Wise has reported its financial year 2026 results for the 12 months up to 31 March, in what is its first earnings release as a US-traded company. This has seen the company provide an update that both highlights ongoing growth while providing key positioning for US investors around the company’s strategic global plans.

Having switched to a dual listing when it began trading on the Nasdaq in May, Wise has switched to reporting in line with standard US accounting practices, which primarily sees the company begin to report in US dollars rather than pounds sterling, but in some cases also share a slightly different mix of figures than it did as a company traded only in the UK.

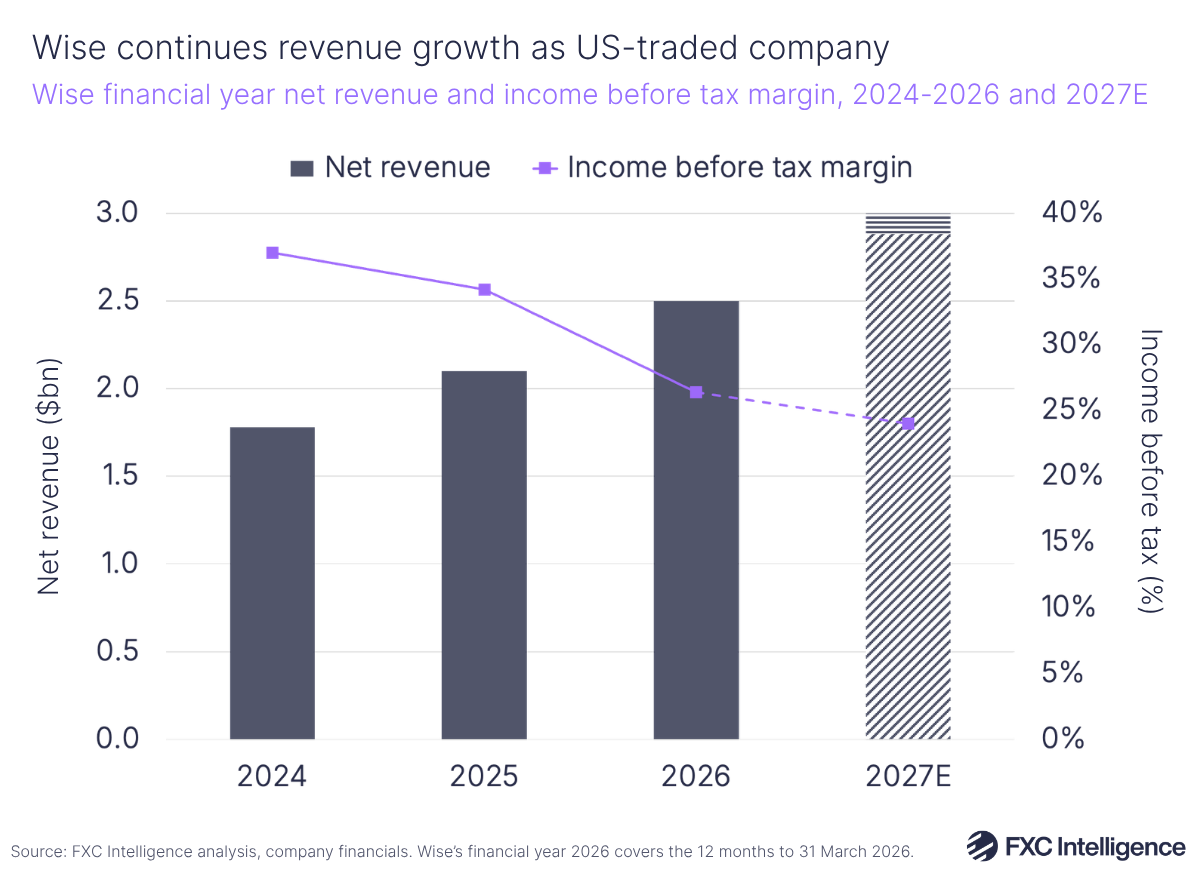

However, the top-line narrative continues, with Wise reporting a 19% YoY increase in net revenue to $2.5bn for FY 2026. It expects to see net revenue achieve a medium-term CAGR of 15-20%, with FY 2024 as its base year, putting this at the top end of its range, and has given the same guidance range for FY 2027, which could see the company cross the $3bn mark for the first time if it achieves the top end of this.

