As we enter 2024, how much has dedollarisation occurred in cross-border payments, and how much is the yuan seeing a gain from the dollar?

Over the past few years, growing numbers of countries have begun to look, or at least consider looking, beyond the dollar for their global currency needs.

Geopolitical events such as the Russia-Ukraine war, and the resulting embargo of Russia, has been a factor, but so too have a wide range of other elements. The changing and increasingly challenging macroeconomic environment has been key, as has growing economic strength in emerging markets who are now looking to improve their own currency sovereignty.

Dedollarisation, the practice of switching away from the US dollar as a reserve currency, medium of exchange or unit of account, is a highly complex topic with myriad driving factors that vary notably from state to state. However, one of the strongest narratives in this space has been the rise of China’s currency, the yuan, in its place.

This is in part the result of the rise of China as an economic challenger to the US, exacerbated by the US Trump administration’s trade war rhetoric, as well as, more recently, by Russia’s shift to China-focused trade in response to Western embargos. The addition of more players to the BRICS bloc has also strengthened China’s perceived position.

However, as we move into 2024, is this perceived dedollarisation and increased favouring of the yuan playing out in the data? We look at some of the latest available datasets to find out.

Dedollarisation in foreign reserves: 2024 to 2034

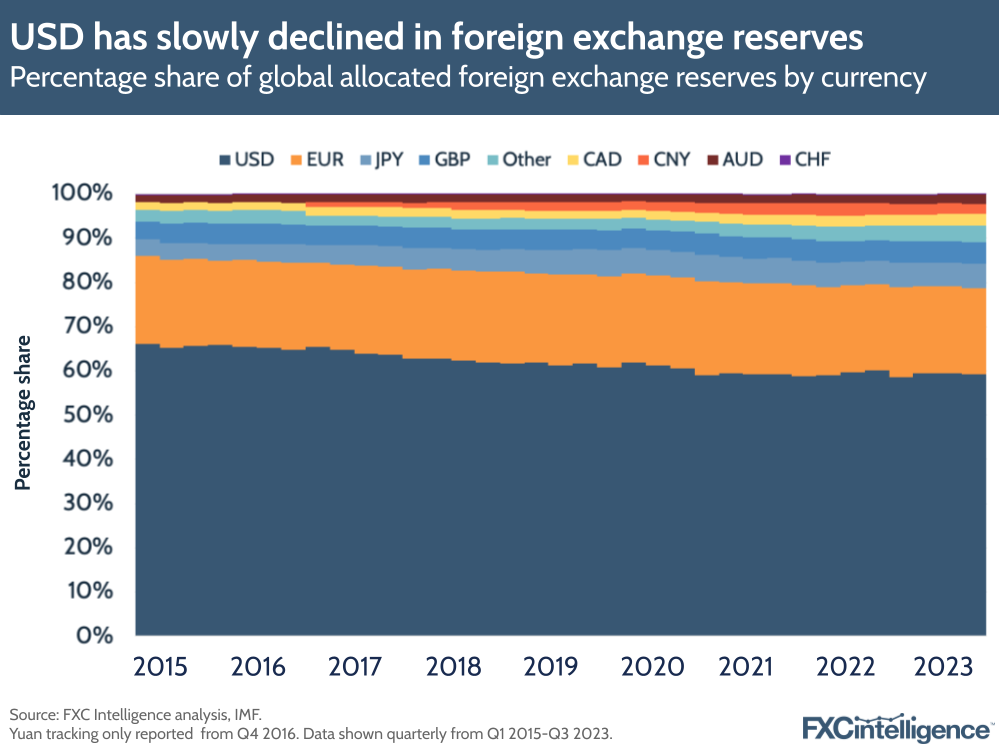

Looking specifically at foreign exchange reserves, there is evidence for a move away from the US dollar.

According to data from the International Monetary Fund (IMF), between Q1 2015 and Q3 2023, the US dollar’s share of global allocated foreign exchange reserves has dropped from 66.0% to 59.2%. Over the same period, the euro has declined only very slightly, seeing its share reduce from 20% to 19.6%.

