OFX saw rapid growth following its acquisition of Firma earlier this year. In the latest in our Post-Earnings Call series, we speak to OFX CEO Skander Malcolm about Firma’s impact on revenues, as well as inflation, the company’s customer strategy and OFX’s approach to geographical expansion.

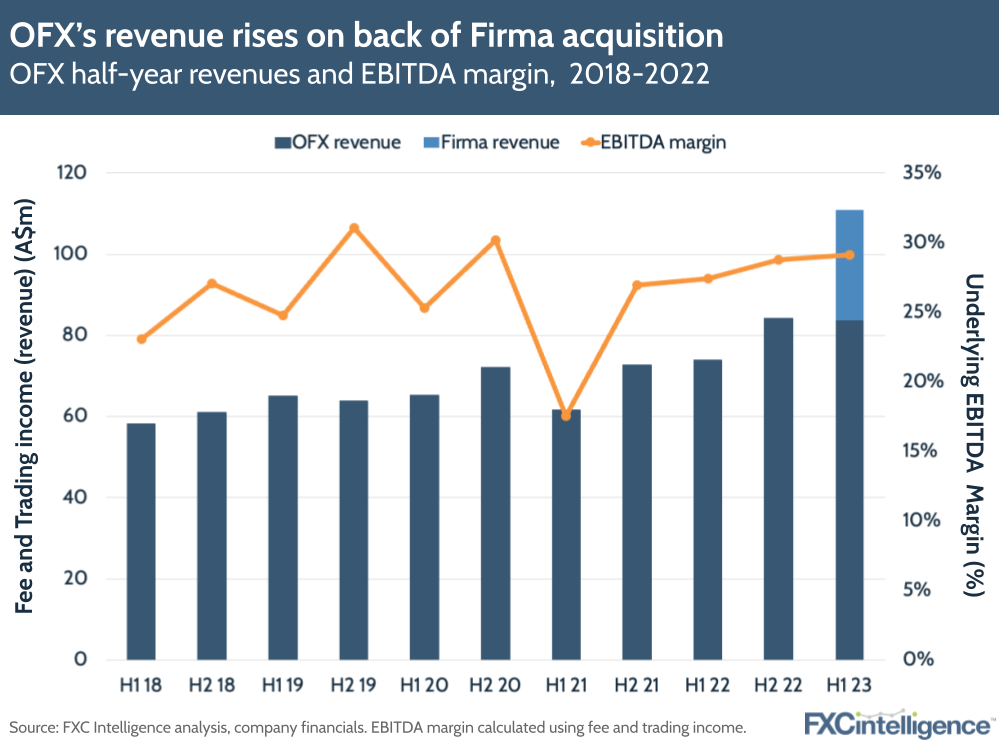

Last week, Australian FX and payments specialist OFX reported its earnings for H1 2023 (running from 1 April to 30 September 2022). OFX’s fee and trading income (overall revenue) increased by 49.9% YoY to A$110.9m, driven by $27.2m in revenues from Canadian FX and payments provider Firma, which the company acquired earlier this year.

Firma drove corporate sales in North America, where OFX saw revenue growth of 117.2% (17.2% excluding Firma), while Europe grew 26.9% (19.7% excluding Firma) and APAC grew 15% (7.3% excluding Firma).

OFX’s corporate segment saw the biggest leap, with 98.2% revenue growth (19.7% excluding Firma). Meanwhile, increased volatility in the West also contributed to an 11.3% rise in the high-value consumer segment, where Firma had a smaller impact, adding just $1.1m. Overall, the company’s number of active clients grew 8.2% to 152,600.

Underlying EBITDA was up 59.4% to $32.3m, which combined with OFX’s net operating income (NOI) of $105.3m gave a solid EBITDA margin of 30.7%. On the other hand, the company’s operating expenses have grown 50.9% to $6.5m, fuelled by the Firma acquisition, while bad and doubtful debts rose to $1.2m, due to provisions on smaller transactions in North America.

Despite these expenses, OFX has upgraded its FY23 guidance, and expects intangible investments to rise to $15m-$17m in FY23. On the back of Firma growth, it has forecast an NOI of $215m-$222m, and an underlying EBITDA of $62m-$67m.

With Firma delivering results for the company, how will OFX look to translate these results to even more profitability gains? I caught up with OFX CEO Skander Malcolm to find out.

OFX key growth drivers in H1 2023

Daniel Webber:

What have been the key growth drivers for OFX this quarter?

Skander Malcolm:

The overall growth in net operating income of 53.4% is very positive, as is over 59% growth in underlying EBITDA – to A$32m. Those are the headline numbers, and Firma’s made a very strong contribution to those. We showed the Firma growth rate at over 30%, which is incredibly impressive given the long-term growth rate has been in the 2-4% range, so it’s an outstanding contribution from the Firma team.

