Remitly has once again reported record results in Q1 2024, as the remittances company continues to see market-leading growth. In the latest in our post-earnings call series, we learn more about the drivers from CEO Matt Oppenheimer.

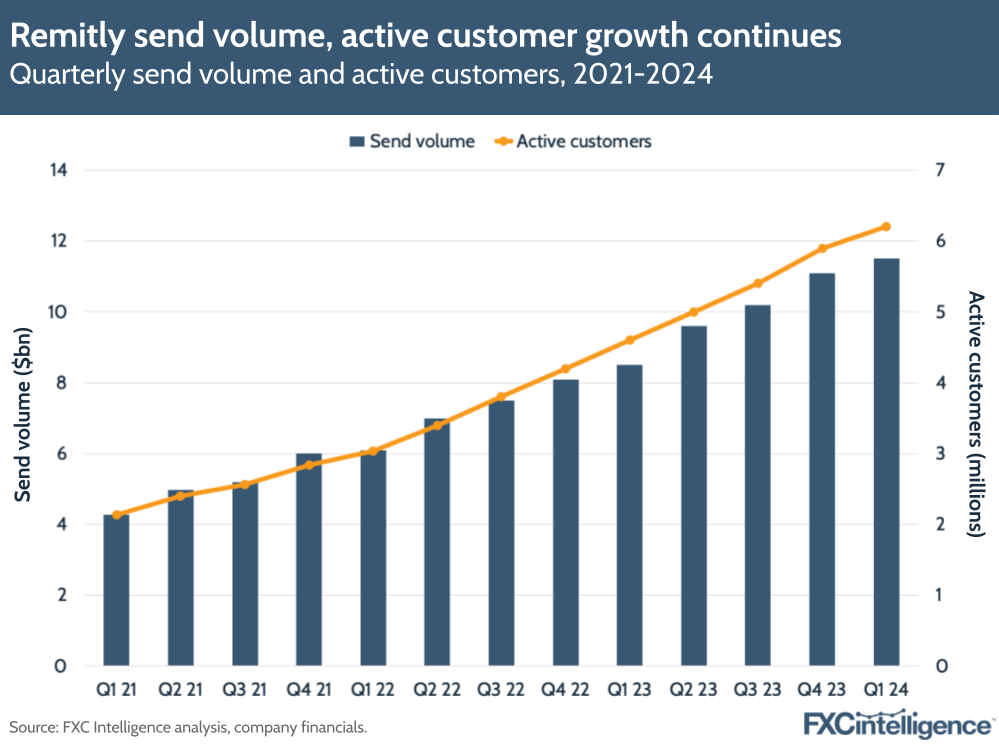

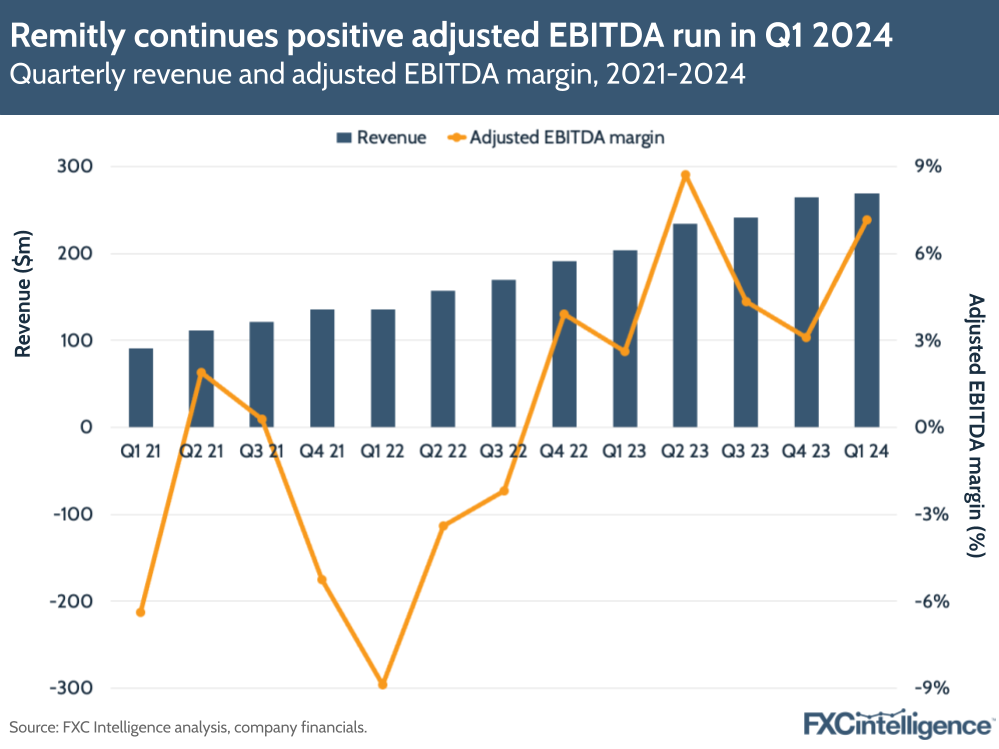

Remitly has continued to break its own records, with Q1 2024 earnings that saw the company increase revenue by 32% YoY to $269.1m, while send volume climbed 34% YoY to $11.5bn and active customers grew 36% to 6.2 million.

The company has also seen improvements in its adjusted EBITDA, which increased from $5.4m in Q1 2023 to $19.3m in Q1 2024. This means the company had an adjusted EBITDA margin of 7.2% in Q1 2024 – its highest to date.

