Artificial intelligence has become a major focus for payments, but leadership expectations can face implementation challenges. As Dutch bank ING moves from AI experimentation to practical reality, CTO Daniele Tonella shares his hard-earned insights on the real-world implementation of agentic AI.

Artificial intelligence, and in particular agentic AI, have been drawing considerable attention from across the financial services sector and beyond. Senior leaders have been quick to extoll the productivity virtues of the technology, with many publicly traded companies drawing a direct line between AI initiatives and cost savings.

However, as anyone who has spent time working with AI tools will know, the technical reality can be more complex. How an organisation approaches AI and agentic deployment can have a profound impact on the end results, and expectations do not always align with reality.

One company that is well aware of this is Dutch banking heavyweight ING, which has spent the last few years engaging in organisation-wide experimentation with the technology.

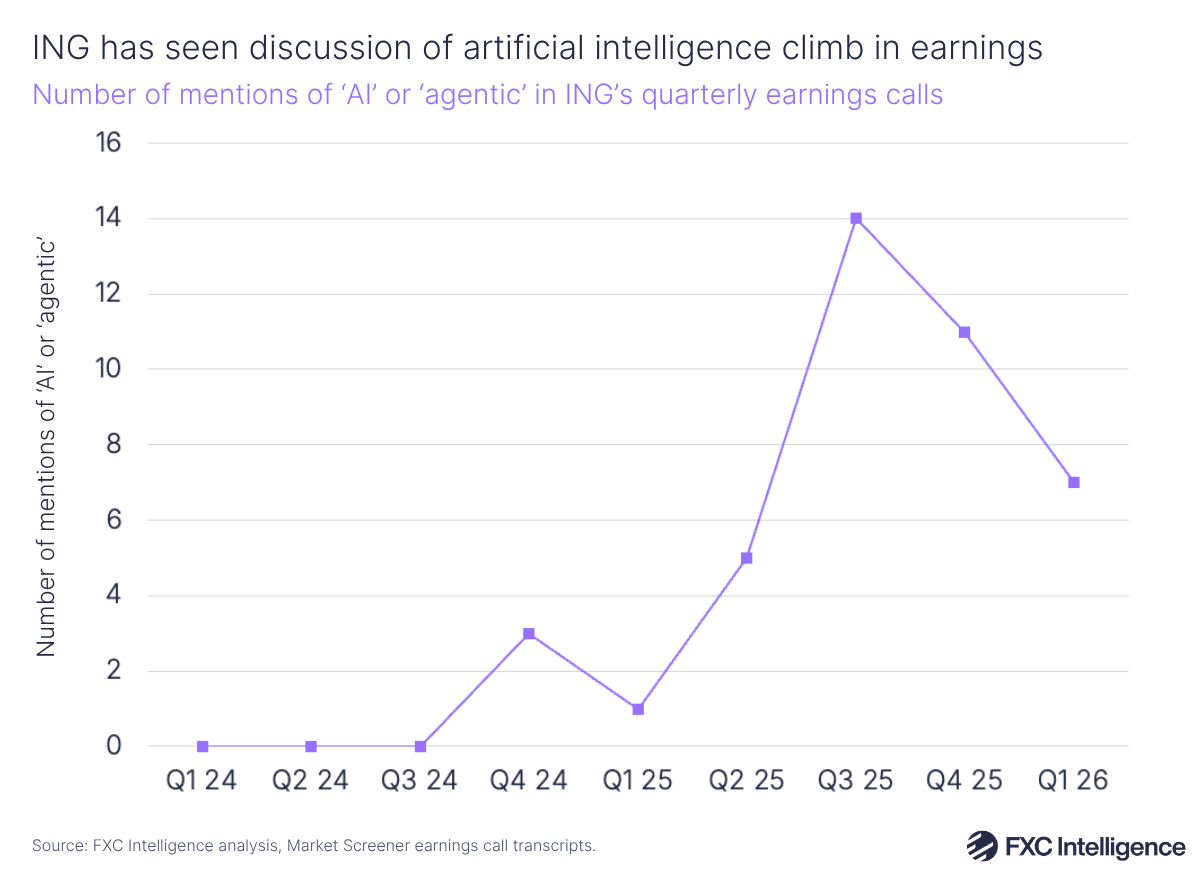

“We are now exiting the experimental phase and entering the industrialisation one,” explains Daniele Tonella, CTO of ING, one of the bank’s senior leaders who has been on the front lines of its AI initiatives.

