Australian money transfer provider OFX saw revenues decline amid macroeconomic headwinds in FY 2026, though the company still targets sustainable growth in the medium term. We analyse OFX’s latest earnings results.

Australian money transfer provider OFX reported another tough year in its earnings for FY 2026 (spanning calendar Q2 2025 to Q1 2026), with lower FX volatility and macroeconomic conditions leading to declining revenues and profits.

Having said this, the company continues to stress its moves to create “sustainable growth” in the long run as it continues to roll out its New Client Platform (NCP) – a financial services solution for businesses extending its services beyond FX to services such as cards, multicurrency accounts, AP automation and integration with accounting platforms.

This forms part of OFX 2.0 – its strategy to diversify OFX’s business and capture a higher share of potential revenue from its core segment of corporate SMEs. According to CEO Skander Malcolm, the company is positioning to expand its total addressable market for SMEs in its core markets from USD 34bn to USD 66bn, while also capturing a consumer TAM of USD 10bn.

OFX is also continuing to undergo a strategic review, which it formally commenced in February after the company received “increasing inbound inorganic interest”. Malcolm said that the review would be concluded shortly pending ongoing conversations with “multiple credible parties”.

Below, we’ve discussed key points from OFX’s FY 2026 performance and its strategy to get growth back on track.

Drivers of OFX’s FY 2026 performance

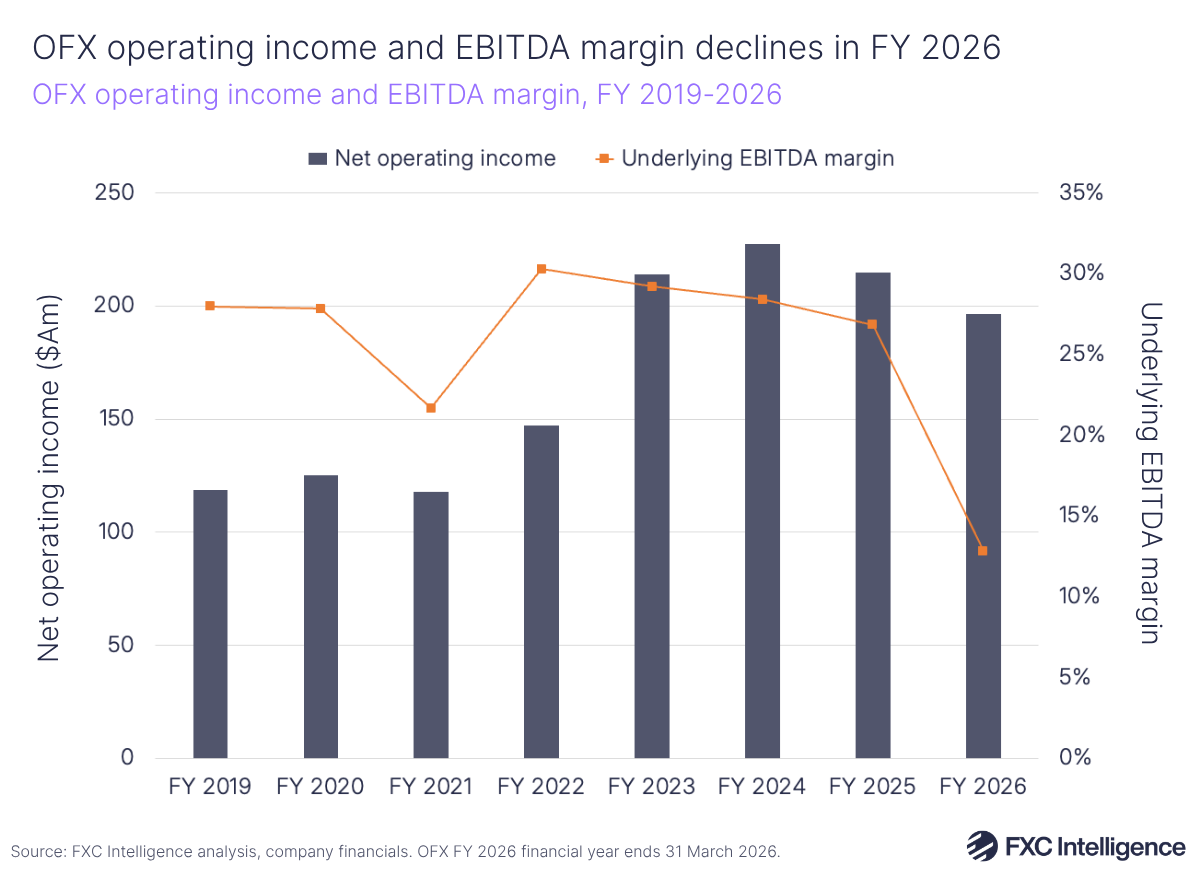

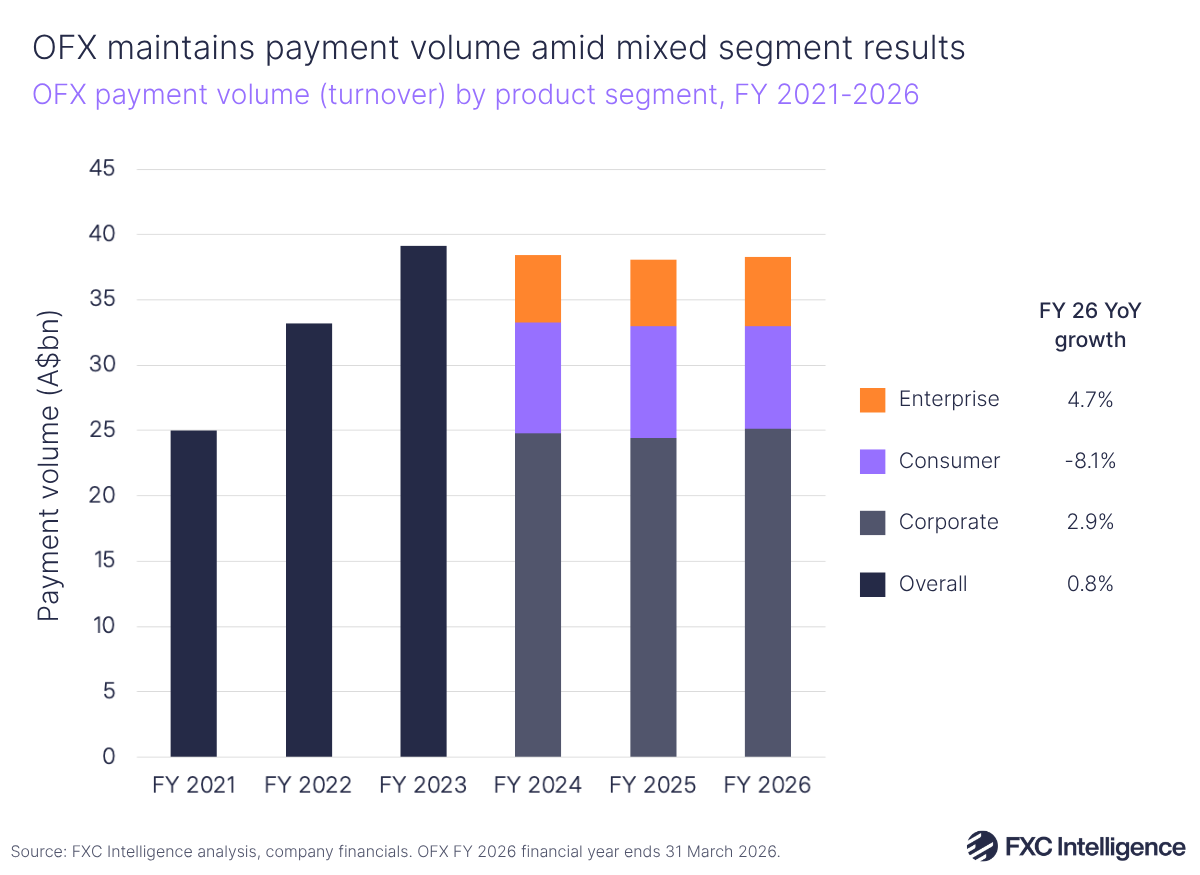

OFX’s net operating income (NOI) declined by 8.5% to A$196.6m, while fee and trading income (i.e. revenue) fell by 8.1% YoY to A$203.9m. The company attributed this to a macroeconomic environment that continues to “dampen” business confidence. Having said this, the company’s overall payments volume – which it refers to as turnover – saw incremental growth of 0.8% to A$38.4bn.

OFX’s underlying EBITDA declined by 56.4% YoY to A$25m, giving a margin of 12.8% versus 26.9% the year prior. While declining NOI accounted for just over half of the EBITDA decline, a significant portion was due to growing investments to deliver OFX’s strategy, including employment across teams, promotion for its NCP platform, GTM enhancements and non-FX platform costs.

The company also mentioned that it had seen an increase in bad debts, accounting for A$6.3m, which OFX attributed partly to a small number of incidents in its North American corporate segment.

