This week, Remitly held its first investor day since its 2021 IPO, in which it frontloaded the company’s shift to focus more on higher-amount senders and SMBs, driven by new and recent product launches. This is part of its evolution from being a low-value remittance provider to being a full-fledged, multi-product cross-border financial services platform, and the announcements were welcomed by investors, driving Remitly’s share price up by 13% by close of the day after the event. Below, we’ve mapped out some of the key takeaways from the event.

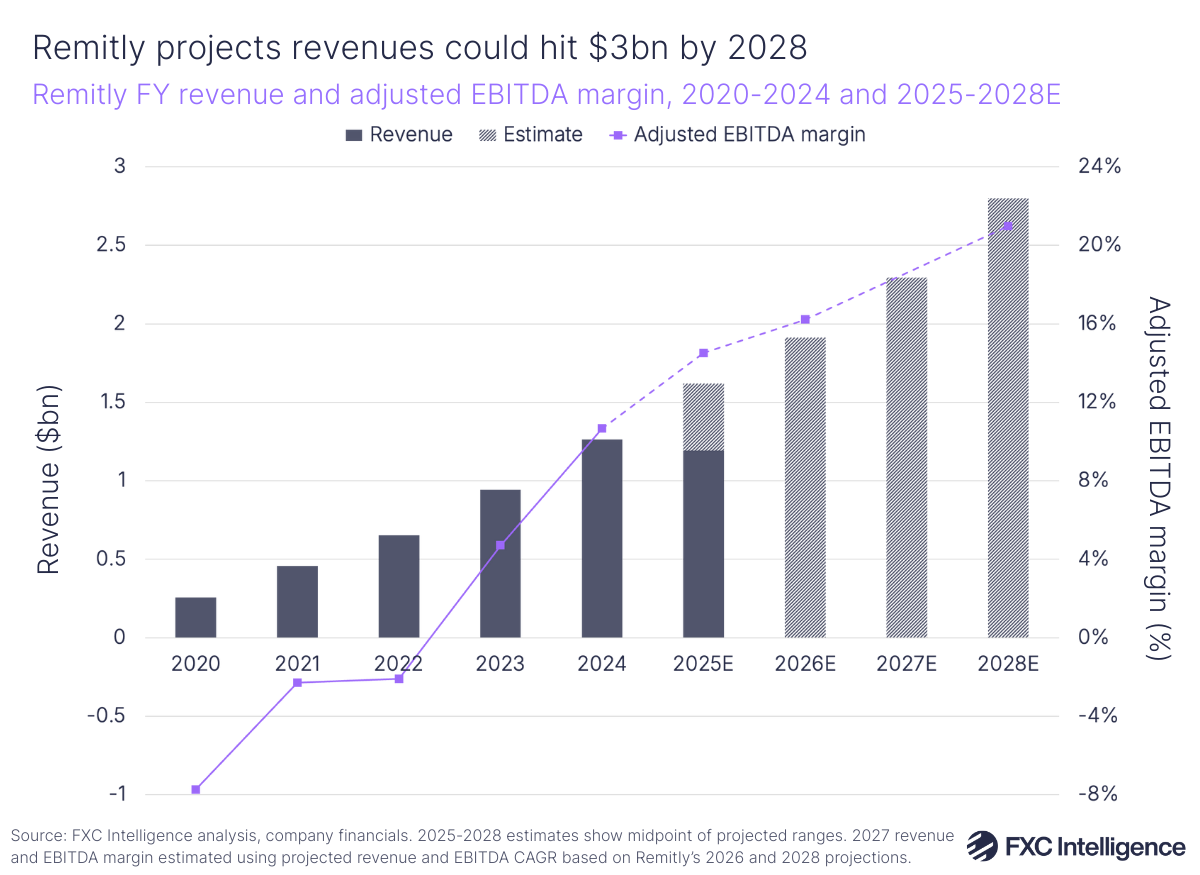

Alongside its Investor Day, Remitly projected revenue growth in the high teens for 2026; assuming it meets its FY guidance for 2025 ($1.6bn) this would be around $1.9bn – alongside an adjusted EBITDA between $300m and $320m.

In 2028, the company expects revenues in the range of $2.6bn-3bn, with adjusted EBITDA between $575m and $600m giving a 20-22% adjusted EBITDA margin. Considering Remitly’s negative margin in its IPO year, the substantial rise in its EBITDA margin reflects how it continues to mature and achieve stronger value from its customers as it continues to reduce costs across transactions.