This shift in phases has been accompanied by a number of high profile announcements. At Money20/20 Europe at the start of June, ING, along with partners Worldline and Mastercard, announced the successful execution of Europe’s first end-to-end agentic payment transaction, while the company has also announced its use of agentic AI to speed up mortgage decisions.

However, the company’s use of AI goes far deeper than a handful of consumer-facing applications, and the insights ING has gleaned from its implementation of the technology have wide-reaching implications for banking and the wider payments sector’s use of agentic AI.

I caught up with Tonella to find out more about how ING has been using the technology, where the biggest gaps between expectations and reality sit, and what the agentic bank could ultimately look like.

Inside ING’s AI rollout

Lucy Ingham:

Starting at a high level, how are you approaching artificial intelligence investment and development, in particular related to agentic AI?

Daniele Tonella:

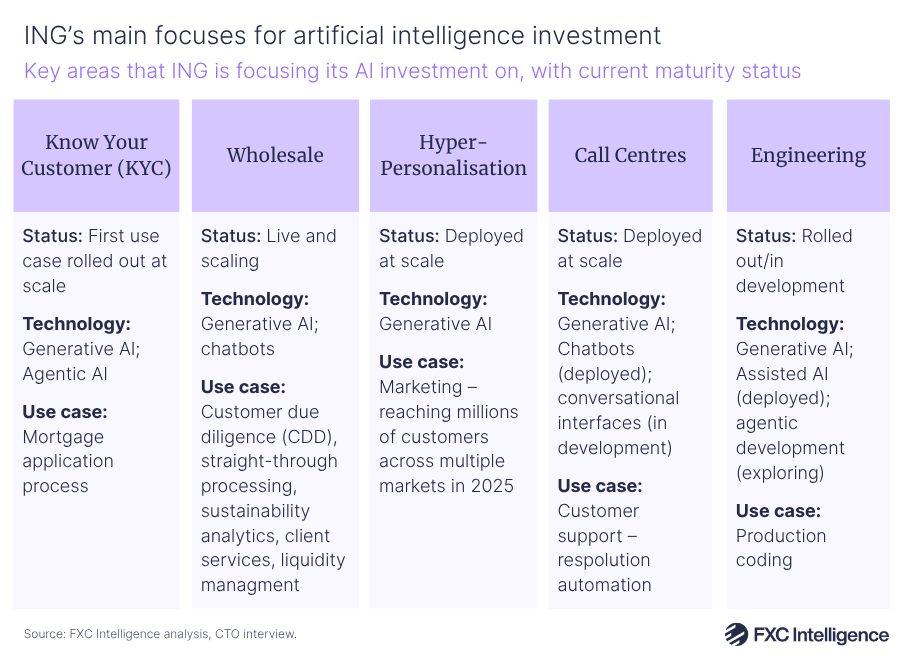

We have chosen five areas where we are investing in AI in general, and agentic specifically, which is in the KYC space, in wholesale lending, hyper-personalisation, call centres and engineering, obviously. These are the five areas we have been exploring.

So far we have rolled out two major use cases at scale. One is in call centers: first chatbots and now we are exploring conversational interfaces. And in mortgages, we have an agentic mortgage process. If you apply for a mortgage in the Netherlands, the process behind the scenes with your documents, before you get the money, is a hybrid of human and agentic. That’s already happened. That is giving us, essentially, more scalability because we can manage more mortgage volume with the same amount of people.

In engineering, we have rolled out assisted AI, so it’s not agentic yet. Essentially, the vast majority of our coding engineers get suggestions by AI. About 27% of the code that gets into production is suggested. And now we are exploring agentic software development, which is a hybrid of autonomous engines that take over a number of activities end-to-end from developers.

Lucy Ingham:

A lot of your initiatives sound like they are more under the hood than client-facing. What is the split there?

Daniele Tonella:

The majority are not immediately visible from the client side. There are multiple levels of hoods, but it’s definitely below the client hood, except chatbots and, at some point, conversational AI. We cannot afford to make stupid mistakes at the client interface, so this is not where we’re going to experiment first.

Below the hood, there is plenty of banking work, like KYC, where we might even start only with document management. KYC is a lot of manual work on documents, and AI can be a fundamental help in that space.

Or listening to client signals. If you are on Google reviews or Trustpilot or whatever platform, that can be agentically read and compiled for the purpose of eliminating friction for clients. That’s under the hood. You will not see it if the thing that was annoying you suddenly disappears, but maybe because you wrote it on a Google review, some bot was reading and was conveying the message to the one owning the application.

