Wise’s FY 2024 results included some strong performances, but the company’s price cuts and revised outlook prompted a share price drop. We caught up with CTO Harsh Sinha and Interim CFO Kingsley Kemish to find out more about the company’s ongoing plans and wider strategy.

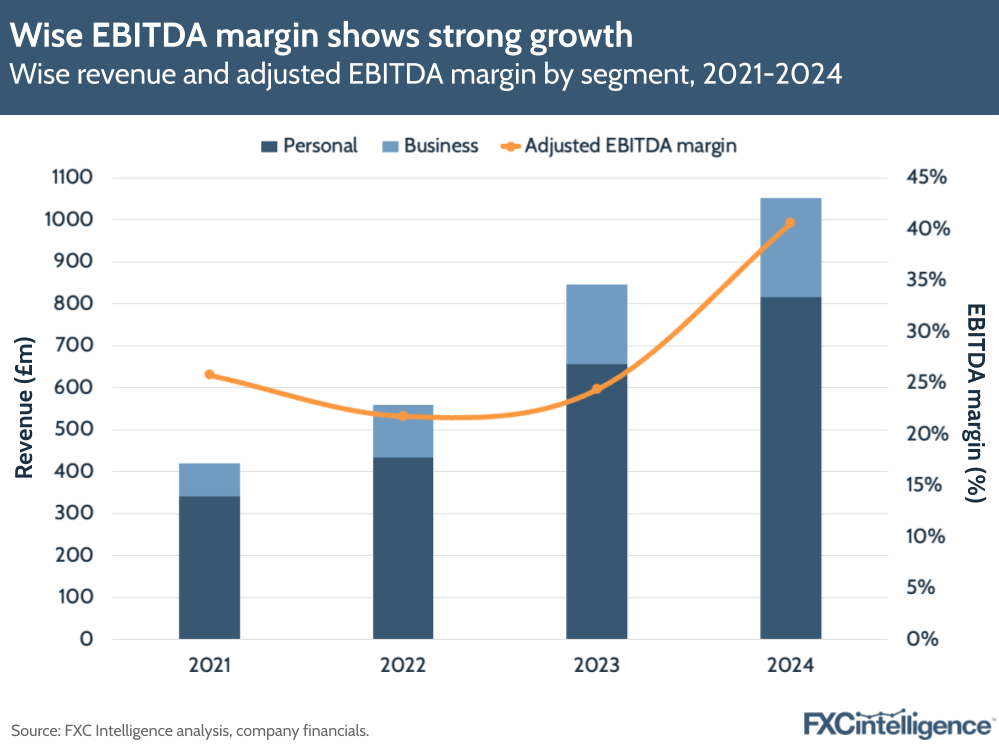

Wise’s top-line FY 2024 (year-end 31 March 2024) results saw the company pass a billion in revenue for the first time, with overall revenue increasing 24% to £1.1bn, while underlying income climbed 31% to £1.2bn. The company’s underlying adjusted EBITDA margin also reached 28% – well above its targets.

Cross-border revenue, meanwhile, increased by 17% to £795.2m, with cross-border take rate rising 2bps to 0.67%, while non-cross-border revenue grew to 31% – a combination of interest income and card-led revenue.

Three years on from its market listing in 2021, Wise now has a network that operates in more than 160 countries and across 40+ currencies, aided by over 65 licences and 90+ banking partners. During this three-year time period, the company has seen active customers increase 2.1x and cross-currency revenue increase 2.2x, while card and other revenue has climbed 6.7x.

This year, a reduction in cost of sales, including lower FX and reduced chargebacks, has allowed Wise to continue in its mission to lower prices, with the company cutting pricing and in doing so laying out a lower mid-term outlook than it had been following for the last few years. However, this, combined with slightly lower-than expected top-line results on some metrics, led to a sharp market reaction, with share prices dropping more than 16% on the news.

Given the increasingly complex nature of the business, as well as the strong growth story for Wise, I caught up with CTO Harsh Sinha and Interim CFO Kingsley Kemish to find out more about how the company is approaching its strategy in pricing and beyond.

