OFX reported a period impacted by economic uncertainty for H1 2026, in which it missed previous expectations. We spoke to CEO Skander Malcolm to discuss how OFX is navigating a period of significant change and its plans to return to growth.

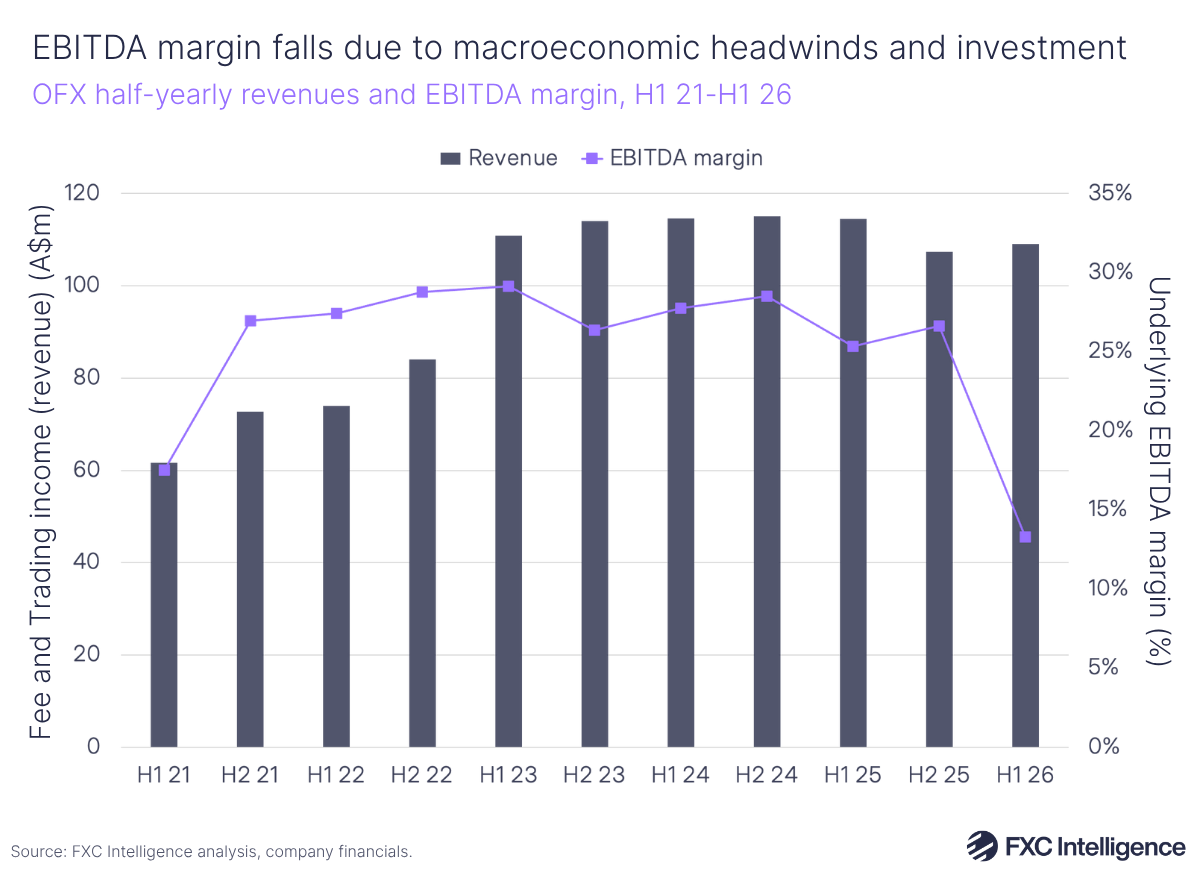

OFX has reported its earnings for H1 26 (covering calendar Q2-Q3 2025), with fee and trading income falling 5% YoY to A$109.1m and net operating income (NOI) falling 6% to A$105m.

The company also reported a significant decrease in underlying EBITDA, by 50% to A$14.5m, resulting in an underlying EBITDA margin of 13%.

