In our latest post-earnings call, we speak to Remitly CEO Matt Oppenheimer about the company’s strong Q3 2022 revenue growth, its targeted approach to marketing and future strategy.

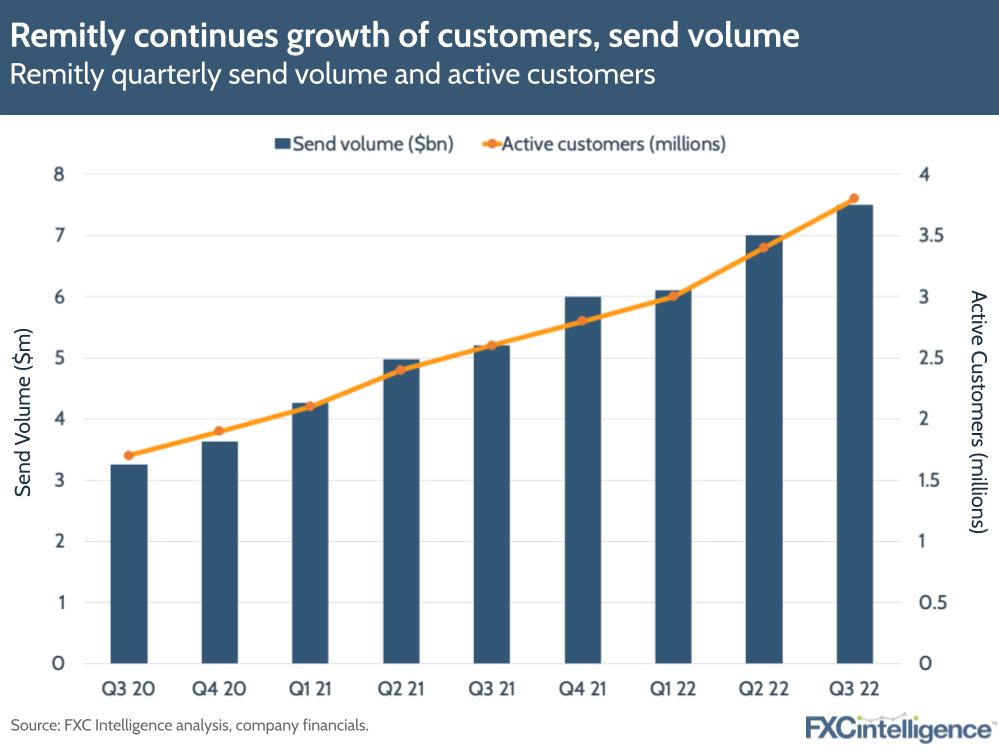

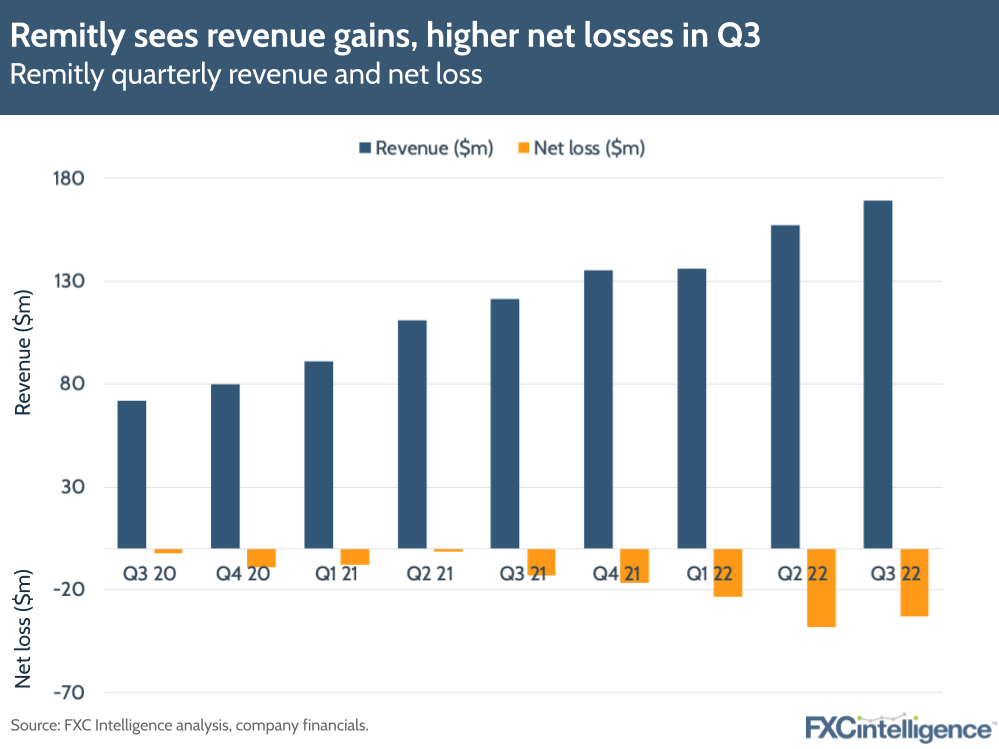

Money transfer player Remitly had another strong quarter, with revenues up 40% YoY to $169.3m in Q3 2022 as a result of customer acquisition and retention, as well as geographical expansion.

The company is continuing to build its customer base, with the number of active quarterly customers increasing 49%, to 3.8 million, since the company’s IPO in September 2021. Send volume increased 44% to $7.5bn, giving a take rate of 2.26% (slightly lower than the 2.33% in Q3 2021).

Since its IPO, Remitly has increased the number of countries it serves from 135 to 170 and the number of corridors served from 1,800 to 4,200. It now has more than 420,000 cash pickup locations worldwide, and provides services to more than 3.9 billion bank accounts and 875 million mobile wallets.

However, the question remains about how Remitly will convert customer loyalty into profitability going forward. Adjusted EBITDA was -$3.7m in Q3, giving Remitly an adjusted EBITDA margin of -2.2% (lower than 0.27% in Q3 2021). It also saw net losses rise to $33.1m, compared to $12.96m last year, while total operating expenses rose 53% to $205m.

I caught up with CEO Matt Oppenheimer to find out how Remitly aims to bridge this gap moving forward, as well as explore its approach to marketing, its upcoming acquisition of Rewire and much more.

Key factors driving revenue growth in Q3

Daniel Webber: It’s been another excellent quarter. What’s driving the continued growth in your top lines?

Matt Oppenheimer:

What’s driving it is two things. One: continued resilience of our existing customer base. That’s a reflection of the service we provide, and the fact that we provide unparalleled peace of mind for our customers. We provide a non-discretionary service and it matters a lot. People are sending money home for things like basic living expenses, and it matters even more when some of the emerging market currencies are depreciating. Customers can get more money home per dollar, per pound or per euro that they send. So, our base performing well is number one.

