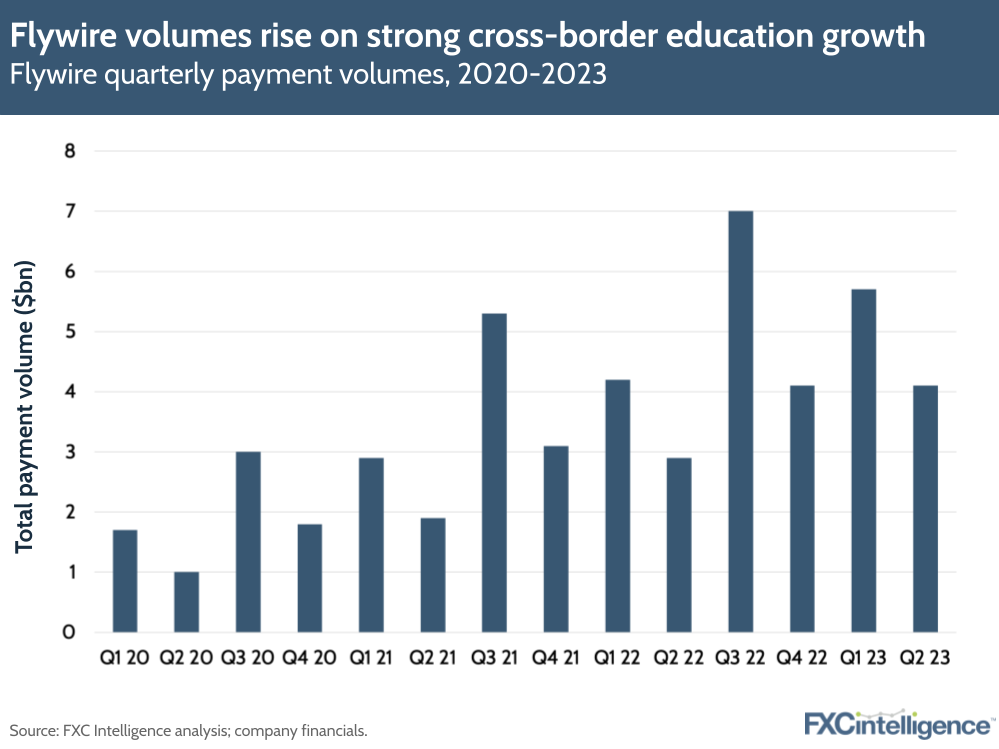

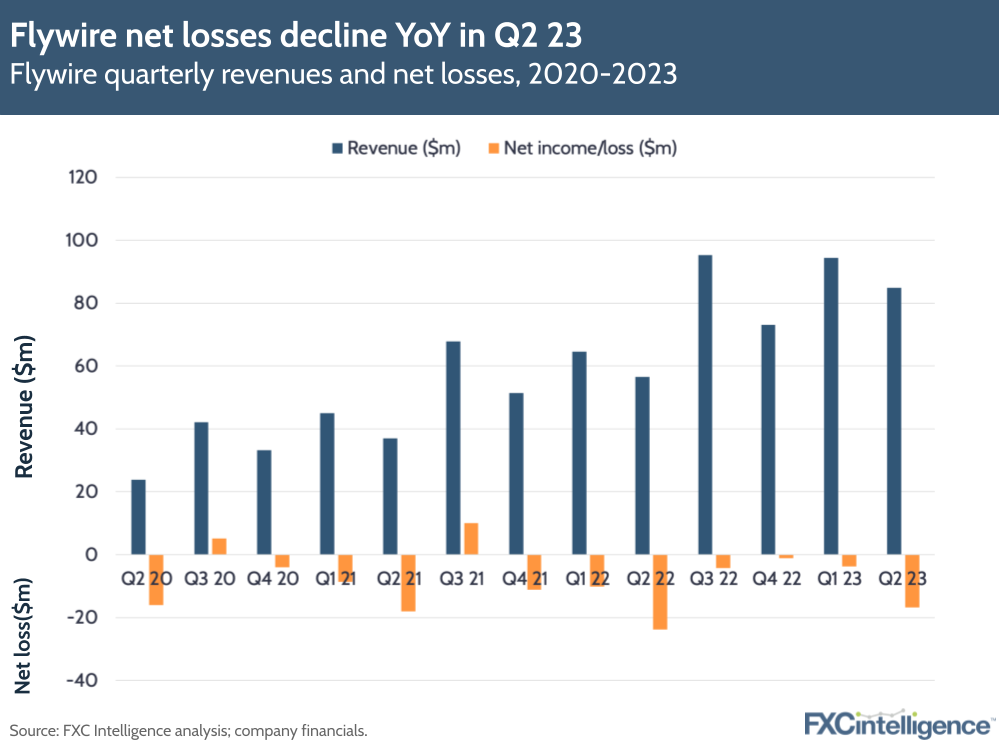

US-based cross-border payments provider Flywire had a strong Q2 23, with revenues rising 50% to $84.9m on the back of a 43% rise in total payment volumes to $4.1bn. Although just below 0, the company’s adjusted EBITDA margin rose compared to Q2 last year as Flywire managed to reduce losses, despite plenty of investments and activity – including a new partnership with Tencent to enable WeChat payments on its platform.

Flywire’s share price fell slightly right after its results, but the price is still up by more than 30% since the start of the year.