Highlights of Wise’s FY 24 performance

Daniel Webber:

Let’s start with the highlights of your full year 2024 results. What are the key points for you?

Harsh Sinha:

Looking at the last year, we had another strong year: strong customer growth over the year. We’re seeing huge demand for Wise everywhere across the globe.

Last year, we served 12.8 million customers. This is 5.4 million new customers, which is an increase of 29% year-over-year. What’s cool is that 3.5 million of these new customers came to us on recommendation from existing customers, so all word-of-mouth growth.

We’re appealing to a much broader set of customers too. More customers are using the Wise Account. Nearly half of personal customers and 60% of business customers are using Wise to not just send, but also spend, hold and receive money.

We’ve also seen the Wise debit card product creating a new segment of card-only users. In fact, they accounted for 17% of our cross-border customers in Q4. In Canada, we saw 400,000 new cards issued in the last financial year.

This also means that customers are holding more money with Wise. And, globally, this is up 44.6%. Globally, this means £16bn, so about $22bn, held with Wise, including our assets product. For US customers specifically, this is about $2bn in balances, which is cash plus interest that customers are earning with us.

Then from an opportunity perspective, we see the space only continue to grow. So we see the huge potential. It’s an $11tn opportunity space. $2tn moves across borders for people like you and I every year and then $9tn moves in the SMB space.

We’re committed to continue to invest into our product and infrastructure, which really drives our growth, because its product-led growth. When people love the product, then they recommend it to their friends.

Some of the highlights for the last year: we became the first non-bank to complete a multi-year integration into NPP, which is Australia’s local payment system.

What this means is payments in and out of Australia become instant, and they also get cheaper. And we become more reliable as we become independent in Australia. That means you can do a US dollar to Australian dollar payment within 20 seconds from source to destination account. Being in the US, you’ve probably seen how ACH can sometimes take a day; in some countries, cross-border payments are getting faster than domestic payments.

We also launched a collaboration with Swift. We launched Correspondent Services with them, which makes it basically easier for banks to take advantage of the Wise infrastructure and connect to us directly.

Talking about banks and other firms and partners who are connecting through our Wise Platform product, we’ve continued to grow in that region. We now support household names like Google Pay, Interactive Brokers, Brex, Ramp. But most recently, in Latin America, we launched a partnership with Nubank, which is the fastest-growing bank in Latin America.

