This week, we declare that IPO season for cross-border payments is in full swing. Corporate and institutional player Argentex LLP listed on London’s AIM stock market on Tuesday. This follows Finablr’s listing last month.

Neobank Monzo raised another £113m as it sets its sights on the US market, and brings with its own white-label cross-border offering.

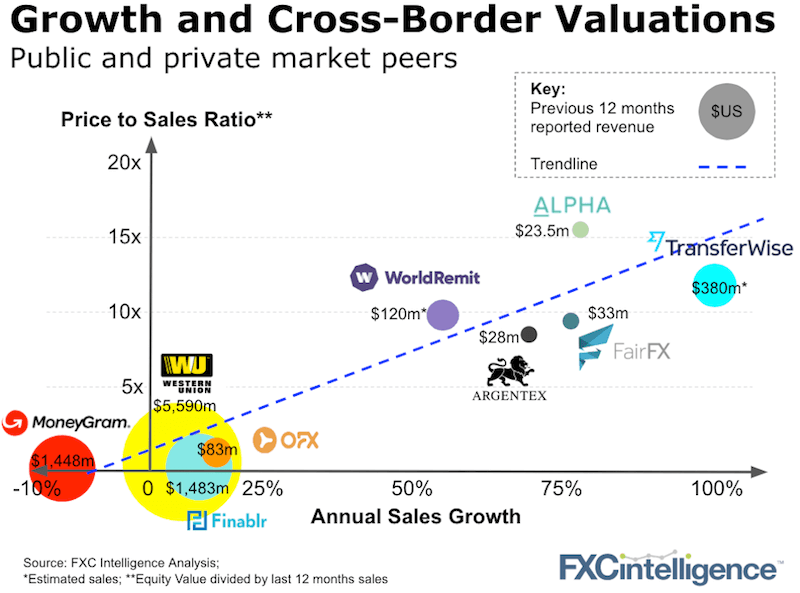

We were surprised by the lack of outliers across these valuation ranges, which provide some pretty clear guidelines for the sector:

The value of growth

As our analysis continues to show that growth is highly valued. If you can show growth and continue to grow, a strong valuation will follow.

For corporate focused players

In the highly fragmented corporate segment, the likes of Alpha and Argentex, albeit from smaller starting points, highlight the growth and value that can be attained with their singular focus.

For the consumer market

Greater consolidation and underlying single digit growth in the global remittance market makes for a challenging background to find double-digit growth. The high-growth players are valued accordingly.

Expect to see more companies added to this map over the next year as more players look to the public markets, either to raise funds or to exit.

Monzo enters the US market – but first raises another $144m to help

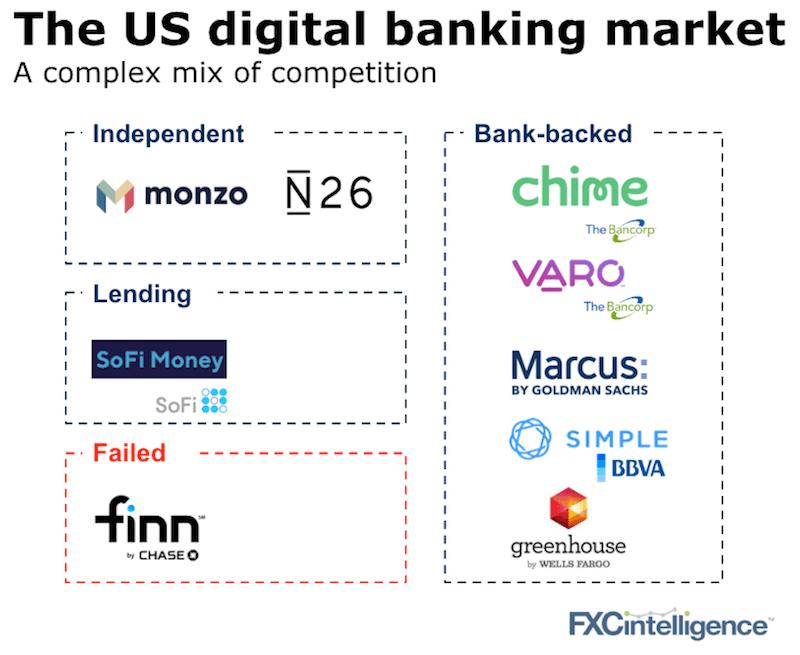

In 2010, 157 banks failed in the US. In 2018, for the first time since the 2008 crash, no banks in the US failed. With a now stabilised but still highly fragmented market, Monzo, the UK-based digital bank is finally crossing the pond bringing with it TransferWise’s white labelled cross-border product.

The US banking market is not for the faint-hearted. Competitors find themselves up against thousands of local banks and credit unions in addition to the big household names (Chase, Wells, Bank of American and Citi).

Competition comes from all angles. Big banks have launched standalone digital banking products but with mixed success. Finn, a bank valued at $350bn backed by J.P. Morgan, recently closed up. Simple, backed by BBVA has struggled to gain customers.

Marcus, on the flip side, has been one of the successes. It has so far brought in about $48bn in deposits and made $5bn in loans so far and recently entered the UK market. Wells Fargo and SoFi, two US financial giants have just launched products but the jury is still out.

Financial product virility does not drive success in the US as easily as it does in the geographically denser European markets. However good the Monzo product it, and an NPS rating of 80 backs this up, will a few hundred million dollars for an unknown brand be enough to win over the US market?

And how much will it use its cross-border offering to win over new customers since many of the players above have no international payments product?

[fxci_space class=”tailor-6332fde0095b7″][/fxci_space]