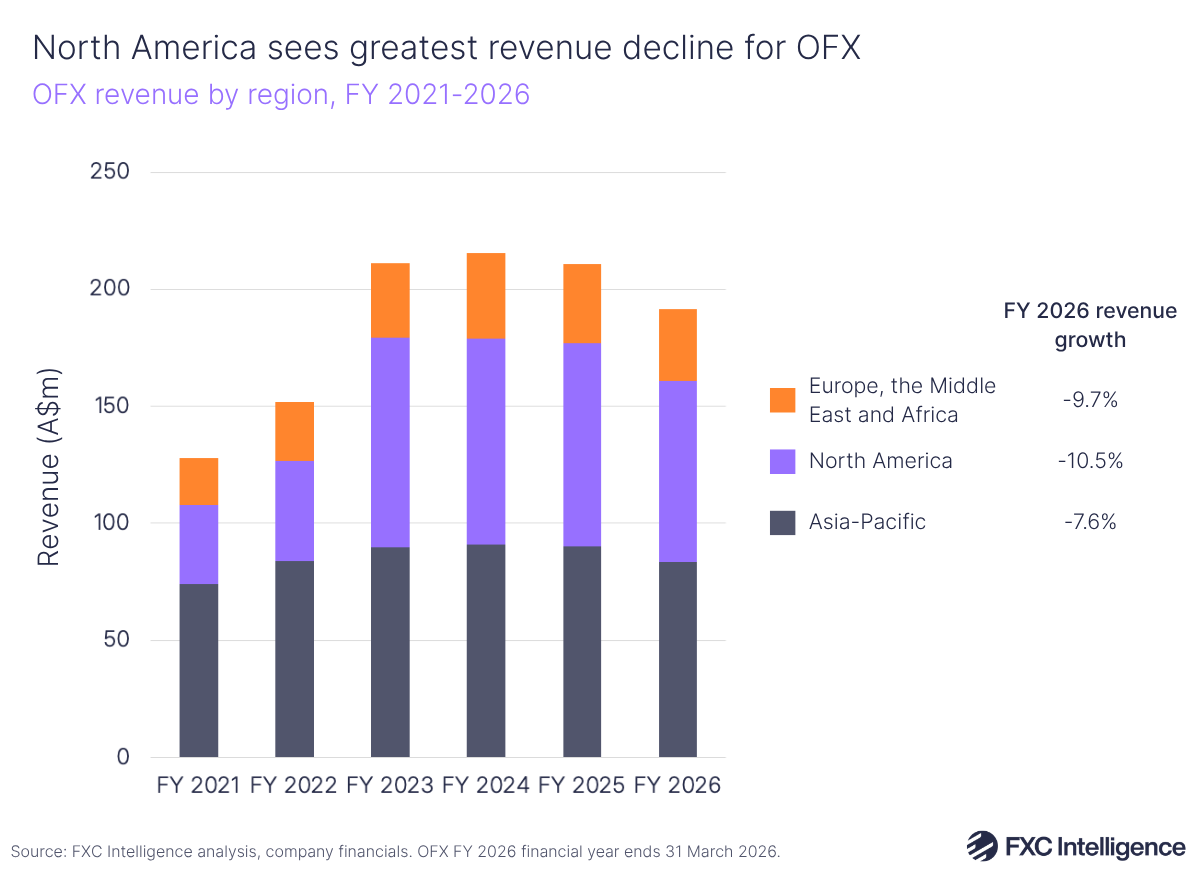

Revenues declined by 10.5% in North America, 9.7% in Europe, the Middle East, and Africa (EMEA) and 7.6% in Asia-Pacific, with client migrations to NCP across the company’s North America and EMEA corporate divisions adding a particular impact.

