Fleetcor-owned Corpay is one of cross-border payments’ biggest non-bank players catering to the B2B space, and has continued to see strong results in its Q3 2023 earnings. We caught up with Group President Mark Frey to find out more about the company’s strategy.

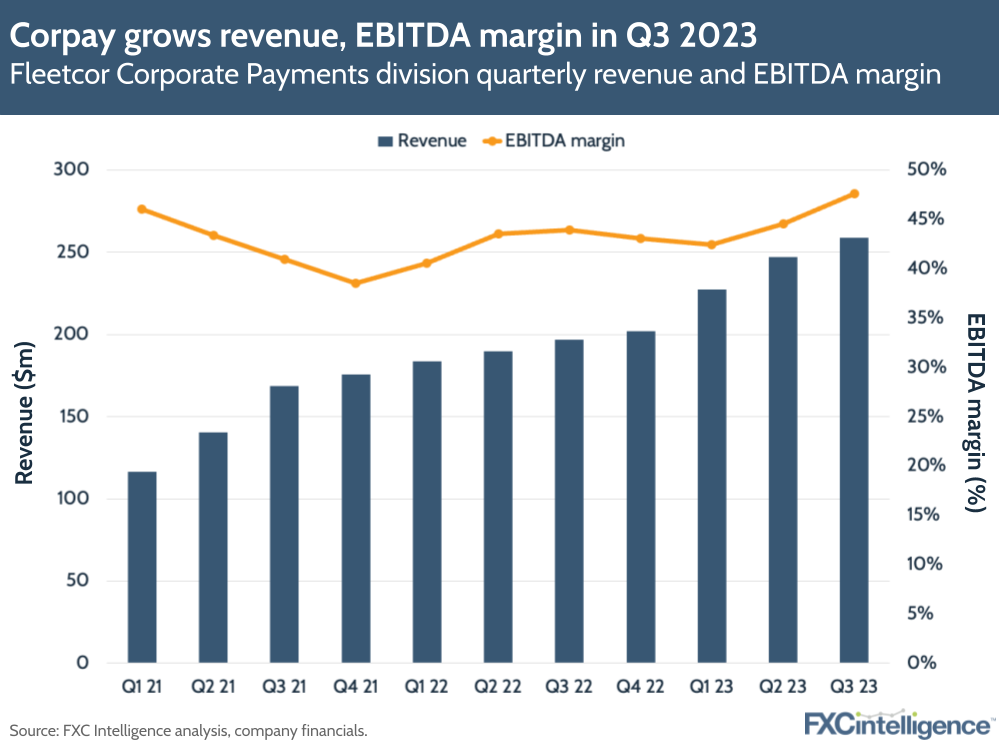

Corpay, the Corporate Payments division of Fleetcor, has seen strong growth in Q3 2023 that has significantly outpaced that of its parent company. Corpay’s revenue grew 31% YoY to $259m in the quarter, compared to Fleetcor’s 9% increase on an organic basis to $971m.

