Last Thursday, central bank leaders from across the G20, as well as representatives from key cross-border payments institutions, met at the Bank of England in London for the Financial Stability Board (FSB) Payments Summit. The third of its kind, although the first to be held in-person, the event saw leaders discuss performance against the 2027 targets of the G20 Roadmap for Cross-Border Payments and what steps need to be taken by both public and private sectors within the industry to bring about future improvements for the industry.

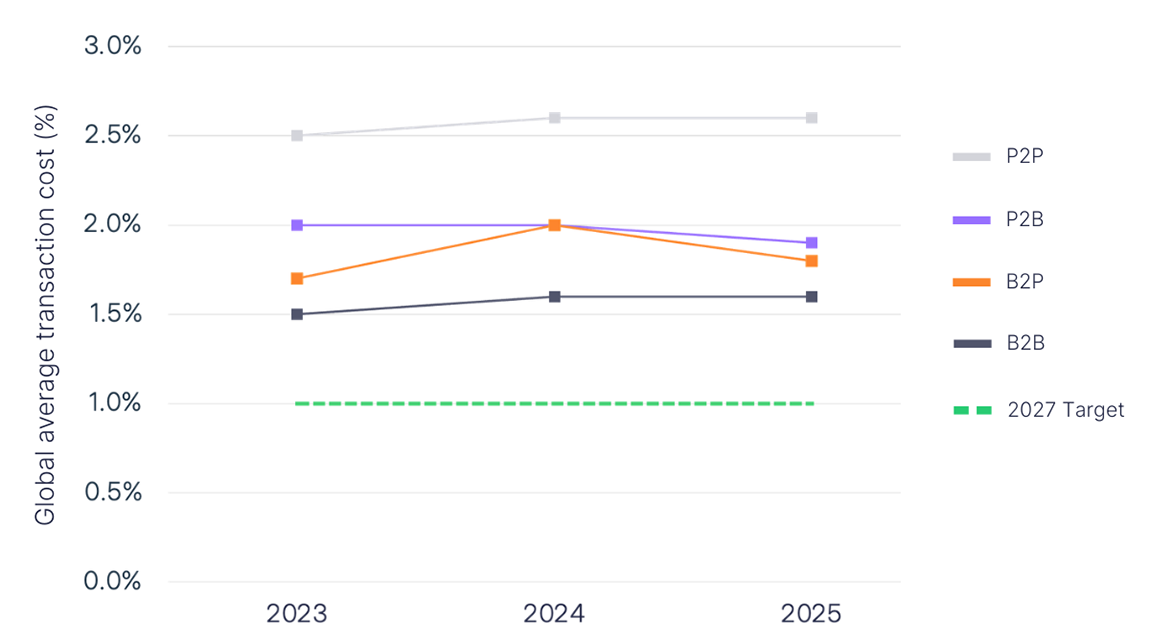

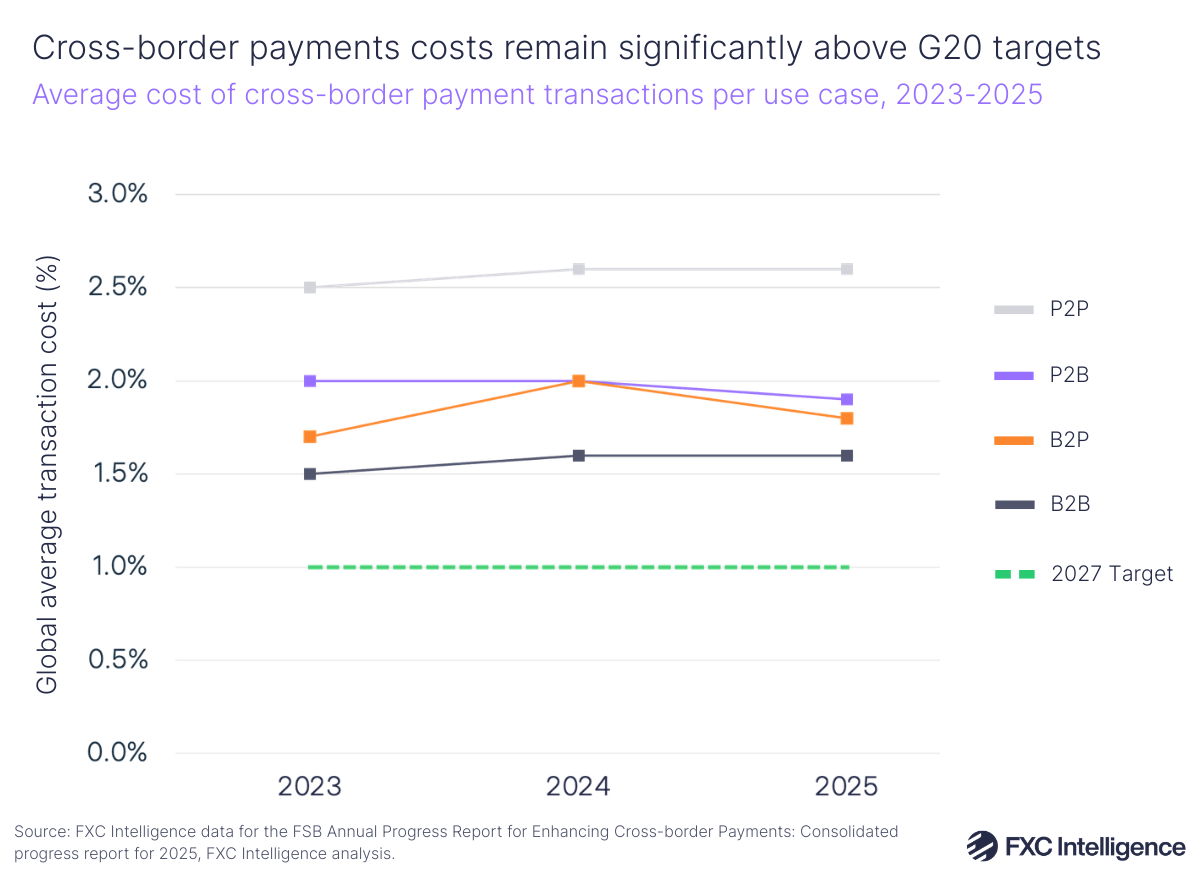

The latest progress report on the G20 Roadmap, which was published in October and includes extensive data provided by FXC Intelligence, showed that the industry is unlikely to achieve its 2027 targets. This includes global average costs of retail cross-border payments being no more than 1% by the end of that year, as well no corridors having an average cost of more than 3% and 75% of all cross-border retail payments delivering funds within an hour of the payment’s initiation.

In his keynote speech at the Summit, Andrew Bailey, Chair of the Financial Stability Board, argued that five years on from the Roadmap “most of the priority actions identified have been completed”. He cited harmonising ISO 20022 requirements, extending real-time gross settlement (RTGS) operating hours to increase the overlap of time zones and a revision of Financial Action Task Force standards around the information accompanying cross-border payments to support anti-money laundering and related efforts. The FSB also highlighted that Swift currently sees 75% of payments reach beneficiary banks in 10 minutes.