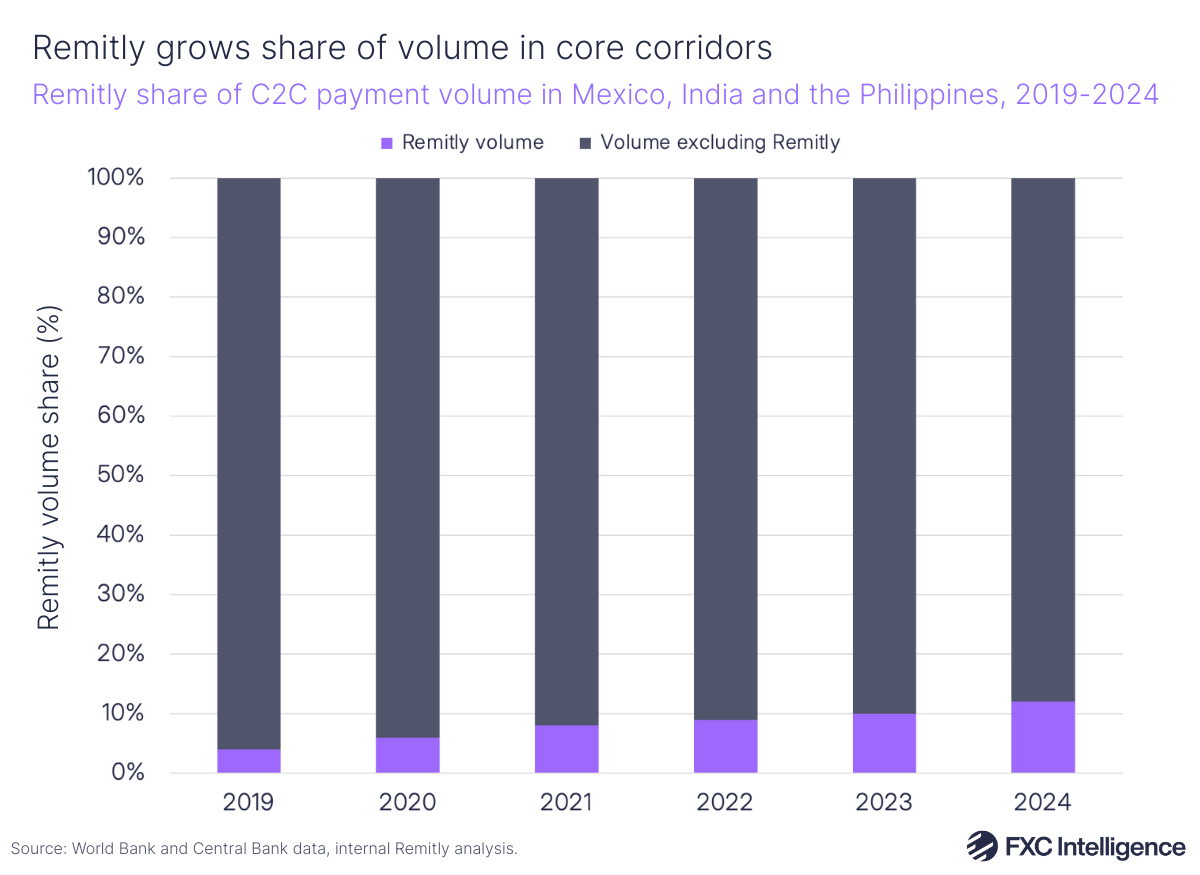

Despite seeing some of the strongest growth out of digital money transfer players, Remitly still sees plenty of opportunity to grow. Based on the company’s own assessment of the global C2C cross-border payments market, it believes it currently has a 3% share of the overall market. Meanwhile, it has grown its share of C2C volumes sent to Mexico, India and the Philippines (what it defines as core corridors) from 4% in 2019 to 12% in 2024. Underpinning this is the company’s growth to 8.9 million quarterly active customers in Q3 2025, spurring send volumes of $70bn and $1bn in revenue less transaction expenses (which Remitly sees as its key metric highlighting scale over time).

