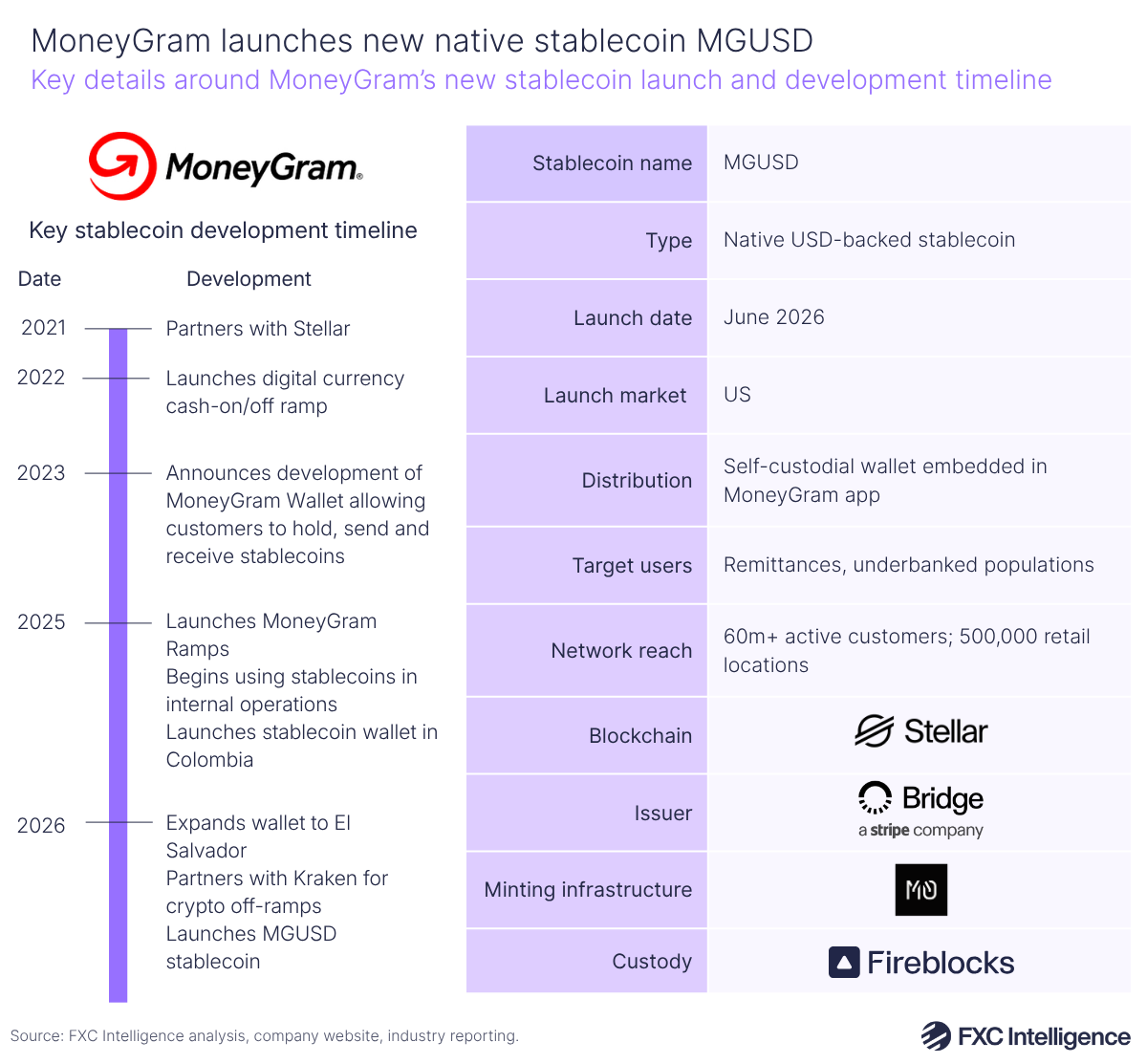

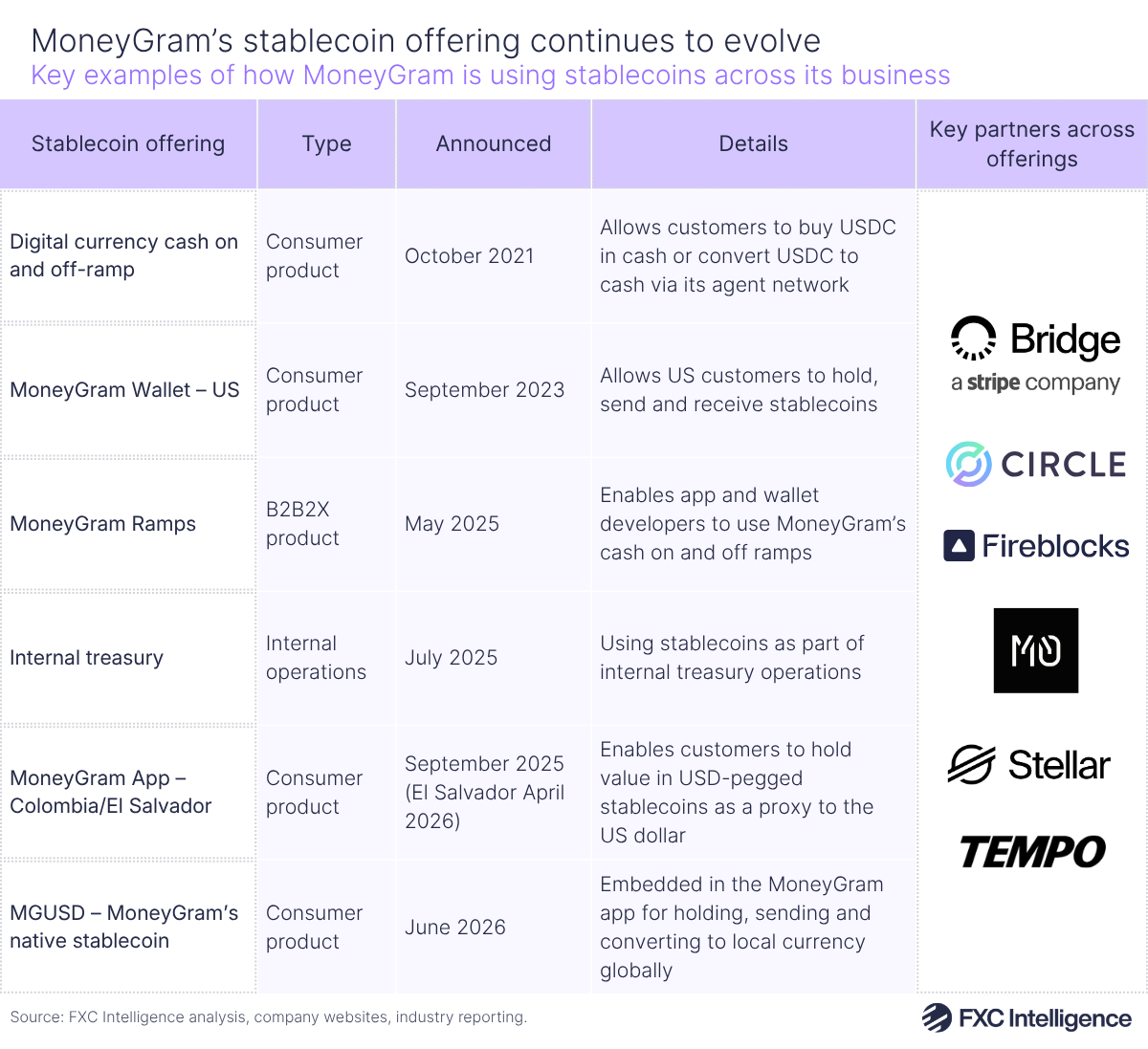

MoneyGram has launched its new USD-backed stablecoin, MGUSD, which customers will be able to access directly from a self-custodial wallet. We spoke to CEO Anthony Soohoo at Money20/20 Europe to find out more about its stablecoin strategy going forward.