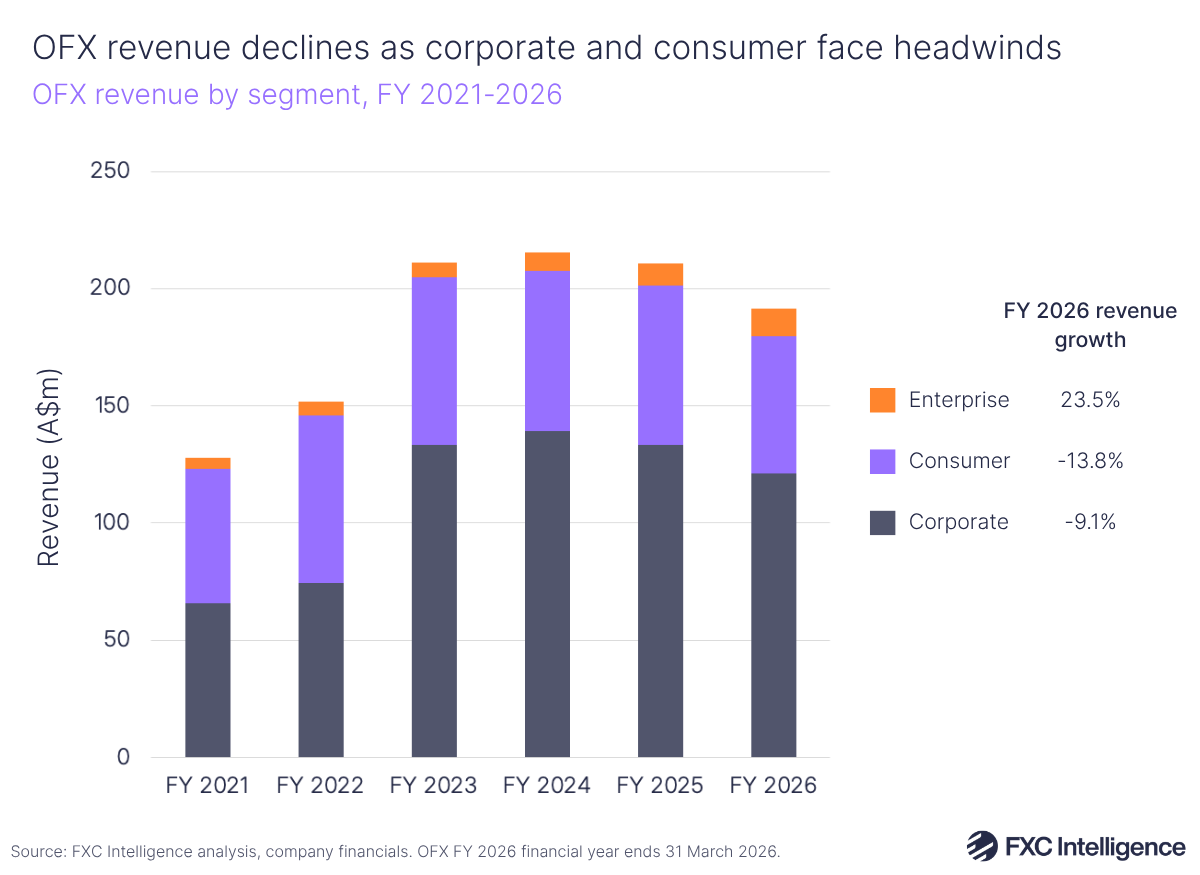

Corporate continues to take the majority of OFX’s business, but saw revenue decline in FY 2026 by 9% to A$121m, with OFX’s high-value consumer division also falling by 13.8%. However, enterprise saw 23.5% revenue growth, marking the third consecutive year with double-digit growth for this segment, with the rise attributed to partners acquired over the last three years.

In particular, OFX continues to see the impacts from weak business confidence that it noted last year in its customers and transactions. In the corporate segment, the company noted a 6% drop in clients to 30,000, with the number of transactions declining by 2.5%.

This led to a 4.1% drop in cross-currency average transaction values (ATV), while cross-currency turnover fell by 6.4% to A$19.1bn. However, same-currency turnover rose by 49.8% to A$6.1bn. OFX noted the shift in customers moving away from forward transactions in H2 2026 in its Corporate business, while the rise in same-currency transactions contributed to a lower NOI margin.

For the consumer segment, active clients fell by 13.4% to 78,300 and there was a 12% decline in transactions. This led to an 8.4% decline in turnover to A$7.8bn, though the segment did see a 4.1% increase in ATV.

During the earnings call, Malcolm noted that a decline in volatility had driven softness in consumer over the last two years, with customers pulling back on FX and transfer services. However, he added that the last two quarters had been steady for the segment on a QoQ basis. Enterprise, meanwhile, saw turnover rise by 5% to A$5.3bn.

OFX’s non-FX gains and growth targets

OFX is keen to look to future plans, with a major focus on moving new and existing customers onto its NCP. This will be key for the company’s multi-year investment, with the company aiming to drive a return to growth in 2027 as part of its OFX 2.0 initiative.

Outlined in previous earnings calls, the NCP is OFX’s scalable, multi-product platform for SMEs. The company has migrated many of its customers across North America, EMEA and Australia onto NCP, finishing the year with 90% of its corporate clients on the platform. The company saw 23,300 active clients on NCP, a rise of 70% versus H1 2026. It is looking to commence migration of its consumers onto the platform in Q4 2027.

The company is seeing increasing uptake of multiple products on its platform, with 8.4% of clients using more than one product versus 4.5% in Q3 2026. This ties into OFX growing its reputation as a business facilitating multiple services beyond transfers for businesses, with a key driver being capturing SMEs that are currently working with banks for services.

