iBanFirst has launched a new Claude-linked agent to speed up treasury for businesses. We sat down with iBanFirst CEO Pierre-Antoine Dusoulier to find out more about how AI is driving its wider growth strategy, with additional commentary from CMO David Remaud.

Artificial intelligence (AI) continues to be a significant driver across all industries, and is already deeply embedded across many aspects of cross-border payments. With the development of generative and agentic AI, the industry has been moving from the initial hype phase into practice to drive efficiency across both internal and customer operations.

New offerings being launched by cross-border payments companies are showing the potential of AI to enhance products for their specific customer types. B2B payments provider iBanFirst is a key example of this, having this week launched iBanFirst Claude MCP for Excel.

The new product allows clients to connect to its API in Excel via Claude. Through the connector, businesses can use Claude to do a number of things, including retrieving live balances from their iBanFirst account, tracking historical payments and FX trades and generating entire tables of data in seconds for reconciliation purposes.

The development is interesting because it’s one of the first instances of a cross-border payments business using the Model Context Protocol (MCP) – Anthropic’s open standard for AI models introduced in 2024 – specifically to enhance workflows for small and medium multinationals (SMMs), which is iBanFirst’s term referring to internationally exposed SMEs and mid-sized companies. iBanFirst has recognised the potential of the technology to answer a clear business need, in this case supporting more efficient operations for businesses that often don’t have the scale to do treasury effectively.

We sat down with iBanFirst CEO Pierre-Antoine Dusoulier to find out more about the company’s growth strategy and how it is using AI to enhance its offering for SMMs, with additional commentary from CMO David Remaud.

