Bank of America has unveiled a new real-time cross-border payments solution for companies and financial institutions. We sat down with Head of Global Payments Product AJ McCray to find out more about the launch and the bank’s plans for the network going forward.

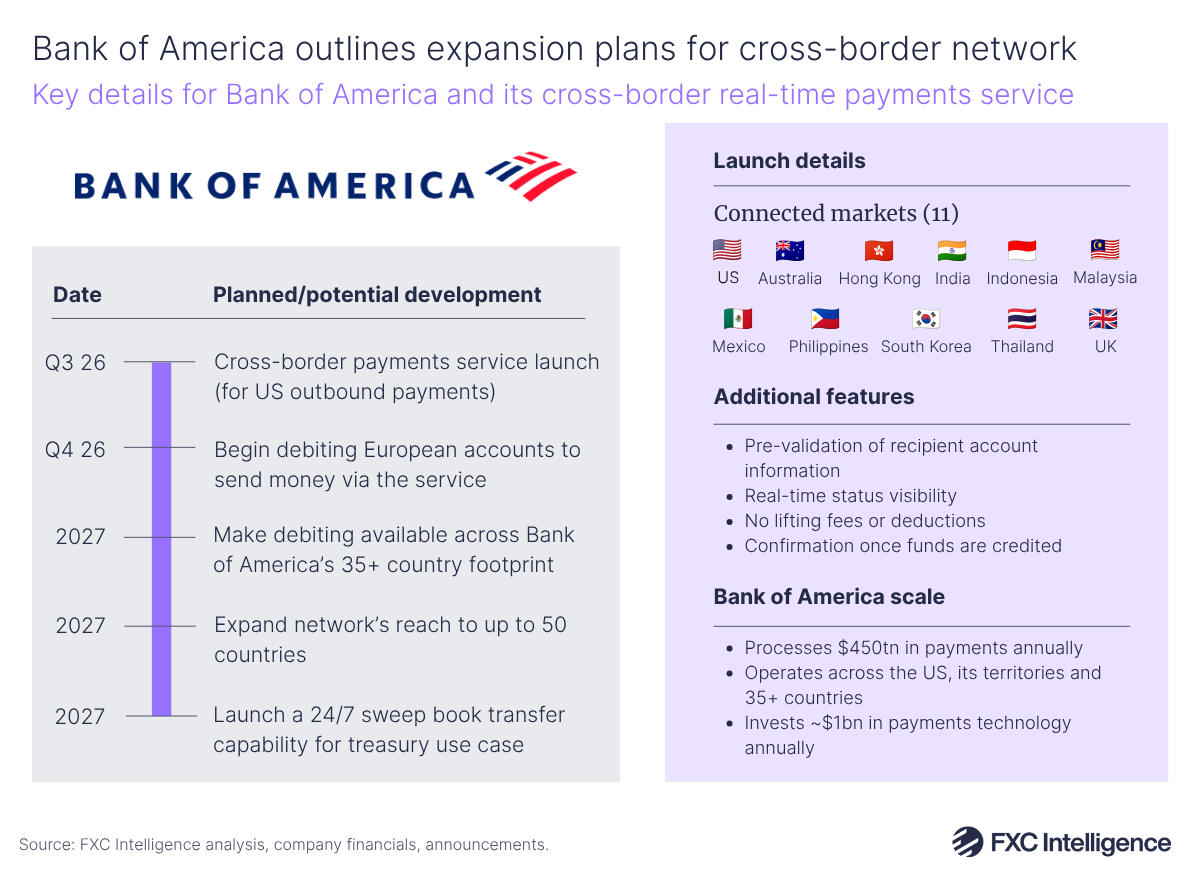

Bank of America plans to launch its own real-time cross-border payments solution in Q3 2026, promising to cut cross-border transfer times down from days to seconds. The bank’s solution connects to a number of existing real-time payment networks worldwide – including Mexico’s SPEI, the UK’s Faster Payments System and India’s UPI – to deliver funds to beneficiaries in their local fiat currency.

“We’re targeting low-value, high-volume cross-border payments that our clients need to process, payments that are largely going to consumers or very small businesses,” explains Bank of America Head of Global Payments Product AJ McCray.

