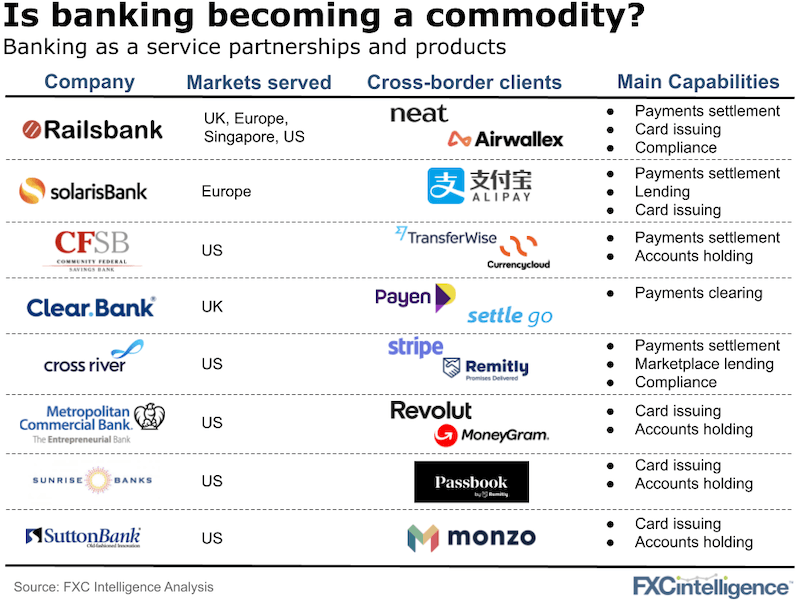

Being a bank can be a pain in the ****. But sometimes (not always) you need to be a bank to offer certain products. Over the last few years, banking as a service (BaaS) has emerged as an offering serving many of the biggest fintech brands.

What’s all the fuss about? We talked to Nigel Verdon, Founder and CEO of Railsbank, one of the new banking “utility” offerings.

Our takeaways and some of Nigel’s thoughts…

- It’s all about speed and cost

Utilising BaaS has the obvious benefit of reducing both the direct costs of building a product yourself and the indirect costs of obtaining the necessary licences to offer the product. As many of the underlying products that BaaS offers are commodities (like making a payment or opening an account), the speed at which a product can be launched can be the key differentiator (something Nigel says Railsbank really focuses on). - Regulation hasn’t fully caught up with Banking as a Service

The Wirecard debacle has highlighted where regulators can really go wrong. BaaS clearly shows that the bars set to be a bank (which can take years to attain) can now be relatively easily passed on to fintechs “borrowing” the banks’ regulatory status. Within this, there is the question of whether many of the services being offered are really clearing services (as Nigel sees them and can be served by e-money licences which Railsbank has) or banking services (as some regulators or the banks might).

Currently, there are not clear cut regulations around products as a service and whether they are formal banking services or e-money services or can be both. And most importantly, there is a lack of regulation on how to deal with these products and their customers when things go wrong. - If open banking would have really worked…

…we wouldn’t need anywhere near the offerings of BaaS. But as Nigel says, the regulators got it wrong focusing on encouraging the end consumers to demand open banking whereas it’s actually the banks and fintechs that need to build the products (using open banking). BaaS and companies such as Plaid have come in to fill that gap. - Let’s get creative

The cleverness behind TransferWise’s new investment product is that it creates a saving product (deposit money, earn interest) without it directly being a savings account. It looks like one, has the core benefits of one, but isn’t one – and therefore TransferWise’s doesn’t need to be a bank or borrow any banking licences.

We definitely expect to see more of this creative product development – something that looks like a banking product, but isn’t one. The fear factor – what happens if it goes wrong – is what will still keep people up at night though.