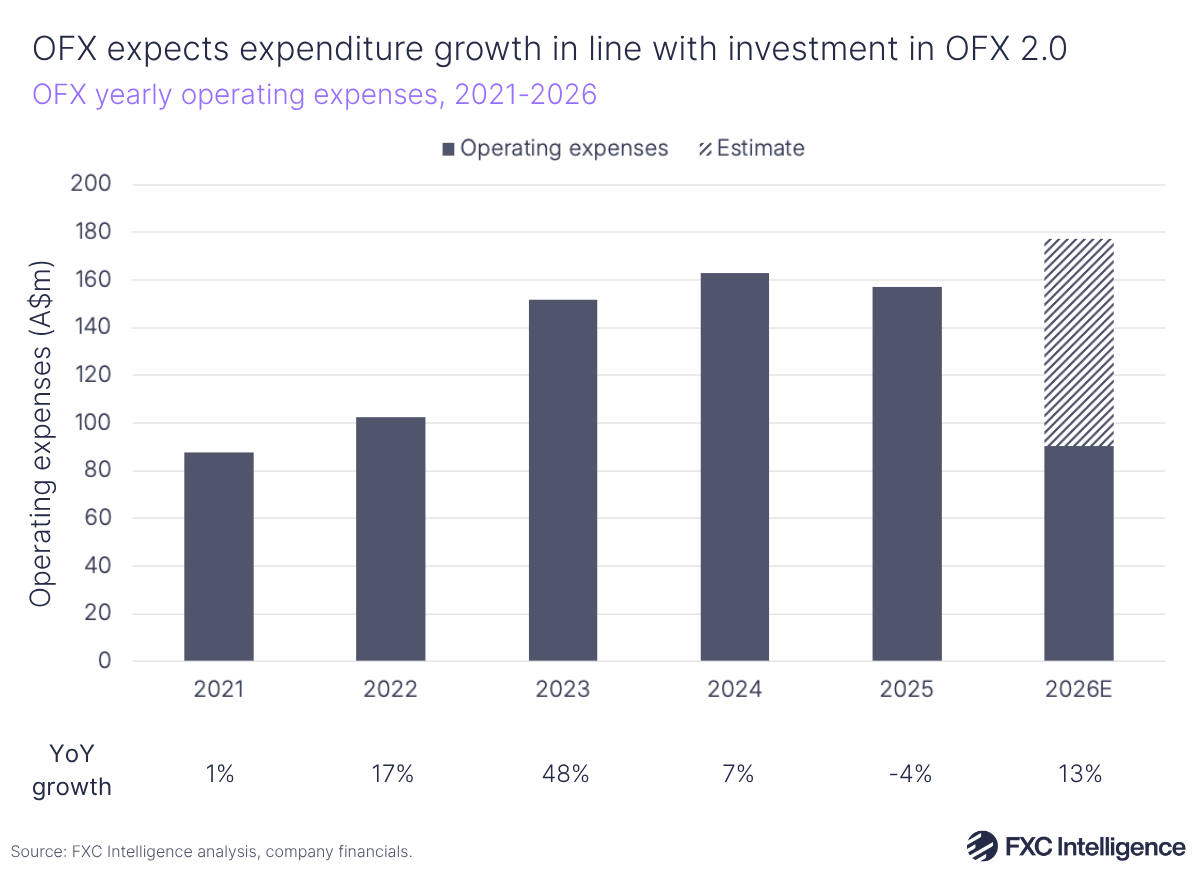

These dips come as OFX invests heavily in its OFX 2.0 platform, through which it is ultimately aiming to double its total addressable market (TAM) and diversify its income sources, with a particular focus on growing non-FX revenue. As the company looks to accelerate its transition to OFX 2.0, its underlying operating expenses grew 10% YoY to A$90.5m.

To find out more about OFX’s recent performance and how it plans to achieve future growth, we caught up with CEO Skander Malcolm.

Progressing OFX’s global strategy

Daniel Webber:

Talk us through OFX’s performance in H1 26.

Skander Malcolm:

In terms of our strategy, we shared back in 2018 that we were pivoting to be focused on B2B and that we were intent on growing more globally. We then implemented various technical transformation projects to help us do that at scale. We also acquired Firma in Canada, which was a global B2B business.

In 2023, we finished the technical transformation, with the last step being the frontend and our wallets. We also found a small licensed company operating here in Australia called Paytron that had that capability.

We initially acquired Paytron for its technology and team but as we got closer to their value proposition, we learned that that opportunity was much more than just wallets and cards. We found that AP automation, expense management and all of the other tasks that SMEs are doing today could be managed by that platform. As a result, we pivoted and accelerated into the broader AP automation space.

Fast forward to now, we announced in our H1 results that we are now live in every major market in the world. We went live in the US a few weeks ago with our full suite of products and our platform is now live in every major market.

Now, we’re in the process of completing the migration of our existing clients onto that platform, which should be around 80% complete in major markets by the end of this quarter. We plan to really ramp up efforts to cross-sell those products, features and services in the coming year.

