Australian money transfer provider OFX has seen further growth in its corporate segment in H1 24, despite macro impacts in North America. In the latest in our post-earnings call series, we speak to OFX CEO Skander Malcolm to find out more about the company’s core drivers and strategy going forward.

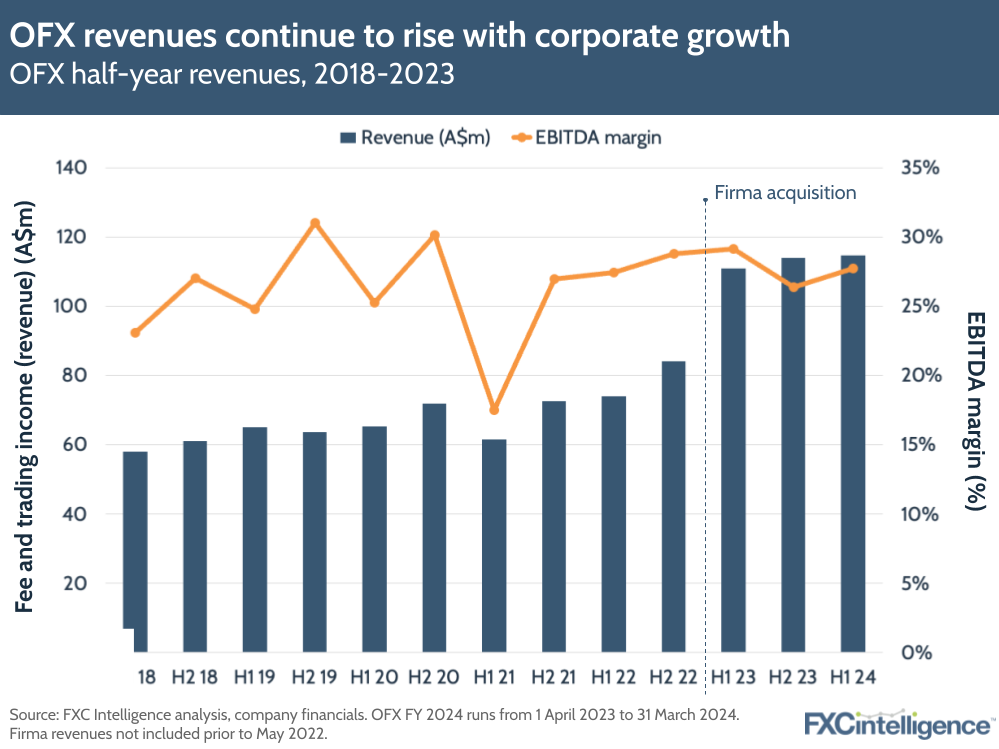

OFX’s revenues grew 3.3% to A$114.6m in H1 2024, which spans calendar Q2 and Q3 2023, while its net operating income (NOI) grew 9.4% to a record A$115.1m.

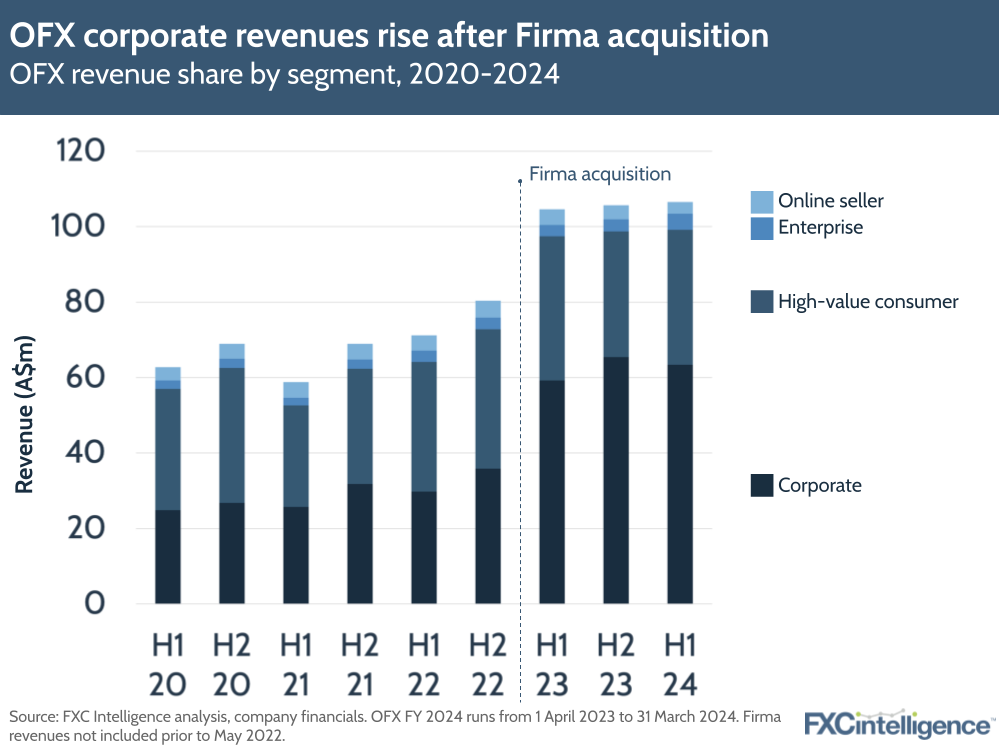

Growth was driven by OFX’s corporate segment, enterprise revenues rising 46% and strength in EMEA and APAC. However, the company’s EBITDA for H1 fell slightly YoY to A$31.8m (though it grew compared to H2 23), which may have prompted the small share price drop after its results.