This was aided by a growing preference for digital receive, with Remitly seeing the year-on-year mix of digital-received transactions increase by almost 500 basis points in the first quarter. Notably, Q1 is also one of the quarters with the lowest seasonal activity, due to a lack of high-send events such as Christmas, Eid or Mother’s Day, meaning the company expects to see stronger send from new and existing customers later in the year.

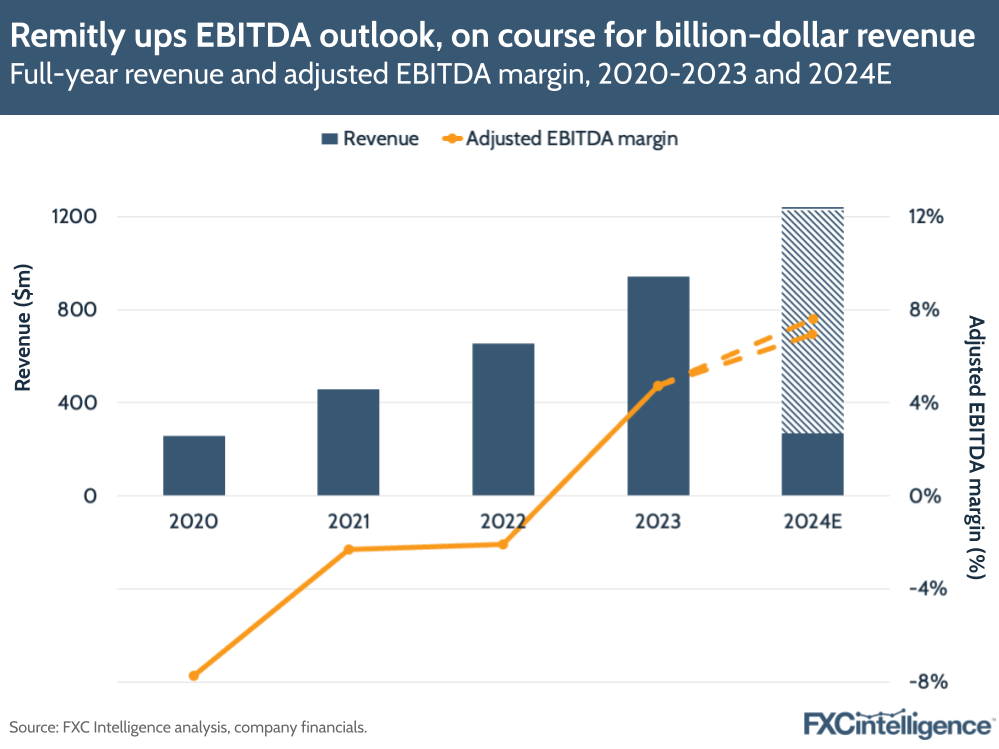

The results led Remitly to reaffirm its projections of FY 2024 revenue between $1.225-1.25bn – its first $1bn-plus year – while the company also increased its adjusted EBITDA projections, meaning it now anticipates a FY adjusted EBITDA margin of 6.9-7.4%.

