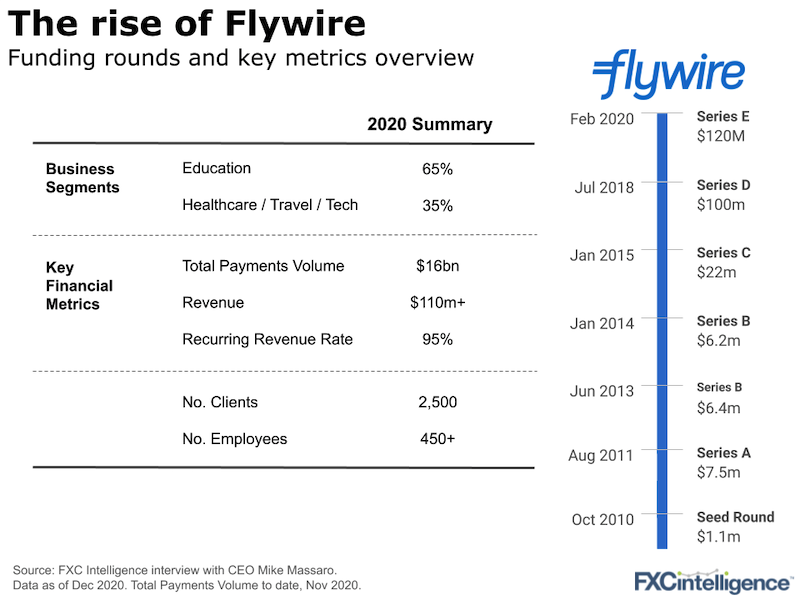

Some may have expected education-focused, receivables payments unicorn Flywire to have a tough year, but not so: the company, which has historically grown at 35-50% per year, still grew this year despite the pandemic. This week we spoke to CEO Mike Massaro to discuss the company’s journey through 2020 and its plans for the future.

Flywire’s growth levers

A number of key growth levers that have helped the company grow even through a challenging year 2020:

- Recurring revenue. The company has a sticky, mostly enterprise customer base with roughly 95% of its revenue this year locked in from these existing customers. The nature of its transactional business model also means that as the customer businesses grow – higher tuition fees; higher holiday spend – so does Flywire’s own revenue, a notion Mike refers to as “natural cohort growth”. We see similar patterns in payment processors serving the e-commerce sector, for example.

- Product expansion. Education was first, healthcare second, and now the focus is on travel and business payments segments in 2021.

- Geographic expansion. Flywire has clients paying tuition fees from 32 countries. Each market has local product development opportunities such as local currency support, which in turn attract more customers.

- New verticals. While most B2B payment companies provide accounts payable solutions, Flywire focuses on the accounts receivables side. Though originally a cross-border business, the company has been working on developing new domestic payment solutions, the opposite growth path to most players and a much more competitive segment. Bill.com and MineralTree (two leading payables players in the US) all started in domestic payments and then went cross-border.

Growth during Covid

With 65% of its business in education, this sector was critical, but the academic year saw some of the company’s Covid-19 growth driven by 2019. Furthermore, many students continued their studies remotely meaning tuition was unaffected, while others opted to defer to 2021. Travel, meanwhile, has been hit harder, but has shown resilience, with many shifting to domestic or regional travel.

Looking to 2021

Mike also expects a slingshot effect on revenues in 2021-22, from the many deferred business payments, new customers and higher university enrolments, particularly from countries with stricter lockdown rules such as Australia, New Zealand and Canada.

Flywire’s revenue and growth puts it in a position to be attractive to either the public markets or a strategic player. As Mike says, there are only three routes a venture-backed business can take, fail, be acquired or go public. Flywire’s choices are now down to just two of those options.