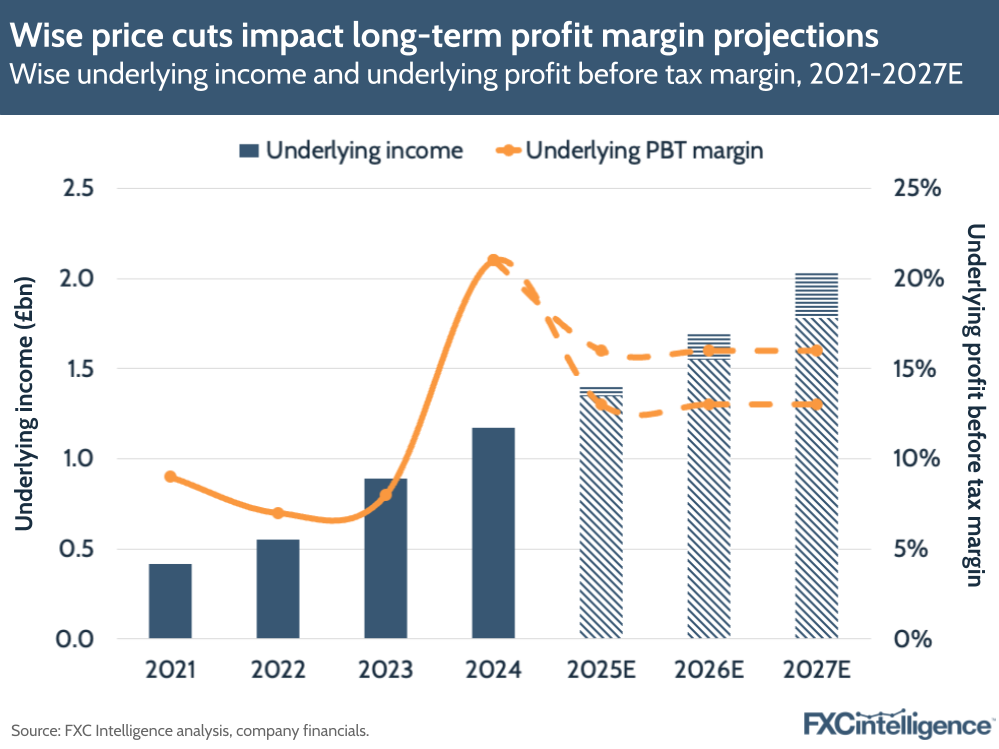

On the financials, we continue to see higher demand for our services and we continue to build Wise in a sustainable, profitable and high-growth manner. 31% increase in underlying income to $1.54bn for the last year. North America was 26% year-over-year growth. And gross profit grew by 51% to over $1bn. Overall, we saw a 225% increase in underlying profit before tax. That equates to $310m.

Wise shifts reporting focus to underlying income

Wise saw its overall income growth increase by 46% YoY, significantly above its previous estimates, which it had revised upwards several times throughout the financial year – the company attributed this to both the performance of the underlying business and the interest rates environment.

In reflection of the interest rates side of this in particular, Wise has shifted its primary financial metrics going forward. It will now focus on underlying income (revenue plus the first 1% gross yield) alongside underlying profit before tax (PBT on underlying income).

Using these metrics, Wise has produced a new set of medium-term growth expectations, its first since those laid out in its IPO, which reflect the fact that the company has lowered its prices and will continue to do so.

This projects underlying income growth of 15-20% in both FY 25 and the medium term on a CAGR basis. Meanwhile, the company also expects an underlying PBT of 13-16%, which it says is equivalent to an underlying adjusted EBITDA margin of 20-23% – a lower rate than it has previously realised or projected.

Wise’s consumer customer profile

Daniel Webber:

Talk us through your consumer customer profile for Wise Account and your money transfers product, because it is different from the remittance customer and the high-touch customers that exist in the market. What is that customer and where are they coming from?

Harsh Sinha:

Most of our customers still come from big banks. If you look at the personal segment, but also the business segment, a lot of people start where the money is and the money is usually in the banks that they’re already domestically banking with.

Then, what happens is, they start having international leads, or they’ve already had international leads but they’re not aware of Wise. They discover Wise, whether it’s through word of mouth – as I said, two-thirds of our growth comes from word of mouth; friends and family recommending their friends and family – or maybe through some marketing channels.

The number one reason they move, we’ve learned, is price. If they can save money, then they will move, and they’ll go through onboarding into a new financial services product. Usually you have to ID verify and download the app and take space on your phone – it’s a lot to ask for people.

Price is the number one reason, but then they stay on for convenience, speed and other things that we’ve built in the product. Over the years, when we started solving the problem, we were solving the problem of send, so transferring money. But, as you know, we’ve moved on to enabling people to hold, spend, receive and also now get a yield on their current account.

That’s actually driven and is driving quite a bit of the growth in the segment, where almost 50% of our personal customers are using the Wise Account and 60% of our business customers are using the Wise Account. That’s basically continued to drive our growth and stickiness in the product.