This week, MoneyGram announced the launch of MGUSD, a native USD-backed stablecoin, which it said will become the “foundation for a growing suite of financial services across its global network”.

The stablecoin is powered by a number of partnerships, with Stripe-owned Bridge as the issuer and M0 providing infrastructure for minting and burning MGUSD tokens, which will then be deployed on the Stellar blockchain at launch. MoneyGram will hold MGUSD in wallets powered by Fireblocks, which will be used to pay out to individual customer wallets embedded in the MoneyGram app.

Launching initially in the US, MoneyGram plans to expand MGUSD globally, with the goal of creating lower costs for consumers, as well as supporting their demand for stable dollar balances amid inflation, currency instability or limited access to financial services. It marks another step from a major cross-border player into issuing its own stablecoin, with Western Union launching its own USDPT token last month.

For MoneyGram, the launch is the latest move in a digital currency strategy spanning back five years, having initially partnered with Stellar in 2021 to settle transfers using Circle’s USDC stablecoin. It has since built out crypto cash off-ramps and recently went live with a USD- backed stablecoin app in Colombia and El Salvador.

The launch also forms part of MoneyGram’s “refounding” strategy, as part of which it is continuing to shift from an omnichannel remittances player to a fintech with a global digital and cash network. MoneyGram serves over 60 million customers across its network spanning nearly 500,000 retail locations, with more than 70% of transactions now digital.

We sat down with CEO Anthony Soohoo at Money20/20 Europe to discuss MoneyGram’s stablecoin plans, how it will drive utility for agents and consumers in its network, as well as the future of MoneyGram in an increasingly AI-driven marketplace. You can watch our full interview with Anthony or read the transcribed Q&A below.

Why MoneyGram launched its own stablecoin

Daniel Webber:

Anthony, a pleasure to be with you at Money20/20 today, and you’ve made a big announcement: MGUSD. Talk to us about that and why you’ve decided to launch it.

Anthony Soohoo:

It’s a big moment for us. This is a moment we’ve been waiting five years to do, because we’ve been working on stablecoin for the last five years and we came to a place where we believe minting our own coin would add value.

MGUSD is a native US dollar stablecoin that we’re issuing and using as a foundation to build all our future services on our network, including how we work with our agents and also how we deal with the consumer. It is not a stablecoin that we’re going to operate and put out there in the wild for other networks. We’re strictly focusing on running that on the MoneyGram network.

How MoneyGram’s MGUSD will support agents and customers

Daniel Webber:

Let’s start with the agents actually, which is a very important part. You have one of the biggest cash networks in the whole world. How will the stablecoin work with agents and how will you hope to support them?

Anthony Soohoo:

If we take a step back, when we think about stablecoin, we look at it as infrastructure. When we think about infrastructure, it’s all based on the fact that we’ve been rebuilding our complete payments infrastructure on blockchain. We’re going to be an open network, we’re going to run multiple types of blockchains on our network. And then within that network, what we can do with our agents is to pay in and pay out. We have to fund these partners and there will be a journey, but we could see a day where we can settle with them in MGUSD.

Then you translate that to the consumer. How does that play out? We have 60 million active customers. We can see a customer going in either through the app or at one of our physical locations, funding their account and converting it into MGUSD and then converting that cash and holding that in terms of doing the send. And then on the receive side, that customer would receive and hold in MGUSD, have the stability of a stable dollar balance and then when they are ready to convert, they convert it to whatever fiat they would use it for.

Could MoneyGram’s MGUSD change its economics?

Daniel Webber:

How does having your own stablecoin start to change the economics for your business?

Anthony Soohoo:

We’ll see how that plays out, I won’t make any broad proclamations. But theoretically, if you play it out, we believe that with stablecoins, because of the nature of instant settlement and transparency as well as the way you can drive higher velocity in your cash [in terms] of how you settle, there’s going to be savings around FX as well as how you cycle through cash.

If you think about most people when they’re running businesses, especially retailers, you’re trying to drive up inventory turns. Stablecoin has a promise to drive up inventory turns of our cash. Now that needs to be played out because there needs to be some level of liquidity before you really start seeing that benefit, so we’re going to see how that goes.