Number two: we added a record number of new customers at a lower customer acquisition cost (CAC). We reduced CAC by 18% quarter-over-quarter, and 19% year-over-year. That record number of new customers adds to our number of total quarterly active users and that flows down through revenue. So, we’re excited about the quarter and what’s to come.

Remitly’s analytical marketing approach

Daniel Webber: You have a big marketing spend, but you’re bringing in a lot of customers. How are you making your marketing more targeted and more efficient?

Matt Oppenheimer:

We tend to be pretty analytical in our marketing approach. There are factors in the external environment, such as the competitive advertising environment changing for digital channels that we market on. We’re able to test that quickly and efficiently in terms of the right customer acquisition cost to pay for each customer. Our marketing team is very strong right now, with a CMO that’s been in the seat less than a year and a team under her that is strong when it comes to creative velocity, creative execution and some of the levers that we can control in our digital marketing channels.

The last thing is the word of mouth effect, which is often underappreciated and it’s one of the advantages of scale. We have gone from 2.6 to 3.8 million quarterly active users since the IPO about a year ago. When you add that many new customers and you provide a great service, those customers are then telling their friends about Remitly. That’s part of why we’re able to not only add more new customers, but also do it at a lower customer acquisition cost and continue to improve quarter on quarter.

Driving customer loyalty and retention

Daniel Webber: Customer loyalty and retention goes hand in hand with the marketing piece. How do you go about retaining customers?