Personal’s role in Wise’s ongoing growth

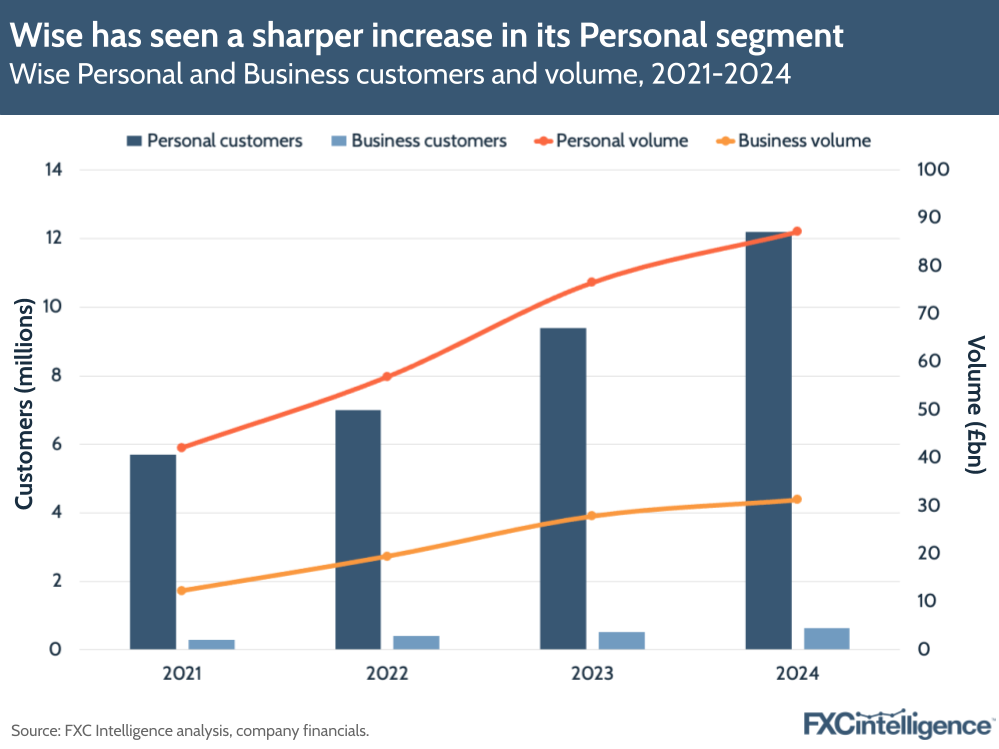

For FY 2024, Wise saw a 29% YoY increase in Personal customers, which reached 12.2 million. Personal volume, meanwhile, increased by 14% to £87.2bn. However, volume per customer reduced by 12% in the Personal segment to £7,100. Nevertheless, underlying income from the Personal segment increased by 30% to £884.4m.

Recommendations have been particularly critical to Wise’s growth. Of the overall 5.4 million customers who were added to Wise in FY 24, the company reports that around 3.5 million joined via recommendations. Wise has also seen active customers increase 29% CAGR over three years for its Personal segment, compared to 27% for Business.

SME customer acquisition

Daniel Webber:

Let’s double click on the SME customer, whose needs slightly differ. Where is that customer coming from and how does your product resonate with them?

Harsh Sinha:

Businesses, eventually, especially for SME, the biggest thing they want to do is get paid. If you’re running a small business, that is the list: just make it easy for me to get paid, please don’t create problems for me.

It’s very true for cross-border businesses; it’s very hard to get paid cross-border, if you look at the traditional banking system. Our product offering enables you to have local account details.

If you’re sitting in the US right now, and you want to get paid in the UK, traditional banks will say, “Have this person from the UK send money to you, Swift it to you”. In the US, people don’t understand what a routing number and ACH account number is because we have sort code and account number here. It’s confusing, and also sometimes cumbersome. The payer’s bank may not even enable international transfers sometimes, depending on where they are. But then they definitely will enable domestic transfers.

You can control your payment experience, and your customer’s payment experience, by enabling them to have local account details with Wise. So you can get a GBP account number and sort code, and then get paid locally. Then you control when you want to move the funds back to USD, versus maybe keeping the funds in pounds because you have a bill coming up in pounds next month.

This, really, is the ability to make it super seamless to receive and manage your finances. You decide what exchange rate you get and when you want to move the funds back to your home currency.

Growth in Wise’s Business segment

In FY 24, Wise’s Business segment saw a 20% increase in customers to 625,800, while volume increased by 12% to £31.3bn. This saw volume per customer reduce by 7% for Business customers to £50,000. However, the company reported a 37% increase in underlying income for Business customers to £288.3m.