Daniel Webber:

There are some really strong partners that you’ve brought into this journey with you. Talk through where each of them fits in for you.

Anthony Soohoo:

We use Stellar for the blockchain. Stripe, they’re helping us with the minting and the orchestration. And then M0 does the smart contracts and those are really the key things to make this thing work on our network. So yeah, it’s pretty exciting.

Inside MoneyGram’s “refounding” strategy

Daniel Webber:

You’ve talked to us before about “refounding” a company that’s been around for not just 10, 20 years, but for 85. Where does this fit into that refounding story?

Anthony Soohoo:

You probably have heard boards as well as leaders talk about wanting their companies and employees to act like owners. Refounding just takes that up another level, where we want everyone to think like founders. What we mean by that is we want them to take ownership, but we also want them to treat it like it’s the company that they’re owning and founding, and they’re taking a look at how things are done today and how they can be done better.

And then in addition, having this intensity of driving change inside the organisation so that we deliver a better outcome for our customers and ultimately our investors. That’s really, in my mind, the definition of refounding. It is for us to get all our employees to think about themselves as refounding the company and we’re rewriting all the rules about how MoneyGram works. What we want to shoot for is to operate with the speed and agility of a startup, but also leveraging the scale and efficiency of a large organisation.

Adaptability in MoneyGram’s company culture

Daniel Webber:

You’re really trying to drive a lot of change and energy through an organisation that has a lot of scale, and wrote in a blog recently about businesses moving from “peacetime to wartime”. Talk us through that.

Anthony Soohoo:

Peacetime originally was centred around the idea of a blog post that Ben Horowitz from a16z wrote, and the idea was organisations that are in peacetime try to drive not just through consensus, but it’s a slow, methodical way of going after opportunities, where you try to do incremental improvements and when you look at opportunities, what you’re trying to do is play defence and not risk the biscuit.

That plays well until you have disruption coming in the market and then at that point in time, what you need is high-fidelity decisions that are made quickly, and you don’t necessarily go after 100% consensus because not everyone’s going to be in agreement, but you follow a leader who’s going to do it. A company culture needs to evolve depending on the competitive nature of where it’s going, and especially the nature of where the world’s going.

In this world where AI is coming in and redefining roles and you have a lot of new changes that organisations need to embrace (digital currency is one of them), when you think about the idea of agentic commerce for every organisation as well as just AI in general, we need to rethink the whole workstream and how things go. So in those places, you really need someone that overlooks all this and thinks through not just what happens in my function, but how this plays out across the org in terms of how work gets done.

So I explored in this article how that plays out in company culture. I cited Yahoo when I was there during peacetime and the stock was going up and it felt great. But eventually when Google came in, wartime hit and they were too slow to react. Certainly, it’s a warning and also for us it’s an inspiration about what to do and what not to do. That’s why I wrote it, and I think I came out of it with a few more ideas about how we can get better, which is always great.

Daniel Webber:

Where do you think you are on the refounding? Where do you think you are on the journey at MoneyGram?

Anthony Soohoo:

Well, the interesting thing about the spirit of continuous improvement is you’re never at the finish, but you always strive for it. If you ask me today, I would say we’re probably at a 5 on a scale of 1 to 10. We might be further ahead actually if the world stayed static, but since the world will continue to evolve, I don’t think you ever want to feel so comfortable that you get out between a 5 and a 6. You want to be there because you want to be hungry enough and open-minded enough that you can always make that change.

Over the next few years, the world’s going to change dramatically with AI, with digital currencies and agentic commerce all kind of converging together, and we’ll see how it all plays out.

Will AI change customer behaviour?

Daniel Webber:

Do you have a sense of how your customer behaviour is going to change, particularly in this AI world? Are they all going to be making agentic payments and never going to be interacting with you, or will they still be involved with cash for example?

Anthony Soohoo:

We’ll have to see how it plays out. If you watch consumers, a lot of them are embracing this concept of automation and personalisation. But at the same time, you are also seeing a backlash on complete autonomy and giving it to AI to handle.