However, the yuan (CNY) has increased during this period. While it did not appear in IMF foreign exchange reserves data at all in Q1 2015, its first appearance in Q4 2016 placed it at 1.1%, and it has since grown to reach 2.4% in Q3 2023.

Notably, the Canadian and Australian dollars have also seen their shares increase over the same timescale, as has the Japanese yen and British pound. The AUD grew from 1.6% to 2.0% between Q1 2015 and Q3 2023, while the CAD increased from 1.7% to 2.5%, the GBP from 3.8% to 5% and the JPY increased from 3.8% to 5.5% over the same period. At present, at least, this suggests that from a foreign exchange reserves perspective, the move is not simply from USD to CNY, but to a broader range of currencies, while there is some evidence to suggest that gold is taking an increased share of reserves too.

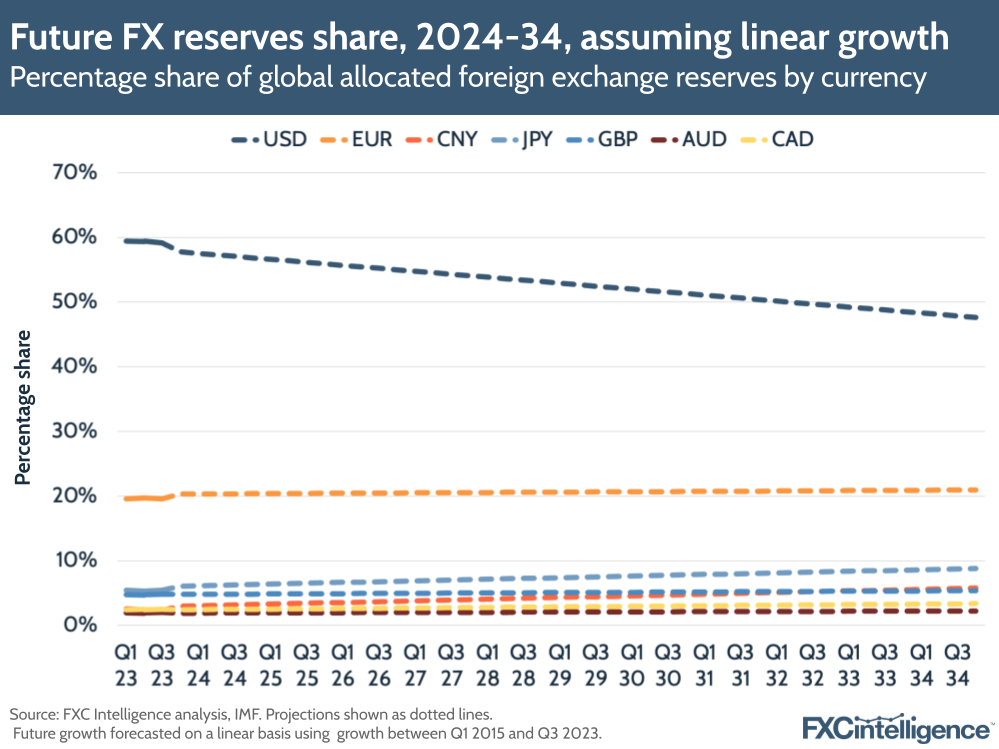

To get some sense of how this may continue to play out, we can look at future growth rates forecast on a linear basis using past growth between Q1 2015 and Q3 2023. While this fails to take into account any potential economic shocks, geopolitical developments or other reshaping factors that may occur over the next decade, making it only a rough measure of future potential trends, it does suggest that a move away from the dollar is set to be a very slow process occurring over decades.

While on this basis the USD is set to lose share over the next decade, dropping below 50% of global currency reserves by the end of 2032, it is set to remain the largest currency for foreign exchange reserves for many decades to come. The euro, meanwhile, is set to remain relatively stable, while the yen will move towards the 10% mark by the end of 2034.

The yuan, meanwhile, is set to see continued growth, but while it is on course to pass GBP in 2032 at current rates, it would only reach 6% by the end of 2034, up from 3% at the end of 2024.

The trend, then, is for dedollarisation, but not exclusively towards the yuan, and instead towards a broader range of global currencies that provide greater hedging from different geopolitical shocks.