iBanFirst’s growth and customer mix

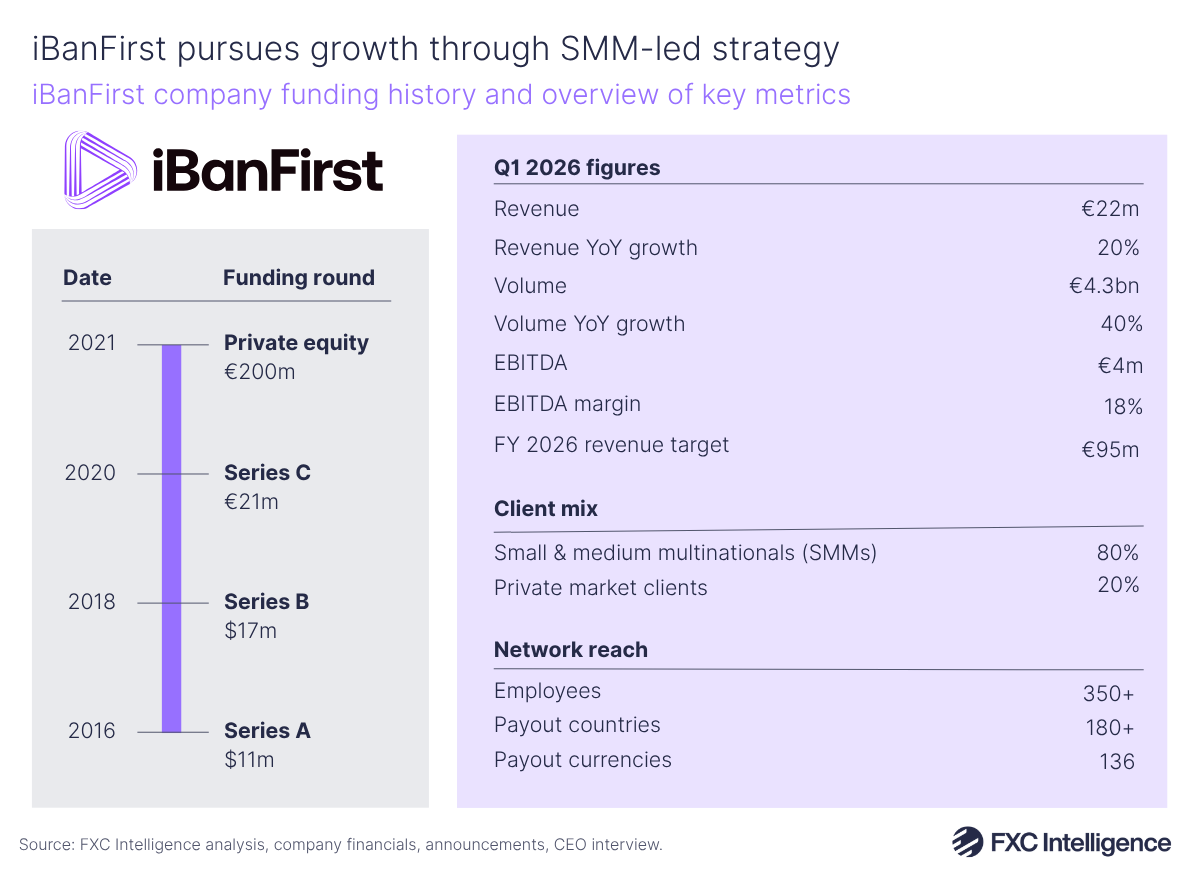

Founded in 2016, iBanFirst has grown to become a significant provider of cross-border payments services to businesses in Europe. Through its platform, businesses can open multicurrency accounts that allow them to hold 25 currencies and execute payments in 136 currencies across more than 180 countries.

For Dusoulier, iBanFirst’s European focus has led to its differentiation to other UK and US-led players in the B2B payments space. The company’s key delivery is its IBAN accounts, which can be tailored depending on the clients’ location and requirements.

“The vision has always been continental Europe,” he says. “We have a lot of clients that are using us not only for cross-border, but also for euro-to-euro payments for example. Clients use our accounts to receive money, not only to do payments but to receive dollars or yen or whatever currencies [they need] on the account we provide to them.”

