The US remittance tax, which sees a 1% tax applied to all cross-border money transfers initiated in cash, began to apply at the start of this year, but details of its implementation are still being finalised. In April, the Internal Revenue Service (IRS) and Department of the Treasury published details of their proposed regulations, inviting public comment on its clarifications and additions to the law. Now the comment period has closed, we take a look at some of the main concerns and changes requested by the industry.

The proposed Excise Tax on Remittance Transfers sees the original law that was passed as part of the One Big Beautiful Bill in mid-2025 fleshed out to include a number of additional details, elements and clarifications intended to make the law consistent and appropriate in its practical application. However, comments submitted on the proposed rulemaking highlight a wide range of industry concerns and calls for change.

Submitted by a range of trade associations, public interest groups, affected companies and individuals, the vast majority of the comments raise concerns with how the law is set to be enacted. Many requested specific granular clarifications or flagged concerns over the increased compliance burden for money transmitters, particularly those who transmit a relatively small number of remittances each month, such as some credit unions.

Meanwhile, many commenters also highlighted concerns that the law would disproportionately impact unbanked or underbanked individuals, or otherwise exacerbate economic inequality. However, there were also a number of concerns raised over specific details of the proposed rulemaking, particularly those introduced by the IRS and Treasury Department.

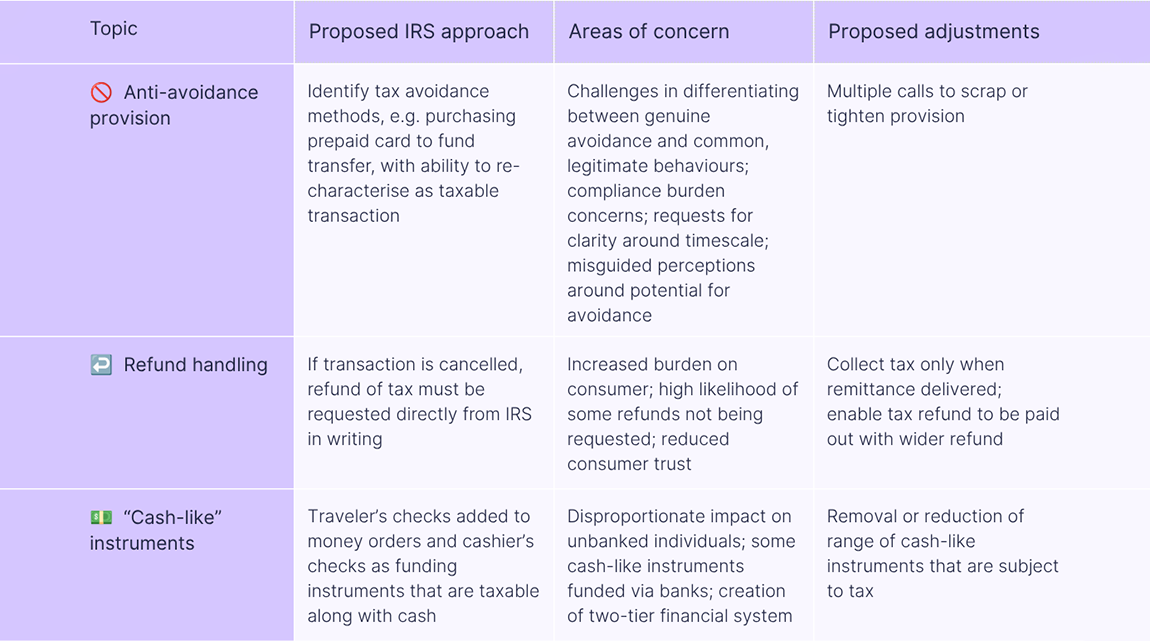

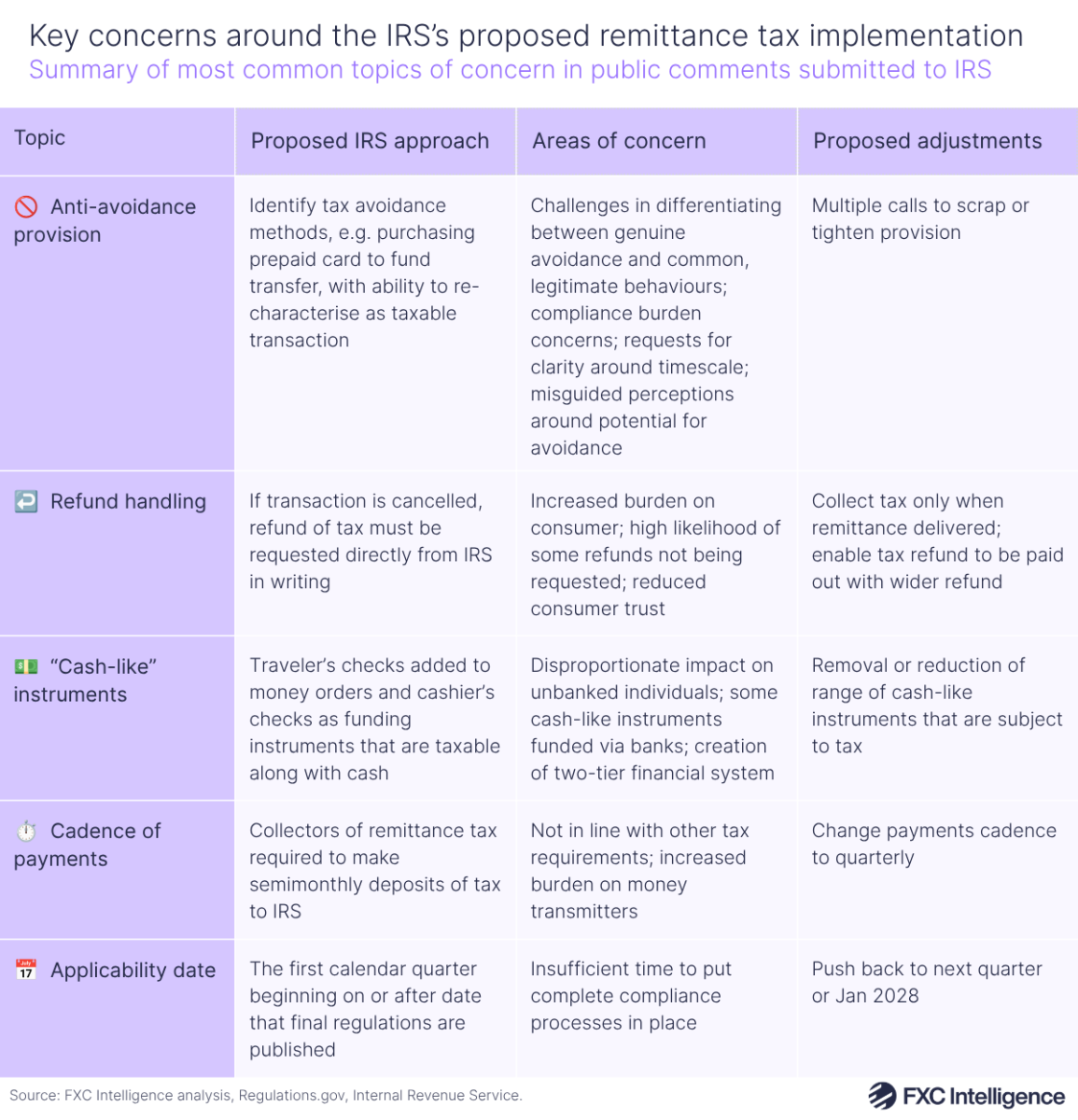

The most common topic is the planned anti-avoidance provision. This is specifically designed to tackle situations where individuals take actions to actively avoid the tax, such as by purchasing a prepaid card from the money transmitter before immediately using it to send a remittance. According to the draft, this would see the IRS reviewing “all facts and circumstances, including facts and circumstances relevant to a remittance transfer provider’s or third party’s pattern of conduct” and having the power to recategorise a remittance transaction so that it is subject to the tax.