The way I believe it’s going to play out is that actually having a physical network is going to be a bigger and bigger asset over time. I feel great about the fact that we have omni-channel – stores and a digital presence – because in terms of benefit for the consumer, you can do all the streamlining on digital, but eventually if you want to send or receive, you might want to talk to a human being to make sure it’s not a deepfake. So that gives us an advantage.

The other point is a lot of times for large-dollar purchases in retail and probably large-dollar sends, you want to talk to a real human being. You go to a bank branch. In our case, it’s going to be the same. So, you potentially place the order on your app, but then you won’t finish the transaction until you talk to a human being. It could play out that way in terms of being hybrid and as the world goes more and more to AI, that the idea of having a physical presence is even more and more important.

Where MoneyGram fits in the cross-border payments space

Daniel Webber:

We were very pleased to announce MoneyGram was on our Top 100 most important cross-border payment companies in the world. In this ecosystem, what’s the positioning that you would like MoneyGram to have in the market?

Anthony Soohoo:

Obviously I want us to be number one, but we’re far from it today. My goal would be that we’re going to control what we can control. We’re going to focus on what we can focus on. Today, as I mentioned, we are building our whole infrastructure on blockchain, and MGUSD that we announced today is just a real foundational part of that infrastructure that we’re going to enable new types of services powered and enabling and using MGUSD. But there’s going to be other things that we’re going to plug on top as well.

What we want to be is the most ubiquitous, but really the most efficient and effective cross-border payments network around the world that operates in the physical and digital realm that also is the bridge between fiat and digital currencies. If that plays out, hopefully we’ll be in a spot in the top 10 and maybe even the top 5, but that would be our vision. At that moment, remittance will probably just be one of the things we do really well, but there might be other use cases.

We will see who else uses that network, but the reason we built our rails product was to allow people to use our network in different ways and our announcement a few weeks ago with Kraken, where we’re their cash off-ramp exclusively right now, is another sign in that direction. The most “crypto exchange” around, Kraken, finds value in giving people cash because right now, in a lot of economies around the world, that is still how they conduct their transactions. So, I don’t think that that’s going to go away completely, but people will be much more intentional when they need cash and when they don’t need cash.

Where MoneyGram is investing to drive change

Daniel Webber:

What else are you thinking about over the coming year?

Anthony Soohoo:

When I think about my goals for the organisation, it really is around three things. It’s constantly improving and enhancing the skills of our team, and that’s about retraining the team we have as well as bringing world-class talent. We recently brought in a new CFO, Marc Winniford. We’re thrilled that he’s here and we continue to build out his bench. He’s brought in some really great talent in the FP&A function in our organisation.

We plan to continue investing across our product org, as well as our retail org and our MGO org. People is going to be one of the areas that we’re going to continue focusing on, how we can get better while streamlining the work.

Then there’s product, and product is near and dear to my heart. How I think about our progress is, is that stuff translating into the products our customers feel and touch, our agents feel and touch, and are we delivering a better experience for them? I think you’ll see drastic improvements there.

And then our network will be stronger and I believe there will be a lot more partners that sign up and strengthen our overall global network. So, maybe the best thing to say is stay tuned.

How FXC Intelligence supports MoneyGram

Daniel Webber:

FXC Intelligence and MoneyGram have been working together for a while. How do you see our role in the industry as well as potentially some of the ways that we can work together?

Anthony Soohoo:

The data you guys share, we use for pricing and some of the other functions. But I would say that you guys are probably as much a connector to insights as anything else, and it’s super helpful working with you and building relationships with you guys. Especially, as I’m a new CEO at MoneyGram and even now I feel like I’ll never feel like I’m not the new guy. But it’s always fun to have a friendly voice to talk to if I ever have issues.

Daniel Webber:

Anthony, thank you very much. Congratulations on the announcement. We wish you much success with that and again congratulations as well on making the top 100.

Anthony Soohoo:

We really are thankful about and appreciative of the recognition.