Q4 2024 also saw Wise reopen onboarding for UK and EU business customers, which had previously been paused while the company worked to respond to increased regulatory requirements.

Growing Wise Platform

Daniel Webber:

On Wise Platform, the enterprise level of your business, you’ve now got 85+ partners from big banks, including Nubank as a fantastic recent addition. What resonates with Wise Platform?

Harsh Sinha:

Banks – definitely the banks that we’re working with – a lot of them are realising that the current offering they have for their customers, if they have one, is subpar. It’s usually more expensive. It’s cumbersome for them to use.

So they are basically, especially the incumbents, coming in to be customer-centric. They want to create a better experience for their customers.

Sometimes, their customers are also pushing them, because they’re seeing that their customers are moving to Wise because they can see the funds flow out. They’re like, “Might as well come and have the Wise infrastructure already”. So the customers are pushing them to bring Wise to them.

Nubank and other neobanks are very different because they always lead just like us with a high NPS [net promotion score] product. They want to build an amazing experience, and they want to have the best players and the best infrastructure connected for their products.

It’s a bit of a difference between newer players versus incumbents. But, over time, I think it’s all driven by either their own customers pushing them for a better experience, or they just want to build the best experience possible for their customers for cross-border payments.

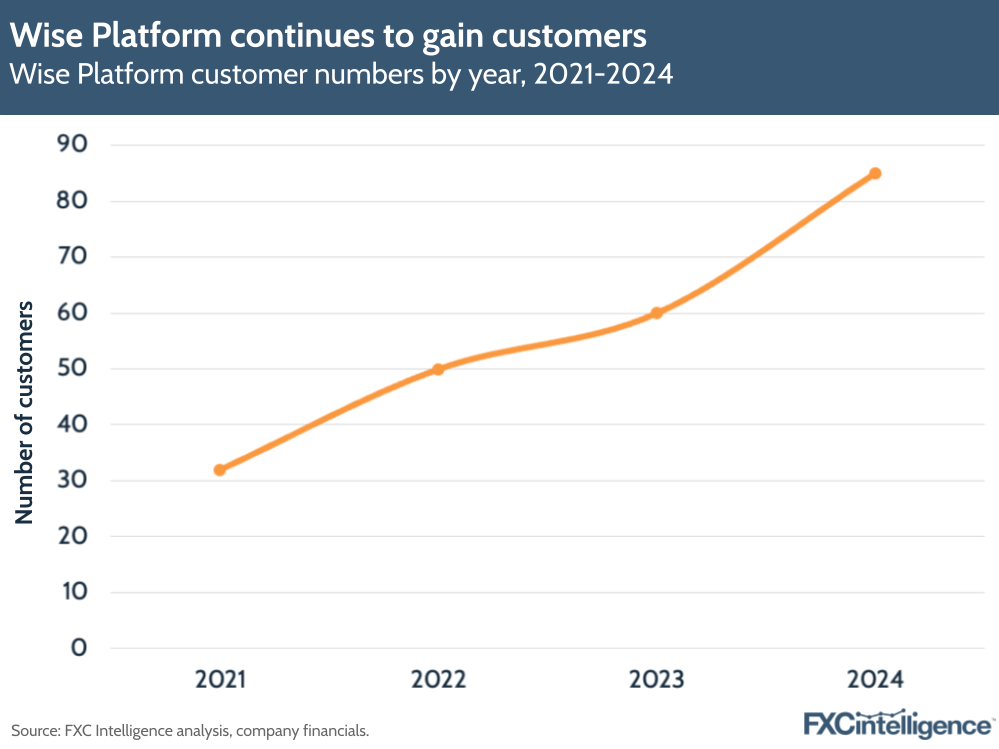

Wise Platform sees customer increase

Wise now reports having over 85 customers for its white-label Wise Platform product, up from 60+ in 2023, and has also added support for customers to issue cards over the company’s infrastructure.

This year also saw Wise become the first non-bank to directly integrate into Australia’s payment system, as well as partner with Swift through its Correspondent Services solution.