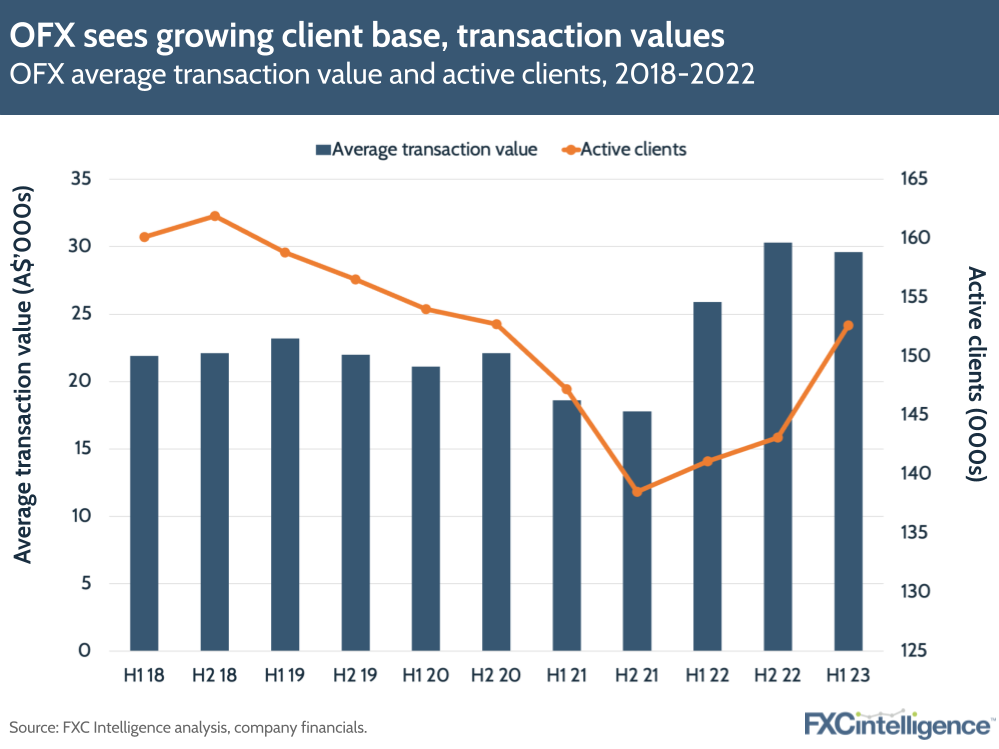

Underneath these results are strong fundamentals. Transactions per active client are going up, including the contribution of Firma where, typically, they’ve had fewer transactions per active client in our corporate compared to the OFX corporate segment. You’re seeing NOI margins going up both on OFX and on Firma. When you get more transactions with better margins, they’re very strong fundamentals.

We’re continuing to see our risk investments keeping us very safe, although we saw a bit of an uptick in provision for bad and doubtful debts. There’s a bit of a pickup in fraud in North America. However, that’s against the backdrop of over A$35m invested in intangible assets in the last four years. There’s a growth in investment in the opex line, particularly in people. We’ve now got over 700 full-time employees, so we’re not producing those outcomes at the expense of investing for the future.

Figure 1

Impact of Firma acquisition

Daniel Webber:

Let’s focus on Firma. How is it driving growth?

Skander Malcolm:

Volatility gives every cross-border payments company some advantage, but you’ve got to take that advantage and I’m incredibly impressed with the Firma commercial team.

The average tenure is just under eight years, so when that volatility arrived, there were employees who were close to their customers and able to support them through that volatility. That showed up in Firma’s very healthy NOI margins and average transaction values, and they continue to have outstanding client retention.

The Firma result is the result of all the hard work over the last several years, with lots of investments in people and a clear growth strategy over time. If you look at the clients that are now using their online channel, that’s now over four million of the 27 million total. Those transactions per active client are the biggest of all.

Their approach to help support their commercial teams by putting an online channel out there is also working. We are delighted with that. Finally, all of these factors – the intangible investments, the risk culture, the focus on NOI margins and the emphasis on running a sustainable company – set us up very well for the risk cycle we’re now in, which presents a higher risk of a combination of high interest rates and high inflation. Frankly, we haven’t seen this in the West for over a decade. OFX is very well positioned to be able to flourish in that environment.

Figure 2

Impact of inflation on OFX

Daniel Webber:

How does inflation affect your business?

Skander Malcolm:

There’s two main impacts, with the first being ticket size. If you’re an SME, you’re paying more for things like inventory, software and wages. Every bill goes up, so your ticket size goes up.

