After rebranding from Fleetcor to Corpay, formerly the name of its Corporate Payments division, Corpay has seen its Q1 2024 growth driven by Corporate Payments’ performance. We learn more from Corpay Cross-Border Solutions Group President Mark Frey.

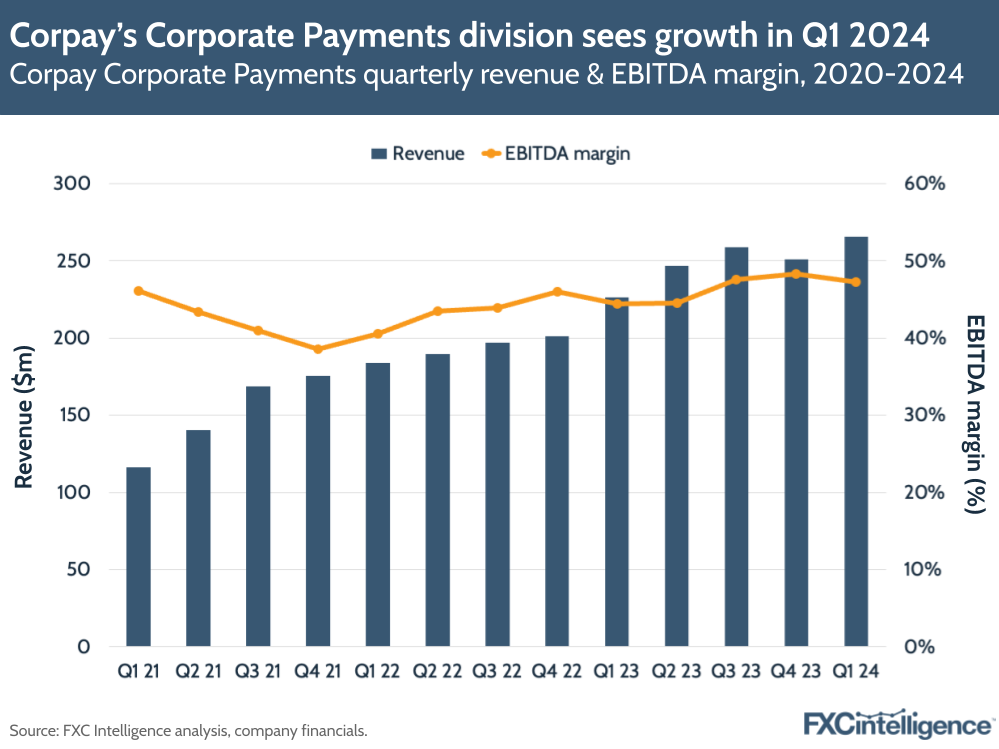

Corpay, formerly known as Fleetcor, has announced its Q1 2024 results, following a rebrand that saw it take the name of what is now its Corporate Payments division. And while its top-line results saw Corpay’s revenues grow 4% YoY to $935.3m, this was primarily driven by the cross-border focused Corporate Payments segment.

Corporate Payments significantly outperformed other divisions, seeing 17% YoY growth to $265.4m, while EBITDA increased 24.6% to $125.5m, to produce an EBITDA margin of 47%. The segment also saw cross-border revenue grow by 18%, while sales increased by 25%.

Corpay also announced the acquisition of accounts-payable-focused corporate payments company Paymerang – a deal that is set to close in Q2 and yield growth from 2025.

To find out more about Corporate Payments’ growth, I caught up with Mark Frey, Group President of Corpay Cross-Border.

Corporate Payments and Corpay’s rebranding from Fleetcor

Daniel Webber:

Let’s start with the branding. The strength of Corporate Payments, formerly Corpay, led it to become the central brand of a very large financial services public company in Corpay, formerly Fleetcor. How are you thinking about that?

Mark Frey:

The rebranding of the broader enterprise is not just a rebrand and a marketing exercise. It is a recognition of the evolution of the franchise and the business moving away from that legacy heritage of the Fleet and Fuel brand in isolation.

Of course, that’s still a big part of the business, but even that vehicle mobility business has really changed over the last few years and has morphed into both a consumer brand and also more of a business mobility payments business rather than just Fleet and Fuel, ultimately. Between that, the Lodging sector, which is very much a corporate payments brand, is built around a specific customer segment.