Lessons learned: Strict governance, clean data and beyond

Lucy Ingham:

What have been the main learnings from your initiatives so far?

Daniele Tonella:

We have learned a couple of things over time. One is, two years ago, we started with a very strict governance that says only the Chief Analytics Officer owns where we are exploring AI. Because in a culture like ours, which is profoundly entrepreneurial, the risk is that everyone starts running and creating things and the mess is complete.

That has functioned very, very well. Today, we have a bit more than a 100 use cases that are moving on the exploration chain from “I have an idea, here’s a prototype, here’s the benefit”, up to industrialisation. And that’s moving pretty fast.

In parallel, we have been also learning what it takes to do AI and agentic the proper way. The marketing at the beginning was “take a big agent, give it all of your context and intention, and you get a result afterwards”. It doesn’t work like that.

We have learned the value of access to clean data, which means we also need to have our own data layer under control, and the value of context: with no context, i.e. no tacit knowledge of the way we do things, agents cannot really be performing. And without proper governance, proper segregation, proper risk management, agents are not suitable for the mission.

Banking is about trust, at the end of the day. In your bank account, you don’t want to have bad things happening because somebody was experimenting with agents, right?

The dependency on access to clean data is a bit underestimated, because you believe the data is there. It’s not always there in the shape you need for a model. If I take the mortgages case, it has taken a lot of additional unexpected effort to fix that part, because the initial logic was “here is the workflow, here are the models, go for it”. And then when you open the hood, you say, “okay, give me the data”, and they say, “wait a moment, where do I get the data?”.

Lucy Ingham:

What does clean data look like in this context?

Daniele Tonella:

That’s a big initiative that we are pushing forward with the so-called data products, because clean data is data you can trust from primary systems, meaning from systems of record where you can trace data lineage, so you know where data is coming from, and where you have enough data to feed the engine.

This is where tacit knowledge comes in, because if you are a back-office employee or if you are an engineer for that matter, there is so much that you know how to do when you use a system that is not documented and is not in the system. How do you give that to an agent?

You see it in engineering: if the model knows more than just the code and the ask, the quality of the result is better – like humans for that matter.

In the engineering space, what we are doing now is, when a coder uses a model, it’s not just interrogating a model. There is a lot of contextual information that gets fed into the model and comes back. What are architectural rules to respect, what are security standards to respect and all of this is not what is necessarily in the brain of the person, but it is in the context around the system, so it’s one notch above.

What is in the brain of the person, I don’t know how to take it out. I’m not sure I want to take it out either, because that’s what I believe is going to make the value of the hybrid human-agentic interface. Things that don’t require a lot of tacit knowledge, go for it. Things that require a mental model, a lot of knowledge of the history, have a human in the loop.

Rules for AI deployment

Lucy Ingham:

How do you ensure that AI is deployed in the right way at an organisational level?

Daniele Tonella:

We have three plus one pillars where we use AI. One is end-user personal productivity – the usual Copilots and everything. There, we are extremely strict on the so-called citizen development, low-code, no-code. Users shall not create agents for themselves alone, because otherwise it’s Excel on steroids.

The second pillar is business AI, which is everything where we use agentic for business purposes to serve clients. That’s in one hyper-scale platform that we have selected, and the technical way of ensuring control there is that we have the traditional separation of duties between the engineers who develop and the engineers who design what has to be delivered.

It’s two different beasts, segregated along the classical software development life cycle. Same rules: you develop, you build, you test, you deploy. That logic is exactly the same.

For the third pillar, AI for engineering, it’s not the same platform, it’s another one. And the plus one is then cybersecurity, which is a bit of a separate animal.

Workload management and tokenomics

Lucy Ingham:

AI adoption is often divided between maximising people’s productivity and eliminating headcount. Is that something you are thinking about?

Daniele Tonella:

Not yet. We are now in the phase where we are starting to create the instruments to track the economic benefits or the risk benefits – which are maybe not monetary – of every single use case.

When you run a proof of concept, you’re interested in seeing how it works and what local benefits you get. But then to scale out, we have to track all of this. That’s what is going to be a bit forced by tokenomics – the AI tokens – because the change in pricing mechanism from paying per seat into paying per token is generating an AI fuel spend that can be significant.

It’s about closing that loop: if the tech spend goes up 20% because of AI, where do I get the benefit, in revenue or in cost?

Lucy Ingham:

Is tokenomics something you’ve had to pay particular attention to?

