A broader customer proposition allows neobanks and payment companies in the cross-border space to increase their revenue and acquire and retain customers. Core banking services (savings and lending) has traditionally provided a significant regulatory burden, which was a good enough reason to keep most of these products on the sidelines.

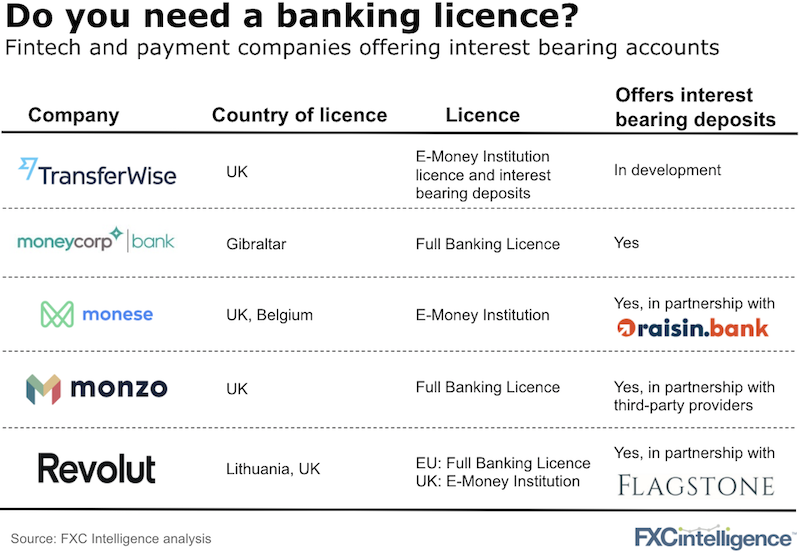

TransferWise seems to be taking advantage of a regulatory market opportunity. Last week, the company announced it has obtained new licences from the UK Financial Conduct Authority (FCA) to allow it to start offering interest bearing deposits for its clients in the next months, but without the need to become a fully regulated bank.

Our thoughts on this strategy:

- Avoiding the burden (and cost) of becoming a formal bank

TransferWise wants customers to be able to decide where their balances sit and the company will not lend out funds through other products as traditional banks do. TransferWise would likely argue (as others in the space do) that with high quality tech-forward KYC/AML systems already in place, they are already adhering to many of the requirements (and costs) a bank does. Therefore, why not offer some banking products if you have the cost base anyway. - Filling a need to offer a savings product

TransferWise already has c.$2bn in deposits through its borderless account. Launching a savings product is likely to increase the number of users, but also the funds available to the company. The company will hope that adding a savings product adds to customer retention, although other than on price and lockup period, savings products are hard to differentiate. - Savings is a really competitive market in the UK

UK high street banks offer very competitive interest rates on saving accounts, unlike the US market where banks such as Goldman Sach’s Marcus easily and quickly gained market share against the incumbents. Even with the Bank of England’s base interest rate remaining at historical lows, UK high street banks’ interest rates still range from around 0.5% to 2.5%. Beating these rates could be expensive for TransferWise. While a more competitive interest rate might also lead to more usage of its debit card for travel, it is not clear whether the company is currently missing out on smaller international payments from the same customers.

Expect more to follow in TransferWise’s path, especially if the FCA (and other regulators) continue to allow regulatory alternatives to offer banking products. Regulators generally like competition and open banking alone has not proved sufficient to pull large customer numbers out of their existing banking relationships.