The company has also seen its income before tax margin – Wise’s preferred metric that tracks very closely to, although several basis points below, EBITDA margin – drop to 26% versus FY 2025’s 34%, with the payments major projecting “around the top” of the 20-25% range for FY 2027.

This is not being framed as a drop so much as “healthy levels of profitability”, offset by the company returning as much interest income to its customers as it can and continuing with its mission of driving down the cost of consumer money transfers. This has seen it continuing to reduce its cross-border take rate each quarter, which stands at 0.51% as of Q4 2026 compared to 0.64% in Q1 2025.

This narrative appears to have chimed positively with investors, with the company seeing its share price climb by more than 10% following the earnings release.

Wise’s first US earnings show increasingly global focus

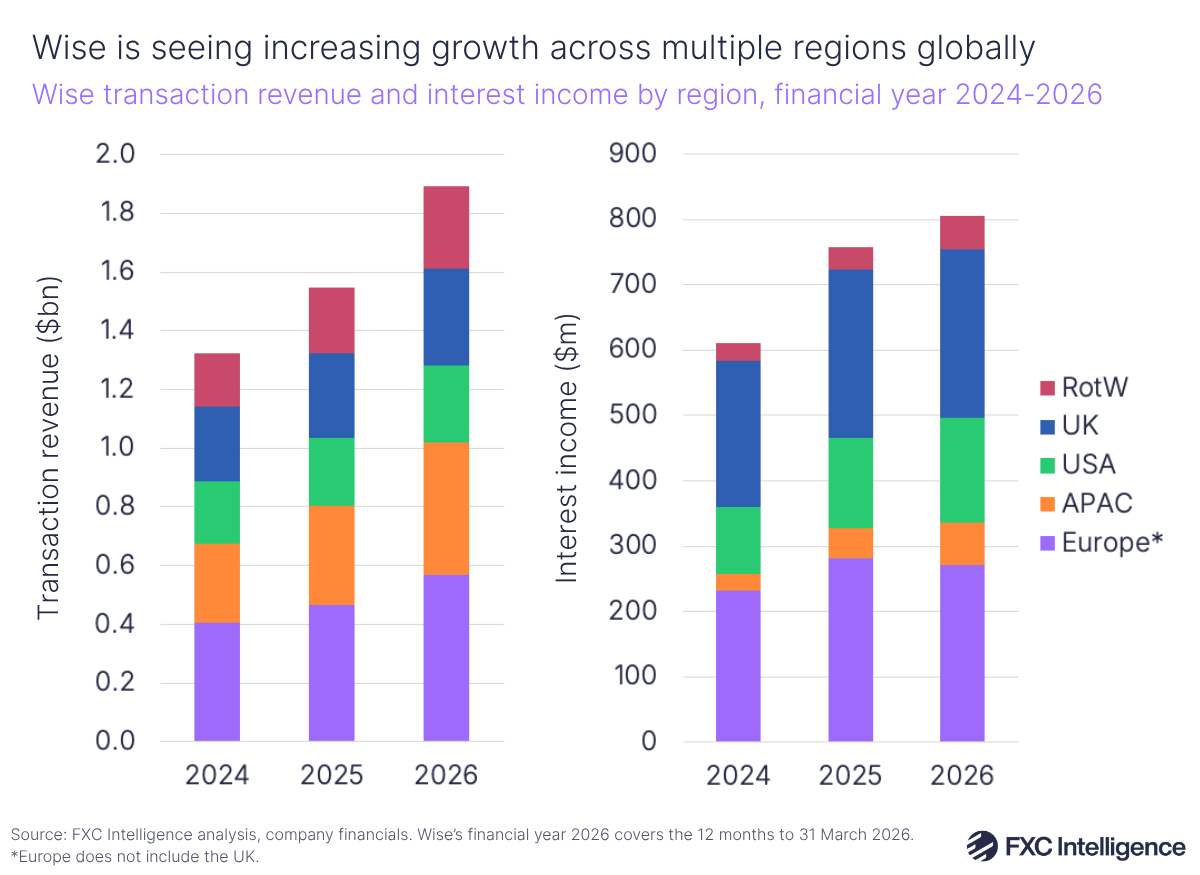

Wise has traditionally seen much of its business come from the UK and mainland Europe, which still dominate its revenue, however there is increasing diversification as the company expands internationally.

In FY 26, the company saw Europe account for 30% of transaction revenue – that is, revenue not attributable to interest income – while the UK accounted for 17%. On net revenue, the story was similar, with Europe accounting for 28% and the UK 23%.

However, while Europe saw a 20% YoY increase in net revenue, one percentage point above the company’s overall growth, Wise’s original market of the UK has seen growth slow from 14% YoY in 2025 to 7% YoY in 2026. Meanwhile, the US, one of Wise’s other longstanding markets, saw 15% YoY growth in net revenue to maintain a 15% share.

The strongest growth was instead seen in Asia-Pacific, with net revenue growing 35% YoY to take a 21% share, while the rest of the world saw 25% YoY growth for a 13% share. Combined, markets outside of Europe still remain slightly below Europe and UK on net revenue share but have grown closer over time, with non-European markets accounting for 48% of net revenue in FY 26.

In support of this, the company has continued to build its infrastructure internationally, in particular highlighting direct connections into the Japanese and Brazilian domestic payment systems that went live over the prior 12 months, as well as adding licences in key markets including South Africa, the UAE and Thailand.