I caught up with Matt Oppenheimer, CEO of Remitly, to find out more about how the company is growing.

Drivers of Remitly’s Q1 2024 growth

Daniel Webber:

Matt, more record revenue and send amounts in quarter one. What’s driving that?

Matt Oppenheimer:

We’re really happy with Q1. You just look at the size of our business now: $269m in revenue for the quarter, up 32% year-on-year, over $1bn in trailing 12 months revenue. Then to combine that with 32% year-on-year growth and adjusted EBITDA, growing from just over $5m a year ago to $19m.

We’re seeing a lot of leverage in the business, we’re really excited about the quarter and what’s driving it ultimately is a combination of two things. One, our customers – got to start and end with that. Their resilience, their tenacity, the predictability of remittances is amazing.

Then the reason we are growing markedly faster than anybody else in the industry, especially with our scale, is the reliability, the speed, the quality of our product. It’s a combination of customers coming back and using our product again and again, retention remaining high, with record new customers that we brought in at great unit economics. So I’m feeling really good about the business.

Customer acquisition sources

Daniel Webber:

It’s probably fair to say you have the biggest digital remittance business now. Where are those customers coming from?

Matt Oppenheimer:

We’re acquiring them, as we always have, via a variety of channels and all of it is data-driven, very measurable. That could be performance marketing or it could be a 360 campaign, but we’re looking at analytics in terms of the return on that investment in a specific geography relative to other geographies and multichannel attribution models.

That’s one: multiple channels that we’ve used for a lot of years. The second is a very fragmented market. So if your question is where are we gaining share from, it’s really fragmented.

The business is built on trust and a big part of the market is what we call corridor or country-specific players. So you are seeing players that have enough scale to provide a great customer experience, to be able to drive down costs on behalf of customers. And you’re seeing digital-first players like us be able to move faster and provide an unparalleled customer experience that drives word-of-mouth and retention.

Some of these things tie together, but it’s a combination of resilient, amazing customers and then out-performance of our product and marketing engine. That’s what we’ve always done and we’re excited about continuing to do.

Cash versus digital customer mix

Daniel Webber:

What’s your sense of the mix of customers that are moving from a more traditional cash funding world versus transitioning from a bank or another digital player?

Matt Oppenheimer:

As with most things in remittances, the answer really varies depending on the country and the corridor. If you take a US-India customer, that customer base tends to be more affluent and has used digital channels for a very long time. If you take US-Mexico or US-Latin America, it might be more cash-based.

So they’re using a digital platform for the first time and we’ve built trust with a large portion of customers in both of those market segments. I could go through others, but the punchline is it really depends on the country and there is an overall shift to digital. We are leading the way on that, both on the way that customers send funds, i.e. going to a cash pickup location in the US versus using a product like ours, and where we disperse funds. It’s becoming more digitised.

And we have the ability to disperse funds at over four billion bank accounts, over a billion mobile wallets, hundreds of thousands of cash pickup locations, even door-to-door delivery. It really depends on the country in terms of how customers want to receive funds, but there is a trend towards digitisation that we’re really proud to lead with our product and it’s doing a lot of great things for customers.

Growing preference for digital receive

Daniel Webber:

You also mentioned that customers are beginning to have a greater preference for receiving digitally. What is driving that? Is it generational, a change in a specific market or something else?

Matt Oppenheimer:

How that digitisation happens again depends on the country. You look at India: demonetisation and a lot of regulatory changes drove digitisation, combined with UPI and the payment systems they’ve built there. When that happens, there still is a need for customers to say, okay, well how do I get money into a UPI account if I’m living in the US or if I’m living abroad or if I’m living in another place?

That’s where we come in and we’re good at getting money in a wide range of disbursement options quickly, reliably, securely. That’s easier said than done. It sounds like table stakes, it’s not.

The India example was because of regulation. If you look at other markets, it might be that there’s a great product in the market like GCash in the Philippines where they’ve built out a solid merchant network. It’s easy to have a store of value that customers can have, but what can you do with those funds?

