Remitly reported better-than-expected FY and Q4 2023 results, and is on track to reach its first $1bn+ revenue year in 2024. In the latest in our post-earnings call series, we speak to CEO Matt Oppenheimer about how the company is growing, and what efficiencies it can achieve as it scales.

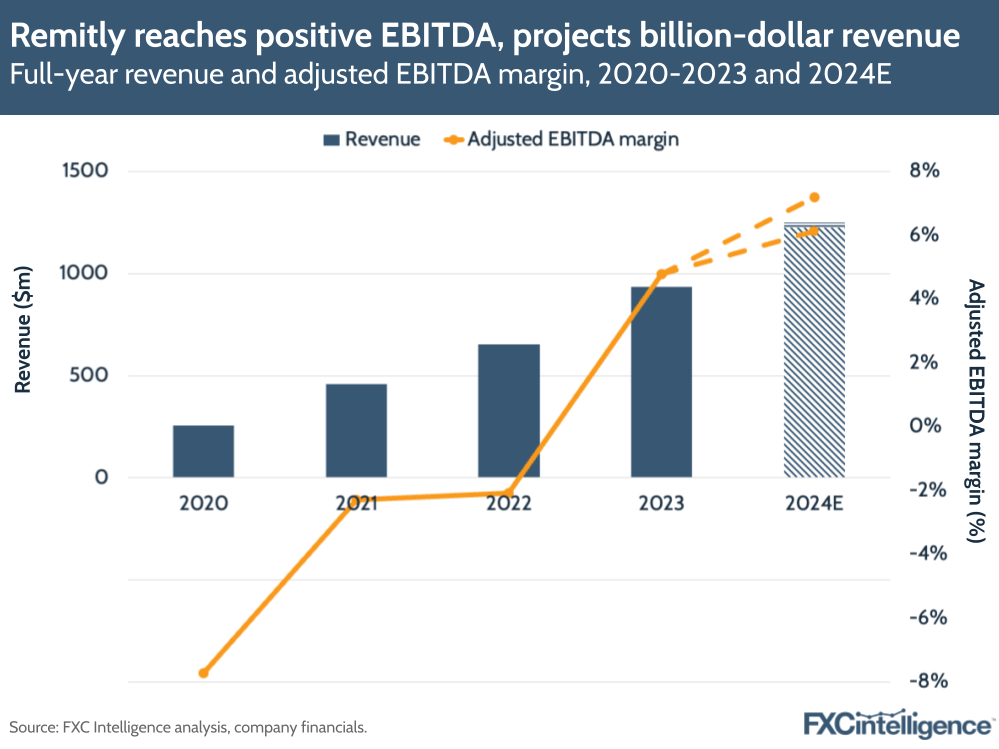

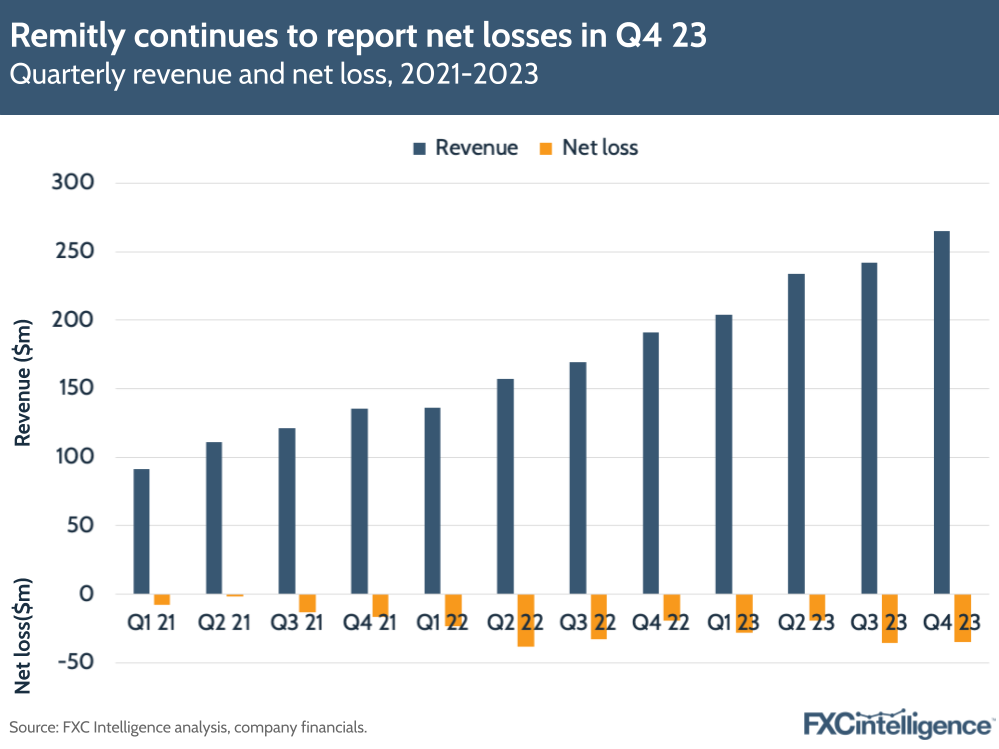

Remitly has announced its Q4 and FY 2023 results, with strong growth and above-expectations results that saw full-year revenues climb 44% YoY to $944m, while Q4 23 revenue increased 39% to $265m. This also extended to adjusted EBITDA, with the company reporting its first positive full-year adjusted EBITDA numbers, producing an adjusted EBITDA margin of 4.7%.