Wise’s growth bolstered by diversified revenue

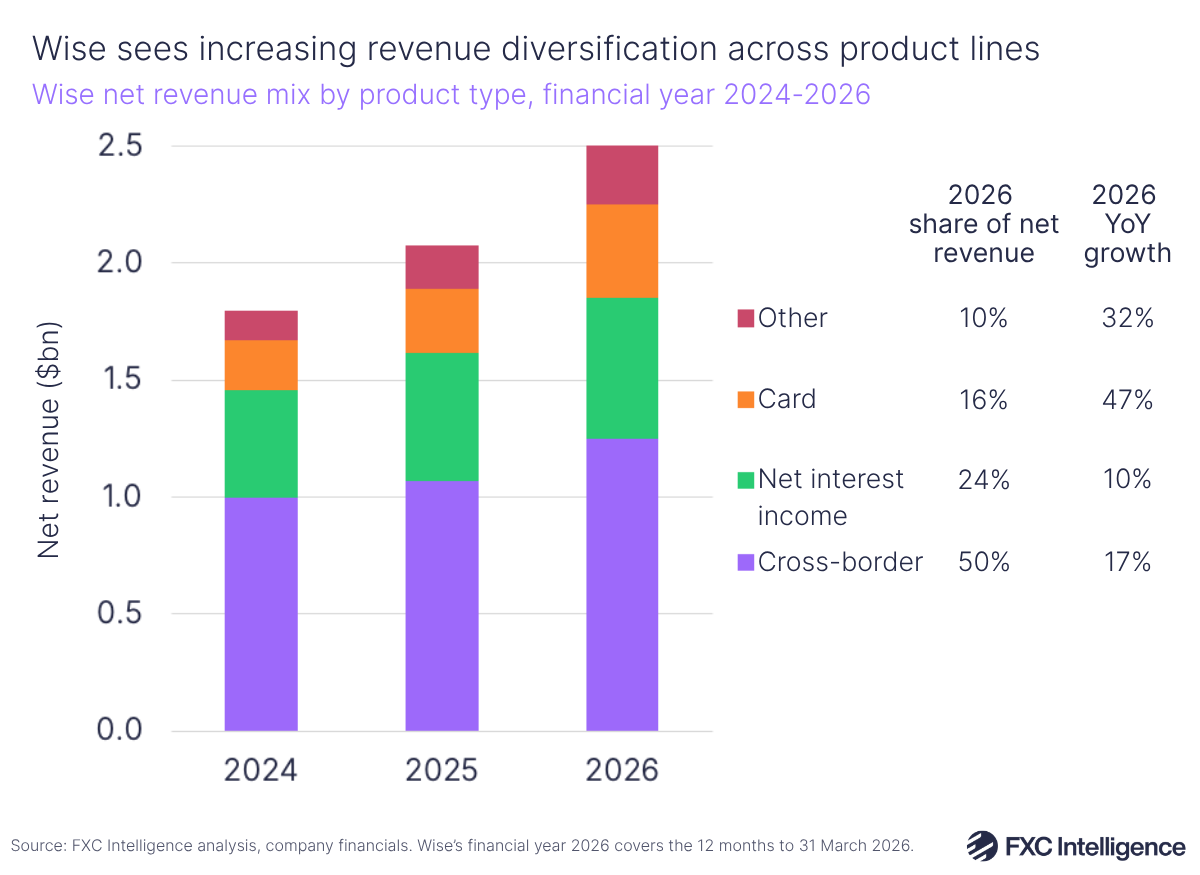

Revenue diversification also goes beyond geographies, with the company continuing to broaden its mix of net revenue from different product types.

Cross-border is its core product area, covering its money transfer services for consumers and businesses, however the company has been increasingly looking to increase its revenue from other value-added areas. This has seen cross-border revenue move from a 56% share in FY 2024 to a 50% share in FY 2026, despite seeing consistent growth.

By contrast, Card income from Wise Accounts and related areas has grown from 12% to 16% over the same period while Other, which covers solutions including domestic money transfers and its asset products, has gone from 7% to 10%.

Net interest income, which is directly impacted by the wider interest environment, has seen its share drop slightly from 26% to 24% between FY 2024 and FY 2026.

