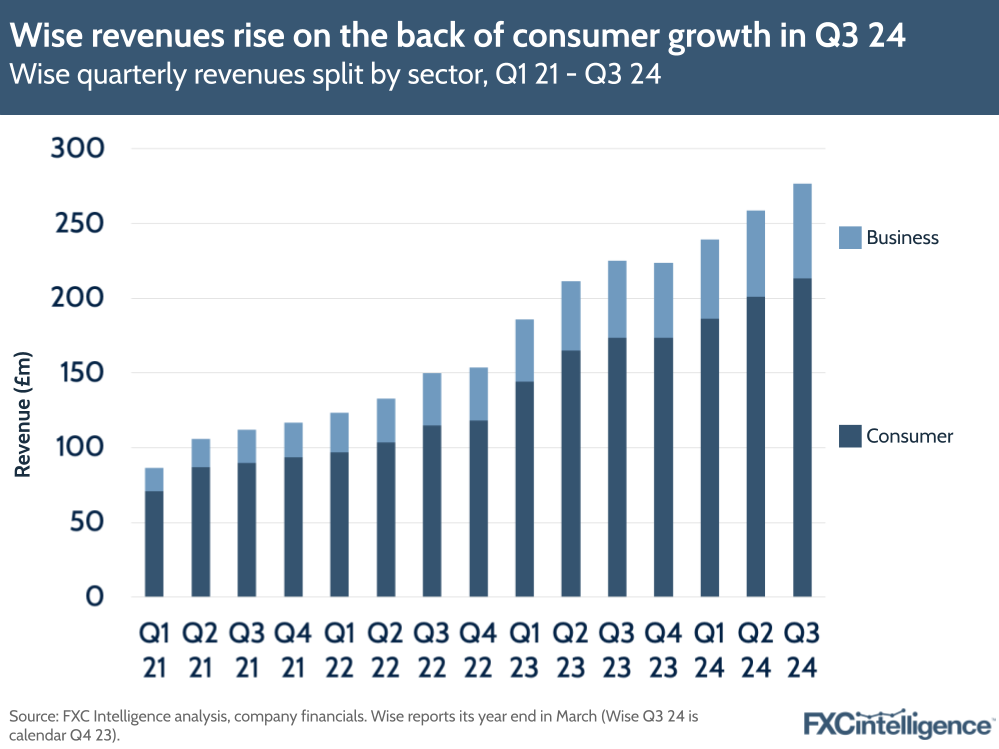

This week, Wise raised its FY 2024 income guidance after it saw revenues rise by 23% to £276.6m in Q3 2024 (calendar Q4 2023), driven primarily by a 30% rise in active customers to 7.5 million.

The company noted a growth in customers using multiple features across its platform, which helped spur a 40% increase in income to £375.1m, and continues to expect high profits this year as a result of higher interest income.

On the back of strong customer growth, Wise is now expecting its overall income to grow 42-44%, a substantial figure for the money transfer space and higher than the 33-38% previously guided.

The company expects its adjusted EBITDA margin to remain high compared to its medium-term guidance of at or above 20%, though it didn’t project a specific margin figure for the year.

Growing multi-feature customers are driving volumes

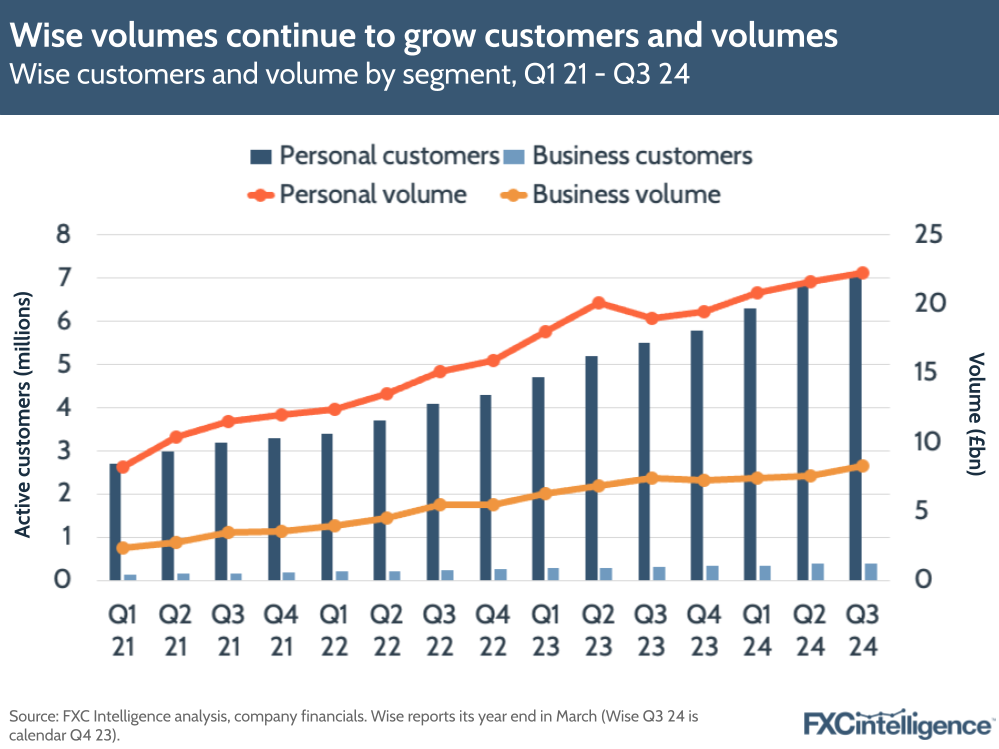

Wise’s personal customers increased 30% YoY to 7.1 million, and active business customers increased 23% YoY to 392,000. Moreover, 46% of personal customers and 60% of business customers are now using multiple features on Wise – such as its international debit card alongside remittance services – which the company said is key for retention and rising revenues.

