In the latest instalment of our Post-Earnings Call Series, Remitly CEO Matt Oppenheimer shares his thoughts on success in Q4 and FY 2021, as well as his future strategy.

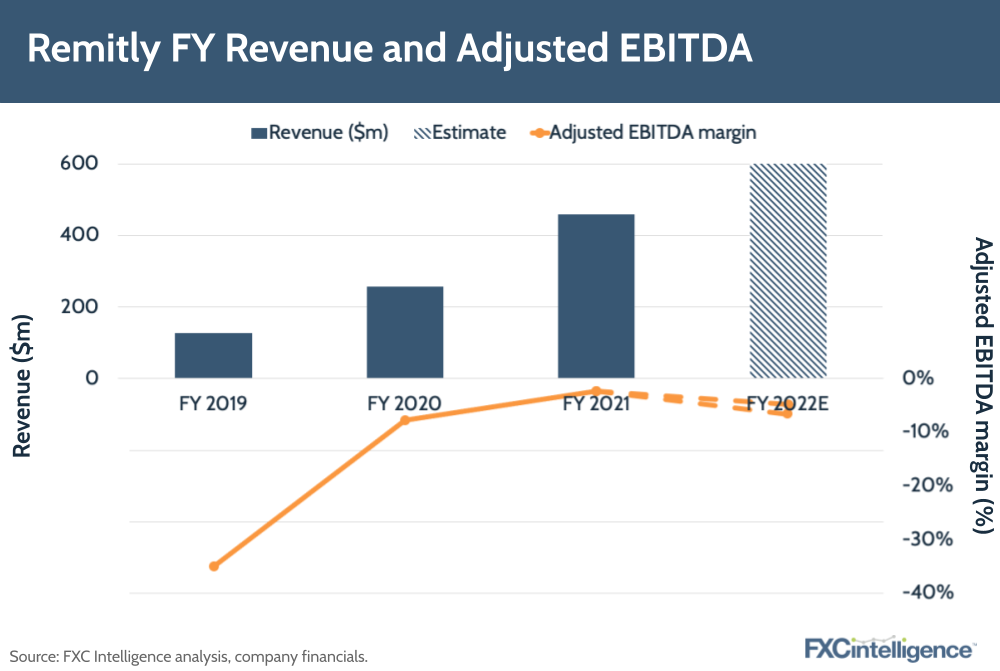

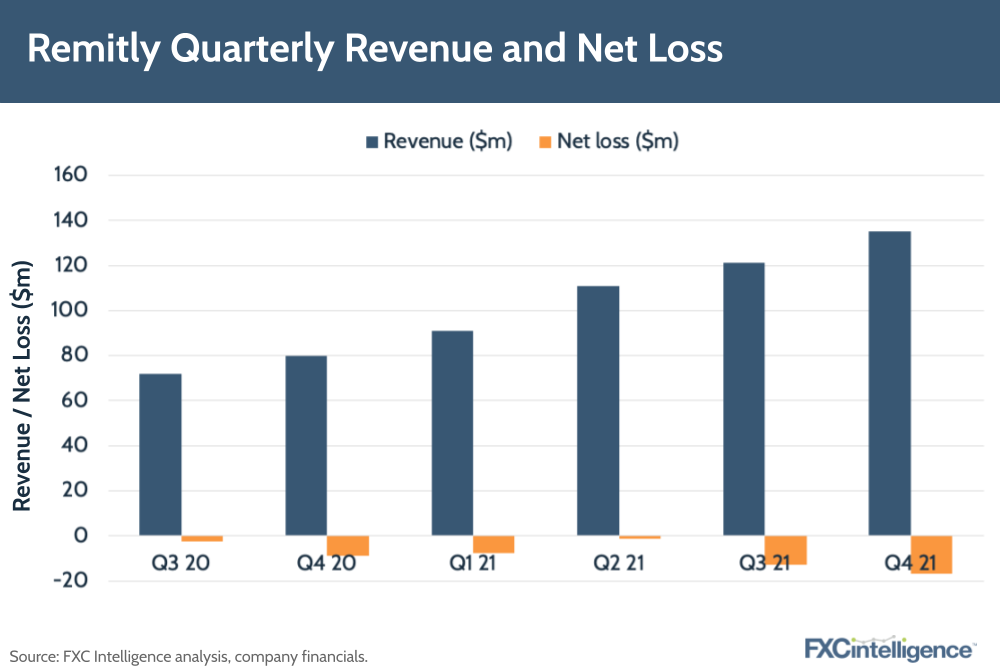

Remitly saw a 78% yoy revenue increase to $459m in its FY 2021 results, having rounded out its Q4 with a 69% increase to $135m.

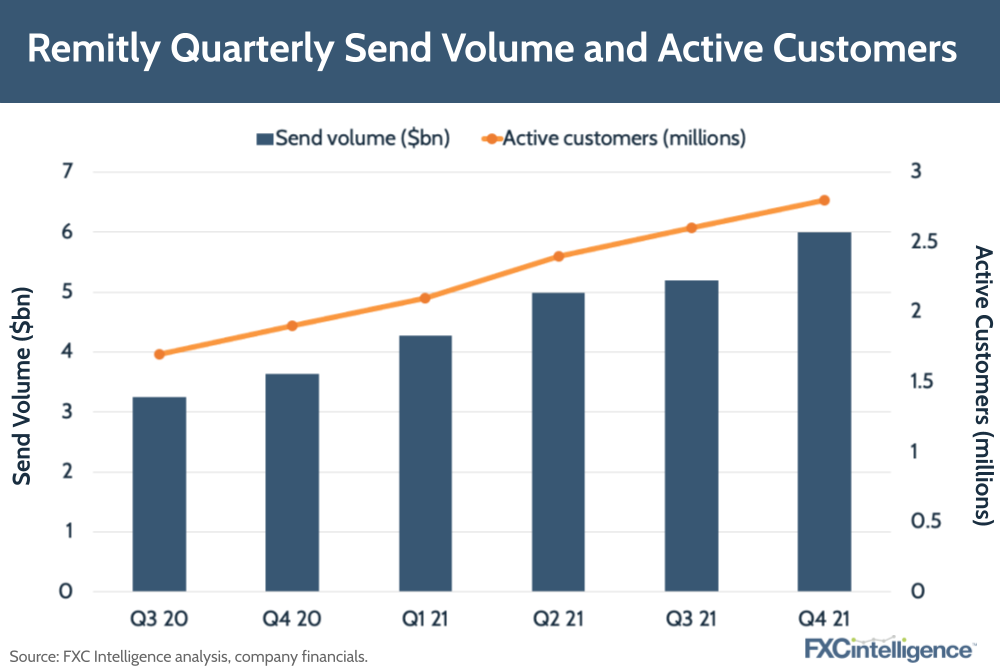

The global money transfer provider cited returning customers as a major factor in its success. Remitly achieved 90% revenue retention as well as a 50% yoy increase in active customers, while the overall remittance market is still only seeing single digit growth. It also massively expanded into new regions, adding more than 700 new payment corridors in 2021, increasing its total number of corridors to more than 2,100.

This year, Remitly is continuing to build its global disbursement network, invest in more financial services and pursue its goal of ‘reinventing the remittance experience’. But how does it plan to make this happen? David Webber sat down with Remitly CEO Matt Oppenheimer to take a deeper dive into the results and find out what 2022 holds for the company.

Remitly’s key growth drivers

Daniel Webber: What’s driven Remitly’s growth over the past year, and what’s going to keep driving it?

Matt Oppenheimer:

First and foremost, because we offer a great service and it’s complex to do so, our customers come back again and again. 90%+ percent of our revenue is from existing customers. Put another way, we have 90% revenue retention.

There are three areas we are continuing to invest in: firstly, continuing to add new customers at the right unit economics. For every dollar we invest, we get $6 back in just the first five years, so we have good LTV/CAC ratios and are investing in new customer acquisition.

Number two, adding new geos. We launched 700 new corridors. We now have 2,100 total and there are lots we intentionally haven’t launched yet. We’ve been very focused in our corridor expansion.