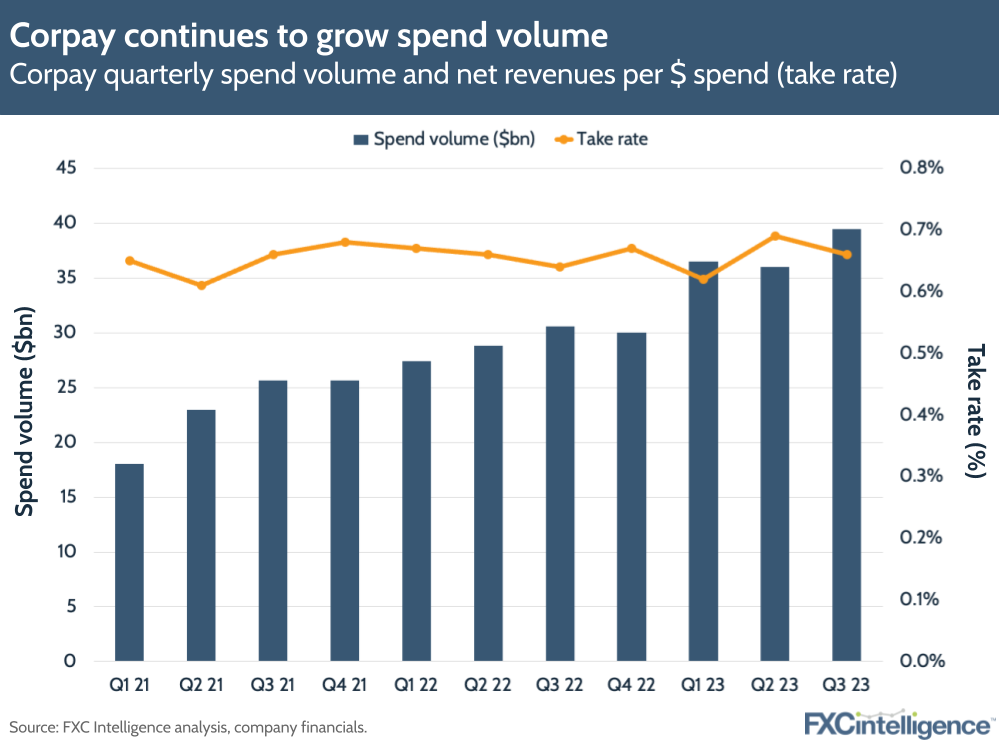

Key to Corpay’s growth was a 29% YoY increase in spend volume, which reached $39.5bn in Q3 2023. Cross-border sales also increased by 28%, driving cross-border revenues up by 19%. The company claims to now be the largest non-bank FX provider in the world, with around 80% of its business outside the US.

Corpay’s business is driven by two main areas: payables and FX. The company’s direct business increased by over 30% YoY, with particularly strong growth in accounts payable, which increased by 28% as the company attracts new customers mostly looking to modernise their AP operations.

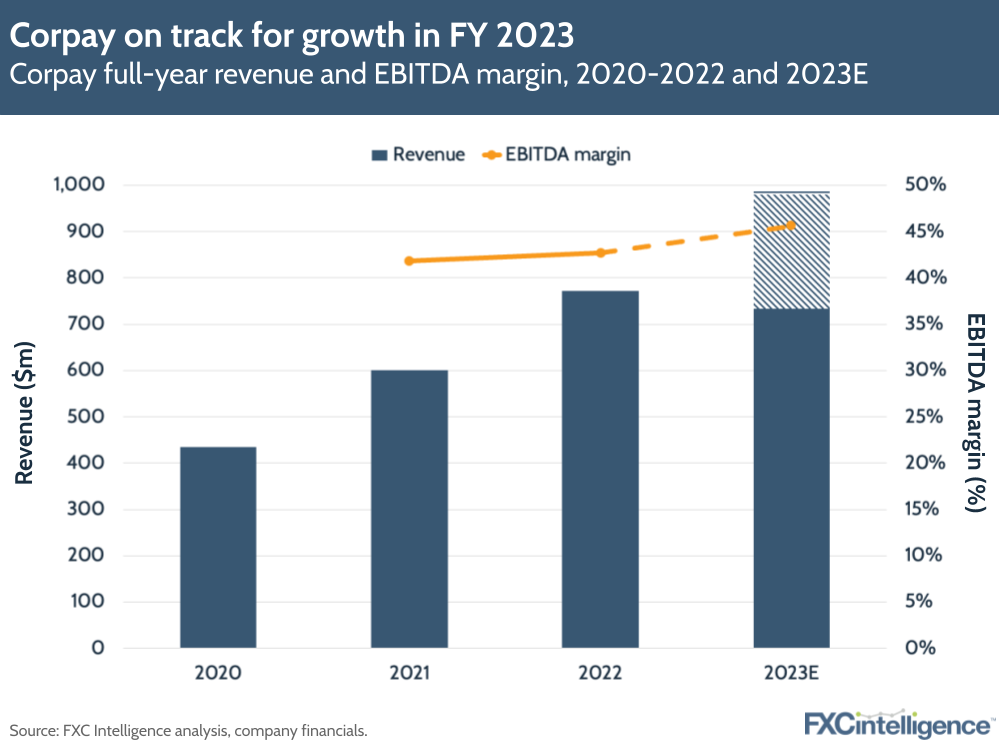

While the company’s last few years has seen it focus on building scale on the cross-border side and refining its software offering, it is now focusing on marketing and sales and is looking towards a goal of $1bn a year in revenue.

There is also the potential of a spin-or-merge play with Corpay, which could potentially see the acquisition of another player to merge it with Corpay and spin the new entity out to form a standalone business, something the company is in ongoing discussions about.

With these moves in mind, I caught up with Corpay Group President Mark Frey to find out what is in store for the company.

Drivers of Corpay’s Q3 2023 earnings results

Daniel Webber:

You’ve had a very good quarter for Corpay, both overall and within cross-border. What’s driving that?

Mark Frey:

The biggest point of success for us in Q3 is total revenue organic growth on our print and on a macro-adjusted basis. It was strong across the Corpay franchise, delivering growth in and around 20-21% for the quarter, with strength in both the domestic segment, the domestic payables business, and cross-border – both north of 20%. Very strong overall growth and on our pro-forma basis from a total revenue perspective.

The biggest thing that underpins that is the new revenue performance, the sales performance of both business units, which was up substantially sequentially, quarter-on-quarter, year-on-year. We saw very strong growth for in-year calendar realised revenue as well as from net new customers trading for the first time in 2023. That has probably been the biggest driver of overall revenue growth across the franchise.