Really, what we’ve begun to do is assemble assets and organise them in a way to go after different types of corporate spend with very specific verticalized solutions. That’s what Corpay is at this stage. We’re a corporate payments company focused on a handful of very strategically chosen segments. And really focusing all of our resources on trying to go as deep into those segments as we possibly can rather than trying to go wider as a broader market play.

Daniel Webber:

How do you think the rebrand will help the overall cross-border and Corporate Payments part of the business?

Mark Frey:

It’s certainly a big win for us in the cross-border business. We no longer have to explain that our parent company is a Fortune 1000, S&P 500, but it’s a different name. We can simply say that we are, and we are part of that heritage. It’s a simpler story to tell to the market and to our customers and partners, no question.

But it also makes it a simpler brand experience and reduces some of the brand confusion around some of the cross-sell efforts that we have within the various Corpay lines as well. It’s a simpler story, ultimately. We’re seeing initial success with that already of being able to act as one company, present ourselves as one company. It makes for a much smoother transaction experience with that cross-selling.

Drivers of Corporate Payments’ Q1 2024 growth

Daniel Webber:

Quarter one was really good for your division. Talk us through what was driving that.

Mark Frey:

17% year-on-year growth and that’s on a print basis. That’s facing a little bit of a headwind in terms of US dollar strength and some interest rate headwinds as well in certain markets. But very positive: sales accelerating much faster than that, continuing to sell and acquire many customers at a very aggressive and impressive pace given the size of the enterprise at this stage.

One of the things that was super attractive about the quarter is that we saw relatively even balanced growth across all geos, all market segments, where we’re seeing double-digit growth in virtually every geography, in all of our key product segments. Very well-balanced growth across the franchise, which is a sustainable way to continue to grow the business and something that we take a great deal of pride in.

Corporate Payments’ geographic highlights

Daniel Webber:

Are there any particular regions you want to highlight? I know APAC was reported as very strong.

Mark Frey:

APAC certainly did have a super strong quarter, and that’s a number of quarters in a row of very accelerated growth. Of our three key regions between North America, EMEA and APAC, APAC is the smallest of the businesses, but catching up rather quickly. Given the out-performance that we’ve seen both in terms of new business performance and new client acquisition, but also same store sales and the performance of the core business unit and the ability to retain customers, it’s continuing to do super well.

In North America, we’ve seen significant returns to growth, in terms of double-digit growth again in Canada. After being a high single-digit grower for a couple of years that business has begun to accelerate again, which is great to see, with great diversity across the payments and the risk management franchises.

We’ve also had a tremendous amount of success selling enterprise payments in the North American market, both to financial institutions, non-bank financial institutions and other partners, where we’re aggregating a mass payments value proposition in addition to the FX cross-border payments for corporates.

And a very similar story in EMEA as well, where we’ve seen that traditional, very FX-centric business become more of a global payments business and seeing significant success in the fintech sector in particular, powering corporate payments for other partners in addition to our FX business and currency risk management business that continues to chug along and do very, very well as a market leader in that space.

Corpay’s approach to enterprise payments

Daniel Webber:

There’s significant competition in enterprise payments, with many different players approaching it in different ways. What differentiates how Corpay approaches the market?

Mark Frey:

We are a little bit unique in our space as a fintech, especially in that we serve both tier one and tier two global financial institutions – a who’s who of money centre banks around the world. Some of the largest banks in the US, the largest banks in Europe come to us looking for emerging markets, payments execution and liquidity, and we’re able to do that very, very effectively and grow that franchise.

But we also serve smaller financial institutions, both in North America and abroad, where we sell major currency solutions and payment clearing in major and minor currencies for those smaller institutions that don’t have the international capability and reach that allows them to compete with tier one financial institutions.

We really service both ends of the banking sector ultimately, both from an emerging markets and a major currency perspective.

But we also have a variety of solutions that are built as well as API integrations for fintech players that have flows that they’re looking to commercialise within their overall organisation. And the ability to have truly global reach, to be able to make payments in as local a fashion as possible as opposed to just partnering with a big bank that is sending US dollar payments around the world, which is very much not what we’re doing in terms of payments execution.

It has been a very successful part of the franchise for us. It’s where a good portion of our new business comes from and is now a business that has reached a fairly material scale in terms of size and profitability – and an important one in terms of how we think about business going forward.

The role of the FX hedging business

Daniel Webber:

Your FX hedging business is a core need of the market and of businesses internationally. How do you think about the strategy there and the importance of that piece of the business?