The third area is new products and services. That includes continuing to reinvent remittances and build peace of mind with every customer. Our digital-first approach and scale is giving us some flywheel effects and we are investing in new products and new financial services for immigrants.

There are so many factors when it comes to short-term market volatility, so we’re genuinely focused on the long term, making sure we educate investors as a newly public company and talking to the right investors. But we’re unflinching in our commitment to continue to deliver results and deliver for our customers. We certainly saw that in Q4 and we believe you can continue to do that, then the stock price and long term will work out as it should.

Figure 1

Expanding into new corridors

Daniel Webber: On the new geographies, that’s a giant opportunity. What do you see differently about the international market compared to the US market and the US customer?

Matt Oppenheimer:

When you think about all of the infrastructure that we’ve built, a lot’s the same. You need the same marketing platform and tools that are unique and proprietary. You need the same infrastructure in terms of compliance and fraud systems that are feeding more data and machine learning into delineating between good customers and bad actors. Pricing, FX, treasury – all of those things are similar.

Where it’s different are things like compliance localisation (for example, how you do local KYC) and things like payment acceptance. There are different ways of collecting funds, such as iDEAL in the Netherlands, SOFORT in other European countries, Faster Payments in the UK.

There are also languages. We’re in 14 languages now, and they need to be localised at scale. That’s one of the pillars we talked about in our S-1, but our strategy has been uniquely focused in those early corridors. Now we’ve created this corridor expansion playbook across language payment, acceptance, compliance and experience (you start to see patterns once you’ve done 17 countries). It gets much faster to do that next incremental country, given the foundation that we’ve laid, but we’re still doing it at a very localised level because what customers care about is sending money – from the US to the Philippines or the UK to Kenya. Each of those experiences needs to be optimised. That’s something that has been key to our success.

Daniel Webber: How much variance do you see on the payback period across your remittance corridors? Are some corridors more profitable than others?

Matt Oppenheimer:

We started with some of the largest, most competitive remittance corridors out there. We’ve proven that we can build large sustainable businesses there. And I do think that when you get into some of the longer-tail corridors, and you look at the world bank data, there are take rates and other things that are much higher. We’re somewhat agnostic on the corridor because we’re going to optimise the customer acquisition costs (the amount we’re willing to invest in that customer relationship) with the lifetime value in that specific corridor. Globally in the long term, I don’t see there being a huge variance in terms of payback across corridors.

With localisation at scale, we’re optimising the customer acquisition costs with lifetime value. And we have a lot of data and analytics that show where we’re doing that at a corridor level. That’s one of the reasons we’ve been able to deliver high ROI growth for a long period of time. We have levers that can adjust the amount we pay versus the lifetime value.

Figure 2

Remitly’s pricing strategy

Daniel Webber: You had a lot of questions about pricing in the earnings call. Tell us about your thoughts on pricing and what industry players can learn from your approach.

Matt Oppenheimer:

We have seen really stable and favourable pricing over time. Over the last seven quarters, our pricing has been stable above 2% take rate. Last quarter, our average revenue per user increased by 13%. That reflects the value of the service that we offer to our customers and that peace of mind is incredibly important.

With our digital approach in scale and size, we can offer a lot more value to our customers because our disbursement network and risk systems are better, meaning fewer transaction delays and fewer good customers are put into a really painful transaction review. I can tell you some stories that are just so painful, and that is common in the industry – not because remittance companies have bad intent, but because they can’t cut through the complexity.

It’s similar to what Amazon did in the early days with ecommerce. It wasn’t a novel idea that Amazon should disrupt or that we should be able to order things online. The reason Amazon won is because they executed and cut friction out of a very complex industry. People assume money transmission is simple, but there’s so much more complexity there.

We want to do with international payments what Amazon did with ecommerce. We’re on the road to do that but, similar to Amazon, you have to have scale size and become a digital-first player to get that flywheel effect and invest in all the legs of the stool of the disbursement network – the compliance and risk systems, payment acceptance, the marketing platform or the corridor specific level, the localisation, all the languages and so on. We’ve already done 100-plus integrations with disbursement providers and the velocity of those is increasing because of our scale incentive. When we were tiny, we couldn’t even get a bank to bank us because we were a money transmitter.

