OFX’s FY 2024 results saw the company unveil a long-term B2B-led strategy alongside its positive yearly earnings performance. We caught up with CEO Skander Malcolm to dive into the details.

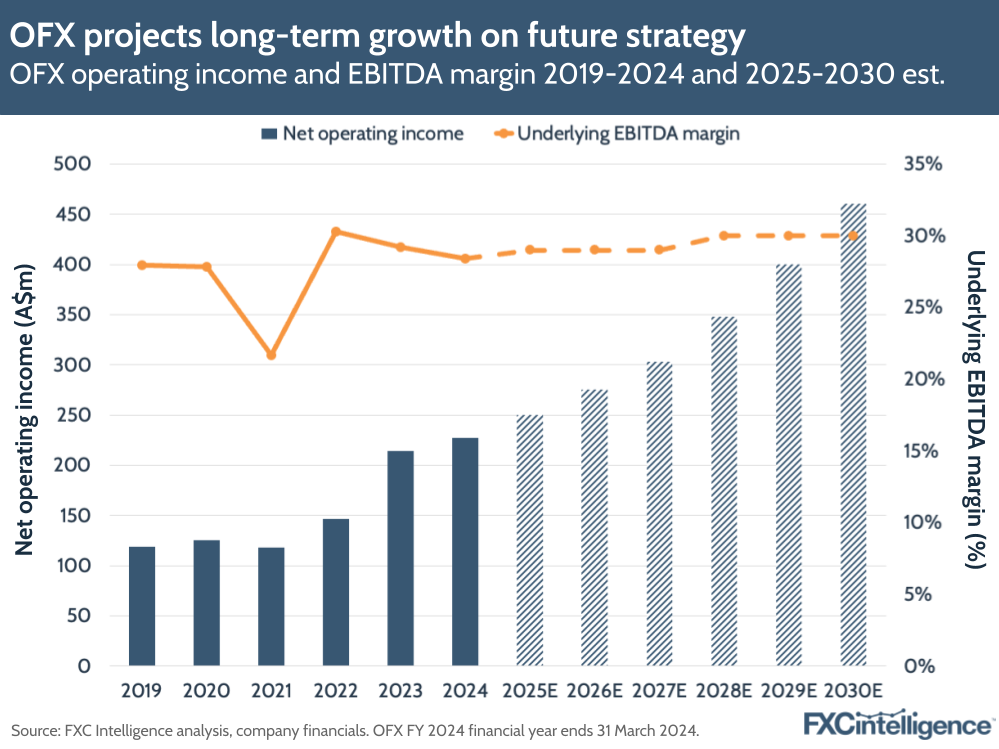

OFX has reported FY 2024 results that the company described as “solid”, with net operating income (NOI) increasing 6.3% YoY to A$227.5m, while underlying EBITDA (excluding Paytron) increased 8.2% to A$67.6m. This put NOI at the lower end of its guidance, while underlying EBITDA was in the middle of its guidance range.

The company, which is now predominantly dominated by its B2B business, faced macroeconomic headwinds during the financial year, which ends 31 March. However, it also had focus on “disciplined costs control” and saw synergies in the integration of Firma, the Canadian corporate FX business that it acquired in 2022.

The earnings announcement was accompanied by the news that it had completed the acquisition of Paytron, which includes a platform with multicurrency, card and invoice management capabilities. OFX now plans to fully integrate and rebrand Paytron as part of OFX.

The acquisition will also form a part of the company’s longer-term strategy, dubbed OFX 2.0, which CEO Skander Malcolm outlined in detail during the call. We caught up with him to learn more about the company’s results and the longer term plans for its development.

Positive market reaction to OFX’s FY 2024 results and strategy

Daniel Webber:

The market responded very positively to your results and the strategic direction you presented. What do you think they have taken from your strategy and earnings that is resonating well?

Skander Malcolm:

We’re obviously very pleased with the market response but, candidly, a lot of what we were planning to do just got communicated and the market liked it. Specifically, the feedback we’re getting from investors that the market really likes is, firstly, there’s an outlook which is very clear not just for fiscal year 25, but for 26, 27 and beyond.

Second of all, they like that the building blocks that underpin that outlook are very clear and they can understand those building blocks. It’s not overly complicated or overly reliant on multiple factors.

