Fleetcor has announced that Corpay, the brand name of its Corporate Payments division, will soon become the name of the whole company. We spoke to Corpay Group President Mark Frey about the rebrand, the group’s impressive FY 23 results and cross-border strategy.

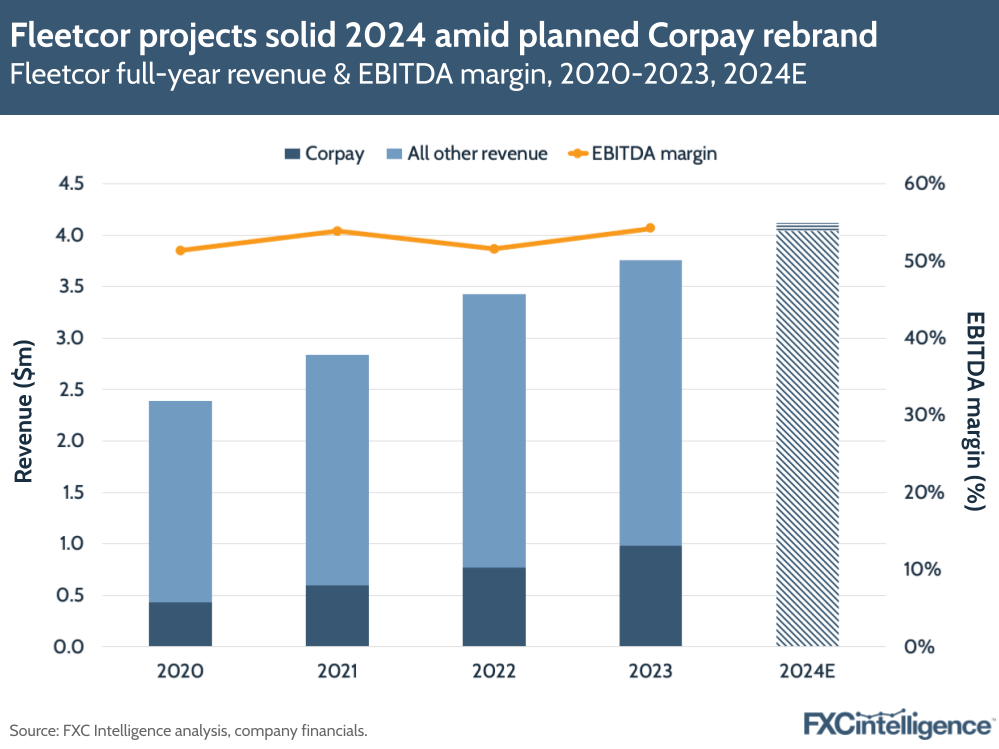

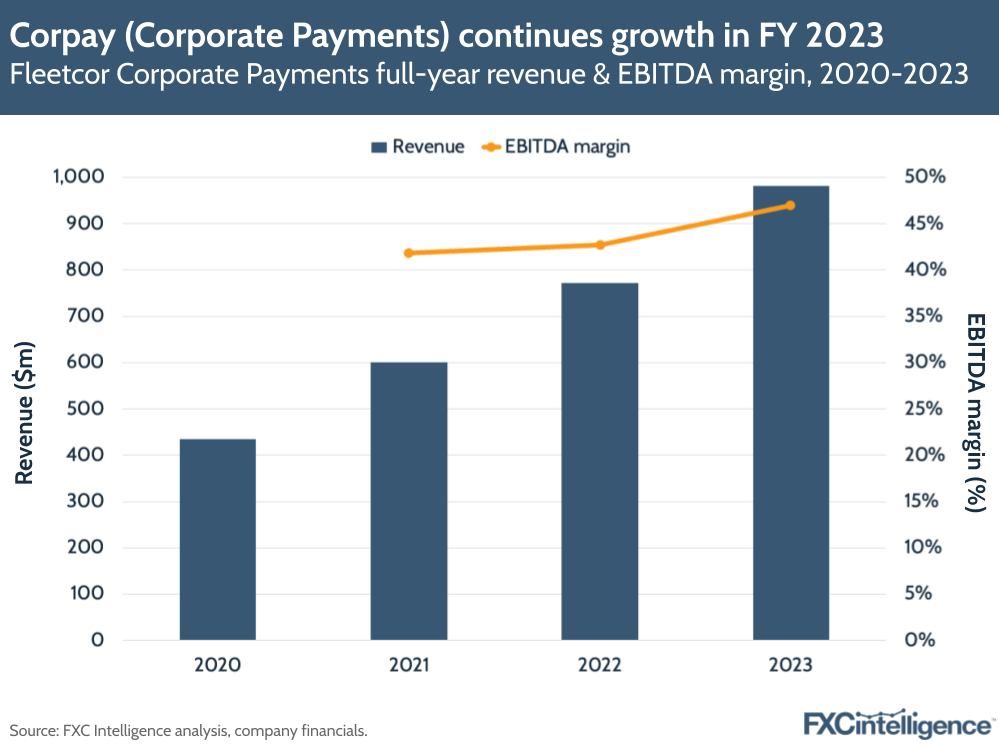

Fleetcor’s Corporate Payments division, also known as Corpay, has had a strong Q4 23 and FY 23. While in Q4 the division saw 15% YoY growth, or 20% without its channel partner business, for FY 23 the segment climbed 27.5% to $981m.

This represented significantly stronger growth than Fleetcor as a whole, which saw FY revenues increase 10% to $3.7bn, although the company did beat analyst forecasts, prompting a share price rise.