Wise’s pricing strategy

Daniel Webber:

You’ve always been competitive on price and have brought your pricing down further, which has also led to your guidance for next year coming down, prompting an instant reaction from the market. Let’s break this down and help people understand how you think about price and your guidance.

Kingsley Kemish:

From a price perspective, we should reiterate that offering the lowest price possible has always been part of the mission of Wise. Low cost has always been one of the key pillars of our mission, so it’s not something new and over time we’ve brought down prices.

Effectively, that’s been a key driver of the growth of the business. It’s definitely one of the areas that we invest in, as an organisation, to drive expansion of new customers and to keep the growth flow going.

More recently, we’ve had less of a capacity to invest in price, but we expect that the investments we’ve made since listing – where we really have invested in our products and infrastructure, as well as in our customer support, customer experience and operational teams – will, in this next medium term, give us the leverage and the ability to scale to offer price reduction. This is alongside the other more traditional things that have driven prices down, which is direct integrations or increased volume through partners that gives us more competitive ability to reduce costs.

Price has always been at the heart of Wise. We’re three years post-listing. We reconfirmed our listing guidance every year over the last three years, but now is a new start.

We’re more than double the size of the business we were at listing. We’ve got this multi-product offering that’s much clearer now. We’re like, “What does the next three years look like?” and that medium term.

That’s why we’re really clear that we expect to be able to invest more in price in the next three years to bring down those cross-currency fees, to make sure we’re giving customers the best price we can, which should also then lead to increases over time.

But this increase in volumes and increase in active customers takes time to come through. And when it does, that will create more capacity to continue the flywheel of price reductions. That’s really what’s in the core of this guidance, going forward, is that we expect to continually be able to reduce those cross-currency fees.

Harsh Sinha:

As a reminder, and I’m sure you know this having talked to us for a while now, but the way we price is we do cost-plus.

Daniel Webber:

Correct, so there’s no change to that principle, which maintains profitability.

Do you see different sensitivities by region or customer type on the pricing, or are you just going to try and bring them down everywhere?

Kingsley Kemish:

We try to bring them down everywhere. Clearly, there are different prices for different markets because the cost to provide the service is different. And, clearly, the volumes we have in some exotic routes, versus some of the volumes we have in more major routes, are different. That gives opportunities of scale.

But it’s the same approach across the board. You’ve been covering us for a long time. We try to make sure the customers are paying the price that’s based off the costs to provide that specific service, with effectively a small amount added from our margin, which creates our profit and our capital to continue to operate and provide the service.

But, otherwise, there’s no cross-subsidisation. We’re trying to make sure we’re very clean on just pricing for the specific service they’re providing.

We had a price reduction in April, with more than two basis points. But, also, in the last month or so, we started this initiative of recalibrating our prices, where we have looked really granularly at the detailed costs to provide services. We’ve enhanced our understanding of the costs to provide the service in different routes and different products, and off the back of that, we’ve adjusted prices.

Some prices have gone up, some prices have come down. We’ve adjusted the balance between fixed fee and variable fee. This is all to make sure that customers are paying a price that’s based off the specific costs that relate to that route and payer method etc.