Third of all, they like the fact that it’s a settled management team that’s putting out a medium-term outlook. They believe that the management team has run the company, operated the company, understands its markets and has a moderate view and isn’t just trying to make a name for themselves.

That outlook is underpinned by a lot of factors that make sense to the market, so the market appreciates that clarity and that medium-term view and hence the positive reaction. Obviously the market will now look to the company to deliver on that, and we’re well aware of that and we’re absolutely ready for that. That’s really what we’ve heard from investors as to why the market responded the way it did.

OFX’s future strategy

As part of the company’s earnings, Malcolm shared the company’s strategy for 2025 and beyond, which focused on both scaling in developed markets globally as well as enhancing its offering to core customers.

Dubbed OFX 2.0, this is intended to deliver annual NOI growth of 10%+ in the medium term (1-3 years) and 15% in the long term (3+ years). It is also expected to deliver underlying EBITDA margins of 28-30% in the medium term and around 30% in the long term.

This will be delivered by tackling more pain points experienced by OFX’s core customers – small or mid-sized businesses with FX turnover of between A$1m-10m. This will include cards, subscription services and beyond, primarily delivered digitally but with the ability to provide human support when needed. This will be aided by the capabilities brought by the Paytron acquisition. As a result, OFX expects to see non-FX revenue grow at a faster rate than FX revenue in the short to medium term.

OFX’s strategic move to B2B

Daniel Webber:

B2B is now the heart of your business, accounting for around 70% of revenue. Where are you focusing the B2B strategy?

Skander Malcolm:

The focus for us is on small and mid-sized businesses that generally have A$1m-10m per annum in foreign exchange or cross-border payments and are obviously looking to grow globally.

We looked at a number of different metrics in our strategy development to identify who our target or ideal client profile is, and we settled on that because numbers of employees can be misleading. Particular types of industries may or may not be strongly indicative of growth possibilities, so we said, in fact, it’s the kind of revenues and the geographies in which we like to operate that are really the most important factors, and that’s where we landed.

We support a range of industries and obviously a range of geographies, but typically they’re moving between one or they generate between A$1m and A$10m in revenue from foreign exchange.