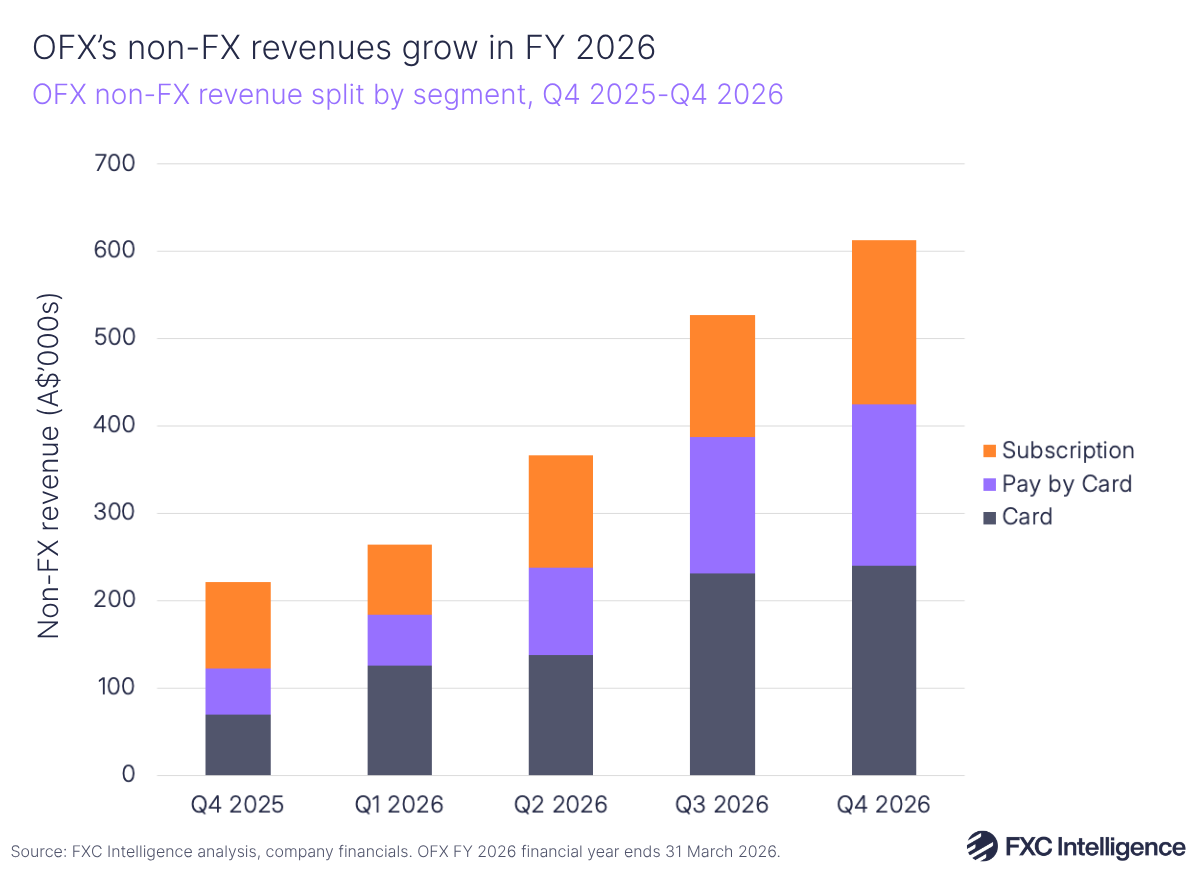

It also highlights a bright spot for OFX’s FY 2026 earnings, which was the growth of its non-FX revenues across areas such as cards, subscriptions and its Pay by Card product. Non-FX revenue grew by 177.4% YoY in Q4 2026 versus Q1 2026, with the company seeing interest income across NCP wallet balances of around A$1m in Q4 2026 alone.

Overall, non-FX revenue grew by 12.1% to A$1.8m in FY 2026. While this still accounts for a small fraction of OFX’s overall corporate piece, the rise is significant versus other areas of the company and highlights OFX’s intent to diversify as it targets a return to growth

OFX is also one of several public players espousing productivity benefits for AI in its latest earnings, and is working on using AI to simplify workflows for clients and accelerate onboarding processes.

In its H1 2026 earnings, OFX had pitched that it was aiming for 15%+ NOI annual growth by FY 2028, with an underlying margin of around 30%. In its latest earnings, it has changed the framing of these objectives slightly to being in the “medium term”.

Malcolm said that the company expects its consumer segment to establish in FY 2027 and return to growth thereafter. He added that recent growth in new trading clients (up 8% YoY in FY 2026) as well as a rise in customers using multiple products on its platform gives the company confidence it can grow in 2027.