Cross-border volumes aided by Business, Wise Platform growth

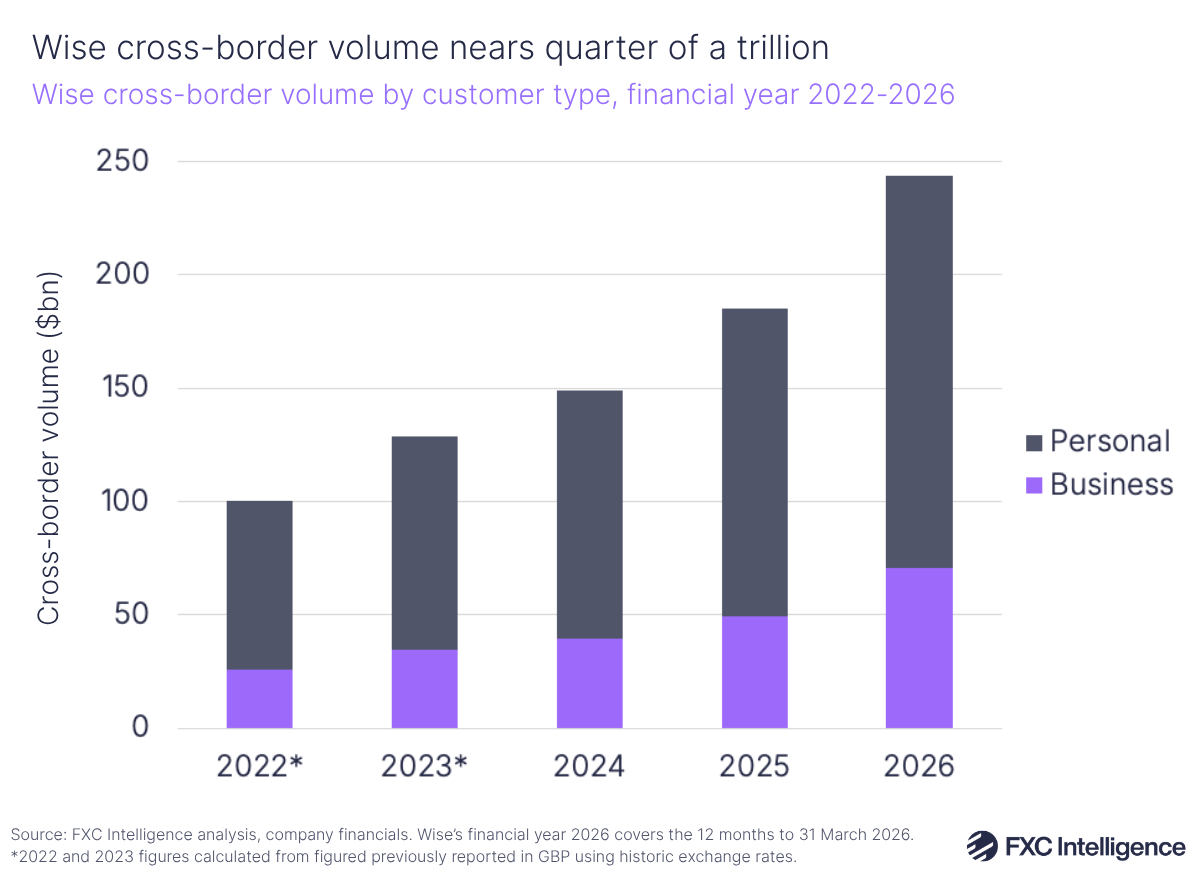

On money movement, the company has seen strong growth in cross-border volume, which saw its strongest increase in several years – at 31% to $243.5bn.

Within this, the smaller and more nascent Business segment has seen the strongest growth, climbing 42% YoY to $70.5bn, while Personal grew 27% to $173bn. While both segments have seen increased growth compared to 2025, Business in particular has seen a notable acceleration.

The company has also seen active customer increase by 21% to 18.9 million overall, with Business increasing 29% to 0.9 million, while Personal has increased 21% to 18 million. Volume per active customer has therefore grown for both segments, but has been more pronounced for Business, rising by 11% YoY.

