Hikmet has been CEO of Western Union (WU) for 10 years and has seen the latest round of remittance focused fintechs emerge around him. Western Union as a whole has been around for 170 years – it’s seen most technologies and competitors emerge around it and has adapted to the majority of them.

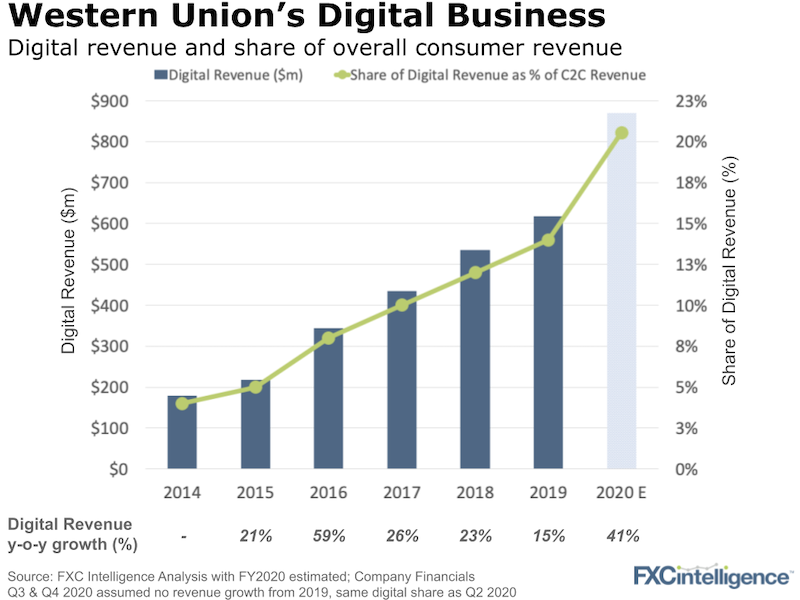

The latest trend in the sector, spurred on by the pandemic, is the rise of digital. Where does Western Union, with the largest digital business by revenue in the space, fit in to this latest development?

Definitions are important. WU’s overall digital business counts any transaction that is initiated on web or mobile as digital (with the most common digital flow being debit card pay in to cash pay out). This is a similar definition and customer to MoneyGram but contrasts with other players who may be entirely digital at both send and receive (TransferWise) or mostly digital send and receive (WorldRemit & Remitly).

Some initial insights from my discussion with Hikmet…

- Western Union has a two-fold data advantage

The first is the breadth of data, which comes from the critical mass of consumers spread over more corridors than any other player. Second, it has history. It is the only player in the sector that has been through 32 recessions in the US. WU is investing heavily in data, especially in terms of dynamic pricing, customer behaviour and fraud prevention. - Western Union’s cash payout network is unique

We’ll dig into more of this in future pieces but the vast proportion of WU’s digital business involves cash payout. That means if you have some of the best payout locations worldwide (think post offices, supermarkets and banks), you have a product edge above and beyond the widely offered account to account. - Scale comes with costs as well as benefits

Hikmet’s magic number is $300m of revenue. When a competitor reaches this size, they begin to face a different set of challenges. This level of scale means market share in multiple countries is enough to get the regulators’ attention. KYC/AML requirements can go up, meaning costs go up. (Note: TransferWise is now above this level and we covered their operating margins recently).

Which takes us back to: what should Western Union, a money transfer business with a run rate coming close to $900m of digital revenue but flat overall revenue growth, be worth? That’s a big question. You’ll have to be patient and wait for what we have coming in the weeks ahead.