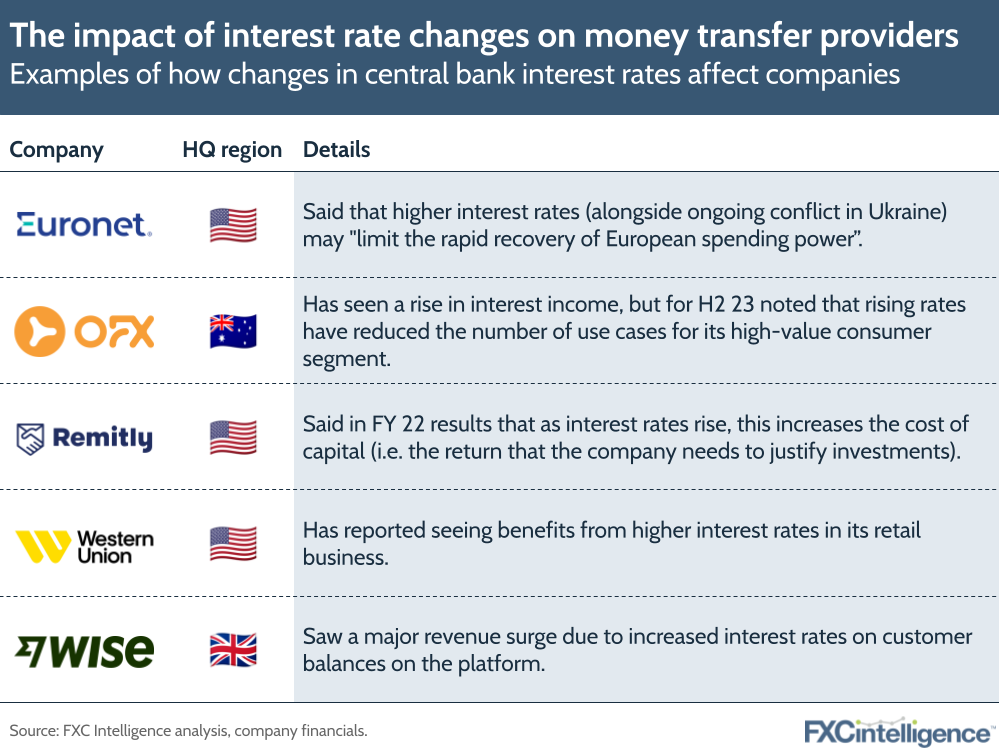

After rising rapidly in 2022, central bank interest rates in a number of major countries appear to have peaked recently. While companies can see higher income from interest on assets, higher rates can also incur larger interest expenses on any debts they may have.

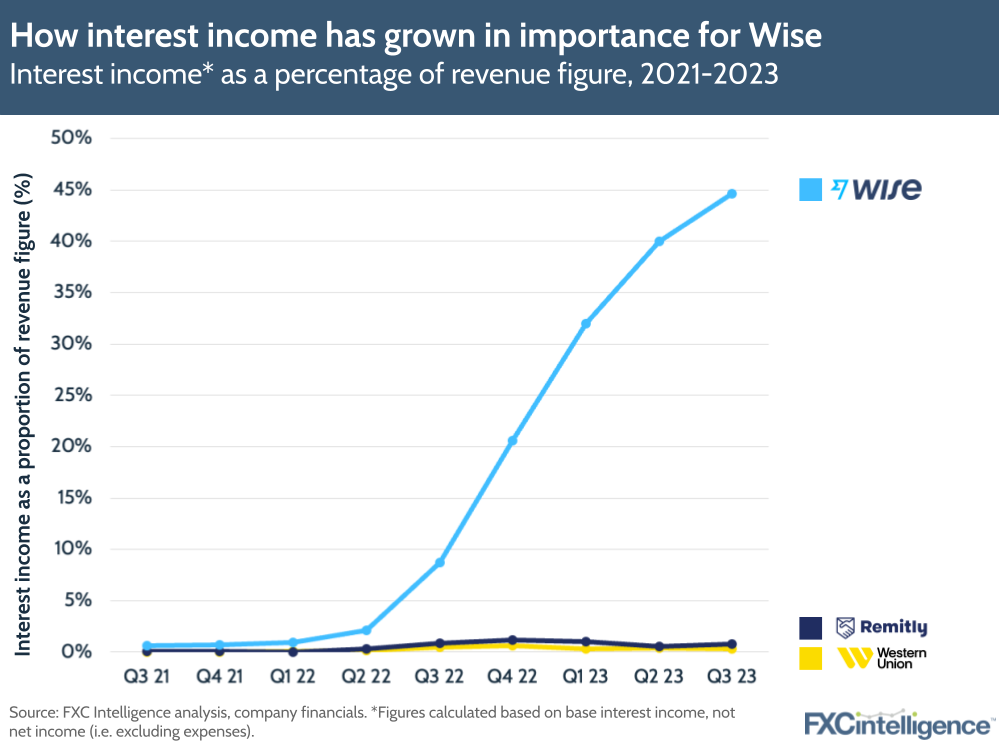

Last week, we discussed the impact that interest rates have had on Wise, which saw income increase by 58% to £656m in H1 24 (equivalent to calendar Q2 and Q3), driven by interest income net of customer benefits rising significantly YoY. Here, Wise saw the income on personal accounts rise from £9.7m in H1 23 to £87.7m in H1 23. While other companies in the money transfer space have not seen this same boost, they have still felt an impact from rising interest rates, as discussed below.