The pivot to B2B

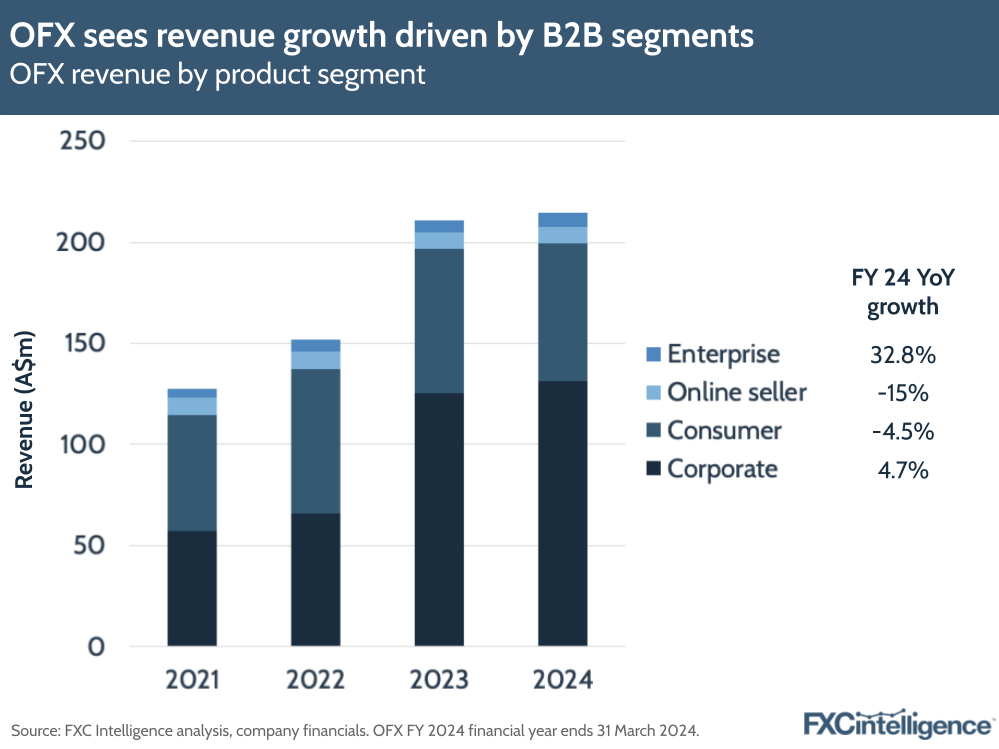

OFX’s pivot to B2B (which comprises its Corporate, OLS and Enterprise segments), a project it began several years ago, is now “well and truly operational”, with almost 70% of revenues now coming from B2B.

The company reports that revenue from new B2B clients was up by 20% YoY, which is particularly key as new B2B clients tend to grow revenue in year two onwards, while B2B has grown 27.6% on a three-year CAGR basis.

The company did see soft growth in 2024 versus 2023, with B2B overall seeing revenue increase by 4.8%, however this was largely the result of factors not expected to persist in 2025. Particular headwinds included challenging economic conditions in Canada and Australia, as well as a decline in revenue from the online sellers (OLS) segment. The OLS segment is set to be reshaped by the Paytron acquisition, which led to a pause on the development of the in-house platform.

The Corporate segment, meanwhile, saw momentum, with three of the five largest subregions seeing growth of 14%+, while overall new revenue increased by 26%+. The UK and Europe performed particularly strongly.

Enterprise saw revenue increase 32.8% YoY, while its three-year CAGR reached 20%+. Here OFX has pivoted to focus on smaller opportunities and activate them quickly, and has also seen strong growth from established clients.

Meanwhile, the company’s high-value consumer segment saw a reduction as a result of declines in activity in high-value use cases such as large purchases, property and wealth transfers, though there was an improvement in April. On a three-year basis, meanwhile, despite the segment seeing a drop in active clients, it has seen 6% growth on a three-year CAGR basis.

OFX’s developed markets focus

Daniel Webber:

Unlike many emerging markets-focused players, you focus on developed markets. What’s the strategy there?

Skander Malcolm:

We like to have a developed market focus because our risk appetite at a public company level is pretty clear about the fact that we want to generate sustainable returns over time.

I have a lot of emerging market experience and I love emerging markets and it’s perfectly valid for any company to be growing in those places. However, for us, at our current size and footprint, there is so much headroom in the markets that we’ve chosen the developed markets.

It sits very nicely in our risk appetite, but that’s where we focus. In the future we may look at that again, but certainly in the medium-term that fits our combination of growth orientation at appropriate risk levels.