Matt Oppenheimer:

Our business comes down to trust, which can be somewhat difficult to build. Our marketing builds that trust with top of funnel, new customers, word of mouth and other things out there.

The retention of our existing customer base has been, and continues to be, very strong. We see that once we’ve built that trust, whether it’s across our great disbursement network where we do direct integrations; payment acceptance; a risk product, delineating between bad actors and good customers; treasury or FX products, all of those things create a much faster and easier to use customer experience. Because of that, customers come back again and again, and we’re continuing to see strong retention with our existing customer base.

Impact of the economic downturn

Daniel Webber: How are you thinking about the broader macro environment and how your customers are behaving within that?

Matt Oppenheimer:

As it pertains to remittances, there’s a lot of resilience because customers are sending money back for basic living expenses. It’s also resilient because, depending on your view of the economy and what will happen, currencies have depreciated in emerging markets. Those markets are at risk of some pretty tough economic times, and in those scenarios remittances are even more important. We’re going to be there to serve our customers and get money home to their families when it matters the most.

Thirdly, in the 20-plus markets that we enable customers to send from, there’s job mobility. For example, during Covid-19, a lot of our customers were hospitality workers. Restaurants shut down and hotels shut down, but because there’s job fluidity in places like the US, Canada and Europe, customers shifted to find other work (such as food delivery, for example). That’s a broader example of why we’ve seen remittances stay so stable during previous recessions.

It’s already still a tight labour market, but especially across blue-collar jobs, our customers are resilient. They have grit, they have tenacity, and they have historically shown that they will find work to be able to build a better life for themselves and their families back home. That’s what we’ve seen in customer behavior. We’re optimistic that we can help customers and their families as they’re sending money back home, regardless of what’s happening in the macroeconomic environment.

Creating profitability against marketing spend

Daniel Webber: When it comes to profitability, how are you thinking about the kind of scale that’s required versus your marketing spend?

Matt Oppenheimer:

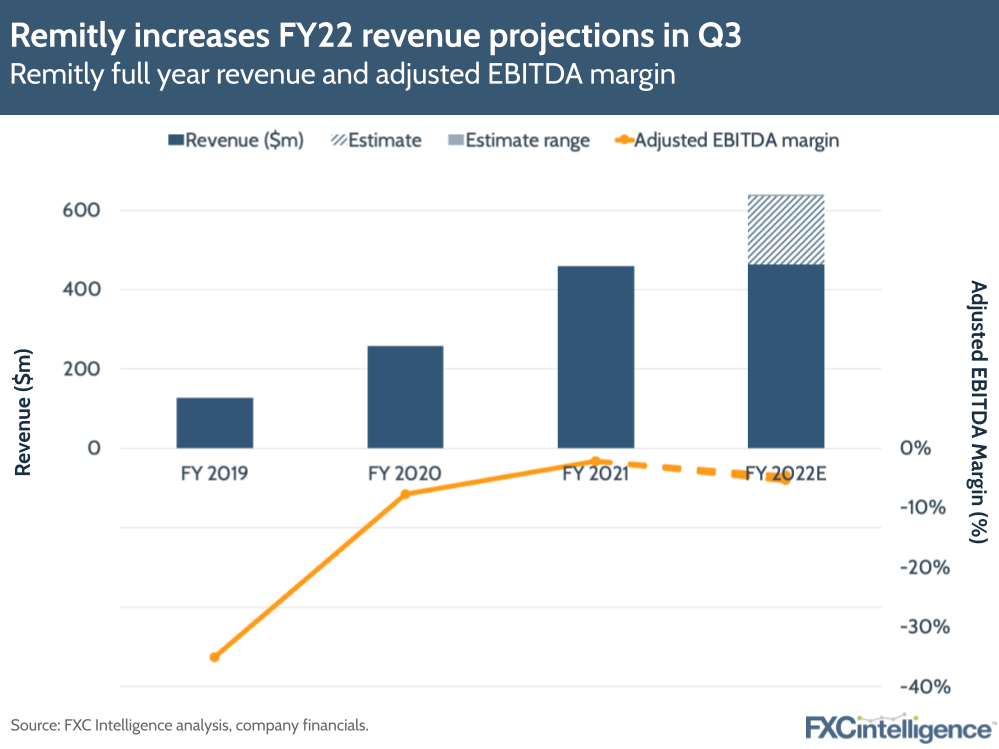

Both are important. Because of our strong performance in Q3, we raised revenue guidance, which we’re excited about. We beat our adjusted EBITDA on the bottom line in terms of expectations, and we maintained our adjusted EBITDA guidance for Q4. We did that because it’s a seasonally high time to acquire new customers and build trust in Q4 because a lot of people send money around the holidays.