Corpay’s client profiles and reseller play

Daniel Webber:

You talked about robust recurring client activities. What does that mean and what does that type of client look like for you?

Mark Frey:

The focus within corporate payments is ultimately to drive relationships with both channel partners and aggregators. That might be fintechs, it might be non-bank financial institutions where they can resell our capability and do so on a recurring revenue basis with their downstream clients. Ultimately leveraging their capability to expand our distribution.

But there’s a large portion of the business that is us going direct to a mid-market corporate customer, both in the domestic US as well as in all the international markets that we serve.

The goal is always to find recurring revenue relationships, long-term relationships with customers that have ongoing payment needs, whether it be cross-border or domestic payables within the US. That is really where we focus our time and attention to generate those long-term recurring customer relationships.

Daniel Webber:

The reseller space is competitive. What do you find are the differentiators for Corpay’s offering there, compared to bank and non-bank peers?

Mark Frey:

It’s the capability on both sides of corporate payments. If we look at the payables business in the US, it is the ability to convert payments to card and retain revenue and volume on card, ultimately because of the differentiated network that we’ve developed over the past generation.

In the cross-border business, it’s really about the differentiated capability in terms of the payout corridor, the ability to make payments in more than 145 currencies, in 200 countries around the world and, for the most part, make those payments in a very localised fashion.

When we think of making cross-border payments, we try to make cross-border payments in as local a fashion as we possibly can, leveraging a local, in-country nostro account and/or in-country partner as opposed to sending foreign currency overseas.

That makes a big difference in terms of the sustainability of that revenue profile and the customer service that that individual client receives in the end.

APIs and the role of technology

Daniel Webber:

What are the pieces on the technology side that resonate with your clients?

Mark Frey:

It’s really a breadth of solutions, it’s not any one thing. Certainly we see customers that are coming to us and they’re looking for us to connect via API to their front end.

It might be web-based or it might be a platform, but that is usually a journey for many organisations, particularly financial institutions that don’t really have the fintech-like capability to develop something quickly and stand it up. We generally see that there are a series of iterative integration steps before we get to a full API connection.

That’s not necessarily the case in the fintech world, so when we partner with a fintech aggregator, it usually is an API connection to begin with, but it can take many, many forms.

We can integrate via Swift, we can integrate via an ERP direct channel. We have some of our customers that are ultimately using a white-label platform, so they leverage our technology and re-skin it and then sell it to their downstream customers as well. That overall tech footprint and integration can take many forms with these partner relationships.

Key markets and geographic trends

Daniel Webber:

80% of your business is outside the US. Are there any geographic trends or interest markets that you are seeing resonating well?

Mark Frey:

Historically, the cross-border business was overwhelmingly North American business. Going back three or four years, we began to grow very aggressively in APAC and the UK/Europe.

Growth in both those regions has accelerated. Both through inorganic acquisition, in the Afex and the GRG [Global Reach Group] deals that we have done over the past few years, but also in terms of the organic revenue growth and the investment that’s going into both of those geographies as well.

The UK continues to be a very strong market for us, it is the second-largest market outside the US, and Europe is quickly gaining.

We see the strongest growth, year-on-year, in continental Europe today. Our particular focus has been Spain and Italy, now expanding into Portugal, France, Sweden. Other markets in Eastern Europe have also been very strong for us.

Then, APAC has grown to be not just an Australian business but a Singaporean business for us in cross-border. That business is growing very robustly, starting from a small base but growing quite nicely now. It’s maturing in terms of the quality of pipeline and the quality of corporate customers and the partner customers that we’re seeing through that Singaporean business.

We look at our overall business and think of Canada as probably being our most mature market, which we’ve been in for the longest period of time, and that is beginning to normalise in terms of growth rate. The US is still a very robust, above-the-line grower for us, in terms of overall geographic composition of our revenue, and then Europe and APAC after that.

Daniel Webber:

Do you find many differences in customer needs between different markets in the world?

Mark Frey:

Certainly, everywhere outside the US to start with is generally a little more FX-centric, to a certain extent.

We’ve seen those businesses grow up, they’re not just purely FX-centric the way they once were. The Australian market, the Canadian market, if I went back five or 10 years ago, were very much FX-centric markets, but we see a lot of payment growth coming from those geographies now through both channel partners and our direct corporate customers that we’re onboarding.

Many more of our customers are looking for a global payouts capability or a global payment opportunity, rather than just being FX-centric. In the US, we’ve seen the reverse. What was once a very US dollar and local currency-centric payment market is now starting to grow up and become a little bit more FX-centric.

We’ve seen a lot of growth with our currency risk management capability in the US that we perhaps haven’t historically seen. The US is beginning to look a little bit more like the other markets in that it’s becoming a little bit more FX-centric, the international markets are becoming a little bit more payment-centric.