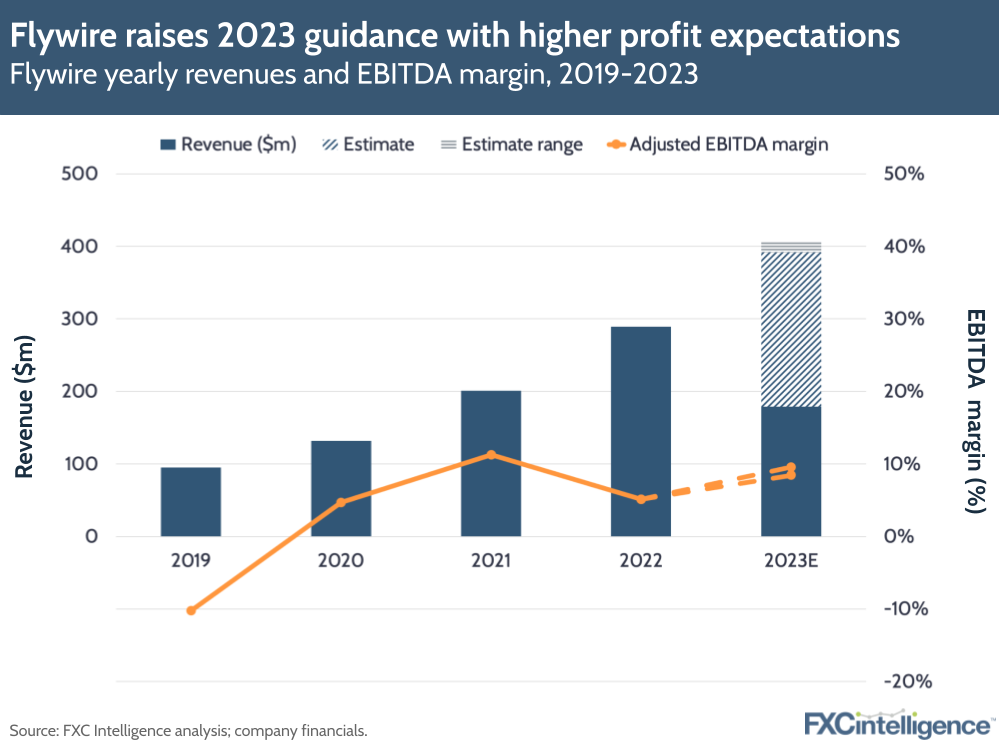

Driven by volume gains across its core segment focuses of travel, education, B2B and healthcare, Flywire has now updated its revenue guidance on the back of future confidence in its education and travel verticals, with revenues now expected to rise by 35-41% to between $392m and $408m, while adjusted EBITDA is expected to grow to $33m-39m.

Payment volumes rise on education, travel performance

Similar to previous quarters, Flywire linked its payment volume rise to strength in international cross-border payment volumes in the UK (expected to peak in Q3), along with higher volumes passing through Flywire’s travel clients at the start of the summer season.

Flywire continues to add new clients, boosting its total by 165 – to more than 3,500. Though the company didn’t break down its revenue and client split across its segments, travel and education remain its core revenue drivers and focuses – particularly as travel returns to the APAC region.

As discussed in our wider piece on education payments, Chinese and Indian students make up a high proportion of international students worldwide, and executives maintain that this is also the case within Australian universities – several of which Flywire has recently partnered with to enable payments. Flywire expects further gains in education for Q3, the predominant season for education payments.

On travel meanwhile, executives said that Flywire’s focus on destination management companies, rather than “small-dollar ecommerce for travel”, remained key to driving its success, as these companies seek out a more straightforward way to process card payments for things like luxury tours and accommodation.

On the other hand, Flywire’s B2B and healthcare segments were a much smaller part of the earnings discussion. This may be because Flywire’s B2B segment had a strong quarter in terms of revenue, according to Flywire COO Rob Orgel, but is growing from a much smaller base. Meanwhile, the company’s healthcare segment apparently had high gross margins, but isn’t growing as fast as other segments.

New partnerships highlight APAC focus

The company has launched new partnerships that reflect it’s interest in the APAC region: one with Tencent to allow Chinese students to pay fees using WeChat Pay; one with DISCO, a Japanese recruitment company with a network of more than 1,000 universities; and one to enable payments for account holders with the State Bank of India, following similar deals with India’s ICICI and HDFC Bank.

The Tencent deal in particular could have a major impact, with WeChat having more than a billion users and being a key part of the payments ecosystem in China.

Flywire also provided updates on its recent acquisitions of two other education payments players: WPM and Cohort Go. On the former, executives said that WPM client growth continued apace and has been primarily focused on cross-border, but the focus could switch to domestic in the future. Meanwhile high school payment volumes increased 50% as a result of CohortGo.

Investment costs and strategy moving forward

Flywire’s net losses were higher than the previous quarter, at -$16.8m, but substantially down compared to -$23.8m in Q2 22; net losses have consistently declined on a YoY basis for the last three quarters. The company also saw higher costs due to adding more employees, scaling up software to meet increased transaction volumes and a 44% increase in selling and marketing expenses.

Flywire expects delayed costs in the second half of the year (e.g. hiring and in marketing), which has reportedly been reflected in its guidance. However, it expects its travel vertical in particular to continue to perform well until the end of the year. While some companies have reported tougher comparisons for travel payments in Q2 since last year’s post-Covid travel boom (see Visa and Mastercard’s results), Flywire remains optimistic that it can continue to ride the wave of travel growth into H2.