Corporate payments-focused Corpay has announced that it is acquiring US-based B2B cross-border business GPS Capital Markets in a significant boost to its Corporate Payments division. We caught up with Group President Mark Frey to find out more.

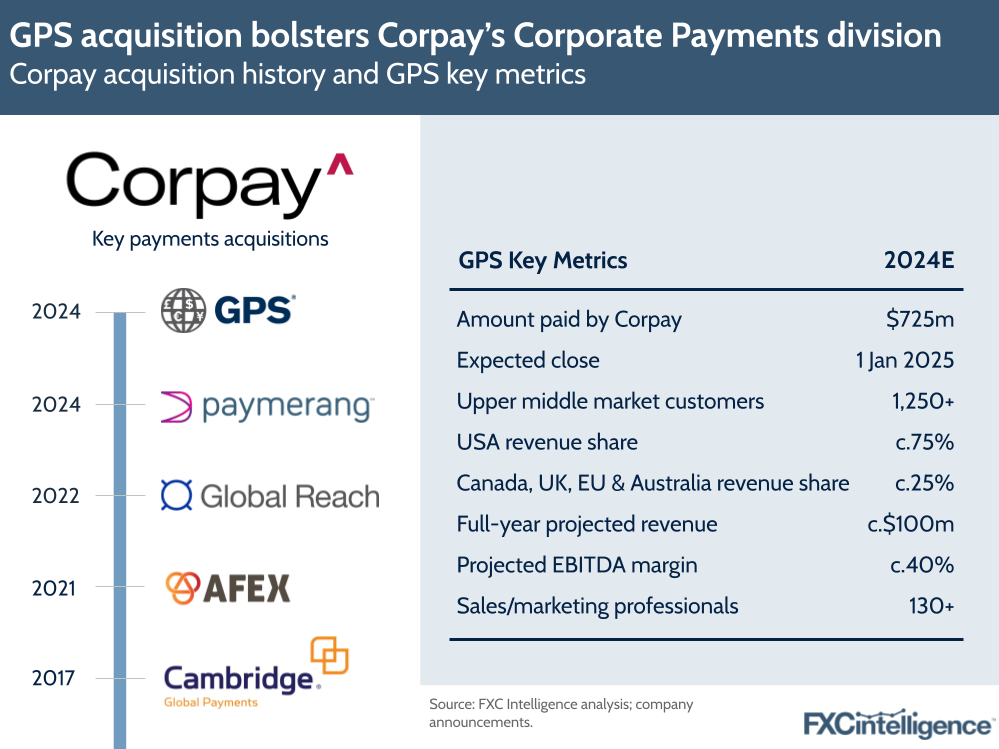

Last week, corporate payments major Corpay announced that it had signed a definitive agreement to acquire GPS Capital Markets, a US-based provider of cross-border payments and treasury management solutions, for $725m.

It is the latest in a series of acquisitions by the company – the third-largest completed by Corpay to-date – and is specifically intended to grow its Corporate Payments business. This division has seen the strongest revenue growth for the company in recent years and gave the parent its current name after it rebranded from Fleetcor earlier this year.

Characterised by Corpay as a high-quality business built and grown by a small number of owners, GPS is notable for its upper middle-market customer base, 75% of which are based in the US. This has made it an attractive purchase, particularly given clear synergies between GPS and Corpay’s Corporate Payments division, which it will be integrated with alongside Paymerang, which the company acquired earlier this year.

Corpay has also highlighted GPS’s netting technologies and balance sheet hedging capabilities, which have the potential to be applied to the needs of both larger clients and Tier 2 and 3 banks.

With this in mind, how does the company see the opportunities for the GPS acquisition, and what will be the priorities for building a post-acquisition strategy? We spoke to Corpay Cross-Border Solutions Group President Mark Frey to find out more.

Key motivations for Corpay’s acquisition of GPS

Daniel Webber:

Corpay is probably the most successful M&A build-and-buy going on in the cross-border payments space. Talk us through what you really like about GPS and why it’s a good fit for the company.

Mark Frey:

We think GPS is another really good fit for us. It’s a quality, well-run business with good, strong management and leadership that has demonstrated the ability to build a great distribution channel and network, particularly in the US, which is their historic and geographic strength.

It makes it a very attractive target for us. What we see is a business that’s focused on high quality mid to large corporate customers. That is definitely moving further up market, much like the journey that we’ve been on over a number of years.

Their recent and/or significant expansion that we’ve seen – into the UK, Europe and now Australia – dovetails very well with the geographic footprint that we have, and a very similar customer base. So there’s a really good fit in terms of the customers.

We were also really attracted to GPS in terms of the distribution talent and some of the back-of-house capability that we see in the executive leadership of that business. Those were the two big drivers for us: customers and individual talent.