Remitly shifts focus to higher value transfers

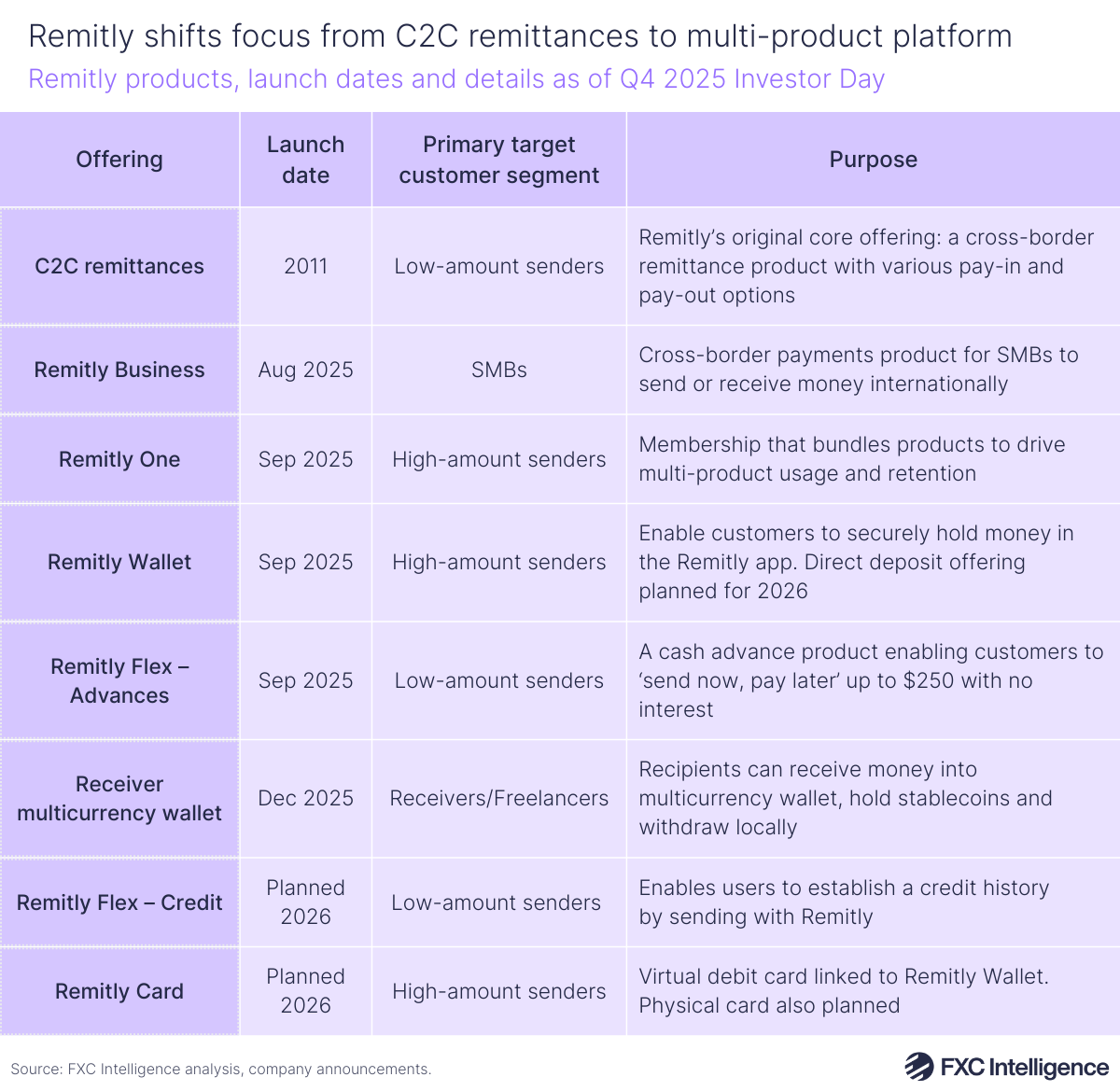

Data-led customer acquisition continues to be one of Remitly’s key strengths. However, it now wants to take its network further to increasingly support higher-value transfers (defined as >$1,000), which currently make up nearly half of its monthly send volume. Such higher-amount senders also have a higher lifetime value to customer acquisition cost ratio and the company claims to see “lower competitive intensity” in targeting these customers, with Remitly Chief Business Officer Pankaj Sharma saying that “hardly any banks” are currently prioritising them.

In particular, Remitly is increasingly aiming to capture SMB flows with Remitly Business, through which businesses pay employees, contractors and suppliers using Remitly’s cross-border payments network. This product exposes Remitly to a $20.2tn opportunity, the company said, citing FXC Intelligence Market Sizing Data. Though the number of businesses Remitly currently serves (over 10,000) is small compared to its personal customers, businesses send transactions that are twice as big and Remitly Business customers also have a higher lifetime value.

Remitly’s new product-led approach powered by stablecoins and AI

This combination of driving greater value across customers underpins Remitly’s growing product set, which in 2025 saw numerous additions aside from Remitly Business. Pivotal amongst these is Remitly One, the company’s membership option, which unlocks access to Remitly Wallet as well as Remitly Flex, its send now, pay later product. The company continues to extend these products, adding new receive capabilities to its wallet targeting freelancers this month and discussing enhancements that will boost Flex and its international card product in 2026. These products continue to target customer retention, which is key to Remitly extracting more revenue while also keeping its acquisition costs down.

Alongside these developments, Remitly is pitching stablecoins and AI as operational enablers for the company’s platform. Ankur Sinha, Chief Product and Technology Officer, said that Remitly’s “partner-first” approach to stablecoins is improving its treasury operations and helping reduce the amount of working capital locked up in prefunding payments. This is leading to incremental improvement in FX spreads, which Remitly expects to get better over time as liquidity pools evolve for digital currencies, and it says it will continue to pass on FX savings from treasury operations to customers. It also wants to enable disbursement in stables, and plans to expand its wallet from the US to more than 80 countries globally, allowing users to hold and move stable currencies.

On AI, agentic AI has already created actionable results for Remitly, which reported that its virtual assistant was now handling 30% of all chat contacts and was on average four times faster at resolving issues, while it is also powering the company’s WhatsApp and Messenger money transfer services to streamline more convenient payments for consumers.

Moving forward, Remitly hopes its core growth and gaining share across both low and high-value senders will continue to drive profitability moving forward, while it expects to see 5-10% of its total revenue from new products by 2028. Its moves to diversify and use its platform – alongside innovations in stablecoins and AI – reflects actions by other maturing digital players as it seeks to address a much wider total addressable market.