That gives us a lot of optionality going into 2023 with regards to profitability and the increasing cost of capital. It’s something that’s on my mind and on our new CFO Hemanth Munipalli’s mind, so we’re excited about adding a large cohort of new customers at great unit economics in Q4.

We’ll be talking about profitability as part of our 2023 guidance and plan once we end the fourth quarter. We’re excited to have Hemanth as a partner to help us think through the path of profitability and what investments we’re making.

The importance of cash versus digital

Daniel Webber: You spoke about the reach of your cash pickup locations and also mobile wallets. Can you talk more about the importance of both?

Matt Oppenheimer:

Both are important, but it really depends on the market. Some markets continue to be more predominantly cash pickup, while some are bank deposits, some are mobile wallets and some are door-to-door delivery.

In markets like the Philippines, if customers want to shift from cash pickup to digital disbursement, then we are going to build the products, the customer experience and the packaging to be able to do that seamlessly with our platform. We’re excited about leading the digitisation on both the send and the receive side. Ultimately, we’ll meet customers where they’re at in terms of how they want to receive funds.

Rewire acquisition: Expanding into new geographies and products

Daniel Webber: What’s your strategy around your upcoming Rewire acquisition?

Matt Oppenheimer:

I just got back from Tel Aviv, where I met the Rewire team. The foundation for any good acquisition is a strong team and a strong culture, and I went to Tel Aviv excited. I came back even more excited.

The first strategic reason for the acquisition was the complementary geographies. We don’t originate from Israel yet. We will once we close that acquisition or once we get regulatory approval. It’ll help us in Europe, where they have a business that we can add to our existing European business.

Secondly, we’ve talked about complementary new products. They have a track record of innovation and a product portfolio that we’re excited about leveraging to continue our journey around complementary products to the core remittance business. We’re excited to close the deal, to get going on that once we have regulatory approval.

Remitly’s partnership with Visa

Daniel Webber: How are you continuing to work with Visa? Where do they fit into your business?

Matt Oppenheimer:

Visa Direct (and Visa more broadly) is a great partner for us. Via that partnership, we can get access to bank accounts across the globe that are linked to a Visa-branded debit card. Instead of the bank account number of the country they’re sending to, customers enter in their 16-digit Visa debit card number. Then we can deposit funds into that account quickly.

Remitly’s B2B strategy

Daniel Webber: What about B2B? How does that fit into your strategy moving forward?

Matt Oppenheimer:

We’ve talked about Remitly for developers, or RFD, which is the B2B product that we’ve partnered with Meta and Coinbase to launch.

Many businesses think they want access just to remittances and our disbursement network. But they then realise the complexity with remittances and international payments is a lot more than that. It’s also our UX, pricing, risk, product – all the things that we’ve talked about – then localising that across 4,000 corridors. We’re now offering an embedded B2B product designed for organisations like banks, credit unions and neobanks, to offer really simple and trusted international payments to their end customers, more fully leveraging our end to end platform.

Daniel Webber: Anything else you’d like to add?

Matt Oppenheimer:

You have to have a deep appreciation for our customers right now: their commitment to their families, work ethic, grit, resilience and flexibility when faced with headwinds. That’s why we grew so quickly in Q3. The foundation of that is our customers and the non-discretionary service that we provide to them, but it’s ultimately them that are sending money back home for incredibly important reasons. We’re just excited and honoured to be able to serve them, and that’s why we’re growing so fast at the end of the day.

Daniel Webber:

Matt, thank you very much.

Matt Oppenheimer:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.