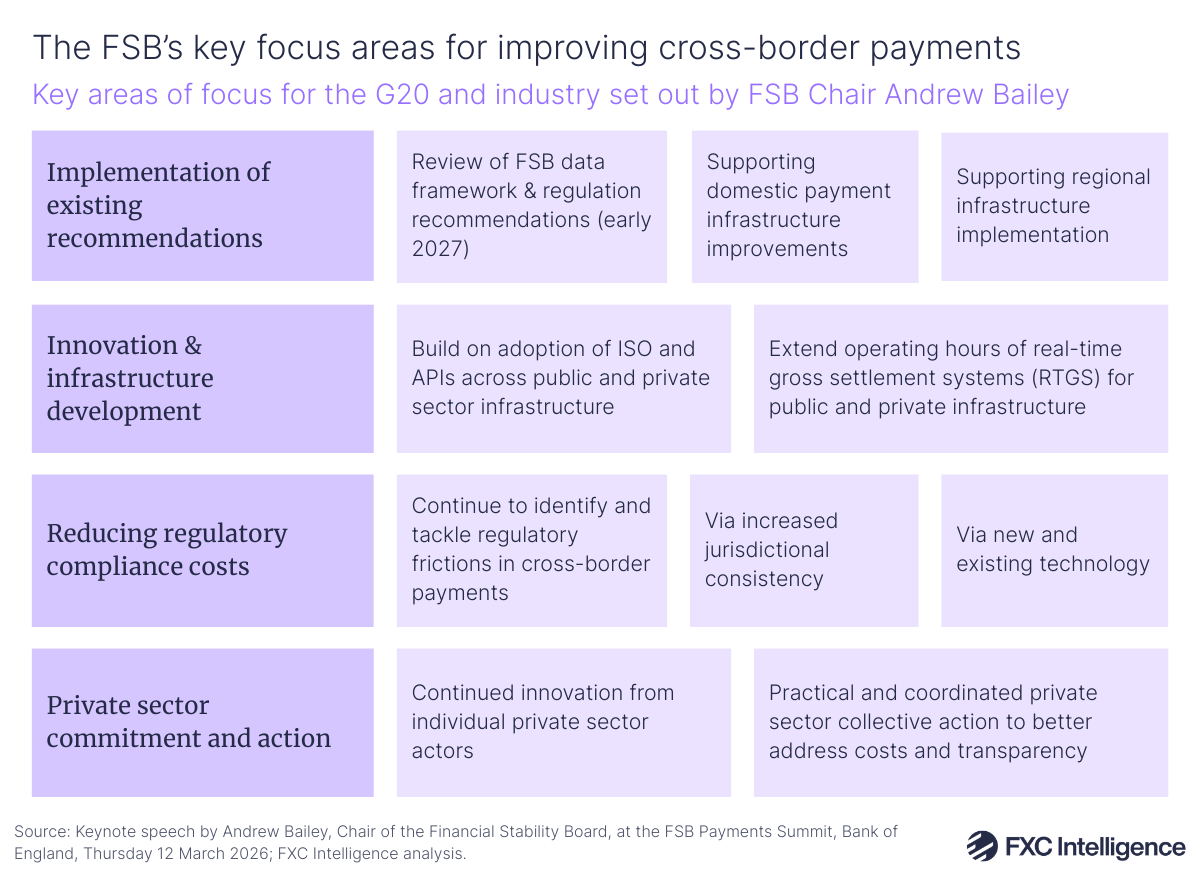

However, while he stressed that he was “hugely positive about the work done” and praised the industry for changing “things for the better”, Bailey also acknowledged that “we are far from reaching the targets the G20 set for 2027”. Characterising the industry as being at a “critical point”, he argued that there was a need to “intensify efforts” to improve speed, cost and transparency within cross-border payments, outlining four priority areas for the industry to focus on over the next few years.

The first has seen the FSB announce a review of the implementation of FSB recommendations around bank and non-bank regulation, supervision and data frameworks, which is set to take place at the start of next year, as well as the launch of a new implementation phrase that will call on both public authorities and the private sector to develop action plans to improve both domestic and regional payment systems.

Secondly, there is a continued focus on ongoing infrastructure development and innovation, particularly those that can deliver the biggest return on investment by capitalising on digital technology. Bailey stressed that this could be delivered by either the public or private sector and that the industry should “start by being open to how this is done” while “respecting the central principles of what is money” – likely a reference to ongoing sovereignty concerns relating to instruments such as stablecoins.

Supporting this is a focus on reducing the cost of regulatory compliance, without diluting the standards themselves. The Roadmap initiative has already identified areas of friction that are beginning to be tackled but the FSB sees greater potential in this area, citing the BIS’s Project Mandala, which has piloted the use of a common protocol to ease compliance with jurisdiction-specific policy.

Finally, Bailey argued that the private sector needed to not only show strong commitment, but to engage in coordinated collective action to build on the already strong efforts shown by many individual cross-border payments organisations.