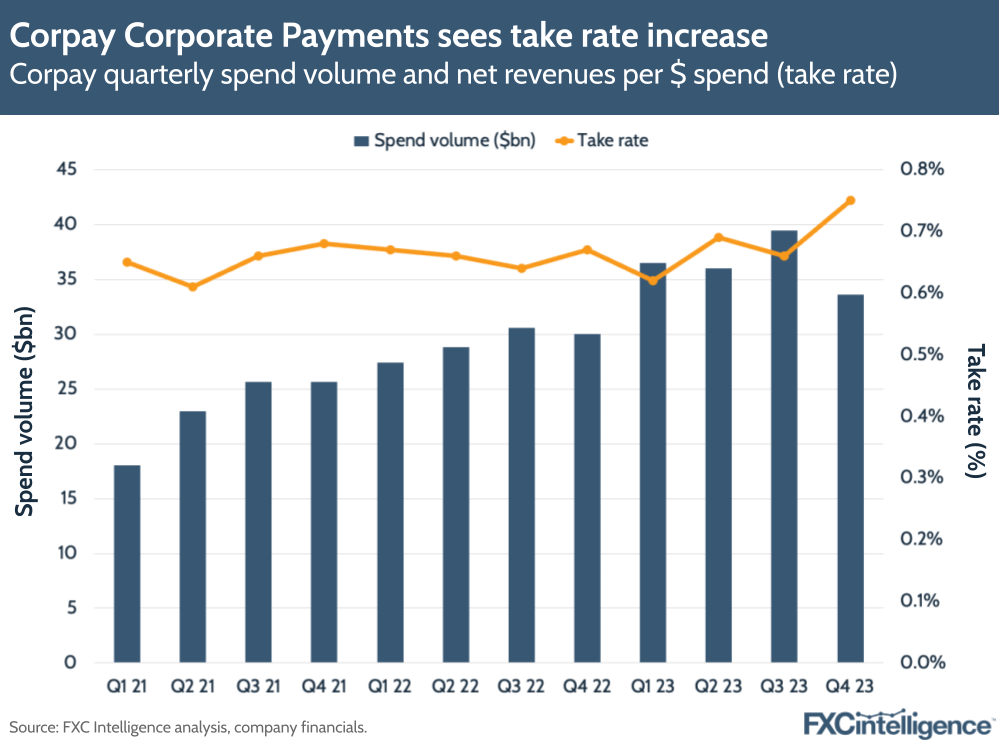

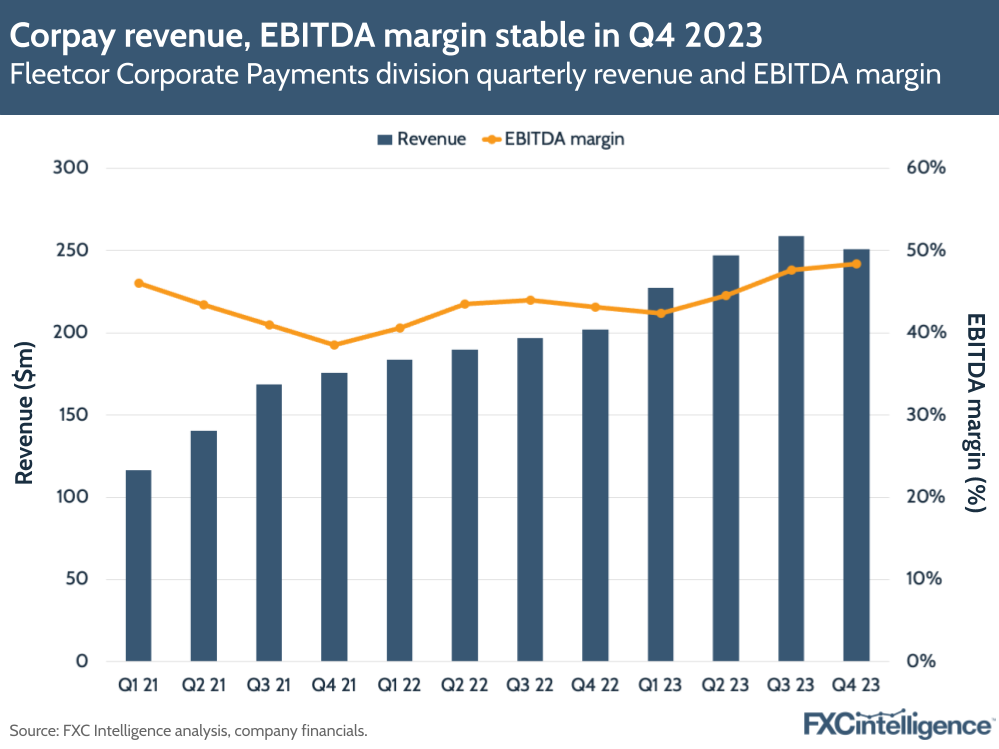

Corporate Payments also saw a 51% YoY increase in operating income to $101m in Q4 23 and 40% growth to $382m for the full year, while its take rate also increased in Q4.

Key to the division’s strong growth was strong sales, which were up over 40% in Q4 and up 50% for FY 23, with Corporate Payments selling to over 100,000 new B2B clients in 2023. The company has also broadened its mid-market offering, with the launch of platform solution Corpay Complete.

Notably, while Fleetcor had been considering spinning off the Corporate Payments division to become the standalone Corpay, it has now instead opted to take a very different tactic. The company announced that it is now planning to rebrand the entire company to Corpay, which is scheduled to occur in March.

With such a significant move in mind, we caught up with Corporate Payments Group President Mark Frey to find out how the division will sit amid the rebrand, what is driving its strong growth and how he sees its strategy going forward.

Fleetcor’s Corpay rebrand

Daniel Webber:

Let’s start with the news that your parent company Fleetcor has decided that the whole organisation should be named Corpay, not just the part you lead. What is driving that rebranding?

Mark Frey:

The driving force behind the idea is really the re-imagined company on a go-forward basis. We really are a business payments or a corporate payments company and that is very much what we’ve become.

Our key segments include the cross-border business as well as our domestic payables business, which have long been branded as Corporate Payments, and now we’ve moved to the official go-to-market and Corpay. But Fleetcor as a whole has been moving further down the path of being a business payments company as opposed to that traditional view of being a fleet-focused organisation.