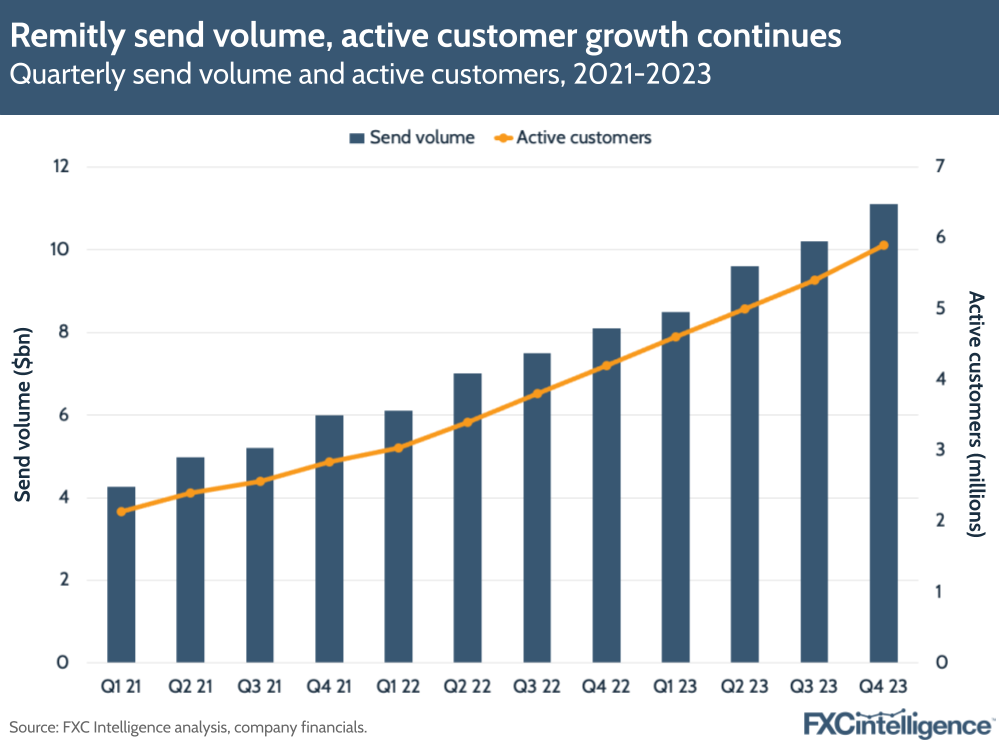

On send volume, Remitly saw a 38% YoY increase to $39.5bn for FY 23, while active customers increased 41% YoY to 5.9 million in the final quarter.

Efficiencies of scale were a key focus of the earnings call, with the company highlighting several data points in support of this, including the fact that it saw revenue less transaction expense increase 56% YoY in 2023 and expects this to continue to grow at a faster rate than revenue alone into 2024 and beyond.

The company also highlighted its use of AI and machine learning to help drive efficiency, as well as discussing the importance of its technology platform to broadening its relationship with existing customers through further related products.

The company is now projecting FY 2024 revenue to pass $1bn for the first time, with a target range of $1.23bn-1.25bn. It also projects adjusted EBITDA of $75m-90m, giving it a projected EBITDA margin of 6-7%. This, alongside its strong results, prompted shares to climb in after-hours trading.

I caught up with Matt Oppenheimer, CEO of Remitly, to find out more about Remitly’s current and future growth, given its successful year.

Drivers of Remitly’s growth in FY and Q4 2023

Daniel Webber:

Another very strong quarter and year for Remitly. What is driving your growth?

Matt Oppenheimer:

What’s driving the performance first and foremost is the resilience of our customers and the non-discretionary nature of our service. I can’t emphasise that enough as the foundation. Not every industry is privileged enough to be able to have the kind of customers that we get to serve every day, and that’s foundational.

Then, you look at some of the structural things that are happening in our specific industry: shifting to digital and, as you get more scale, being able to deliver a much more reliable, fast and affordable service. You see the kind of retention rates that we have, combined with the fact that – as we grow to a very large customer base – we’re now serving over five million customers per quarter.

You see that there’s a word of mouth and structural benefit that is continuing to benefit our business in terms of building trust with new customers, continuing to deliver a superior product to our existing customers, and that is ultimately what’s driving our performance.

Efficiencies of scale

Daniel Webber:

Your general direction is to continue to drive more efficiency as you grow. Given you are the largest digital remittances business out there, what does scale continue to mean in this space, and where do those efficiencies come from?