The new service is aiming to support the bank’s corporate, commercial and financial institution clients with a range of use cases, including international remittances, gig‑worker payouts and ecommerce marketplace vendor payments.

We sat down down with McCray to find out more about Bank of America’s decision to launch the cross-border payments network, the capabilities and reach it will offer at launch and future plans for the service.

Bank of America’s new real-time cross-border service

According to McCray, there has been increasing demand from both large companies and the bank’s correspondent banking network to offer faster, cheaper and more transparent cross-border payments as end recipients expect them to match the speed of real-time domestic payments.

“We have seen more and more of this demand over the past several years, especially as the use cases grow and the companies themselves grow.”

McCray explains that another key factor behind the imminent launch is “infrastructure readiness”, given that a large number of domestic real-time payment schemes across the globe are now very well established, with many also enabling cross-border payments in some form. “These types of payments have traditionally been processed through wire. Until recently, there has not been an alternative infrastructure to move money cross-border outside of the wire system,” he adds.

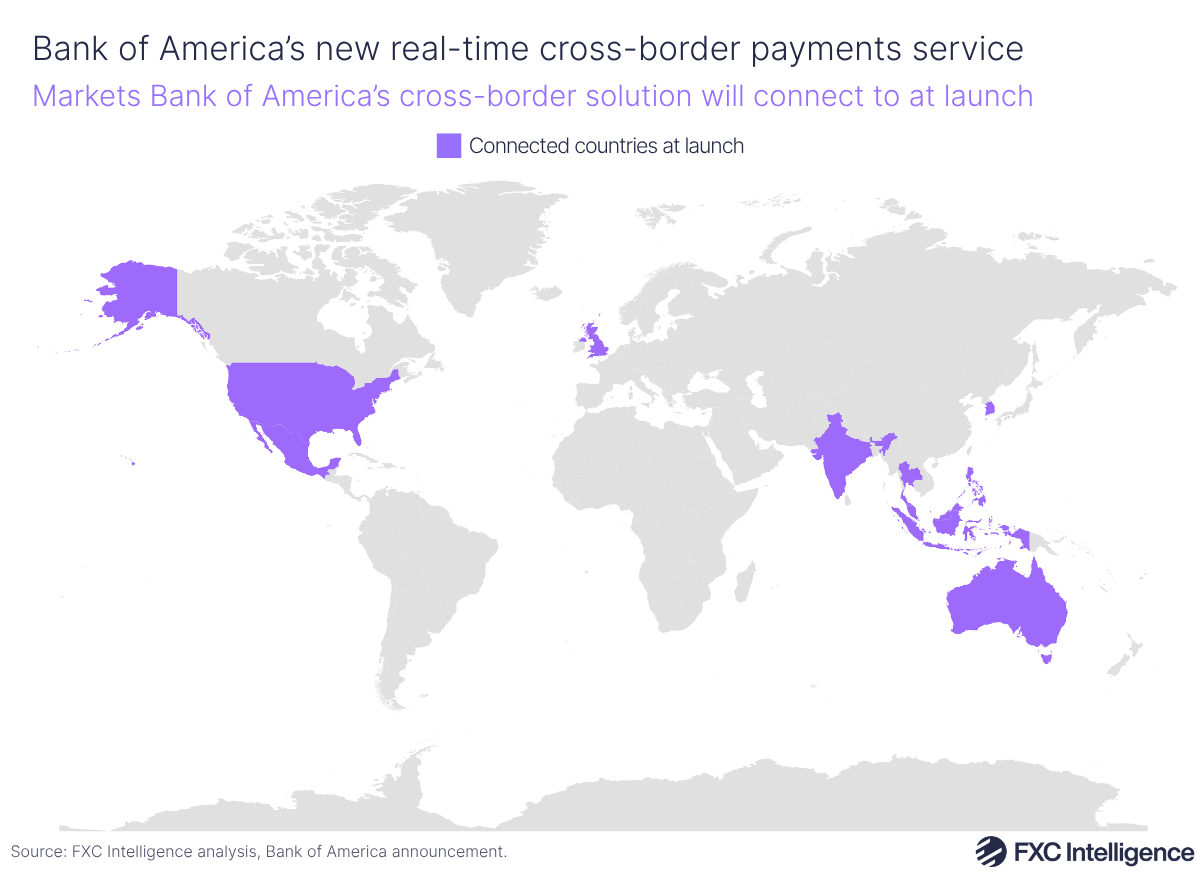

At launch, Bank of America’s new service will connect to 10 countries, including some of the largest recipients of remittances in the world: Mexico, India and the Philippines. The bank could also potentially expand the network’s reach to up to 50 countries by the end of 2027. “Other countries that are high on our list include Brazil, Japan and Singapore,” explains McCray. “We’re also looking at countries in the Middle East and Africa.”

To begin with, the cross-border payment service will enable outbound payments from the US, although the bank has plans to enable European accounts to send payments to the same set of countries, having seen the most demand from Europe. Next year, Bank of America will look to expand even further, making the service available across its entire more than 35 country footprint.

“This solution will help our customers fulfill their goals while helping us expand our relationships with those same customers. Our approach starts with the client problem and we then figure out the best way to solve it. We are investing in the areas that we think our clients care about most.”

The service will also enable Bank of America clients to receive inbound real‑time payments into the US. By delivering faster, cheaper and more transparent global payments, the bank is also supporting the G20 targets for enhancing cross-border payments.

Providing greater insight into cross-border payments

The new solution will enable the sending and receiving of funds instantly either through financial messaging service Swift or CashPro, Bank of America’s digital banking platform for corporate and institutional clients.

“We’re going to be offering this service through two main channels,” explains McCray. “One is our CashPro channel, that our corporate clients use, and the second is through Swift, the channel that our FIs use.”

CashPro provides the bank’s clients with a single point of access for payments, receivables, liquidity, foreign exchange, investments and trade services.