This is just a recognition of the evolution of the business, of the future direction of the business, that it will increasingly be a Corporate Payments-driven business, even in the vehicle mobility sector and certainly in the lodging sector. If we think across our three key market segments in Corporate Payments, lodging and then vehicle mobility payments, they’re all ultimately Corporate Payments businesses, just with a different flavour of the payment that we’re making for different segments of customer.

The rebrand is a recognition of that evolution that has been underway for some time, and also a nod to the future in terms of the continued focus on the corporate payment side of the business and business payments in general.

Daniel Webber:

Is that going to change your role in the business?

Mark Frey:

No change. I’m going to continue to lead the cross-border payments segment. And no change to our overall executive structure.

We’ve done a little bit of re-segmentation ultimately in combining the fuel business in Brazil into one vehicle mobility business and there’s been a little bit of movement there. But we’ve basically adjusted that business to be run by two Group Presidents on a regional basis, one for the Americas and one for Europe and APAC.

Those gentlemen all obviously have a longstanding pedigree with the organisation and are the right individuals to lead that business respectively going forward. So I have a lot of confidence about the leadership of that group.

Drivers of Corporate Payments growth

Daniel Webber:

The Corporate Payments business saw 27.5% revenue growth in FY 2023, which is very good, particularly given that over 20% for three years in a row qualifies as a high-growth business. What is driving that and do you expect it to continue?