Matt Oppenheimer:

Remittances are like any payments business in some respect, in that the more scale that we have, the better we can deliver our service.

What I mean by that is we can integrate with more payment collection providers, whether that’s debit card, whether that’s bank deposit, whether that’s alternative payment systems. Then we can also do that on the disbursement side.

Not only do we have access to billions of bank accounts, hundreds of thousands of cash pickup locations, billions of mobile wallets, but the quality of those integrations gets better and better. Unlike 10 years ago when we were subscale, when we could do one what we call direct integration, which is call it with a specific bank in India or the Philippines or Mexico or Columbia or you name it, we’d be relying on aggregators and that would increase the cost and decrease the reliability.

Now we’re getting more and more to the last mile. Then there’s other elements in between that transaction that we probably don’t talk about enough in terms of building out world-class risk systems so that we prevent bad actors, but also deliver a seamless experience to good customers.

We do that via machine learning and some of the other emerging technologies, combined with just having more data on our platform to the point where the machine learning models get better. All of that results in benefits of scale that then gives us efficiencies – whether that’s on the transaction expense side or on the customer support expense side – and that we’re delivering in terms of improvements in Q4.

But of equal importance, it also is a symbol of the fact that our product is getting more and more trusted, more and more reliable. That continues to drive retention, which continues to drive word-of-mouth effects, which brings down things like customer acquisition cost. So we’re really feeling that flywheel effect of scale, and we’re really pleased about what it means for our business.

Remitly’s use of AI

Daniel Webber:

You talked about AI quite a lot on the earnings call. Where do you see AI having an impact?

Matt Oppenheimer:

In many ways, we’re just getting started in our effort to leverage it.

There are opportunities to help give our agents tools to streamline and improve customer support from an AI standpoint. I mentioned our risk systems: I think there are opportunities both from an AI as well as machine learning, which is different but related, in terms of looking at large data sets and delineating between good customers and bad actors. So we see there being a lot of opportunities across multiple vectors.

While we showed some significant improvements – 260 basis point improvement as an example on our customer support costs year-on-year – there’s a lot more that we can continue to leverage there while making sure we’re maintaining the privacy, the security, the other elements that I think are also really important to keep top of mind whenever thinking about new technology, including AI.

About 95% of customers go through without having to contact customer support. That number was a lot smaller a few years ago, and the investments we’re making, including in AI, will continue to make it so that contacting support is not necessary, given that the transaction will go through even more seamlessly.

Remitly’s marketing spend

Daniel Webber:

Your marketing spend helps drive the business. What are the flywheel effects?

Matt Oppenheimer:

Most important is that as our user base grows and as our product continues to get more differentiated, there’s a word-of-mouth effect that is helpful.

Our business comes down to trust and there’s really no better way to build trust than one of our loyal customers saying, “Hey, I had an amazing experience with Remitly. You can use them, you can trust them. It’s remarkable.”

We’re seeing more of that word-of-mouth effect, which is different from marketing, but does help with elements of customer acquisition cost and overall growth rates.

That’s the biggest, you said flywheel, I think structural benefit. Then our marketing team just continues to execute very well from a whole funnel perspective and with a very measured, very data-driven, very unit economic lens that I think not every company has and is something that has always driven our growth and continues to.

Deepening customer relationships

Daniel Webber:

You talked about how you want to deepen your relationship with your customers. What can you share on that?

Matt Oppenheimer:

There’s a wide range of pain points that our customers have when they move to a new country. Financial services are not designed for people who move or live and work abroad. So that, combined with a lot of what we built – including as I mentioned on the earnings call, this technology platform – makes it so that it’s easier and faster to leverage different subcomponents of what we built in remittances, to then launch new products on top of that.

It puts us in a really solid position to leverage those kinds of assets. To leverage the trust we have with customers, to leverage our deep understanding of them, both qualitatively and quantitatively. To be able to launch and build new products and services on top of that, that really focus on cross-border financial services pain points, of which there are many.

You should expect, as I mentioned on the earnings call today, additional testing, additional product launches in that space, and we’ll talk about it in more detail as those get to sufficient scale.

Daniel Webber:

Matt, is there anything you’d like to mention that we haven’t covered?

Matt Oppenheimer:

We are genuinely really excited about Q4 performance, about 2023 performance, about our guide for 2024. We’re excited about all of that because we continue to deliver for our customers.

I’ll end where I started: we are so fortunate to get to serve our customers specifically. Their tenacity, their resilience, the reason they send money back home. Not every business is that lucky.

That is the foundation. Then within that foundation, we are, I believe, outperforming a lot of the other remittance companies out there. But it’s a real honour to serve our customers because it’s a resilient, growing market, which is very different from a lot of other businesses out there. And the reason it’s a resilient, growing market is because we have incredibly resilient and heroic customers, really.

Daniel Webber:

Matt, thank you.

Matt Oppenheimer:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.