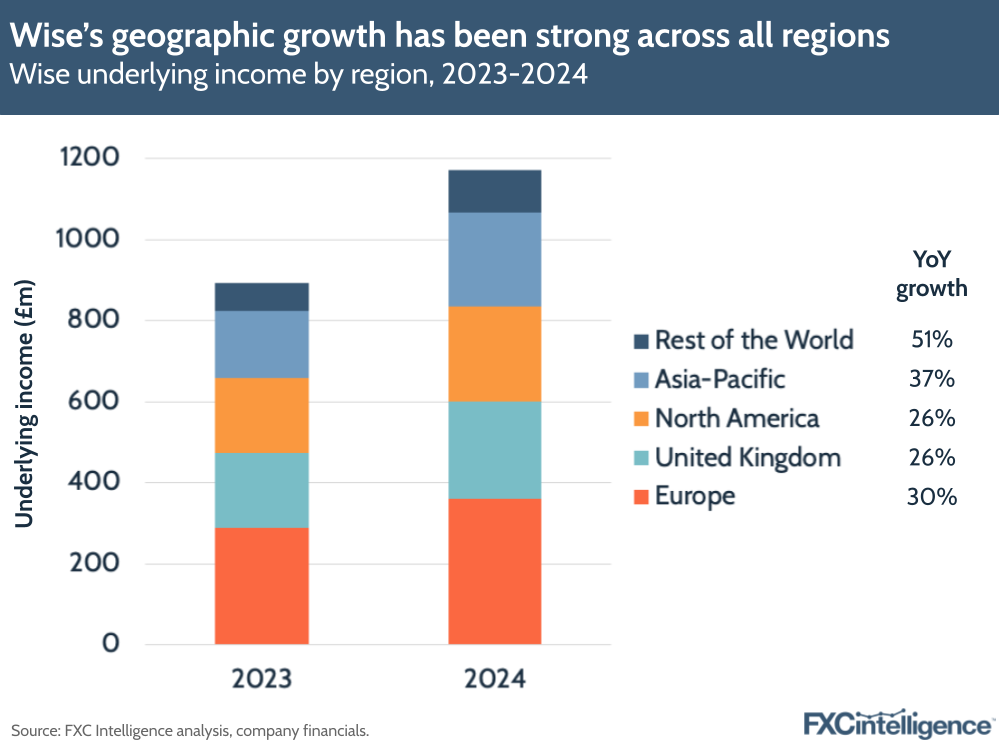

Wise’s geographic growth

Wise saw strong geographic growth in all regions, with no region seeing underlying income growth of less than 26% or revenue growth of less than 19%. The company’s oldest and best established market, the UK, saw the lowest revenue growth, followed by North America’s 26% underlying income and 20% revenue growth.

However, Rest of the World was the company’s fastest growing region in FY 24, at 51% underlying income growth and 44% revenue growth, with Brazil being a particular growth driver. Beyond this, Asia-Pacific also saw very strong increases, with 37% underlying income growth and 34% revenue growth. This will continue to be a focus in 2025, with Australia being one of two key markets for targeted expansion in brand marketing.

Cost reduction opportunities

Daniel Webber:

What are the areas that provide the biggest opportunities to bring down particular cost segments?

Kingsley Kemish:

Direct integration has been the biggest win in reducing costs. I wasn’t around when we got the direct integrations with Faster Payments, but I’ve seen the stats of the quite dramatic impact it had on both costs and speed.

Harsh Sinha:

We became the first non-bank in the UK to get connected to the Faster Payments scheme, which is the real-time payment scheme here, and we saw our costs go down considerably. I think we went from 60 pence per transaction to about six pence.

That was the bare bones, and we had to obviously add a bit on margin and stuff. But that’s a massive cost reduction. Then we can turn around and give that back to our customers as a price drop.

If you’re not directly connected, it can eat a lot into your costs and increase your costs a lot. So that’s one of the biggest levers we have. That’s why we take this approach of continuing to invest longer term into directly connecting into each payment system.