Geographic development and growth

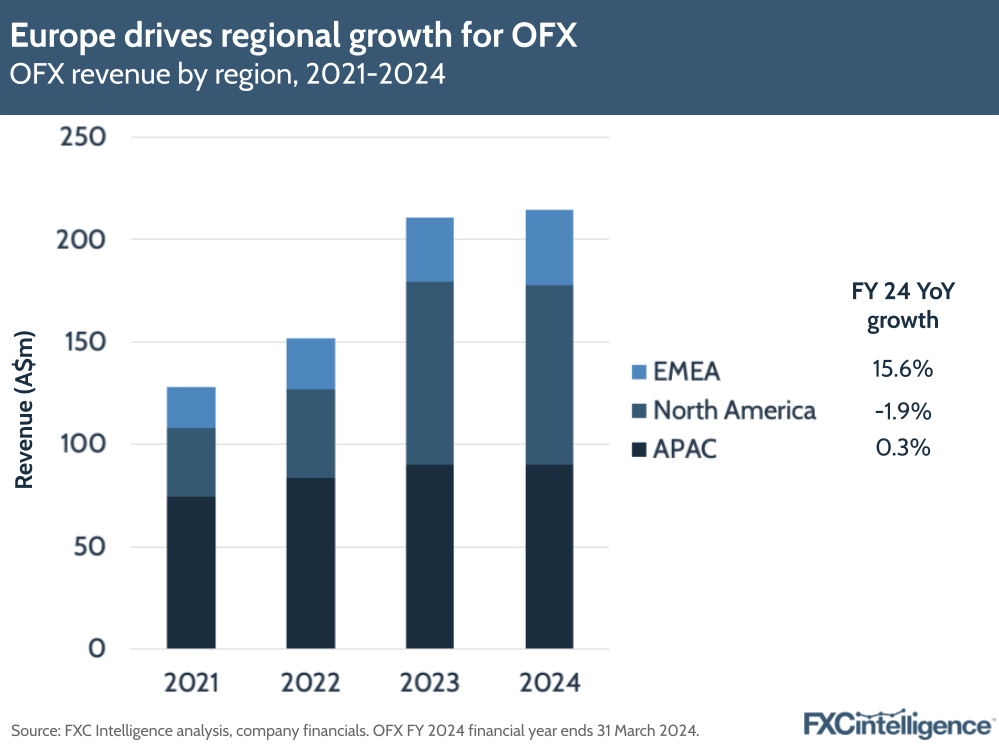

OFX has increasingly focused on growing in developed markets beyond its home market of Australia, an effort that is now paying off. In FY 2024 the company saw 65% of revenue generated outside of Australia – up from 50% three years previously.

This was accelerated by the acquisition of Canada-based Firma, with North America now accounting for 41% of revenue. EMEA, meanwhile, saw strong organic growth, increasing 15.6% YoY to account for 17% of revenue.

This increased geographic diversification benefits OFX not only because it reduces risk, but because it allows the company to tap into a far greater total addressable market, allowing it to generate “healthy” NOI margins while increasing EBITDA margins as a result of offshore scale.

OFX 2.0 and the impact of the Paytron acquisition

Daniel Webber:

You’ve characterised the next stage as OFX 2.0. Talk through what that involves and where your acquisition of Paytron fits into it.

Skander Malcolm:

This is really the culmination of a lot of work in the strategy area. All good strategy starts outside the company with clients and markets before it comes into the company and capabilities.

What we were seeing externally was that the target client was loving what OFX could provide in terms of cross-border payments. Loves the digital interface, loves the combination of digital plus human that we’ve been operating for some time and very, very well. But what they were saying to us was, there’s a lot of jobs in and around payments in our world that you can’t help with and there’s even other payment types like cards that you can’t help with today.

Even though we had developed a wallet and we were moving very well in our online sellers segment, it was clear to us that clients were asking for more jobs to be solved and capabilities to pay.

Obviously we were on that journey to build the cards capability. Paytron came along and we initially thought, well, the value in this is: technically there is an operating wallet, there’s an operating set of cards and then there are also ways in which the Paytron team had developed simplifying the jobs these clients were facing.

What has happened since the acquisition in May is we’ve worked very closely with them. We’ve worked very closely with our internal teams to build out how that is going to get integrated. We are going live within a matter of weeks so that all new OFX clients in Australia who are corporate are going to get that proposition as well as Paytron clients getting rebranded to OFX.

The evolution around Paytron is that what clients were telling us was “all these jobs actually create more pain than the payment itself; we love you for the payment, but if you could solve those other jobs, we would feel very grateful and you would really save us a great deal of time and money”.

As we shared in the investor presentation, there’s an example of an OFX client who loved OFX, who literally said, “Doing more business in the US, need to have this capability. Would love to do with you, but because you don’t have that capability, I’m going to look externally.”

They looked at a couple of firms. They chose Paytron really for the integrations that were available around invoice management workflows, cards. They picked up Paytron and on their first day they issued 50 cards and they didn’t even know that OFX had bought Paytron. When we sat down with them and went through it all, they were like, “Oh, thank goodness it’s OFX, because the service piece was always really, really important.”

We shared with investors the revenue profile of that client compared to what we also see in some of the competition in Paytron overall, and as you know, compared to OFX, there’s a significant amount of revenue and client advocacy that we’re missing as a result of not offering those services. Really it’s an evolution from where we were, heading into an exciting area, and we’re all very energised by getting that in place and rolling it out globally.

Card revenue generation

Daniel Webber:

How do you generate revenue from cards versus the traditional FX space?

Skander Malcolm:

In a traditional FX space, and the way OFX grew up, was what we would call deals. A client gives us the money, we go and purchase the foreign currency that they’re looking for, and the beneficiary receives the money.