The differences between the US and the rest of the world are becoming much less stark today than they were four or five years ago.

Daniel Webber:

What is driving that change in the US market?

Mark Frey:

One of the changes in our business is that we’ve moved decidedly upmarket. We’re no longer a small business payments company, we’ve moved into the mid-to-large-corporate space.

As the business has become more partner-centric as well, the cross-border centricity of those larger enterprises is much higher than a small business in the US. That’s where you still see the very stark contrast: small business in the US is largely domestic-oriented, but big business in the US looks not dissimilar to other economies around the world.

Part of it is our mix in the customers that we’ve onboarded to our business, ultimately, are just a little bit more FX-centric because they’re larger in size.

Daniel Webber:

By contrast, what is driving Europe’s move to becoming more payment-centric?

Mark Frey:

If I look at Southern Europe, the overall competitiveness and capability of some of the regional banks is not as high as it is in the UK and some of the other markets. There’s a real element of the market being underserved in terms of global payment capability in parts of Europe and so we see that part of the business growing quite nicely.

But it’s a relatively balanced business for us in Europe, where it is a payments-driven and an FX-centric market. That is a really good competitive mix for us of being able to compete very well with the large regional players and the tier-one money centre banks that operate in that geography as well.

Corpay’s potential future as a standalone business

Daniel Webber:

There has been some conversation around how Corpay might evolve as a standalone or merged entity. Talk us through that discussion.

Mark Frey:

With Fleetcor’s strategic review of the overall franchise, there’s been lots of interest in the Corporate Payments division in particular because of the growth rate and because of the size of the TAM in both the domestic business in the US, as well as the cross-border business globally.

It’s a highly-attractive space; it’s no secret that our growth rates have been above the line average versus the rest of Fleetcor and continuing to exhibit very strong performance year-on-year, quarter-on-quarter, from an overall sales perspective.

There’s been lots of interest in terms of what a possible strategic review of that Corporate Payments business would look like. I think as Ron [Clarke, Fleetcor CEO] said on the earnings call, we continue to evaluate alternatives and we continue to look at any way to generate value for shareholders.

We’re being very active in terms of turning over every stone to look at opportunities.

New product offerings

Daniel Webber:

Can you provide any colour on your new products?

Mark Frey:

We put a ton of focus and investment in our financial institution solutions that we’re leveraging both in the domestic US market and in Europe, the UK, Canada and Australia as well. There we continue to focus not just on mid-market corporates, but on smaller financial institutions that can leverage our capability to outsource their international treasury or FX capability to us.

We’re continuing to invest in the core integrations to the core ERP systems that power those banks or the banking-as-a-service software providers.

Then we’re building out white-label solutions for organisations that really need a technology footprint but don’t have it today that is cross-border centric, that they can push down to their direct corporate and/or private client customers. That’s been a big area of investment for us that we’ve had tremendous success in. It’s a franchise of our business in cross-border that has really taken off in the last year.

We have long been in the US financial institutions business, ultimately in providing cross-border services to those institutions. But with our emerging markets capability – where we become the payout provider to tier-one financial institutions around the world that are looking to move money from the Northern Hemisphere to the south, with a particular focus on Latin America and Africa as our geographic corridors of strength – it’s been a big area of investment for us. It’s a business that’s performed very well since 2015 when we started that franchise.

The other key thing that we’re in the midst of launching and rolling out at scale is our multicurrency account capability. We’ve always had multicurrency account capability, which acted as a store of value and an operational account for customers that are doing business internationally. We’ve added a lot more capability to that as an AR solution for export-based customers that are collecting foreign currencies from customers around the world.

We are really now pivoting that business so that we can act somewhat as a correspondent bank for smaller financial institutions that are looking to have access to a broader correspondent banking footprint. Those are both areas of high growth for us that we think are going to be important parts of the growth story for ‘24 and beyond.

Daniel Webber:

Great. Is there anything else that you would like to cover?

Mark Frey:

The key element for us is that we still think of the business as an organic growth machine, where we still can deliver 20%-plus or high teens to low twenties percent growth year-on-year, on an organic basis. But we expect that we will continue to do deals across the corporate payments franchise, both in the domestic North American business, but in the cross-border business as well.

There are lots of attractive targets that we think are going to be coming to market and we expect to be involved in all of those discussions.

It’s a stated part of our overall strategy and something that I think we’re well positioned to do at Fleetcor as well. Something that I think will be an important part of the story as we continue to grow the business.

Depending on how you look at it, we certainly see that we are the largest in the non-bank B2B space. We look to accelerate that advantage by growing faster than our competitors and continuing to do deals that will bring capability and geographic expansion to the franchise.

Daniel Webber:

Mark, Thank you.

Mark Frey:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.