OFX targets return to growth following disappointing results

The 5% YoY decrease in fee and trading income, 6% fall to NOI and 10% growth in operational expenditure resulted in OFX’s underlying EBITDA margin falling to 13% – significantly lower than the 25% margin seen in the same period in the previous year.

During its latest earnings call, the company explained that it had experienced a period of softer trading, which, combined with the company’s deliberate increase in investment into its transition to OFX 2.0, resulted in disappointing financial results. Selena Verth, OFX’s CFO, explained that “ongoing macroeconomic uncertainty” led to reduced business confidence across much of the globe. In fact, the company said that it saw a 6% decline in APAC, an 8% decline in North America and only a 2% increase across EMEA.

Despite headwinds, the company is targeting NOI growth in H2 26, as well as an underlying EBITDA margin of around 30% in FY 2028.

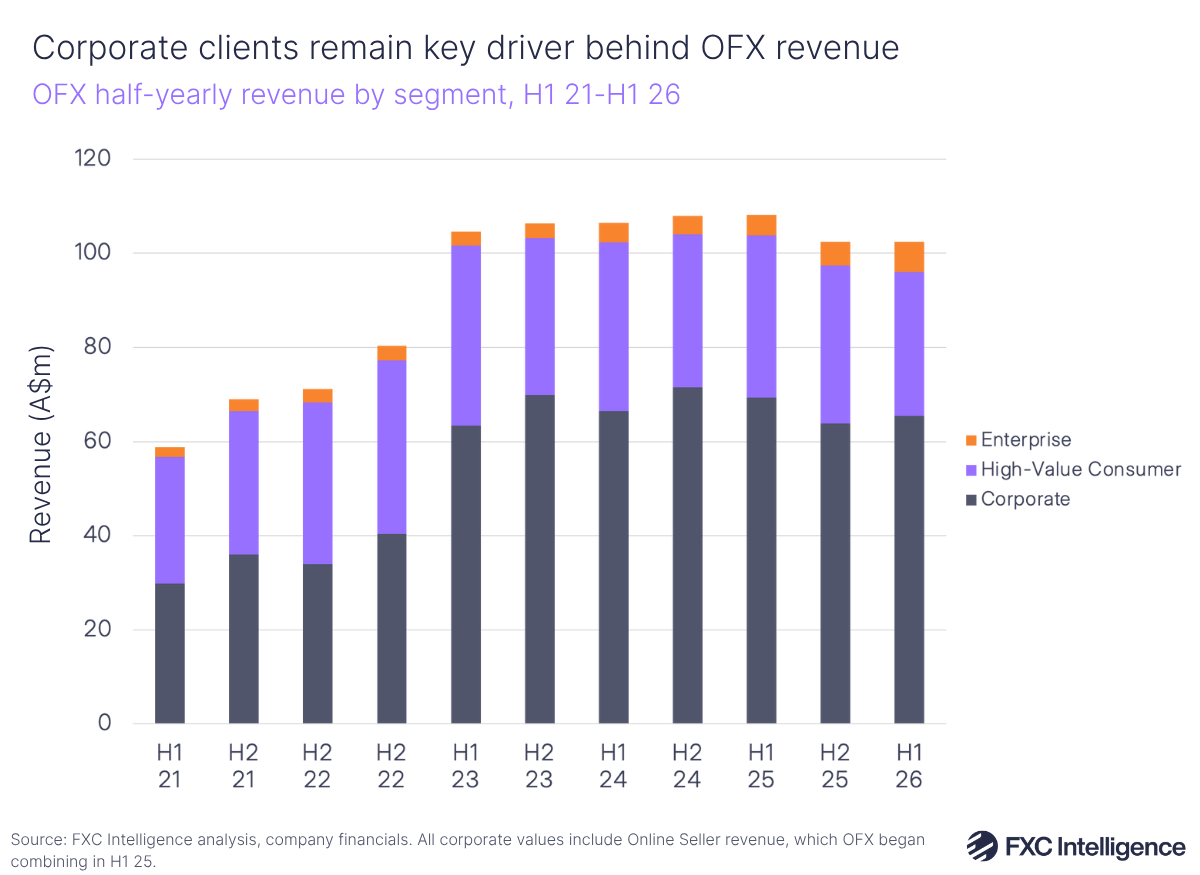

B2B revenues fell by 2% compared to H1 25, with OFX’s Corporate segment, which is the company’s largest contributor to its revenue (with a 64% share), falling 6% to A$65.4m. However, the smaller portion of OFX’s B2B revenues from the Enterprise segment did increase by 48% YoY – from A$4.4m in H1 25 to A$6.5m in H1 26. High-Value Consumer (B2C) revenues declined more quickly than B2B, at 11% YoY to A$30.6m. OFX attributed this drop to “unusually quiet market conditions”.