“Corporate treasurers have been investing in modernising their own technology over the past few years and they are now ready to interact with their banks in a more sophisticated way, such as via APIs or machine-to-machine connectivity. At the same time, we’ve been investing in our platform, both in terms of our payments capabilities and channel capabilities. As a result, our clients can interact with us in more expansive ways and take advantage of the latest payments technology.”

CashPro supports a number of different connectivity options, including online, mobile, API and file‑based channels. McCray says Bank of America will receive API messages from its clients to initiate payments, it will then be able to carry out the payment and send a notification of completion back to the client in seconds. The bank also plans to provide greater richness of data to clients, which will enable them to respond to errors more quickly.

“Another area we’re investing in quite heavily is CashPro Insights, which provides clients with analysis and recommendations. As corporate treasurers become more sophisticated and grow their ability to ingest more information from the bank, they’re looking to the bank for insights on how they can improve their efficiency or reduce their costs, for example,” McCray explains.

Inside the network’s roadmap

While Bank of America’s new real-time cross-border payments service will initially support low-value transactions, McCray says it has also seen demand for some high-value use cases, including from multinational corporations wanting to move money across their own treasury and liquidity structures.

“Next year, we plan to roll out a 24/7 sweep book transfer capability, where treasurers can move very high-value across their treasury structures from say Dublin to Singapore, or wherever their locations are,” says McCray. “That’s one key use case that we’re building towards.”

The bank is also considering how it can better service other use cases, including supply chain finance where large multinational corporations need to pay suppliers in other countries.

“Say an oil and gas company needs to make supplier payments and many of those suppliers are also Bank of America customers; we can fulfill that need within our own network. So we’re also looking to expand this notion of external cross-border real-time payments with the internal sweeps to carry out supplier payments for multinationals.”

McCray believes that the ability to carry out high-value payments externally across financial institutions is currently missing in the market but there are a number of ways that this need could be serviced.

“You’ve got a few choices about how that may work. One is you could take the wire infrastructure and improve it. Second, you could take the real-time payments infrastructure and increase the limits. The third option is to build a new network, where you get the 24/7, instant payments that support this. From our perspective, we’re largely neutral on which one will be the winner. We’re investing in all of them and for us, it’s about being able to meet the client’s needs.”

Looking to the future, McCray believes that cross-border payments will gradually offer a more local payment experience, with more “detailed and actionable” reporting back for corporate treasurers – something he says Bank of America is specifically “investing towards”.