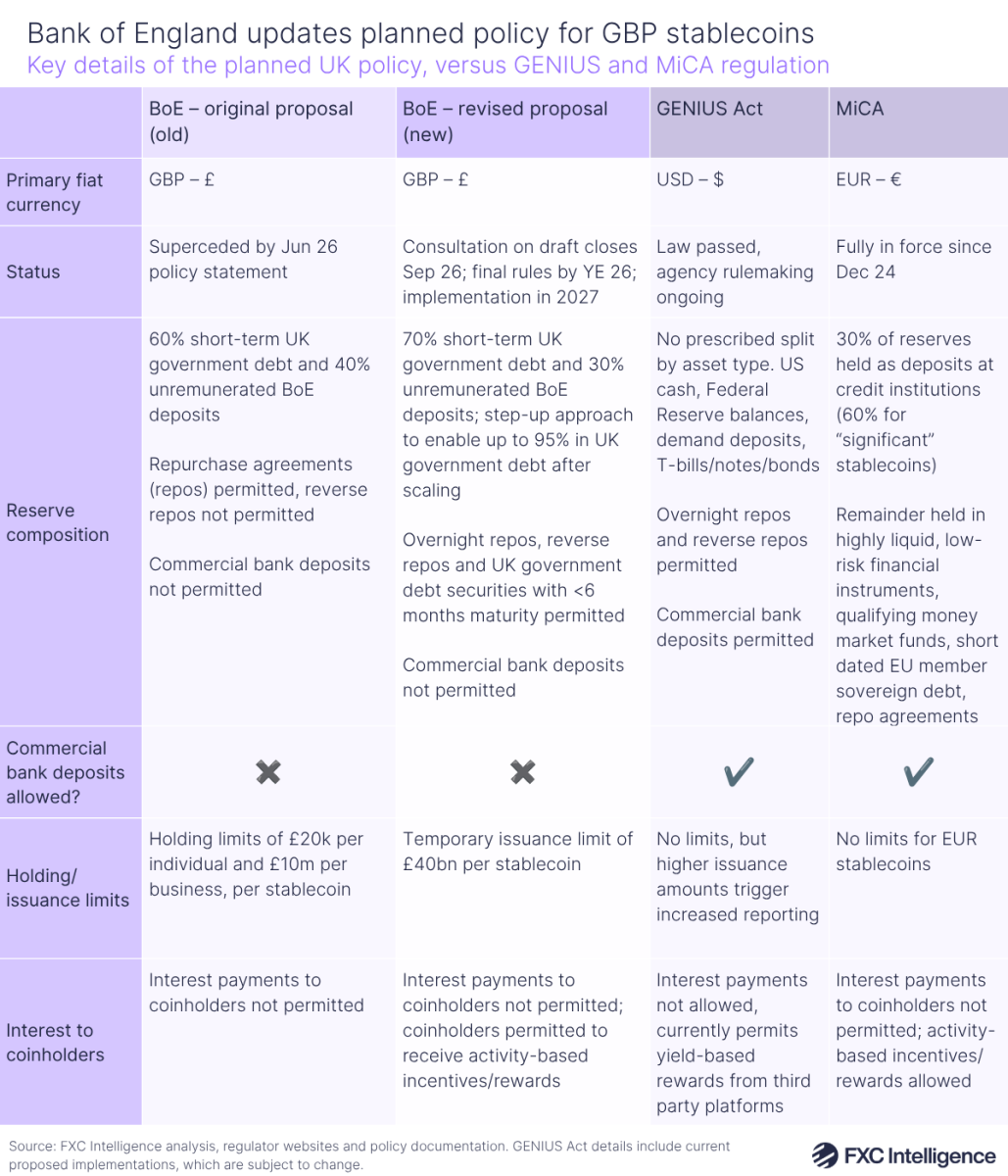

This week saw the Bank of England (BoE) publish a much-anticipated policy statement on what it terms “sterling denominated systemic stablecoins” – that is, GBP-pegged stablecoins for widespread use in payments, which will be jointly regulated by the Bank and the UK’s Financial Conduct Authority (FCA). An update of the original November 2025 policy proposal, this has undergone significant revisions in response to industry feedback, and while there will now be another round of consultation before it is finalised at the end the year, it is likely to be close to the final version.

The FCA will regulate areas around issuing, custody and approval to trade UK-issued stablecoins, as well as regulating their use in payments as policy evolves, and the BoE and FCA are also planning to issue a joint publication that will lay out how the two aspects of the UK’s stablecoin regime will interlink. However, the latest BoE update provides clarity on the Bank’s policy positions ahead of finalisation in late 2026.

The BoE sees GBP-pegged stablecoins as having the potential to play a significant role in the future payments landscape, and much of the policy and the adjustments have been made with this in mind. As a result, the institution is taking a “step-up” approach to some areas of stablecoin policy, by initially permitting relatively restrictive requirements before opening these as adoption grows and the landscape matures.

Despite this, many of the adjustments have seen the Bank loosen some of the more conservative restrictions, particularly around areas such as reserves, with the requirement for 40% of backing held in unremunerated BoE deposits now adjusted to 30% and reverse repos now being allowed.

However, this still makes the BoE policy more restrictive than Europe’s MiCA or the US’s GENIUS Act, as it does not permit funds to be held in commercial banks. As a result, the 30% held with the BoE cannot contribute towards an issuer’s reserve income – the single biggest source of revenue for many issuers.

Beyond this, the BoE has also relaxed initially highly restrictive limits around holding amounts, instead switching to a £40bn cap on issuance for a single stablecoin that is intended to be a temporary guardrail that will be removed once credit provision concerns are fully mitigated. No equivalent limits exist for other major policies.

In other areas, the BoE stance is largely in line with MiCA and GENIUS, including interest payments to stablecoin holders, bankruptcy protections and redemption rights, although the BoE has clarified its definition of “end of day” for redemption requests to be processed.

It is likely that some in the industry will still feel the policy remains too conservative, but it remains to be seen whether the BoE will relax it further ahead of its 2027 implementation. We’ll dig into the UK’s stablecoin policy further, including the roles of the Bank and FCA, when additional details are released.