Interchange fees are once again in the news, as a class action lawsuit against Mastercard and Visa related to the charges businesses face on received card payments has been given the go-ahead to advance in the UK. This isn’t the first time interchange fees have been the source of dispute in the payments industry; they were similarly the source of friction between Amazon and Visa a couple of years ago. But what are they, and why can they prove contentious?

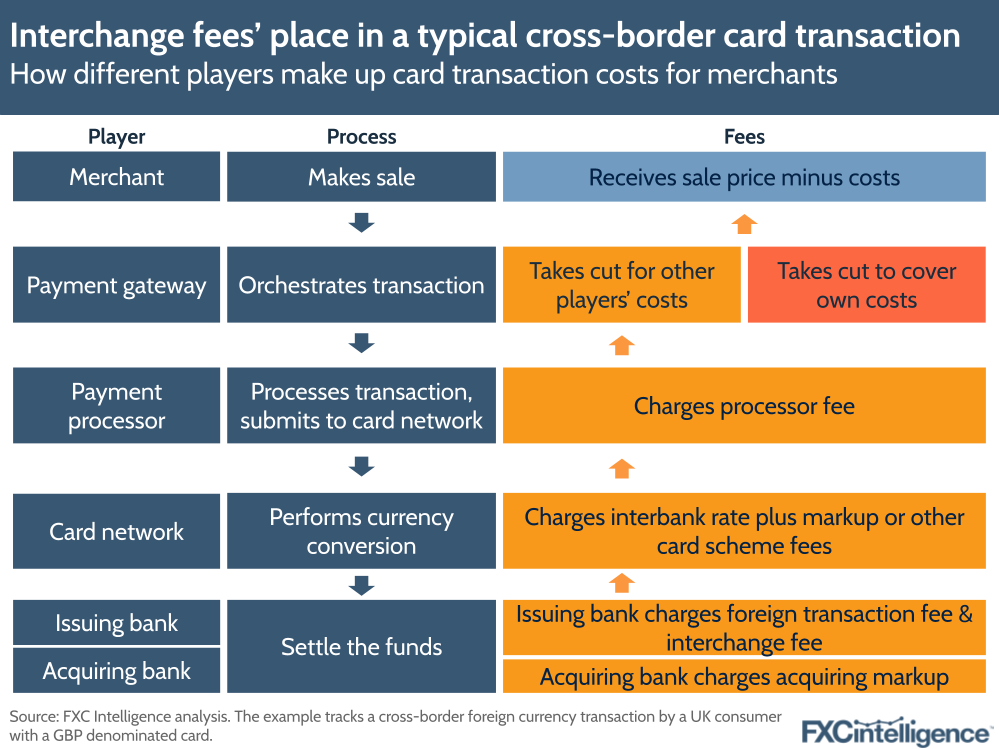

At the simplest level, interchange fees are one of three parts of the fees charged to a merchant for card processing, along with processing fees and card scheme fees. However, interchange fees make up the bulk of the charge incurred by merchants and, while not directly paid by consumers, may often be passed on through things such as FX margins.

These three fees are together often referred to as the Merchant Service Charge: the money paid by a merchant to their acquiring bank for both the card services and the technology necessary to process transactions. The processing fee, as the name suggests, is charged by the payment processor for processing the transaction – this could be a company such as PayPal or Fiserv. The card scheme, for instance Mastercard or Visa, then receives the card scheme fee for the use of their network.

Finally, there is the interchange fee itself. This is paid by the merchant’s acquiring bank, which holds a business’ account and accepts deposits from its sales, to the issuing bank, which provides the card to the customer, to cover a variety of costs and the inherent risk of approving a payment. Where things become complicated, however, is that while the banks are the recipients of these fees, it is the card schemes that charge and collect them on their behalf; more importantly, it is the card schemes that determine the rate of the fee in the first place.

The mechanisms behind multilateral interchange fees

There are in fact two kinds of interchange fees: bilateral and multilateral. The former is rarer, but sees an interchange rate directly agreed between an issuing and an acquiring bank. Theoretically, any merchant could negotiate such an agreement with their acquiring bank, but in reality this is impractical for all but the largest of entities. More commonly, interchange fees will be multilateral, in which the rate is agreed by multiple parties and payable between the respective payment service providers of the customer and the merchant.

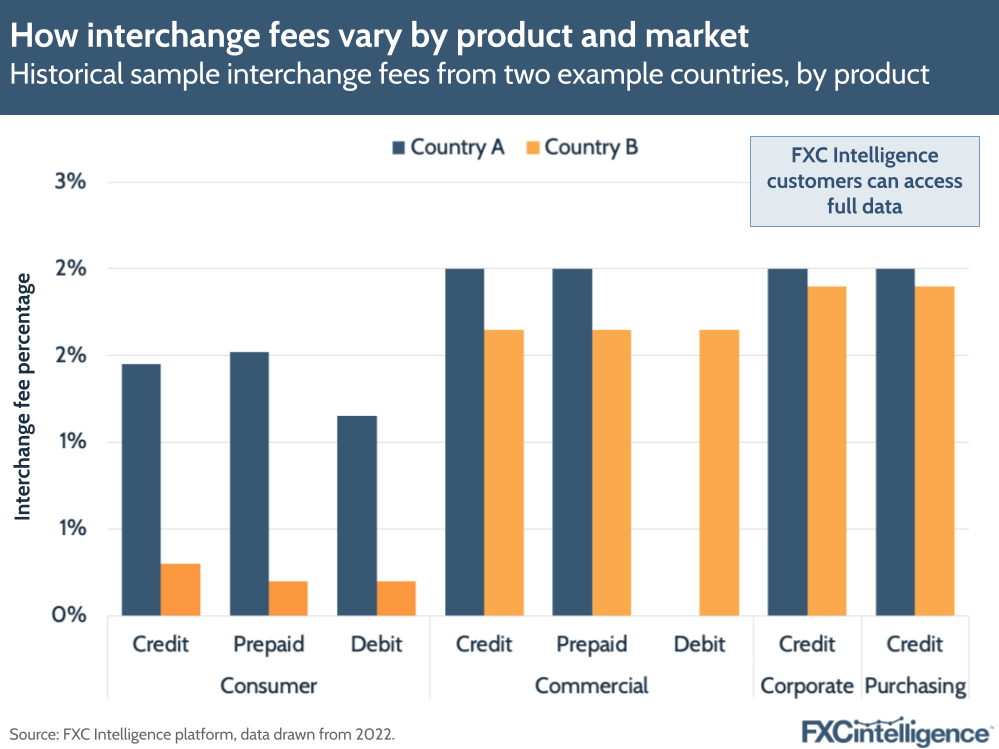

It is important to note, however, that interchange fees as set by card schemes are neither universal nor static. Visa and Mastercard set different rates for different regions, and publish updated rates in April and October each year (something not all other card networks do publicly). There are further factors that complicate interchange fees, with there being differences based not just on region or card scheme, but also what kind of card is being used to pay, whether the transaction is card-present or card-not-present, a merchant’s category code and whether the transaction is domestic or cross-border.

The European Commission has previously stated that interchange fees make up roughly 70% of the price merchants incur from payment service providers, however Stripe has estimated that it may be as high as 90%. Given this significant proportion, it is not surprising that merchants place such importance on the rates being set for interchange fees and why we are now seeing action on these merchants behalf to challenge what are seen by some to be prohibitively high rates.

How can I use cross-border card data to support my ecommerce strategy?