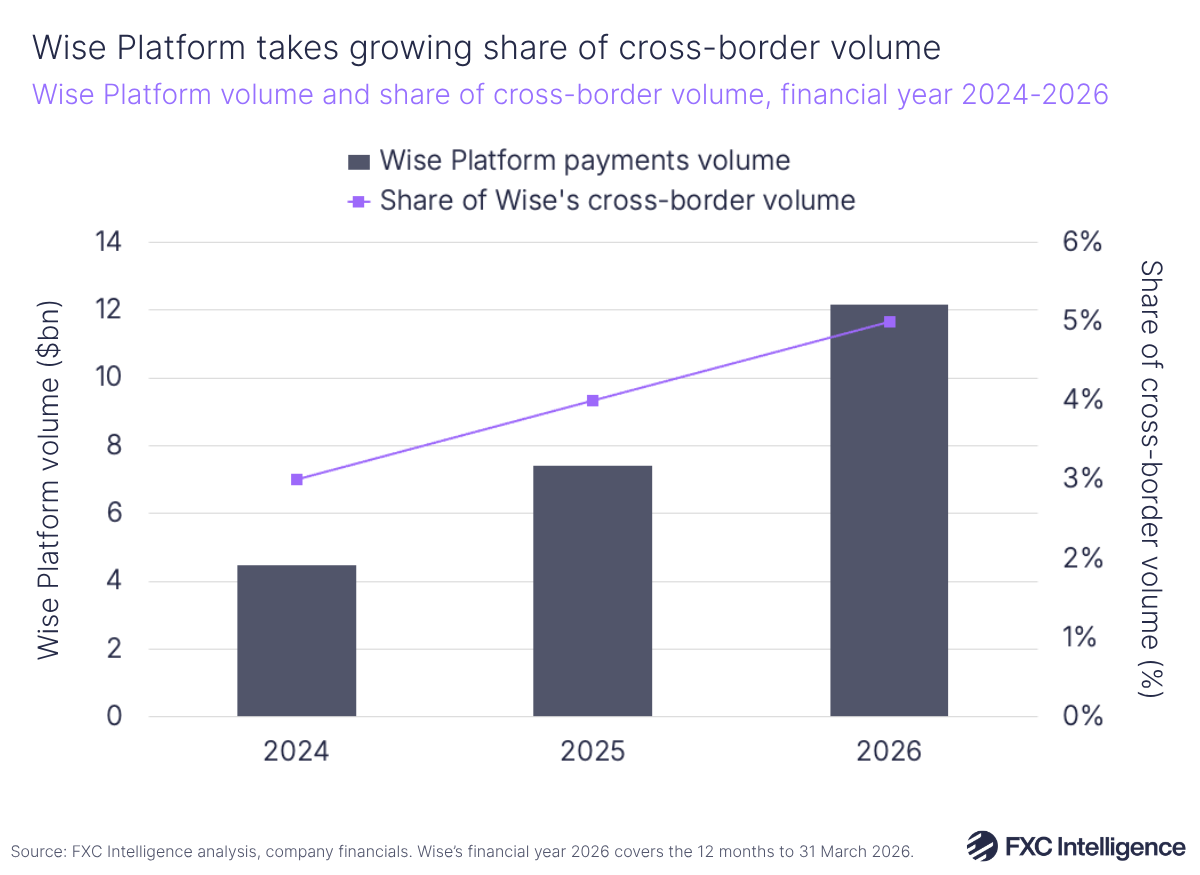

Wise Platform, the company’s network solution, is also reported to have seen stronger growth than its money transfers products, and now accounts for 5% of all cross-border payments volume, up from 4% in FY 2025. This puts volume moved on the platform in the financial year at around $12bn, representing around a 64% increase on the previous year, aided by signings including Raiffeisen, UniCredit and Malaysia’s MBSB Bank.

The company has previously stated that it expects Wise Platform’s share to reach 10% in the mid-term and 50% in the long-term, with CEO Kristo Käärmann saying on the call that the latest results put the segment on track to achieve this. He also highlighted South Africa’s Capitec Bank as having recently gone live on the platform, representing flows that do not form part of the current 5%.

However, Wise does not yet report direct revenue for Wise Platform, advising in its annual report that this is “not yet a material percentage (i.e., currently generates less than 10%) of the Group’s overall transaction revenue”, and instead recognising this largely within its cross-border revenue.

Wise Account sees growth in FY 2026

Another area that is helping driving growth is Wise Account, the company’s multicurrency account and card solution that also offers investment solutions in some markets via Wise Assets.

Overall, the company has seen the amount customers are holding with Wise climb notably over the past year, with overall customer holdings increasing 40% YoY to $39bn. Within this, account balances have grown 36% to $30bn, while holdings in Wise Assets have increased 55% to $9bn.

This growth has been aided both by increased use in existing markets and rollouts in additional markets, with Brazil seeing the launch of Wise Assets, and has also helped drive interest income, although the company’s continued effort to distribute 80% of this back to customers has muted this area of growth.