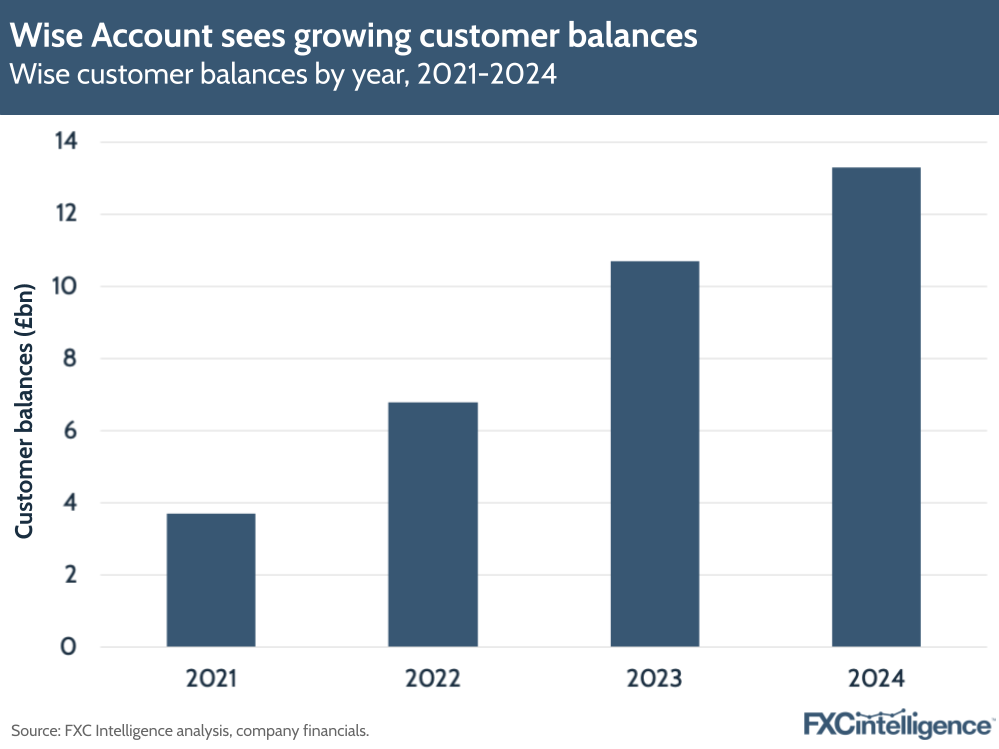

Wise Account provides additional growth

Wise Account has seen growing adoption in FY 24, with 48% of personal customers and 60% of business customers now using the service. Customer balances now total £13.3bn – a 24% YoY increase – with £2.9bn under custody, a 523% increase on FY 23.

This was partially driven by several improvements in FY 24, including improvements to transfers for expats living in China, as well as the launch of interest assets in five European countries and stock assets in 11.

The company now also has a significant number of card-only active customers, who use Wise Account without also using the company’s money transfers services. This group now accounts for 17% of Wise Account customers.

Crucially, the product’s customers brought more underlying income than transfer-only customers, with around 25% more for Personal and around 100% more for Business customers.

Lessons from the Wise Account

Daniel Webber:

The Wise Account has now been around for a while, and appears to be a very successful product. What are you learning as you see more usage of it, and what has been unexpected?

Harsh Sinha:

Generally, the way we do product development and integration is by basing it on feedback and what problems we can solve for customers. We started off with the transfers product because the founders had that problem to start, and then they found other friends and other folks around who had that problem.

Over time, as we continued to talk to our customers and did discovery, we realised people were saying, “Hey, actually, sometimes I would love to not just have the money go through you but actually have it parked with you. Because I have a need to receive funds, and hold funds, and maybe do the same transaction in the other currency next month”.

That led to this idea of starting to hold funds. Once you start holding funds, you have to use those funds, so then we started issuing a debit card. So that’s how the natural iteration of the product happened.

Fast-forward now 13 years, we see the Wise Account actually becoming quite a central part of the finances for a lot of businesses, and also for people who live international lives. For example, I live a pretty international life, I have it as my primary account, but there’s a lot of people like me who have that too.

You can get your salary paid into it. You can pay your bills. You can do direct debits. You can get your social security paid into it. So it’s becoming more and more like a full-fledged account that works locally in the domestic setting but, more importantly, it really shines when you have international needs.

The surprising part is how quickly the uptake’s been. Also, based on the principles of giving customers a return, with interest rates going up, that obviously has helped increase the balances.

Finally, as we shared in this earnings report, this new segment of card-only customers who hold funds with us and then use us for international purchases or travel, this has been an interesting discovery for us. That there’s a need for a different segment who would usually not be there if it was just a transfers business.

Kingsley Kemish:

It’s the multiple uses of the account that’s important. There’s not one use. In the middle, you’ve got people who are doing some transfers, but also using the card. And then you go into the business, where the card is a vital part of expense management and other things. It’s got a lot of uses for different customers.

Daniel Webber:

Harsh, Kingsley, thank you.

Harsh Singha & Kingsley Kemish:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.