Focusing on non-FX revenue growth

Daniel Webber:

What can you tell us about your plans to grow non-FX revenue?

Skander Malcolm:

I think that the industry has done an outstanding job of offering much better integrated platforms to SMEs for managing their businesses than banks can offer. With that, AP, AR, expense management and other products are all earning very good revenue by earning interest.

OFX is also on that journey. In Q2 26, we grew non-FX revenues just under 24% and that’s excluding any kind of interest income.

We’re seeing the take-up of products from new clients, certainly in line or higher than our expectations. The growth in customer balances has been significantly better than our expectations.

When we look at the industry growth in terms of revenue and clients, it’s largely coming from that integrated value proposition. Meanwhile, most of the growth in revenue is not coming from FX, but from clients using platforms to do more than just FX.

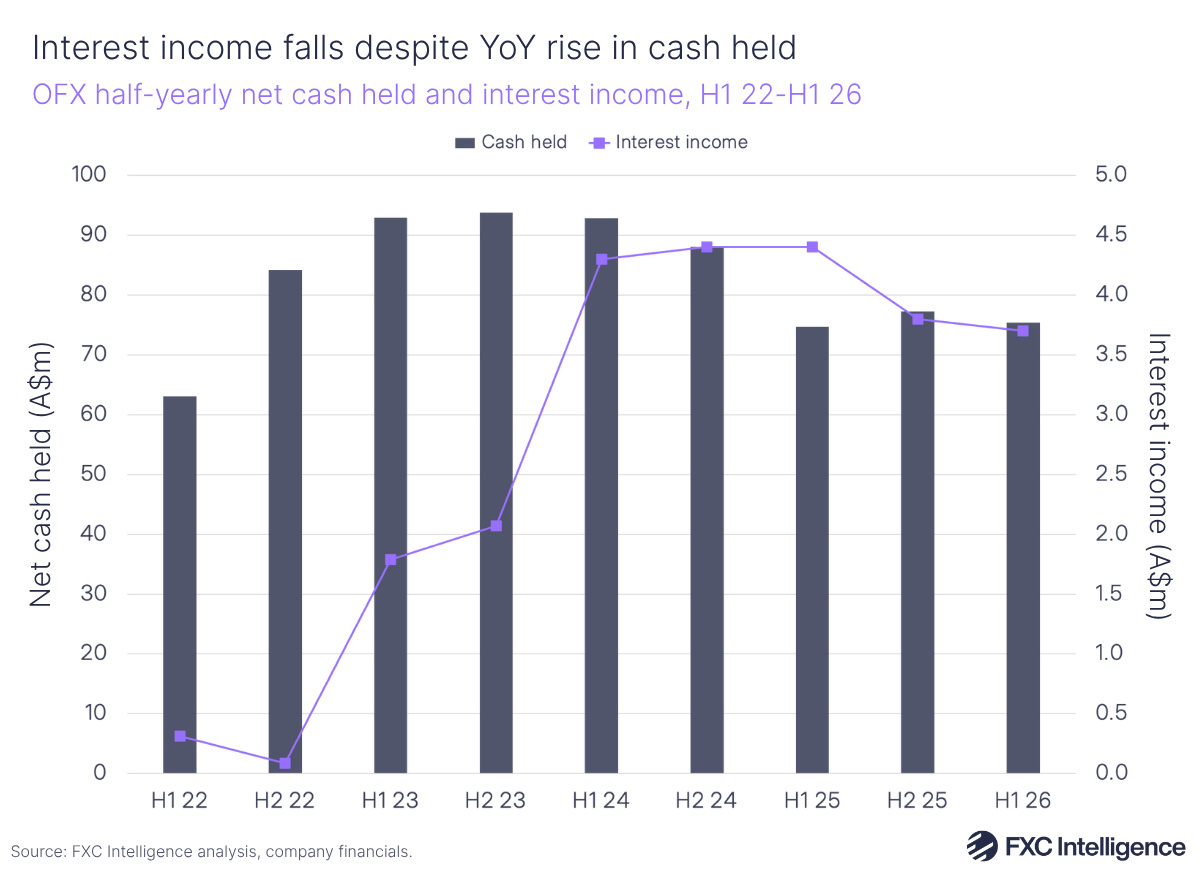

OFX sees non-FX revenue fall YoY, while growth in cash held offsets interest rate cuts

OFX reported that its non-FX revenue, which includes revenue from cards, Pay by Card, subscription and other payment fees excluding interest income, fell from A$0.9m in H1 25 to A$0.6m in H1 26. During the earnings call, it attributed this fall to a vendor switch, which it addressed prior to Q2 26 (calendar Q3 25).