Mark Frey:

We’re very excited about what the future of the Corporate Payments business looks like, both in terms of the domestic payables business as well as the cross-border business. We’re looking at both growing 20+% for the foreseeable future.

Not only is the organic growth and same-store sales very attractive in terms of the businesses, but the rate at which we sell is super attractive in terms of how we acquire net-new business and net-new customers; how those customers ultimately transition and are retained within the business over the long haul. That’s certainly an exciting aspect of the business.

We’ve got some new key products coming out in the domestic payables business that we’re super excited about and a cross-sell opportunity with the rest of the Corpay enterprise in terms of the vehicle mobility segment and lodging.

Then in cross-border, new products again. New geographies, with geographic expansion that allows us to take our value proposition to new underserved markets, particularly in Western Europe where we think we compete really well and we can continue that above trend overall growth that we’ve achieved in EMEA over the past number of years.

We’re super excited about the organic growth story with the new products and the new markets and new segments that we’re chasing. But I also think we have a very constructive view of what we think the future of the M&A pipeline looks like in Corporate Payments.

Corpay’s M&A prospects

Daniel Webber:

Let’s talk about your M&A pipeline. What’s the focus there?

Mark Frey:

We will be having a heavy focus on Corporate Payments in terms of M&A opportunities on a go-forward basis. There’s a very well diversified and attractive pipeline of transactions that we’re looking at. And I’m super excited about what the future looks like.

Just playing out our preexisting strategy, which is almost a roll-up strategy, especially in the cross-border business. We can take these other entities, roll them into the broader corporate organisation, accelerate growth and have some cost synergy and operational leverage that we can gain out of the transactions as well.

It’s a super exciting time for us. We’ve got a healthy balance sheet, with capital to deploy and lots of targets that we want to chase after.

Daniel Webber:

What types of businesses are you looking at? What would move the needle for you from an acquisition standpoint?

Mark Frey:

We look at it a few different ways. We’re always looking for opportunities where we can acquire an organisation with significant customers. Ultimately that will be accreted to the bottom line and we can accelerate growth in sales by taking our enhanced product and capability and putting it in the hands of capable salespeople that can sell more to their existing customer segments.

There are lots of opportunities that exist in the cross-border payments space of firms that have a global footprint and that look a lot like us, but are smaller or perhaps less efficient, which we can put on our platform and accelerate the growth they’re in and make more profitable. There’s certainly those types of deals. We’ve done a few of those transactions in the past, such as Afex and Global Reach.

But we also look at capability plays as well, whether it’s a piece of technology licensing or a jurisdiction that is super attractive that we can bolt onto our core platform and grow it through our distribution network very well.

From an overall corporate finance perspective, there are a few things that stand out about our growth model in cross-border. We’re very unique in the marketplace. We sell very efficiently in terms of new business acquisition and acquiring growth.

We do that very well in the marketplace. So our ability to take an existing capability and sell it very aggressively across our customer segments is something that we think very highly of and we’ve been able to do with a long track record. But we also think in terms of our ability to accelerate earnings growth because of the efficiency and the operational leverage that we have in our platform as well.

It’s really the perfect time for us to continue to look at opportunities to roll up the market and consolidate the space a little bit. But we’re also looking for those capability things that we can bolt onto the existing organisation and chase new segments, serve new categories of customers, fill in the cross-border payment space, but a new segmentation ultimately.

There are attractive opportunities that we see with technology in particular that we can bolt on to our existing tech stack. And that’s absolutely something that we look at in the future as well.

Growing market share

Daniel Webber:

What allows you to grow faster than the rate of the market? Where’s that share coming from?

Mark Frey:

We’re taking share from both ends of the spectrum. Certainly I think we compete really well against the smaller fintech organisations that have good capability and good technology but perhaps aren’t as mature in terms of the strength of balance sheet and financial performance, don’t have the global presence or the breadth of capability that we have across a number of different customer segments.

We compete very well against those from a capability perspective, but we’re also still a very agile, nimble tech-forward organisation. We develop new products and deploy very quickly. We can beat many of the smaller fintechs at their own game based on our size and strengthen our ability to move fast.

When we compare that to the financial institutions, either tier one global money centre banks or tier two financial institutions, again we have those fintech characteristics, but with the size and strength of being a Fortune 1000 S&P 500 company that allows us to compete very well against banks as well.

Now in some cases those banks are our partners or clients as well. They’re coming to us looking for liquidity and payout capability in certain emerging markets around the world where we have built a network and footprint that is unrivalled, I think, in the marketplace. We do well in that space as well.