Following its acquisitions of Canada-based Firma, and more recently Australia-based Paytron, the company has continued to see a growth shift towards B2B. Corporate revenues were up by 7.2%, while the company’s high-value consumer segment declined by 7% YoY to A$35.8m. OFX did note that it was comparing to unusually strong revenues for consumer in H1 23.

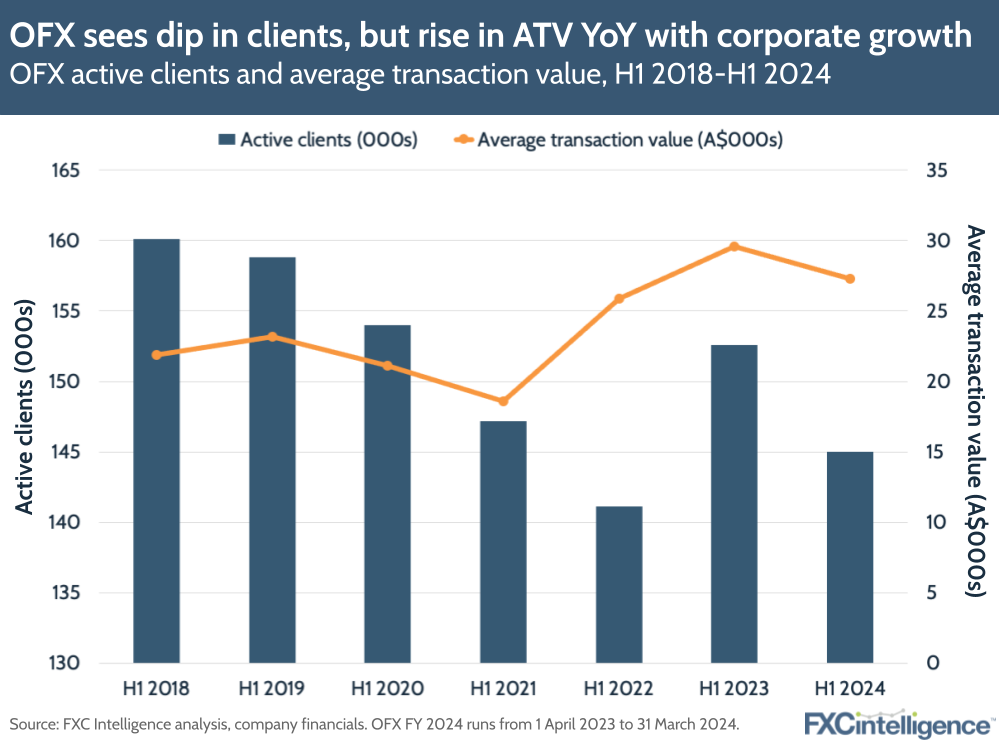

The company recorded over 103,000 active consumer clients for the half, with 29,300 active corporate clients, but transactions for corporate were at 354,700 for the half, while for consumer they were at 225,400. In addition, average transaction values (ATVs) for the corporate segment were at A$32,400, compared to A$20,000 for consumer, showing the additional value of the company’s B2B focus.

Having said this, OFX did mention that corporate ATVs overall had declined by 12.2%, driven by a stronger dollar and “lower corporate confidence” in North America, particularly Canada. Looking forward, the company has curbed the upper end of its guidance for NOI and adjusted EBITDA, which it now expects to be A$225m-238m and A$63m-70m respectively (compared to A$225m-243m and A$63m-74m forecast previously). Including Paytron, the company expects an NOI of A$226m-239m and an EBITDA of A$59m-66m.

We spoke to OFX CEO Skander Malcolm about key drivers and challenges for OFX so far this year, as well as the company’s acquisitions strategy going forward.

OFX key revenue drivers in H1 24

Daniel Webber:

What have been the key trends driving the core parts of OFX in H1 24?

Skander Malcolm:

Clearly, the goal is to grow NOI and underlying EBITDA at a healthy rate and we did that in the half. Corporate continues to be the strongest driver of that growth, both in NOI and in underlying EBITDA.

We did see a fairly unusual half in our corporate segment, specifically in Canada. Canadian corporates were facing three things at the same time that other corporates around the world were not. They were seeing reduced business confidence in Canada generally, coupled with a very strong US dollar, so US dollar sellers were naturally a little reluctant to book large transactions.