Customer growth remains a core driver for Wise’s volumes. Specifically, cross-border volumes grew by 16% (18% on a constant currency basis) to £30.6bn, a solid increase though not as high as last year’s 28%. Across personal and consumer transactions, Wise’s overall take rate rose by 5 bps to 0.9%.

In contrast to previous earnings reports, consumer volumes rose at a faster rate than business volumes in Q3 2024, with consumer volumes rising 17% to £22.3bn while business volumes rose 12% to £8.3bn.

Compared to last year, volume per send once again declined for consumers (-11%) and businesses (-9%), though this was affected by the significant customer rise in both segments. In its trading update, Wise said that it had continued to see faster volume growth amongst customers sending more than £10,000 per month, compared to customers sending less than £10,000 per month.

This could reflect the growing importance of its product to businesses, which send much higher volumes through Wise than consumers on average. Though business customers still only account for 5% of Wise’s overall customers and volume growth has slowed since last year, businesses still account for around 27% of Wise’s volumes and 23% of its revenues.

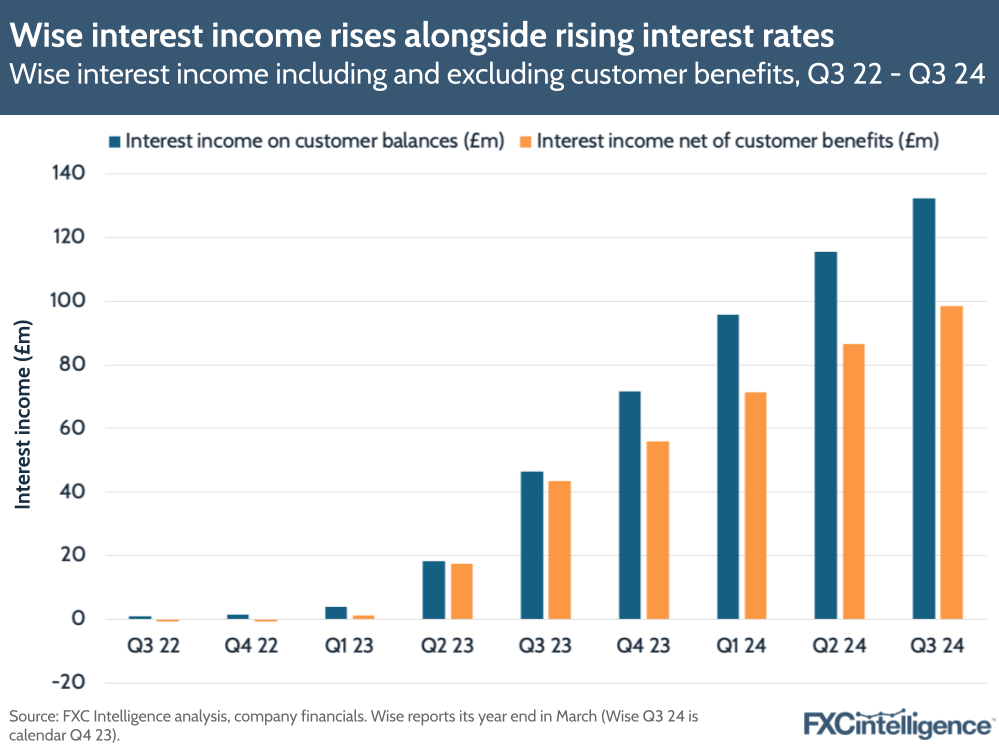

Interest expected to drive profits in FY 2024

Wise’s higher growth guidance reflects its higher interest income, which continues to drive profits for the company as customer numbers rise and customers hold higher balances in their accounts.

Overall, balances held on Wise Accounts rose 28% to £12.9bn, and the gross yield on these balances was 4.2% versus 3.8% last quarter. Wise noted that 1.1% of balances, or around £33.7m, was returned to its customers.

As FXC Intelligence previously discussed with Wise CFO Matt Briers, the company hopes in the long run to return much more of account interest to customers, but it hasn’t been able to do so because of its current banking status. Notably, Wise’s share price has not seen much change after its positive results; while interest rates are still high, central banks are coming under pressure to cut them, which could have an impact on Wise’s revenues.

Having said this, Wise Co-Founder and CEO Kristo Käärmann noted that the company had expanded its Interest Asset across seven European markets, meaning customers holding USD in those regions could opt in to earn a return on those balances. CFO Matt Briers did stress to FXC last year that the company’s underlying growth meant that it would not be dependent on a high interest rate environment.

Wise continues to see high growth relative to the rest of the money transfer market. Though there was no mention of the company’s recent partnership with Swift to facilitate easier cross-border payments for financial institutions, the company has continued to build up its platform through numerous partnerships, including with UK bank Allica, digital travel business Agoa and spend management solution Payhawk.