Then there’s some really interesting technology capability within that business as it relates to balance sheet hedging and intercompany netting, which are two key things that we’ve been focused on for a number of years. We really see being able to bolt that technology into our overall capability as allowing us to run a little bit faster and ultimately be a leader in the space.

So it’s really those three key drivers that we see as being the key points of value for us.

This is a deal that is right down the fairway: it’s right where we want to be in terms of market size, geography, the size of the business. It is a sizeable asset and is a well-run organisation that fits very well culturally with the Corpay identity as well.

GPS presents an attractive purchase for Corpay

As a profitable company, GPS Capital Markets is an attractive acquisition for Corpay, having seen a c.19% revenue CAGR since 2016. In 2024, it is expected to deliver around $100m revenue, with a mid-40% EBITDA margin.

Crucially, GPS clients are on average three times bigger in terms of spend than the rest of Corpay’s US-originated cross-border business, with some being c.$10bn-valuation public companies. As a result, this is an opportunity for Corpay to broaden its client base to the upper end of the middle market and cross-sell other products to this group.

Here in particular, Corpay sees opportunities to develop a multicurrency account for this customer segment, covering both deposits and disbursements.

From a cross-border perspective, GPS also comes with lower risk than Corpay’s existing business. It not only has a higher share of spot payments, as opposed to hedging, but also runs a lower tenor (the time remaining before a contract expires) on some of its contracts, reducing its credit exposure.

GPS’s netting opportunity

Daniel Webber:

Netting is a topic that’s seeing growing focus in cross-border payments. Talk us through GPS’s netting technology and how you are thinking about it.

Mark Frey:

The way that we think about it is that this is a tool that allows us to move significantly up market into a Fortune 1,000 customer set. To provide a differentiated piece of technology to a large corporate with subsidiaries or divisions all around the world that allows them to streamline and better manage their FX and cross-border payments.

If you think for a moment of a global parent company in the US that has subsidiaries all around the world, and they’re making intercompany payments between those subsidiaries all day long, every day, that aggregates into hundreds or thousands of transactions per month.

What this solution is designed to do is – on a weekly basis or a monthly basis, whatever cycle they determine is appropriate for their business – to net and aggregate all of those transactions and to simplify them so that each subsidiary or division has one net settlement for that month to the network and receives or sends one single payment in their domestic currency.

Everything else is effectively netted out across the group. So what you get is a significant reduction in transactions; a significant reduction in payments and fees that are paid associated with that; and a significant netting of foreign exchange flows so that the FX that you’re trading is substantially less than what it would be from doing all of these individual transactions.

The cost savings from the hard costs and the FX spread that you don’t pay as a customer are significant, but also the time saving; the accounting treatment, the automation that exists with this solution is a huge time-saver for these organisations.

It’s a play that we see works well at the big end of town, in terms of very large corporate customers. There’s significant value in terms of reduced transaction costs and a streamlining of accounting processes and treasury workflows. And we believe that this is a tool that will work really well, going significantly up market into much larger corporates than we would typically have access to as a non-bank FX player.

Balance sheet hedging capabilities

Daniel Webber:

You also mentioned GPS’s balance sheet hedging capabilities. What benefits does that bring?

Mark Frey:

The balance sheet hedging capability is quite mature within the GPS platform. Quite simply, we believe that the plan for us will be to simply lift that product and bolt it to the core technology stack at Corpay.

That product will live on: the customers that continue to use that will have access to that tool. We ultimately believe it is a tool that we can sell and position to many more customers around the world that are looking to manage the FX exposure inherent within their balance sheet.

Again, it’s a tool that allows us to move upmarket into larger corporate customers. It provides for automation and accuracy in reporting and accounting for FX transactions. It adds another increased level of sophistication for that large corporate customer that’s looking for improved workflow, streamlined processes and consolidated relationship management from an FX perspective.