Many commentators, particularly trade bodies representing money transmitters and other financial institutions, raised serious concerns about this provision, with this attracting more calls to eliminate or narrow it than any other part of the rulemaking. Several argued that concerns that prepaid cards could and would be used in this way were unfounded, partially due to KYC-related restrictions on using such cards for cross-border transactions, and highlighted significant compliance challenges relating to the provision. The Money Service Business Association, for example, highlighted that providers cannot reliably monitor the sale of prepaid cards by their agents, while America’s Credit Unions highlighted a need for guidance around timing thresholds for issuing prepaid cards to avoid falling foul of the law.

The handling of refunds in situations where a remittance was cancelled or otherwise failed to be delivered is the next most common area of concern. Under the law at present, the tax is collected at the point that the transaction is initiated, meaning that if it is then cancelled, the money transmitter cannot return the tax paid to the customer along with their send amount and transaction fee. Instead, the customer has to make a formal request to the IRS for the money to be refunded, an additional burden in terms of time and resources that many feel will cause customer frustration, reduce trust in the financial institutions involved and see unduly collected taxes fail to be returned to the customer.

Other concerns focused on broader issues related to the classification of some payment instruments as “cash-like”, including the disproportionate impact on poorer, unbanked individuals as well as questions over why cashier’s checks are being treated differently to other bank-linked payment methods.

There are also practical concerns for transmitters. The rulemaking currently proposes transmitters send tax payments semimonthly every half-month, which commentators said was out of step with the quarterly cadence of other taxes and created an unnecessary extra burden, while several organisations also requested more time to comply with the final ruling, given that it could apply with almost no notice once the final law was published.

Beyond these issues, there were also comments that echoed criticisms of the original law. Some raised concerns about a lack of alignment with broader policy objectives, while others requested exemptions for a variety of groups, including US taxpayers, military service personnel and churches.

With comments now closed, the next step will be for the Treasury and IRS to review these and form the final version of the law for the industry to comply with. There is no published timeline for next steps, however it is likely that the final regulations will be published by the end of 2026 or early 2027 – and we’ll share final details and which of the comments have been taken onboard once this is available.