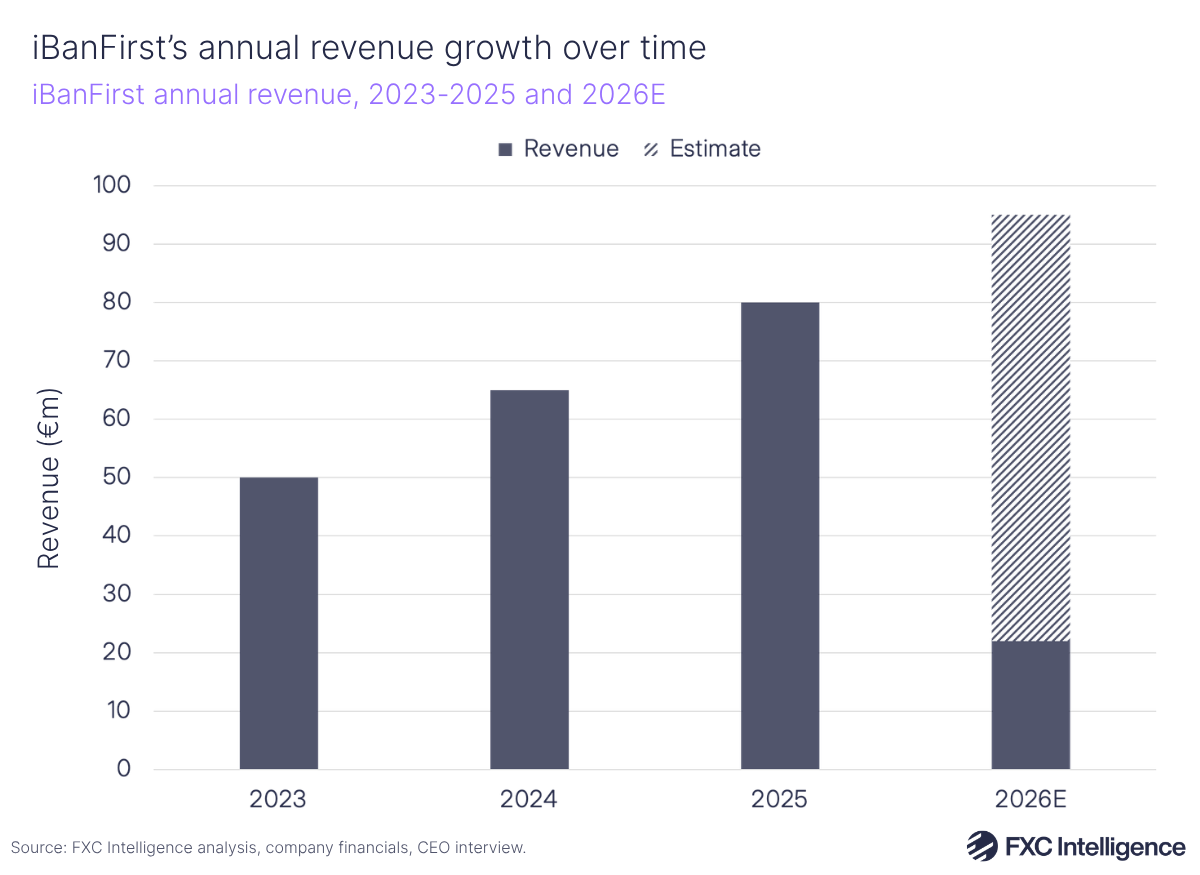

iBanFirst saw revenues grow by 20% to €22m in Q1 2026 on the back of 40% volume growth to €4.3bn, driving an EBITDA of €4m. Having seen €80m in revenue in 2025, the company is targeting €95m annual revenue in 2026, up 19% YoY on its 2025 revenue figure.

Dusoulier and Remaud maintain that SMMs are iBanFirst’s core customer focus. The company has accrued 10,000 customers, but Remaud says that it sees an opportunity to grow and serve one million SMMs in continental Europe.

Having said this, iBanFirst is also pursuing private clients, which includes high-net-worth individuals, investment clients and family offices, with this taking up around 20% of its business versus 80% for corporates. The company recently opened a new Luxembourg office and has enabled Luxembourg IBANs alongside its wider IBAN offering to support this emerging client segment.

Here, Remaud notes, iBanFirst’s platform and ability to open accounts overnight, as well as its strong foothold in continental Europe and the UK, is continuing to drive the business’s growth.

What problem is iBanFirst’s new AI product solving for businesses?

As SMMs expand payments to other countries, they face complexities around currency conversion, complying with local regulations and fragmented banking infrastructure.

iBanFirst already offers services to enable easier reconciliation, allowing businesses to centralise data across their currencies, accounts and transaction history. However, one issue it continued to see SMMs face was that many of the tools that are in the market are built for complexity and priced for large enterprises.

As a result, many businesses are still significantly focused on using Excel for treasury operations, leading to laborious processes across exporting, pasting and reformatting data. “Probably 90% of our clients are following their treasury on Excel,” says Dusoulier. “They are too small to buy or implement a treasury management system (TMS).”

iBanFirst saw the gap to use Claude and MCP to significantly simplify the process by building an agentic treasurer for SMMs, allowing CFOs to quickly generate the data they need by typing a question into their Excel spreadsheet, without needing any platform exports, data cleanup or additional software knowledge.

“We have many connectors to connect enterprise resource planning (ERP), accounting software and so on, but at the end of the day, this is complex,” says Remaud. “Now, with Excel and Claude, we really match the needs of the SMMs, simplifying their process and integrating their existing process.

“You just take your cash management, treasury [and] Excel, and thanks to Claude and iBanFirst MCP, you turn it into a treasurer.”

The importance of human validation in AI payments

A key part of the conversation around any new AI payments technology is the extent to which they have human oversight. In B2B payments, the scale and sensitivity of payments makes human validation a particular aspect that many in the space will care about.

Remaud says that by design, iBanFirst has been focused on improving automation while at the same time offering finance teams at different levels multiple signatures, or verification checks, to integrate the flow.

An example of this is iBanPay, the company’s AI-powered invoice assistant launched in October 2025. Clients send invoices to a dedicated email address and the tool scans their account and sets up payment drafts automatically, before asking the sender to review and verify the payment.

The assistant can create dozens or even hundreds of drafts of payments, with the CFO setting the rules or validating which ones will be sent themselves. Remaud says that the automation actually results in less mistakes being made than if they were to type information manually.

In the same way, iBanFirst’s new MCP offering ensures that information can be checked at the payment stage.

“It’s all about the architecture of the API,” says Remaud. “At the end of the day, we are the payment provider, so we don’t want AI to go directly into that moat of payments. The architecture splits the two, so whenever your information goes into Excel, or you trigger and generate payment orders from Excel, it goes into a specific part and then it goes into the human validations.

“The true differentiation we have by design is that we are splitting treasury, data and automation from the core of the payment that needs to be highly secured and controlled.”

iBanFirst’s move into AI provides a clear example of a practical, external-facing product that captures the needs of its target market. While a significant portion of the cross-border payments industry’s focus has been on the potential for AI to deliver agentic payments – particularly in ecommerce – we can expect to see more solutions that help businesses scale more efficiently as B2B players tap into a growing opportunity worldwide.