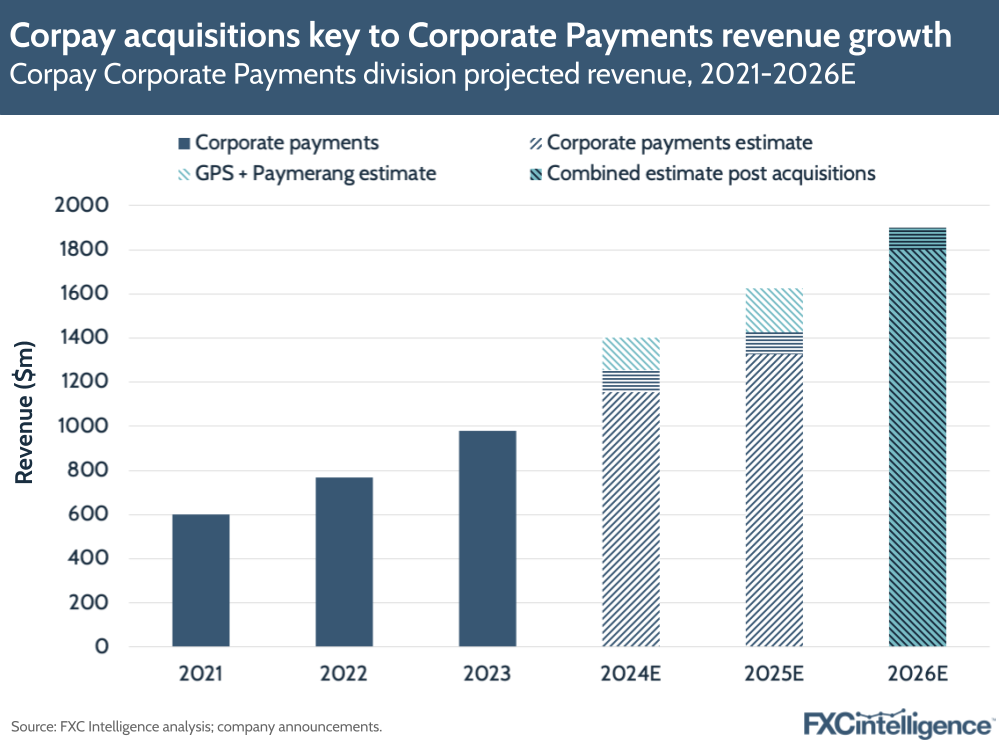

GPS, Paymerang synergies to help Corpay Corporate Payments approach $2bn

Corpay expects both GPS and Paymerang to achieve significant synergies with the Corporate Payments division, and together are key to it reaching close to $2bn revenue by 2026, at which point the segment would account for almost 40% of Corpay’s overall revenue.

Together, GPS and Paymerang are expected to provide around $200m in incremental revenue in 2025 and increase the overall Corporate Payments business by approximately 15%.

Corpay sees significant synergies between Corporate Payments and GPS in particular due to the high levels of adjacencies between the two. As a result, it expects to see EBITDA increase by more than 50% above the BAU number for 2025. This is expected to be the result of realising expense opportunities around the technology system, back office and compliance operations, alongside additional products, including some focused on credit.

From a cross-border perspective, the company expects to see its current revenue mix of 60% cross-border to 40% payables remaining the same over the next three years. However, it sees increasing opportunities to cater to the cross-border needs of $100m-500m revenue enterprise companies, which are often currently served by Tier 2 banks with little FX-specific expertise.

Cross-border payments’ revenue share

Daniel Webber:

Cross-border currently accounts for 60% of the Corporate Payments revenue. Do you expect that to grow as you approach $2bn revenue?

Mark Frey:

These businesses are growing in lockstep in high-teens, low-20s year-on-year, every year, organically. We’re focused on doing deals on both sides of the fence.

The domestic payables business has a live deal with the Paymerang acquisition that they’re set to close early next month. We’re obviously working on GPS. And we believe we will continue to execute on that strategy and we will continue to be acquisitive in Corporate Payments for both the payables and the cross-border sides of the house.

It’s important to build these businesses in lockstep and that they will continue to grow at similar rates. We purposefully invest in the businesses to continue to grow at similar rates and we believe that there’s a long runway for us to be able to do that well into the years ahead.

Corpay’s ongoing acquisition strategy

Daniel Webber:

If 60% of your $2bn target revenue is cross-border that’s $1.2bn – that’s a significant cross-border payments business. How much are further acquisitions going to contribute to reaching that number?

Mark Frey:

We believe we’ve got a plan organically to get to that $1.2bn, but we don’t plan to necessarily do it organically alone. We will continue to be acquisitive in the space.

We do expect that, every 12 to 24 months, we will execute another sizeable deal. We still think that there are lots of attractive targets that are reaching levels of maturity, that those opportunities will come to market, and we expect to be involved in all of those conversations and try to acquire the best assets. The best assets in the market, and also those assets that we think are the best fit for us, that we really believe we can improve those businesses.

That’s always a big part of the focus for us: we’re looking for assets and capability that are interesting, but with a financial profile that we can optimise the revenue performance and the revenue growth and drive sales, which is the superpower of our organisation.

We can sell more effectively and more efficiently than most organisations, given the size and scale of the business. And we have economies of scale in terms of the back office processing as well, where we can leverage those economies of scale in our processes to optimise the OpEx of the business to generate significantly more profit growth.

Our focus is always to drive profitable revenue growth, top and bottom line. We believe that GPS is the next wave that will enable that on an inorganic basis, but organically we continue to chug along.

We’re growing a little faster than 20% this year; growing the bottom line just under 30%. It’s a nice story and continues to be one, and we believe there’s a lot more runway both in terms of the M&A pipeline that we see in the years ahead and we see no reason why things will slow down organically in terms of what we’re doing as well.

Daniel Webber:

Mark, thank you.

Mark Frey:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.