Payments in dollar and yuan: Insights from Swift

While foreign reserves show some evidence for dedollarisation, is the same true for cross-border payments?

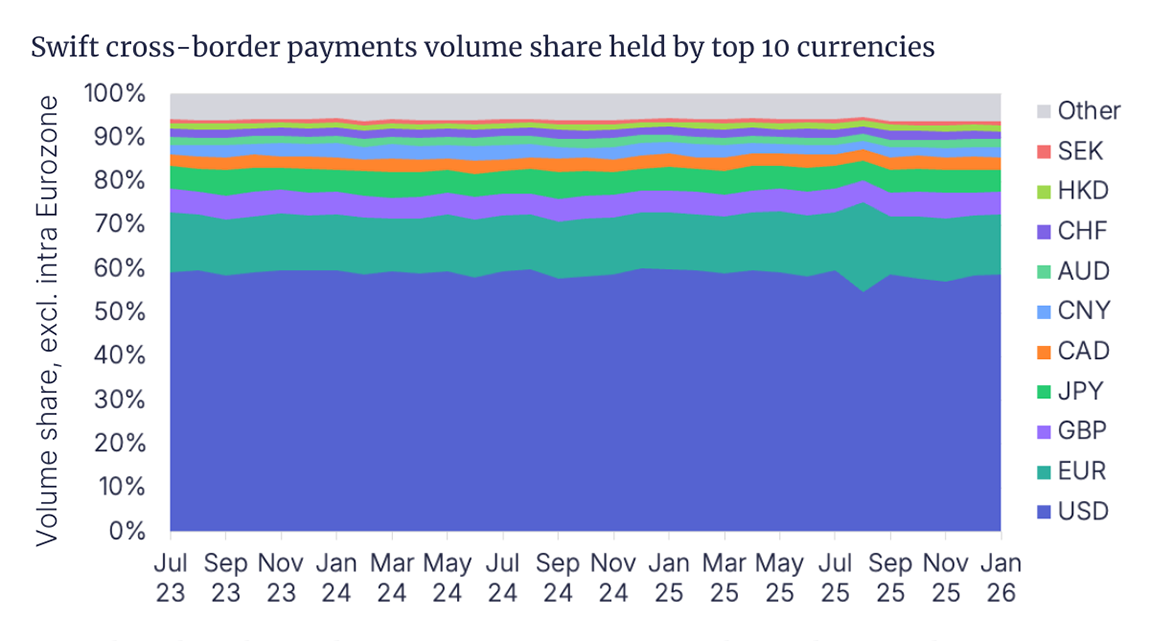

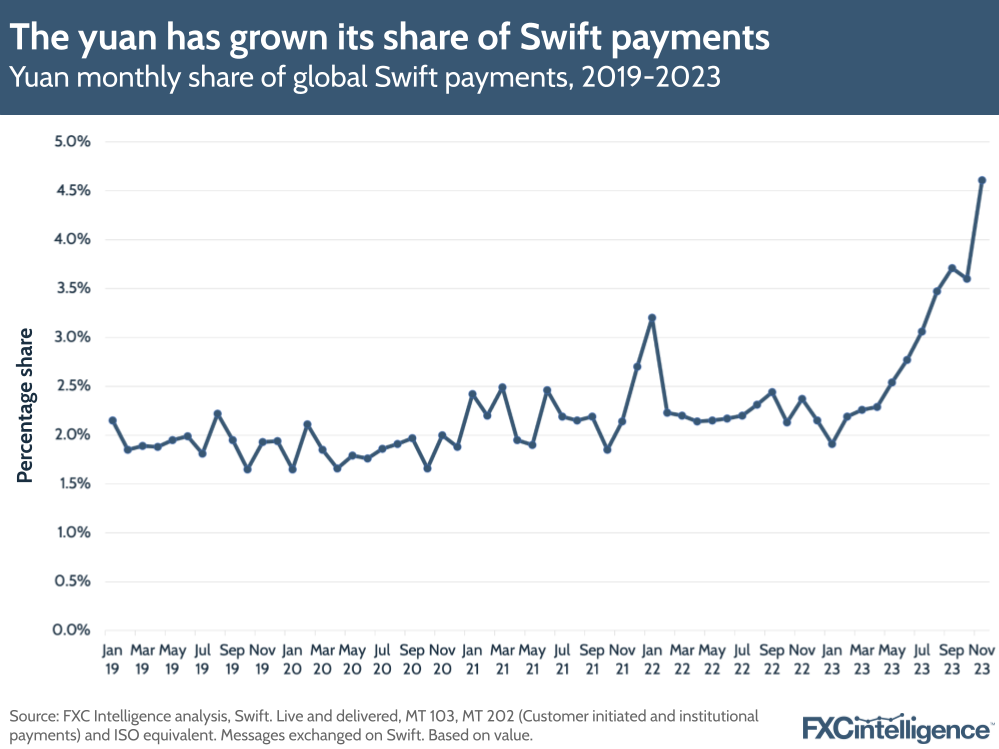

Looking at data from Swift, there has been a clear rise in the yuan’s share of global customer-initiated and institutional Swift payments over the past few years. While CNY accounted for 2.2% of global Swift payments