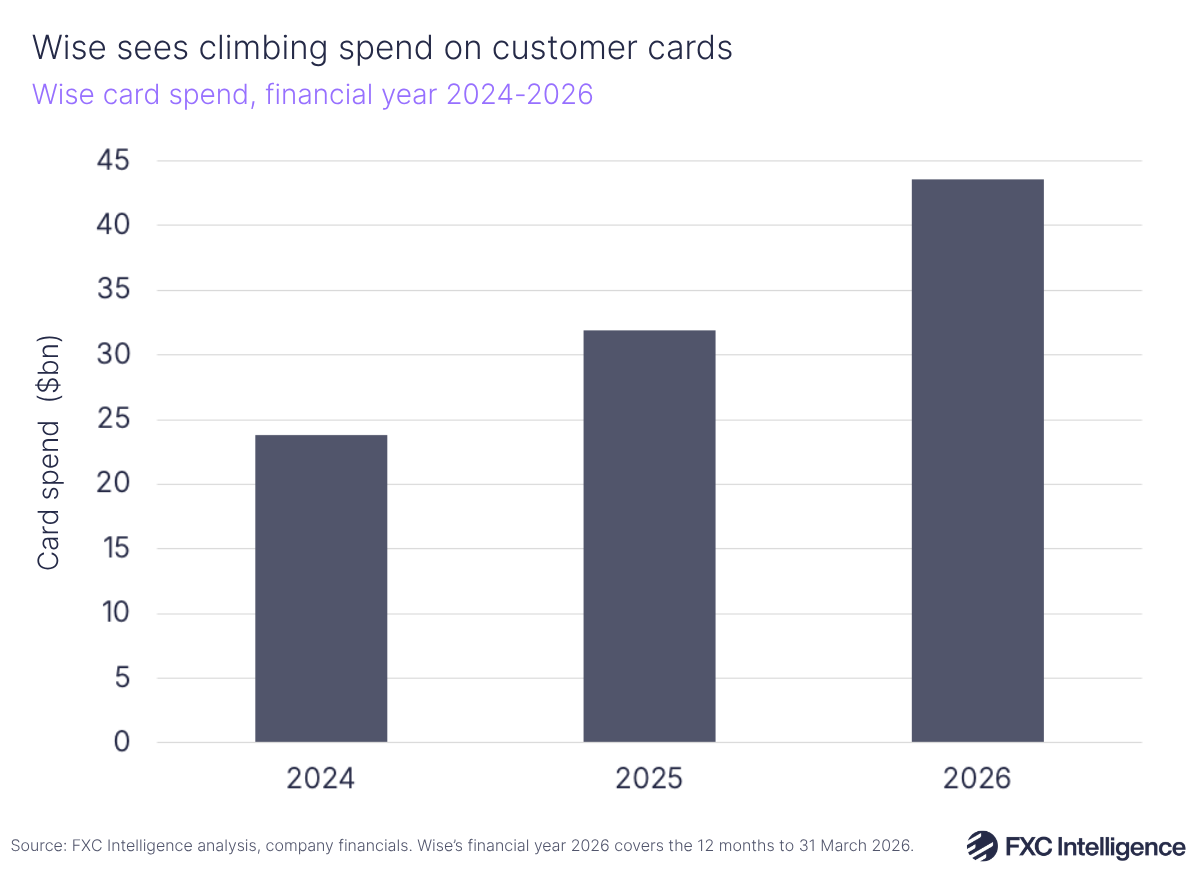

An increase in Account customers has also bolstered spend on customer cards, with Wise seeing card spend grow by 37% YoY to $43.6bn. This has driven increased card revenue, with the company highlighting the EU, Australia and the UK as being particularly strong areas of adoption.