Following this, the company saw 24% growth of non-FX revenue in Q2 26, when compared to Q1 26, with over 6,000 clients now holding an interest-bearing balance on the platform – indicating positive signs of growth.

OFX also saw interest income dip 15% YoY to A$3.7m. This income was largely affected by rate cuts, although the company noted that its interest income remained flat compared to H2 25, despite two further rate cuts in the last half.

As a result, OFX managed to outgrow the recent rate cuts thanks to building cash balances across all regions. These efforts led to a slight YoY rise in the net cash OFX held to A$75.4m.

Looking to the future, the company plans for its transition to its New Client Platform (NCP) to bolster interest income even further through wallet functionality, which enables clients to hold cash directly with OFX – expanding the company’s net cash available.

Global trends and market opportunities

Daniel Webber:

What different trends are you seeing across the globe?

Skander Malcolm:

We saw significant uptake on subscriptions and cards in Australia. We have a particular nuance in Australia, which is that Australian SMEs love loyalty points. One of the products that we offer enables clients to fund an invoice into their wallet using a card which attracts points from a different issuer. They then get points from their issuer and they can pay their invoice with OFX. In H1, we saw that trend begin to ramp back up. In other parts of the world, we offer cash back on the transactions themselves.

The biggest single surprising data for us in H1 was the growth in balances in Australia. We’re seeing that Australian SMEs are very happy to fund their wallet, whether it’s sitting in US dollars, Australian dollars, sterling or euro, and they will plan out all of their transactions for the coming month and use it a little bit like their working capital account. We see that as a great sign of engagement and that they trust us. We of course take that very seriously.

As we launch in other parts of the world, we learn new things. We also launched the first fully digital forwards product. We’ve already seen clients self-select into that product in the UK and in Australia, which is encouraging.

Investing in OFX 2.0 to capture global market opportunities

OFX says that its 2.0 platform should enable it to capture a larger TAM in its core markets: namely Australia, New Zealand, Canada, the US, Hong Kong, Singapore, the UK and the rest of Europe (including the Nordics). It estimates that it can expand its TAM from $34bn to $66bn with OFX 2.0.

Via market research, the company says it found that between 77% and 87% of clients that need the cross-border transfer products and services it provides are trying to get them from banks. However, it also found that more than 74% of SMEs would be willing to switch away from banks if they were offered the right combination of products and services. As a result, OFX is doubling down on investing to win over some of these clients, through which it predicts it can achieve higher revenue per client.

As it looks to accelerate its transition to OFX 2.0, the company has reported a 10% YoY increase to its underlying operating expenses to A$90.5m in H1 26. Looking at its projections for FY 26, OFX estimates that it will deliver operating expenditure in the range of A$173.7m to A$181.2m.

The midpoint of this range suggests that OFX plans to close to match its expenditure in H1, spending around A$87m in H2. This would see the company reporting a higher operating expenditure than in any full-year period previously, and see a 13% rise compared to FY 25.

Leveraging stablecoins and AI

Daniel Webber:

AI and stablecoins remain two of the biggest topics in the industry. What are OFX’s plans in regard to each of these?

Skander Malcolm:

We’ve been looking at and studying stablecoins, as well as talking to various industry players. We think the most likely use case for us in the short term would be to use stablecoins for treasury management. We’re looking at a number of opportunities in that space.

We have also been experimenting with AI, largely on internal use cases. We’ve used it a lot in things like bank reconciliations. We’ve been experimenting in terms of building out agentic AI for our service teams, but it’s largely experiments. We’ve also done some customer facing experiments – for example, when clients upload receipts, we’re using OCR to read the receipt and then AI to categorise them.

There’s a very significant set of opportunities that we’ve got plans for AI which we’ll reveal in due course. We need to be agile and jump on the things that work and scale them and quickly pivot when we see that things aren’t working.

Daniel Webber:

Is there anything else you’d like to cover?

Skander Malcolm:

We feel incredibly encouraged by the execution around the world because it’s quite a big undertaking to put a new platform in place all around the world.

Now, OFX is truly global. It’s a huge undertaking to ask all your clients to move from one platform to another, and to see that go so successfully is very encouraging. Ultimately, we’re feeling very energised by the possibilities.

Daniel Webber:

Excellent. Skander, thank you very much for your time.

Skander Malcolm:

Thanks Daniel.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.