We’re at this really exciting point where we can reinvent remittances, given our scale size and growth rate, and that’s what customers value. They want their money to get there when they were promised it would get there, and have that peace of mind.

Figure 3

Rolling out new products

Daniel Webber: Let’s talk about new products. You have Passbook – talk us through how you plan to roll that out and execute it.

Matt Oppenheimer:

Traditional financial services are not built for immigrants. When I moved to the UK and I worked for Barclays, it was hard to get an account because they didn’t have my history of living in that country. Our customers have even deeper challenges when it comes to getting a bank account set up.

That’s why we launched Passbook, which is a bank account specifically designed for immigrants. We haven’t pre-announced other products, but there are other pain points that our customers have due to not having a history of being in that specific country that they’ve moved to.

If you think about broad financial services, having the direct deposit account is crucial for that relationship. It’s a longer investment, given that you’ve got to build out all the core functionality as well as differentiated features, but it’s foundational for multiple benefits around broad financial services that we can offer our customers. So we’re excited about that.

If you look at those three investment areas I mentioned, the new products had the longest lead time in terms of showing a return, but we’re very excited about the pain points we’re solving and the products that we’re building to solve those pain points.

Cryptocurrency’s potential for remittances

Daniel Webber: What do you think about crypto? Will it play more of a role in Remitly’s strategy moving forward?

Matt Oppenheimer:

With crypto, the question is: what is the problem that this specific blockchain or cryptocurrency is going to solve? I predicted that Bitcoin would be a store of value similar to gold or another asset class and that’s what it’s become. Not great for a payment method because of the volatility. We all know that now. But it’s important to rewind eight years ago when Bitcoin was being talked about as a global default currency.

What are the areas that I’m excited about right now? The idea of digital ownership, non-fungible tokens, is fascinating, especially as we move more and more into the digital world. It sounds like a bizarre concept at first, owning a piece of digital art. But when you take a step back and think about the original art versus prints and being able to validate the original, et cetera, NFTs are fascinating. There’s a lot of speculation and pricing and I don’t know what the right price is, but that’s a problem that blockchain and cryptocurrencies can solve.

When it comes to remittances, what we’ve seen in crypto is one: if you look at all the legs of the stool, there isn’t a single cryptocurrency that solves all those legs of the stool. And two, there is the need to onboard and offboard funds, unless there was one global currency, but that’s inherently a regulatory problem more than a technology problem. A lot of sovereign nations want control over their own currency, but as long as there’s the need to onboard and offboard funds (whether that’s crypto-to-fiat, fiat-to-crypto) that is what we are good at and we can do that well and that puts us in a unique position for how crypto evolves.

Unlike other remittance companies, we’re going to lean into crypto and learn in a customer-centric way. Because if it’s good for customers, it’s good for us and we can be on the leading edge. Some of those companies will be enormously successful and some will fail. But by partnering, we’ve had much more of a front-row seat as some of these companies have expanded and realised they needed us to test if they can be successful.

Again, when Amazon went into the third-party seller business, they were enabling third-party sellers to sell off of their platform. They did that because there was a flywheel effect, and more transactions going through the platform created more scale. Similarly, in the event that some of the crypto companies are successful, most of them will just add additional TAM to our business, but we’re going to be the ones partnering and leaning in on that so we’re on the cutting edge of how things are evolving.

Daniel Webber: Anything else you want to talk about?

Matt Oppenheimer:

I heard an amazing story of a customer who was trying to send money to the Ukraine and had a bunch of delays with a legacy provider, and he talked about how impactful it was for his family when he switched to us. That sort of thing is at the heart of what we do and why we do it. The sacrifices that our customers make to be able to do that is amazing, so that’s always the most important point. Everything else follows.

Daniel Webber: Always a pleasure Matt, thank you.

Matt Oppenheimer:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.