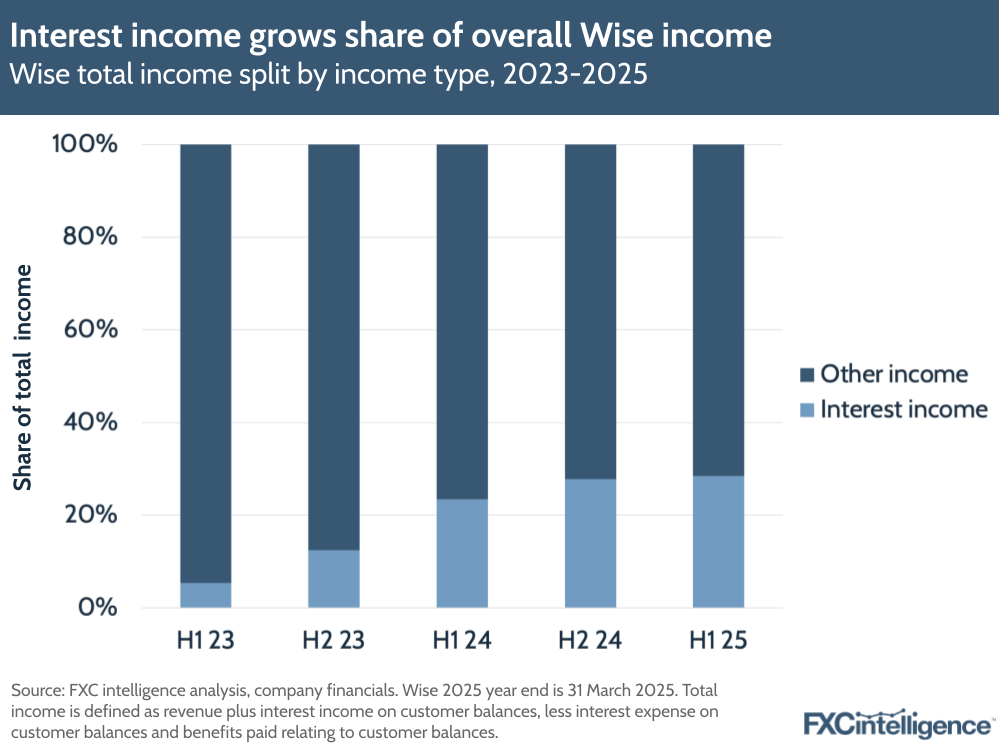

Wise interest income grows share of overall income

Wise continues to see an impact on its overall income from interest held on customer accounts. Interest income above the first 1% yield rose by 50% to £230.2m in H1 2025. This was due to overall 23% growth in average customer balances.

The company said that out of the £230.2m, it was intended for 20% (£46m) to be retained while aiming to return the remaining 80% (£184.2m) to customers, under Wise’s interest income framework. However, in the end £84.8m (37%) was paid out to customers, with the company saying the majority of this related to the UK, where it cannot directly pay interest to Wise account holders under the terms of its licence.

Wise has maintained that the company is “highly profitable with limited reliance on interest income”, with its underlying PBT (which excludes any customer benefits being paid out) rising 57%. However, it has repeatedly said it wants to grow the amount that it pays back to customers.

Wise Account’s impact on revenue

Daniel Webber:

Growing cards revenue is an interesting driver for your business. Talk us through how your Wise Account card offering is evolving and what the unit economics are there.

Martin Adams:

We haven’t disclosed the P&L for the cards alone, but cards and other is a significant chunk of our revenue now and it’s growing very quickly.

Card and other revenue grew by 52% year-on-year, and this really just does reflect the resonance of the Wise Account, people opening a Wise Account, holding money in the account, using the card. It’s growing really quickly, and if you think about our active customer numbers – those customers in a period who have been active from a cross-border perspective – it’s now around a fifth, about 20% of these, that are card-only within a period of time.

They’ve travelled, they’ve used the card, but they haven’t done a transfer by this definition within that period of time. Maybe in the next quarter, they do a transfer, they use the card as well, but it’s a significant proportion of our active customer base now.

Daniel Webber:

Is there interchange revenue on the card?

Martin Adams:

That’s correct, that’s how we generate revenue.

Daniel Webber:

We’re almost at time. Are there any closing thoughts you would like to share?

Emmanuel Thomassin:

What is amazing is, because we speak about Standard Chartered, the infrastructure that has been put in place, that continues to be put in place. This is the first Tier 1 bank, but it positively shouldn’t be not the last.

The more we invest in infrastructure, in speed and quality of service, the more it would become difficult for classic banks to compete with their quality of service. This is a starting point, and we will see volumes coming, moving towards Wise from these banks and new banks coming or further partners. So to focus on the fundamentals, like Wise has been doing for the last 14 years, is very, very important.

Daniel Webber:

Emmanuel, Martin, thank you.

Emmanuel Thomassin and Martin Adams:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.