Daniele Tonella:

Not at the beginning, because the whole market was in exploration mode, and it was heavily subsidised by capital. Now the market is slightly turning into, “you’ve played, now make something out of it because we are going to send you an invoice”. That’s a phenomenal moment to close that loop and see where it is valuable and where it is just fancy.

But also, educating our own people: if I take coders, when they code and the agent is helping them, they can select what model to use – they don’t see the cost implications. Frontier models are way more expensive than normal models, not necessarily for better quality. How do I educate the engineers, to say, “wait a moment, so for this question, go with a low-end model, it’s more than enough and costs 20 times less”?

Employee ownership and adoption strategies

Lucy Ingham:

Have you had to do much work to get your team on board with AI initially?

Daniele Tonella:

There is a hell of a lot of curiosity. ING is a very entrepreneurial bank, very digital-oriented, so the challenge is not the one of infusing energy. The challenge is the one of maintaining focus and ensuring that we scale everything and we don’t waste energy into too many micro-things. That industrialisation effort is the one that we have to bring in.

People are very curious and are very attentive to the training that we are giving, because learning about AI has multiple levels. You can learn how it works under the hood, you can learn how to use it for prompting. But where they’re most interested in is they want to learn how we have designed the way of using that safely inside the bank. There, twice already we have had training about our platform for engineers and we reached the upper limit of the training platform of people that can join, so the interest is gigantic.

Lucy Ingham:

Beyond engineers, are you finding the same is true for other parts of the business?

Daniele Tonella:

Enormously. The bank made a very smart choice at the onset of all of this with a separation of duties.

The Chief Operating Officer owns AI from a business perspective; the Chief Analytics Officer oversees the use cases we decide to do or not to do; Chief Risk Officer owns AI risk; and as the Chief Technology Officer, I own the engine below.

That separation generates attention and traction in all parts of the organisation. So, operations is fiercely pushing for cases where they see value, and the beauty of the mechanism is that those cases are not built with external agencies or with low-code, no-code or whatever, they are built on a tech platform. That is the natural way of doing technology in a digital organisation like a bank.

Lucy Ingham:

Have there been any challenges with that shared-ownership approach?

Daniele Tonella:

Of course. When you manage a socio-technical system at that scale, there are plenty of mostly human challenges. The big dilemma is the one of managing the balance between the need for speed of innovation, acceleration and ‘no questions asked, just do it’, with the need for control.

Control in the sense of reliability, resiliency, risk management, but also survivability of the platform, geopolitical conversations, all of that. And on the other side, also manage the cost angle, because there’s not infinite resources. The discussion – and it’s a very mature one – is along those three: where do we go very fast and break things, where do we go very slow because we need to be safe and how do we cope with money?

Agentic AI’s banking impact

Lucy Ingham:

Are there any areas in banking where you see there ultimately being more or less impact from agentic AI?

Daniele Tonella:

I think every area will profit from it, because essentially every area that is a benefit in any way from digital technologies will benefit from it. I cannot imagine an area in the bank that won’t – maybe physical security, but even there I can imagine AI to contribute in one way or the other. So, I think there is no area that is out of reach.

[A particularly interesting area is] cybersecurity, because the recent announcements on the proficiency of models in the cybersecurity space are going to make the whole industry rethink software quality, dependency on third parties and the value of cleaning up software imperfections in production.

This is gigantic because it’s going to change the view of the commercial side on what is important in tech a lot. It will become more and more important to have clean technology in prod than to have sufficiently good technology.

Building tomorrow’s AI-first bank

Lucy Ingham:

Do you have an end goal for using AI at ING?

Daniele Tonella:

I don’t think there is an end goal, because it’s a technology that enables profound transformation. What shape the transformation is going to exactly have, is still a bit beyond the horizon. Today, we are using it a lot to optimise the processes we’re sitting on. But in revolutionary terms, we are still thinking about this.

We’re discussing what an AI-first bank is, both in terms of how we serve our clients, but also how we function inside the organisation. Maybe the traditional separation of commercial or front office and IT is gone. Maybe the separation is above the platform and below the platform: below the platform are the ones that build the instruments, and above the platform is still the engineers that use the instruments.

We are trying to explore what a bank looks like in a world where AI is there and is under control. It’s a bit like what we did 8 to 10 years ago with agile, where we broke the whole logic on how we do projects and we went fully into agile. Something similar is ahead of us, and we’re trying to think what shape that could have.

Lucy Ingham:

Daniele, it’s been a pleasure, thank you.

Daniele Tonella:

You’re welcome, thank you.