Mark Frey:

It is absolutely an important business for us and one that does very well in each of the three key geographies we originate business in. Our approach is very consistent in terms of what we’ve tried to do in the marketplace over the last few years. We bring great quality talent; we try to be very customer-centric; we try to be customised with the solutions.

But I think where we’ve really begun to accelerate in the last few years is introducing a great deal more technology into that value proposition where we can help measure, quantify and better manage the risk leveraging technology for our customers.

We’ve introduced intercompany netting solutions that have allowed us to move significantly up market into the Fortune 1000 customer set, that traditionally wouldn’t have dealt FX or non-currency risk management with a non-bank broker. But they’re coming to us because of our technology, the software that we can provide to them that allows them to streamline their FX and payment processes through their intercompany subsidiaries around the world.

We’ve also introduced a bounty hedging tool that allows large organisations to better manage and monitor the risk that sits on their balance sheet, not just their cash flow, which is the traditional view of currency risk management. It really is these treasury management software solutions that have powered our growth and, in combination with a very customer-centric approach, have proven to be very successful in the marketplace.

Daniel Webber:

Being a large, publicly listed company must help, because there are very few traditional FX hedging companies that are part of such companies.

Mark Frey:

Yes, no question. Being a Fortune 1000, S&P 500 publicly traded company that is SOX compliant and has the regulatory and licensing footprint that we have all the way around the world certainly helps. Size and scale is important, and it’s also our approach.

We’re a very conservative organisation. We focus on selling deliverable forward contracts to a lot of our customers. And we have other capabilities that we offer in certain markets as well, but it is a very straightforward approach that resonates with our clients and allows them to better manage their business and focus on running their core franchise rather than worrying what currency that’s in.

Cross-border’s profitability drivers

Daniel Webber:

There are many players in the cross-border payments space that have not yet reached sustained profitability. Talk us through how you are driving profitability in the cross-border business.

Mark Frey:

The cross-border business is a roughly $700m revenue business, a little bit bigger than that. In calendar ‘24 we will produce close to $400m in EBITDA, in the mid to high 50s in terms of EBITDA margin. It’s one thing to grow 20%+ year-on-year. It’s another thing to grow EBITDA 25% at that scale and that size.

When we think of being a growth organisation, it’s not revenue at all costs. It’s profitable revenue growth that we’re looking to achieve and we ultimately want to build a sustainable profit-making organisation that delivers returns to our shareholders. And so, focused on trying to build a business at scale, trying to do it super efficiently and leveraging technology everywhere that we possibly can to be as efficient as possible.

As we get bigger, some of those things get actually easier because we invest more in technology, we can invest more in automation, and that allows us to achieve a scale that some of the smaller organisations will just struggle to be able to achieve. Certainly we see that from the research that we do in the marketplace that our size certainly gives us some advantages, especially in the world of global payments.

Corpay’s acquisition of Paymerang

Daniel Webber:

Corpay is a very good acquirer, and you just announced the acquisition of AP automation player Paymerang. Where will that sit in the business?

Mark Frey:

It’ll be part of the domestic corporate payments business in the US.

I think we’ve been very clear and Ron Clarke, our chairman and CEO, has been very clear that we expect to be very active from an M&A perspective in corporate payments, both domestically in the US and as far as the cross-border business goes as well.

It’s something that we spend a fair amount of time on – I spend a fair amount of my time surveying the market and looking at opportunities – and certainly we see a lot of attractive opportunities out there for us to do what we’ve done previously with other transactions. We will continue to focus on that and it will be part of our go-forward strategy for the sustained future.

Daniel Webber:

Paymerang adds some specific verticals. Is there anything particular that links it to the cross-border space, or is it more of a domestic offering?

Mark Frey:

It’s really both. It is definitely a US domestic play, but there are certain segments that the business is focused on. I’ll pick on one: the education vertical is something where there is a specific capability and a sales force designed to pursue that market segment, which is also highly attractive in the cross-border payment space as well – and one that everyone is actively pursuing.

A transaction like this gives us a real advantage in that we have that domestic card processing capability and incoming AR solutions, in addition to the cross-border capability for international students. It’s something that we’re really excited about, that we think gives us some differentiation in the marketplace and something that will allow us to continue to grow that segment.

Daniel Webber:

Mark, thank you.

Mark Frey:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.