Impact of rising rates on money transfer companies

As in any other industry, interest rate changes impact profitability for money transfer companies as their losses will include interest expenses. In their FY 2022 earnings call earlier this year, Remitly executives mentioned that the cost of capital (i.e. the amount of return that companies need to justify an investment) increases as rates rise.

Rate changes also affects exchange rates, which in turn have an impact on money transfer pricing and also affect consumer spending across certain corridors. Some companies, particularly OFX and Euronet (which owns Ria and Xe), have also noted that negative impacts of rising rates on consumer behaviour can affect revenues.

Having said this, Wise is reaping the benefit of higher rates, specifically due to a higher rate of interest income accrued on customer balances held on its platform. When comparing the company’s interest income figure for calendar Q3 2023 (Q2 24 in Wise’s financial year) against Western Union and Remitly, interest income is proportionally a far higher percentage of Wise’s overall revenue figure.

It should be said that the figure included here relates to Wise’s overall interest income figure on customer balances, which excludes the impact of paying interest expenses and benefits related to customer balances. The company shared that it has paid customers over £53m in benefits in the first half of its financial year, which constitutes around 35% of its interest income.

Even considering expenses and benefits, the benefit to the company of expanding from money transfers into savings accounts near the end of last year is clear.

How central bank interest rates are changing

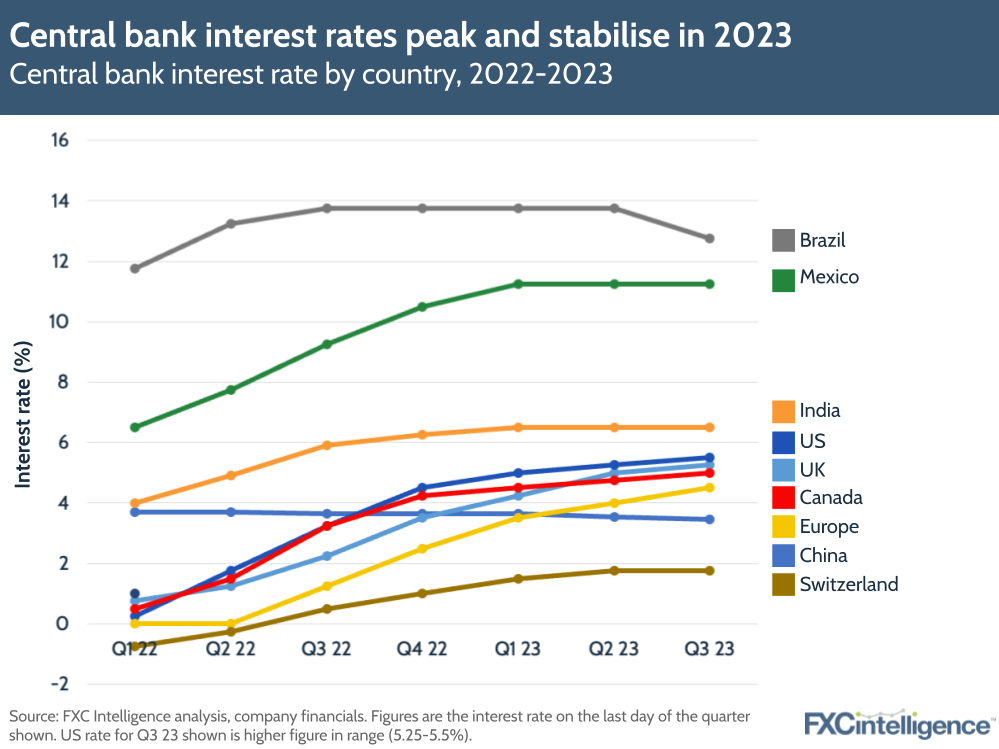

Comparing how central bank interest rates have changed over 2023 compared to last year shows that rates seem to be peaking out and levelling in some countries. At the start of November, for example, the US Federal Reserve said that it would be keeping its rate at around 5.4% after raising it just once since May, compared to multiple hikes last year. Having said this, the current rate is still the highest level in 22 years.

Inflation has dropped in some countries, particularly the UK and the US, which has led to the pause in interest rate hikes, but they could stay high for some time. The UK, for example, saw inflation fall sharply to 4.6% in October – down from an 11% peak in 2022, but still above government targets of 2%. Some have speculated, however, that the Bank of England’s current interest rate of 5.25% could stay the same until well into next year.

If rates do go down eventually, the question then is what this would mean for Wise, which has seen a significantly higher adjusted EBITDA margin as a result of higher interest income from higher rates, but doesn’t want its earnings to depend on this income. To mitigate this, the company has said that it wants to use around 1% of interest income to ensure it meets or is above its 20% EBITDA margin target, and then share back up to 80% of the remaining interest with customers.

However, as Wise is not currently licensed as a bank, it isn’t allowed to pay this amount of interest back to customers under UK law. The company has been in discussion with regulators about this, but unless Wise becomes a bank or the law is changed, it will likely continue to see an impact from interest rates on its profit margin, which it has guided for in its FY 24 outlook.