in January 2019, this has risen to 4.6% in November 2023 – a faster rise than the yuan’s share of foreign exchange reserves and one that has been particularly marked in 2023.

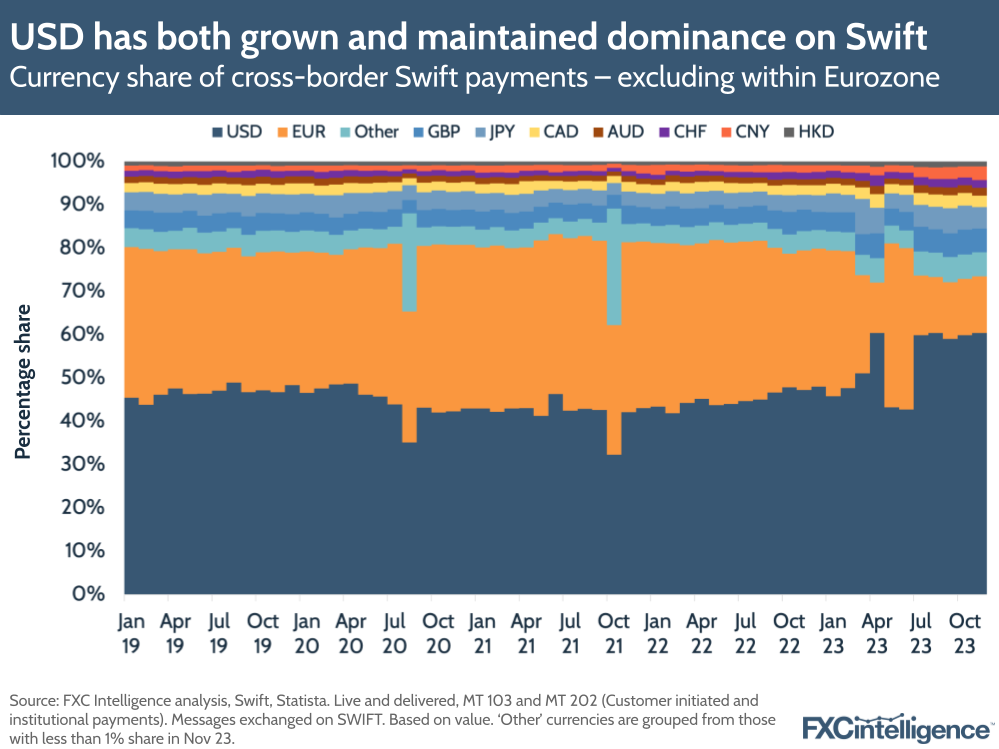

However, there has not been a move away from the US dollar over the same period. Instead, this has also seen growth, with the USD rising from 45% of all non-eurozone cross-border Swift payments in January 2019 to 60% in November 2023.