In a world where there’s wallets and cards, first of all, there’s a wallet, so the client would fund the wallet and then they would execute the transaction as they had done previously. They could do that with either a card or a bank-to-bank payment, which is the traditional way. But in the world of cards, there’s three extra revenue streams.

First of all, when they fund the wallet, obviously now there are funds sitting in the wallet and the company is earning interest income on the float.

Second of all, when the client uses the card, the issuer or us, we would earn effectively interchange revenue, which depending on the jurisdiction, could be anywhere from 50 basis points to 150 basis points on the transaction.

Third of all, we offer the client many options to fund that wallet. Now they may choose to fund it bank-to-bank, they may use a debit card to fund it, they may even use a credit card to fund it. Depending on how they fund the account, there could then be fees associated with that.

What we would also do in the world of Paytron is that, beyond the card, we offer various workflow integrations for the client and also corporate expense management. The core product will be free and a client will have the wallet. They could have up to three cards.

They can do what they’ve always done with OFX, but we’ll also say that if you want to have 50 cards or a hundred cards,then there’ll be a subscription service, so you’ll earn subscription fees from that.

To summarise, you’re getting interest income, you’re getting interchange income, you’re getting fee income from ways in which clients fund the wallet and you’re getting potentially subscription revenue from the client as well. And all of that in exchange for a much more comprehensive and simplified service to the client, so many more revenue streams, margin expansion and obviously a much happier customer.

Enterprise performance and strategy

Daniel Webber:

OFX’s Enterprise segment has performed well. What’s driving that and how are you positioning OFX in the Enterprise space?

Skander Malcolm:

We look at enterprise as a way in which we can effectively help B2B2B or B2B2C clients who have some form of embedded cross-border payment in their business model.

For example, share registry companies may well have issuers who have shareholders overseas. Traditionally if dividends were being distributed for example, or share sale proceeds, the share registry company would have a global bank, global bank would convert that into whatever currency was being paid into often at a very expensive rate. Then they would cut a check in that currency and then send it to the shareholder, so the whole thing was expensive, slow and actually created a lot of reconciliation and other customer service issues for the share registry company.

In that example, we digitise the process, because we have licences all over the world we can sign up shareholders in different jurisdictions, they can elect to receive those dividends or share sale proceeds. Digitally, they’ll get the money the same day at a vastly better rate and it’s all digital. The share registry business gets a much more digital process.

They get much happier issuers and of course issuers get a much better shareholder experience, and obviously we get EBITDA-accreted clients because we are doing large numbers of payments in one file and so on.

That’s just one use case. That’s a business that takes time because clearly these large clients have a lot of competing priorities. You can win the client, but then you’ve got to integrate with the technology, you’ve got to activate with their various distribution channels.

It’s certainly taken time, but we’re very pleased with the progress and you could see last year we grew over 32%. The good news is that more and more of that revenue in that segment is coming from the newer clients. We’ve got a couple of very large clients in OFX and they’re growing, but the really exciting thing is the new clients are activating and growing quite quickly. We continue to see that as a segment we’re going to grow globally in the medium-term.

OFX’s consumer business

Daniel Webber:

Let’s touch on the consumer side of the business, which is still important although now a smaller share of the overall business than it used to be. How are you thinking about the consumer segment?

Skander Malcolm:

It’s still a very healthy business for us and we’re good at it. We’ve particularly focused on larger-value use cases like wealth transfers, house purchases and so on.

We haven’t been marketing to go win new clients for three years now. Whilst active clients go down – the number of active clients since the first half of 21 is down 20% – revenues are up 30% in the segment. We’ve had those types of clients tend to activate when there’s periods of volatility. We haven’t seen much volatility, but there’s three or four elections ahead in the countries we serve, so we’ll see how we go.

Daniel Webber:

Skander, anything else you want to cover?

Skander Malcolm:

It’s absolutely fantastic to complete that Firma integration in less than two years, so ahead of time, generated 30% EPS accretion. There’s not too many transactions I’ve ever seen in financial services like that. The team’s in good shape and we’re very happy with that.

We’re very happy generally with our intangible investments delivering scale as well, and that can now shift into much more product-centric investments, which generally have a higher ROI and a bigger customer impact in the short term. So in good shape.

Daniel Webber:

Skander, thank you.

Skander Malcolm:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.