We are very much like a financial institution, in that we have a global footprint, we have the balance sheet and the financial strength. We are building a brand that I think is more recognised in the marketplace, but we’ve been able to assemble a network by leveraging the best of our banking partners around the world rather than just trying to do it all on our own.

At the same time, we compete super well against those smaller fintechs that don’t have that strength and balance sheet, that can’t run as fast as we do because of the resources that we have and the ability to invest in the business given the profitability of the franchise.

What we’re really trying to do is charge right up the middle between those two ends of the spectrum to be something a little bit unique.

Very much like a bank in terms of size and capability and financial strength, but behave more like a fintech in terms of our agility, our ability to roll out new products and develop new features for our customers. And in so doing, we hope we can take share from both ends of that spectrum.

The impact of Corporate Payments’ scale

Daniel Webber:

There are very few players in the market that have your scale. Where does that scale really differentiate you?

Mark Frey:

It drives down the average cost of transactions. From the expense base side of the business, it allows for a great deal more efficiency.

Part of it’s the strategy that we’ve employed as well. We have a single tech stack and one operational platform across the entirety of the business. When we’ve done acquisitions, we’ve taken great care to very quickly move all of those customers in the entirety of that business onto the operational tech stack and platform of Corpay going forward.

That’s given us operational efficiencies that lowers our cost to serve and gives us one common operational platform, which reduces payment errors as well as reducing exception handling and challenges that you would typically have with a matrix of different types of systems, which many financial institutions struggle with.

We also have very young systems that we’ve been able to effectively develop and augment over the past decade, which put us in a place where we can compete very well against the large banks as well, as a result of that.

That operational scale really helps our efficiency in terms of how we process payments. It helps in terms of lowering the average cost to serve for each individual transaction, but it also allows us to go after larger customers and serve large financial institutions that are aggregating business and bringing it to us and expanding our distribution.

Targeting the mid-size market

Daniel Webber:

Your new product Corpay Complete is tailored to the mid-size market. What are you hoping to achieve with this product?

Mark Frey:

This is a product that we’re really focusing on the US domestic market, where we believe that there is a very underserved mid-market opportunity with corporates that are looking to consolidate workflow with respect to processing payments and really provide full AP automation, ultimately from the start to end of the overall payment process.

It’s a technology solution that will allow mid-size companies – which are always starved of resources – to scale their back office to make them more efficient in terms of their finance department and have better relationships with their vendors, ultimately by paying them faster with greater efficiency and less cost.

It’s that workflow solution that we really think is perfectly targeted towards that mid-market, where the customers that we hear from are always looking for a solution that is easy to enable, easy to integrate with and can help automate workflows, irrespective of the ERP or the accounting package that they might be running.

Daniel Webber:

What’s the importance of the cross-border piece versus the domestic piece for this type of solution?

Mark Frey:

Those businesses are fully integrated. When that US domestic firm comes to us and we’re processing their domestic AP and they have some component of their international business as well, that flows through to the cross-border side of the business and we process those payments as well and vice versa. There is a really tight integration between those two business units and we can serve each other’s customers ultimately very effectively.

Digging into Corporate Payments’ numbers

Daniel Webber:

Take rate went up in the last quarter to quite healthy levels. What drove that and do you expect it to stay there?

Mark Frey:

It’s something that we’re always focused on as the business is trying to be more efficient, trying to show more value to clients so that we can extract price and economic gains. We do think it’s sustainable: it’s something that we think we can continue to do as we have over a long track record of time.

Then it comes from the operational leverage as well. We will drop that revenue to the bottom line with increasing efficiency as the business continues to scale up.

Daniel Webber:

Is there any colour you can give on the breakout of cross-border payments within the Corporate Payments segment?

Mark Frey:

I can share just a high-level metric that we will be a circa $700m business in cross-border payments in 2024.

The take rate between domestic and cross-border is very, very similar. The revenue allocation and/or volume allocation follows that.

When we joined the Fleetcor group, soon to be Corpay, in 2017, we were a nice tuck-in acquisition that added some capability to Fleetcor. We’ve obviously become a more important part of the business.

Corporate Payments in general is a huge part of the business and with the trend growth rate that we see in Corporate Payments, it’s obviously becoming a bigger part of the franchise going forward.

That is represented by the evolution of the business overall more towards business payments and Corporate Payments in general. And that’s reflected in the brand change as well.

Daniel Webber:

Mark, thank you.

Mark Frey:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.