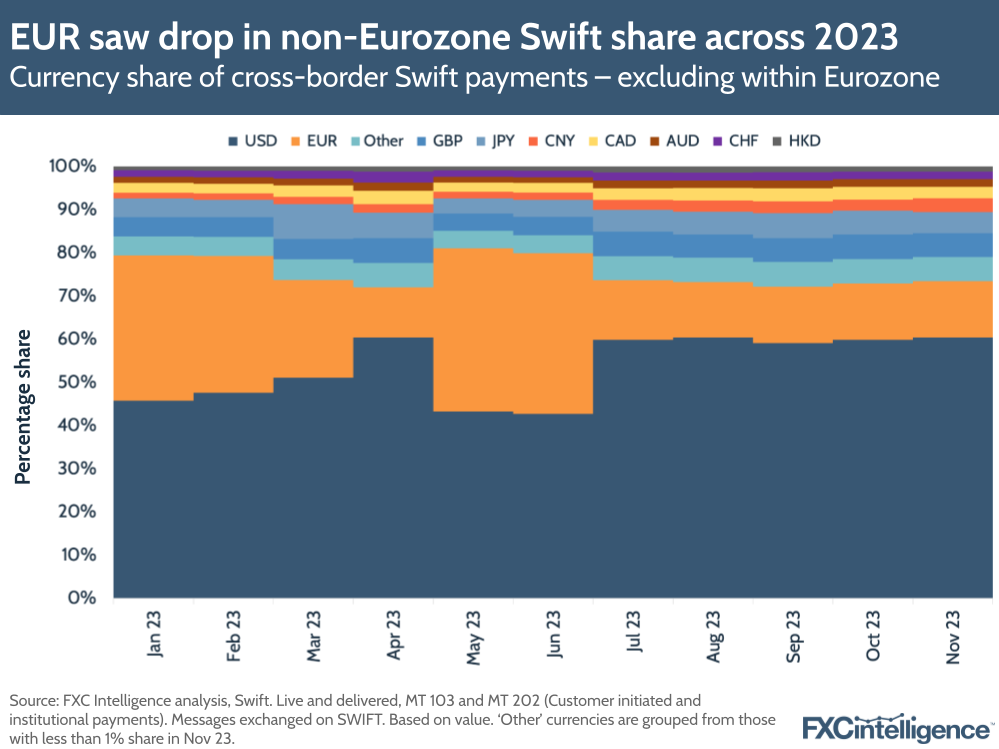

Much of the biggest shifts in currency have happened across 2023, and may be a result of the increasing strength in the US dollar seen towards the end of 2022. Notably, while both the US dollar and yuan gained share during this period, along with the yen and pound, the euro lost the most share during 2023.

Currencies in Chinese trade

Meanwhile, for trade to and from China, there has been a sharp uptick in the use of the yuan for non-banking cross-border payments both into and originating from the country. Here, the US dollar is the primary source of payments share and has been losing out at around the same rate that the yuan has been gaining.

In March 2023, the yuan passed the dollar for payments out of China for the first time and passed 50% of all payments in June 2023. Payments into China have been a little slower, but here the yuan passed the dollar in May 2023.

This suggests that the yuan-specific dedollarisation narrative does meaningfully apply to China, even if it doesn’t hold out so robustly on a global scale.

The prospects for dedollarisation in 2024

Based on current trends, the world is slowly drifting away from its significant reliance on the US dollar as the global second currency, however, attempts to characterise this as an acute and rapid occurrence significantly overstate the situation, as do stories of this being a strong shift to a single other currency.

Global foreign exchange reserves are seeing declining holdings in US dollars, however this will require generational timescales to reach significant levels of change without a major geopolitical event. Meanwhile, cross-border payments in dollars remain strong, and have particularly seen sharp gains in 2023 – although whether this trend continues into 2024 remains to be seen.

Crucially, we are not seeing dedollarisation occur in a manner where large amounts of the world are simply moving from dollars to one other currency. Instead, countries are diversifying their holdings across a broader range of currencies and, if this holds, we would expect to see greater numbers of currencies pass the 1% mark in the future.

Dedollarisation is often characterised as a shift from one financial superpower to another, however the evidence instead leans towards a nuanced shift to a more decentralised range of financial powers.

As geopolitical tensions continue into 2024 and beyond, and are compounded by factors such as climate change and migration, we can expect to see these trends develop, but how much they will remain on current trendlines is unclear. With so much uncertainty and potential for change, we can expect the subject of dedollarisation to continue to evolve over the next few years.