Then you saw corporate credit in Canada and the US, which is where a lot of the clients are, shrink and, therefore, they were seeing a little more reticence from their clients. They were seeing this very unusual exchange rate and [drop in] business confidence happening at the same time, which meant that ATVs dropped by over 20%. The good news is that they actually increased the number of transactions by more than the ATV so revenue was flattish/slightly up. That’s very encouraging because you want to make sure you retain clients and lots of transactions indicate a very engaged client.

But every other region in corporate – US, UK, Europe, Australia, New Zealand – saw healthy growth numbers and were generating more transactions, steady ATVs and better margin, so that segment is performing very well. We’ve already seen Canadian ATVs getting back to historical levels in the second half.

Enterprise is obviously a standout at north of 40% growth, driven by a combination of long-standing clients who are very active; the newer clients like Link and Wise Tech activating really well; and then the newest clients, Shift and Automic, also contributing quickly. Obviously, it’s delightful to have our first win up in North America with the Toronto Stock Exchange. So, enterprise looks like it’s got very good momentum and we’d expect that to continue in the second half.

The consumer segment was healthy, with a return to some of those high-value use cases. We’re seeing continued strengths from our existing consumer clients, and then the online sellers portfolio was a little soft. Fundamentally, the reason for that is we didn’t do a lot of investment in product because of the Paytron acquisition, which is really where that product will sit on that platform, and that looks like an exceptionally good fit. All in all, [we’ve had] healthy margins, good growth and strategically more conviction than ever that the pivot to B2B is where the future of OFX will be.

How OFX is growing its corporate client base

Daniel Webber:

On the corporate side, global registrations are up 41.9% – higher than some of the other growth numbers. What is it about your corporate product that is resonating and taking share from other product offerings in the market?

Skander Malcolm:

We’re hugely encouraged by that growth and registrations. In addition to that, we’ve actually seen a substantial growth in conversion rates of those registrations into new dealing clients. I particularly single out North America for the work we’ve done around onboarding, making sure that we have the right fraud controls, but equally more digital and simpler ways to onboard the clients. So, not only have we seen a great growth in registrations, but a really strong growth in dealing clients in corporate all around the world, which, as you say, is very encouraging.

I’d say the reasons for that are, number one, the value proposition of OFX has always been “digital plus human”. The “plus human” is registering as being really critical during uncertain times when you can actually talk to someone. For example, we’re seeing the average first three months of revenue be higher than normal, which would suggest we’re acquiring higher value for corporate clients than historical trends.

Secondly, there’s no doubt that the competition has been increasing price quite substantially, which means that the difference in price from the growth companies – who are really pushing very hard to acquire lots of clients at a low price – has become negligible. We see that all over the world. So if your digital platform is easy to use and onboard with, your price is very competitive and you’ve got service, that combination is clearly resonating a lot more than it did 12 months ago.

The final thing is we’ve invested a lot over the last three years in salespeople and sales operations. So the effectiveness, the return on investment on salespeople has continued to grow, in addition to better digital marketing. So all of that generates strong registration growth, which will really flow through in next year’s numbers because typically our corporates tend to build their business with us. Consumers tend to give it mostly to you right upfront, so you’ll see the revenue in the first six to 12 months, whereas corporate it’s a build over 12 months. So, you’ll see that registration growth in next year’s numbers.

OFX’s acquisition strategy

Daniel Webber:

You’ve made numerous acquisitions recently, including Firma and Paytron. What are you looking for in terms of acquisitions going forward?

Skander Malcolm:

We’re very active in terms of looking at opportunities. I would say during the Northern Hemisphere summer, it was pretty quiet. A lot of people are on vacation. After that, there was an IPO in our space that really gave folks a lot of confidence that the IPO market was open and that that was a good path. Subsequently, there was a profit downgrade and there’s been a big hit to the share price, and that has meant that some of those folks are now reconsidering whether that’s really the best path out.

Obviously, we are here, we’ve got a great track record with Firma in terms of integration. We’ve paid down a lot of the debt. So there’s opportunity there for us and we’re active in assessing those opportunities. We’d love it to be UK and Europe, but we’d love it to be in North America too.

Daniel Webber:

Are you looking at acquisitions to add capabilities or in terms of adding revenue and profitability?

Skander Malcolm:

More of the latter. We love what we’ve acquired with Paytron, both in terms of capability and the team, and our product roadmap is pretty clear. Our technology is very advanced, so there’s not a capability that I’m out there looking for at the moment, and the Paytron acquisition actually accelerated some of the capabilities that we were building ourselves.

It’s more likely to be that Firma style where there’s a good portfolio and they have salespeople. That’s the sort of thing that we’re more focused on.

How OFX’s competition is evolving

Daniel Webber:

Anything else you’d like to add?

Skander Malcolm:

It’s fascinating to see how these business models are evolving. We’re seeing various competitors out on the market be a lot clearer about who they’re focused on and we think that’s a good thing. We think the level of intensity of competition continues to be high, but people are saying, “This is really what I’m focused on”, as are we.

Net-net, that’s a good thing because it allows us to compete to our strengths. We can help prospects understand what their choices are and be pretty clear about that. And the strategy is very clear from OFX, so, net-net, we like the future.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.