Investment underpins increasing operating expenses

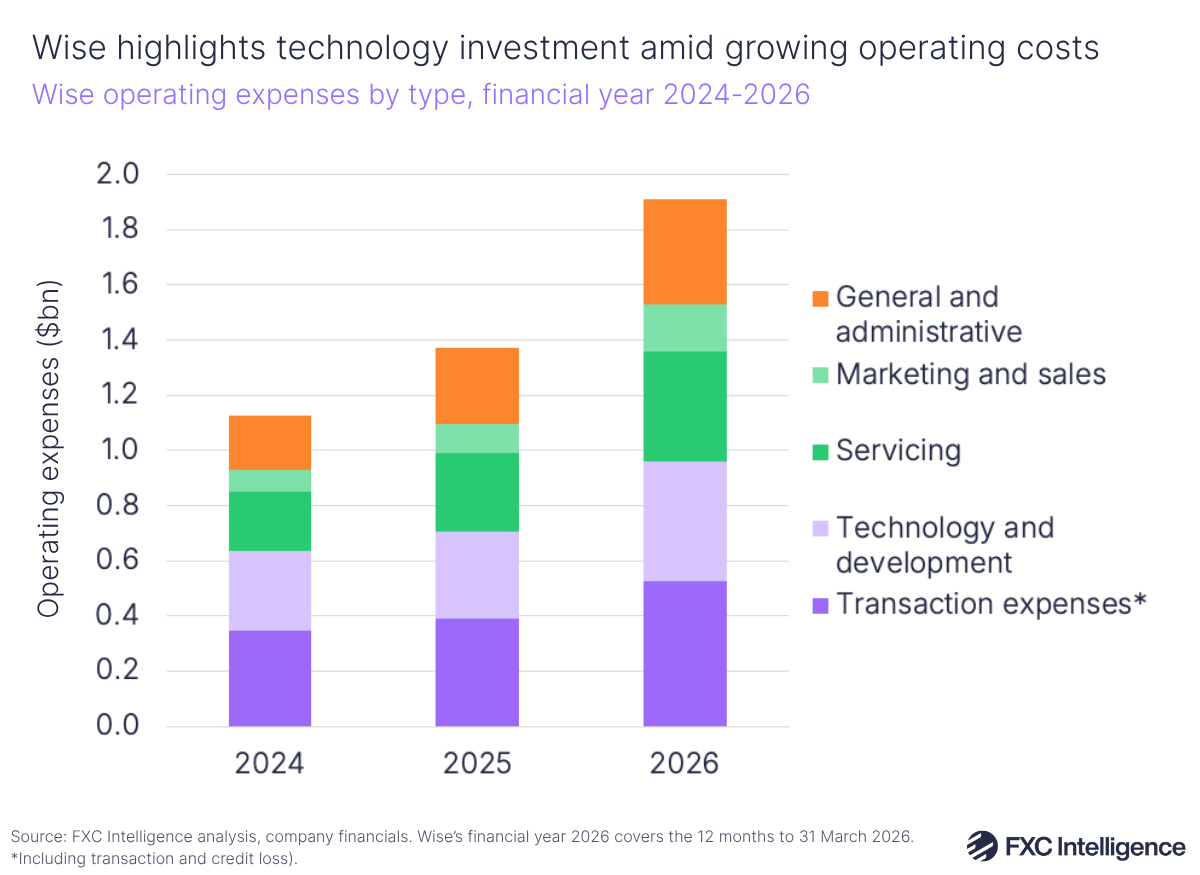

Alongside increases in revenue and volume, Wise has seen its total operating expenses grow by 40% YoY to $1.9bn. This is partly due to the recruitment and onboarding of more than 2,000 new employees, as well as ongoing investment in infrastructure, with the company expecting to continue investment into 2027, although at a slower pace.

Marketing in particular saw a strong upswing in spending, increasing by 62% YoY to $172m, aided by a focus on new channels and increased brand marketing investments, amid growth in the size of Wise Platform and Wise Business sales teams. The company is targeting a minimum 20% return on this.

Continued investment in technology and development saw spend grow by 38% YoY to $434m, which underpinned the maintenance of existing products and their rollout to new regions, as well as the development of new products and services. However, not all of this spend is on growing headcount, with the company also implementing a variety of AI tools to support coding and development.

The company is also deploying the technology in a number of other areas in the business, with 50% of customer support chats now handled with AI automations without the involvement of a human.

Wise’s narrative sits apart from the wider industry

While AI was mentioned during the call, stablecoins – the other trending topic within cross-border payments – were notably absent. Wise has been previously resistant to stablecoins, and is one of very few high profile companies in the sector not to have announced or launched a stablecoin-related product, with Käärmann previously indicating that he did not see the technology improving the company’s offering at present.

This focus on a differentiated approach is also reflected in the company’s investment narrative. While many companies in the space have been focused on highlighting AI-led operational efficiency, Wise’s mentions of the technology were perfunctory and its presentation of increased spending were framed positively due to their resulting business impact, rather than as an area of concern.

Investors are so far responding positively to this narrative, although it will be interesting to see how this evolves as the company beds in as a US-listed entity.