Secondly, central bankers are raising interest rates to respond to inflation, meaning the cost of interest has gone up, and that has two effects. For our SME clients who have debt, that’s a bigger bill to pay, so they’re looking at other ways to save money. We’ve seen an increase in the number of forwards and the penetration of forward contracts because they protect against the big swings in volatility. When you’ve got inflation and higher interest rates, you have much more layers of focus on your cost line and certainty.

It’s starting to have an effect on competition. We’re seeing significant price rises from competitors who’ve said for many years that the price is going to zero. We’ve also seen some of the new entrants to the market increasing prices dramatically. For example, one company I know has increased their price by 60% in the last three weeks. That again is inflation and interest rate-driven, because the cost of investors’ money has gone up and investors are saying they want to see a return on that, which tends to drive increased pricing.

Figure 3

Exploring global expansion opportunities

Daniel Webber:

Following the Firma acquisition, where geographically are you now seeing the most opportunities?

Skander Malcolm:

We’ve been saying since 2018 that the biggest growth opportunities are in the largest markets, and that’s traditionally been North America and UK/Europe. Disproportionately, that’s where we’ve been investing. We think APAC has terrific potential, not just Australia and New Zealand but up in Asia.

However, the infrastructure that we’ve got in place in North America and UK/Europe means that we can add Firma, for example, up in North America and see 20% underlying EPS accretion in year one. If you step back and say, well you’ve got a UK license, you’ve got a European license and you’ve got a very good team in Europe, those opportunities are there for us to add scale and margin and accretion very quickly.

So it’s not a case per se of just North America or just UK/Europe or just APAC. We look at all of those opportunities, and having that infrastructure in place is what breaks open the opportunity to add the scale.

Figure 4

OFX’s customer acquisition strategy

Daniel Webber:

Are you going for more of the same type of customer, or are you also going for different types of corporate customers?

Skander Malcolm:

The corporate segment ranges from micro businesses, which can look like consumer, into small businesses, mid-size and even large corporates. Our sweet spot is small to mid-size, and Firma was typically slightly bigger in terms of clients. Their ATVs [average transaction values] were higher, but that was partially because they didn’t have as deep a penetration of the client wallet, which was because they didn’t have the online platform that was picking up the smaller value transactions that corporates have.

We definitely think the sweet spot is smaller, mid-size. In the small space, we’ve got a lot of the product capability that we need, and we can see that the growth in that particular subset of corporates is strong and continuous. In the mid-size, there’ll be more investment risk products as we mature, and our investment in TreasurUp is an example of that. That will give us better access to mid-size corporates.

Risk versus credit products

Daniel Webber:

Will you be staying in the risk space, as opposed to moving more into credit products?

Skander Malcolm:

SMEs have a need for credit products, working capital and those types of things. I have a lending and leasing background and so do others in the management team, so I understand those businesses very well. They’re more (what I would call) balance sheet businesses than flow businesses, so those skills are different skills.

We certainly partner with organisations, particularly in the ecommerce space, who provide back credit, working capital, inventory financing or things like that. We know our clients like that, but whether we are the provider of that is another question. It’s certainly something we’ve looked at many times, but right now we’re comfortable staying on the flow side.

Creating profitable growth

Daniel Webber:

How are you thinking about profitable growth moving forward?

Skander Malcolm:

There’s a range of investors. Some investors absolutely value profitless growth, because they’re still putting money into organisations that are not turning a profit. Their thesis is just a different thesis to ours.

Ever since I’ve been in the role, we’ve said that we want to pitch ourselves as a sustainable growth company. The type of investor that values that, they look for a specialist business that can make money on its core service, not a business where the customer and the returns are all about selling multiple products to that customer. It’s not that one’s wrong or right, it’s just that we have chosen the path of being a specialist provider where we believe we can make a reasonable return on the core product.

Because of the size of the markets and our relative size to those, there’s a lot of headroom. It doesn’t mean that by making a profit, you’re going to have X growth. It’s just how you make more earnings from more clients in the space in which you’re very good at. There’s a lot of work we still have to do, and you can see that in the growth and intangible investments in our product and service delivery worldwide. We think there’s a lot of headroom for us to grow profitably over the next several years in that flow space.

Daniel Webber:

Anything else you’d like to add?

Skander Malcolm:

As we head into the risk-off environment, I couldn’t be more proud of the team, and this was our first acquisition. Some folks had experience with M&A, but most folks didn’t. So those results have all been delivered while the large majority have been of people who have had no experience in M&A.

The core business has continued to perform very well. The Firma contribution’s been exceptional but, in addition to that, there’s also been a significant technical programme and product programme being delivered. I couldn’t be more delighted with the team and their ability to execute at the moment.

Daniel Webber:

Skander, thank you.

Skander Malcolm:

Thanks very much.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.