It’s been a stressful week for many thanks to the collapse of both Signature Bank and Silicon Valley Bank – although news that depositors will be fully covered has allayed significant concerns. However, there are still potential impacts to the payments industry ahead as both banks were heavily involved in payments.

While the biggest concerns surrounding the safety of customer deposits are now over, there are questions that remain and longer-term potential fallouts for the industry.

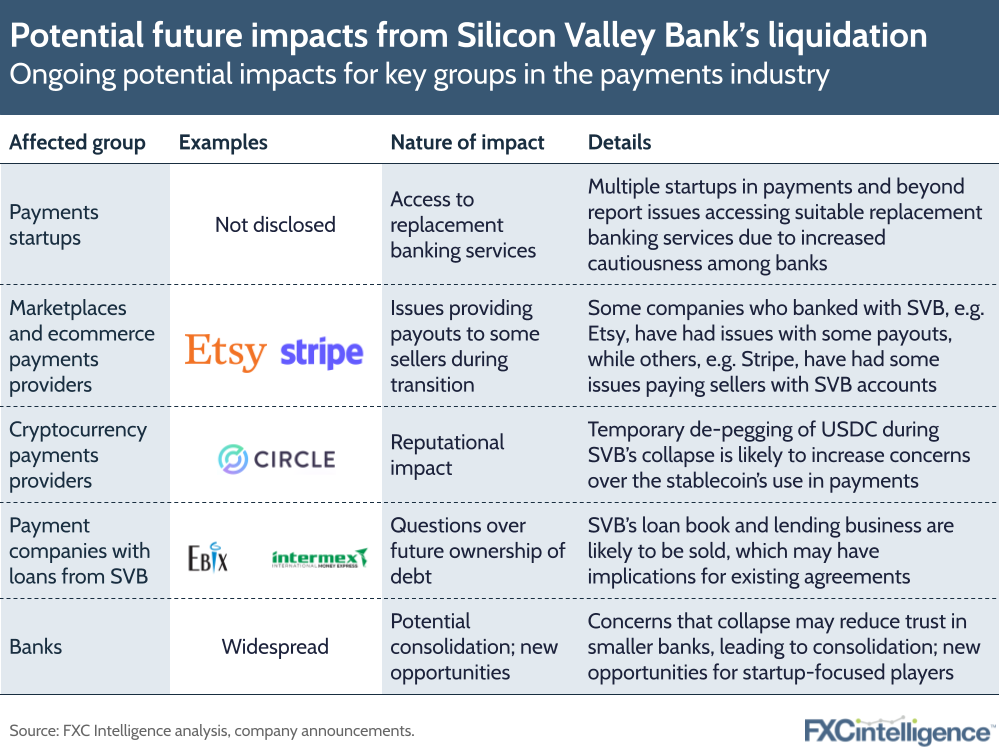

For payments fintechs big and small, many of whom banked with SVB, this includes the challenge of finding a suitable replacement bank, with multiple reports of issues with this in both the US and UK. A number of reports suggest that some startups are struggling to find a new bank as many are increasingly cautious about the customers they take on. However, there may also be an opportunity here for neobanks and other more recently established players in the cross-border payments space, with groups such as Wise, Monzo and Airwallex all catering to internationally minded businesses.

On the ecommerce side, meanwhile, challenges in shifting banks are having ongoing knock-on impacts. While Etsy, which itself was affected, is likely to resolve its delayed payouts to sellers shortly, Stripe and others continue to report some problems making payments to customers with SVB. For some, these issues have been developed into an opportunity, with Bill announcing a number of services aimed at bridging the gap while customers shift providers.

These issues are likely to be relatively short-term, but among cryptocurrency players the hit may be more subtle. Circle’s stablecoin USDC temporarily lost its peg over the incident, which is likely to shake confidence – particularly key given the past challenges other stablecoins have faced and the fact that USDC is used by a number of cross-border payments players, including MoneyGram.

Furthermore, it is not yet clear if there will be any knock-on impacts for those who had loans with SVB. This includes a number of payments players, with SVB listed as lenders in the public filings of Ebix, Flywire, Remitly and Intermex over the past year. The bank’s loan book and lending business are likely to be sold off, with private equity players Apollo and Blackstone among those expressing interest, and this may have some implications for those arrangements.

Finally, there are concerns that the event could lead to consolidation in the uniquely fragmented US banking industry. The incident, along with the collapse of Signature, has highlighted the potential (often unseen) risks of smaller or mid-sized banks, and may see companies increasingly looking to bank with bigger players only. But it would be unfair to only single out smaller banks. Credit Suisse, one of Europe’s largest banks, now needs the support of the Swiss Central Bank. Much change lies ahead again.