GCash has done a good job of building out a merchant network and other things to make their mobile wallet a viable store of value that customers can actually use. GCash was our very first partner that we ever worked with, so we’ve been working with them for a long time and we’re on the leading edge of a lot of the mobile wallets.

As I mentioned, we can send money to over a billion mobile wallets across the world. And the number of those integrations, the number of direct integrations and the quality of those integrations make it so that, if customers want money into a GCash account in the Philippines, it is fast, it is easy and a great way to do it is with Remitly.

There may be different reasons why a country becomes more digitised, like the India and Philippines example are different, but once that happens, we’re very good at allowing customers to get those funds quickly, efficiently and effectively.

The impact of seasonality

Daniel Webber:

You mentioned seasonality in the earnings call. Can you add a bit of colour about how you think about seasonality in the business?

Matt Oppenheimer:

We shared a little bit of a cohort view last quarter in Q4, but we’re looking at a cohort basis and a monthly active basis. The way to think about it from a customer standpoint is customers send for a wide variety of reasons.

They might send for rent or groceries – basically living expenses – tuition, Mother’s Day, Christmas, Eid, Ramadan. There’s so many different reasons customers send, but if you take a step back and you think about if a customer is sending for rent and groceries and things like that, they’re definitely going to send for something like Eid or for Christmas.

A lot of those holidays fall in Q4, so you see more active customers in Q4 because of that. Over the last decade of building this business, you still see a lot of active customers, but not every customer is active every month. It doesn’t mean they churn, it just means that different customers are active in different months. Lots of customers on a percentage basis are always active in Q4 because of the holidays.

So as we look at Q1, it’s very typical in terms of the number of active customers we saw and we’re really excited about the cohorts of customers that we’ve added – record numbers again in Q1, record numbers in Q4 – and how you can project that out to the both active customer and revenue growth as you look towards the rest of the year and beyond.

Artificial intelligence and Remitly

Daniel Webber:

AI is really having an impact. Where are you seeing it help?

Matt Oppenheimer:

There have been other hype cycles where I was a bit more of a sceptic. In this instance, there’s a lot of hype, but wow, there’s a lot of tangible customer value that will be driven by generative AI. I don’t know if you use any of the AI tools personally, but I use ChatGPT multiple times every day. It is unbelievable.

When you think about what that means for us as a business and for our customers, what it means is being able to help our customer support agents become more efficient and effective in terms of responding to customer contacts.

It means automating a lot. We’ve been using things like machine learning already for years, but as the technology gets better at being able to improve our risk systems such that fewer customers get put into any sort of review or experience that’s full of friction.

There’s marketing opportunities I mentioned on the earnings call where creative velocity and quality can increase; our marketing team has done an amazing job of doing that, which has improved our customer acquisition cost and marketing delivery.

So many opportunities. What it means to cut through the hype in my view is: what does it mean for customers? There’s lots of applicability and I think lots more to come on that front and we’re excited about the potential for it to improve our product.

Daniel Webber:

Matt, is there anything else you’d like to cover?

Matt Oppenheimer:

I mentioned our customers, that’s fundamentally why our business is doing well, but the specific example I’ll talk about now with our customers is I started this business living in Nairobi, Kenya. They’re not getting as much press recently, but there’s some pretty devastating floods that are happening in East Africa right now.

What we do during instances like that is we have a disaster response program where we waive fees, we help customers in those specific regions and areas for a period of time and it drives, it’s a good thing to do because it’s the right thing to do, most importantly, but it also drives word of mouth, brand affinity, all of that.

Remittances are important, but they’re especially important during natural disasters, during tragedy, during things like that. So I think about the ability that we’re giving folks across the world now in 170 countries to be able to support their loved ones during tragedies, like what’s happening in Kenya right now.

That’s why I do what we do. That’s what gets the team motivated every day. It’s really amazing to see how you do see increases in remittances during tragedies, whether that was an earthquake in Mexico years ago, whether that’s the flooding in Kenya.

The Kenya one is more personal to me because I used to live there and a lot of the things that I’ve been seeing are places that I used to go. I’m really proud of the team delivering for our customers when it’s needed most. And that’s certainly one example right now with the flooding happening in East Africa.

Daniel Webber:

We wish everyone well there. Matt, thank you.

Matt Oppenheimer:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.