FXC Intelligence’s Daniel Webber spoke to MoneyGram CEO Alex Holmes and COO Kamila Chytil about the company’s FY 2020 earnings results, digital focus and future plans.

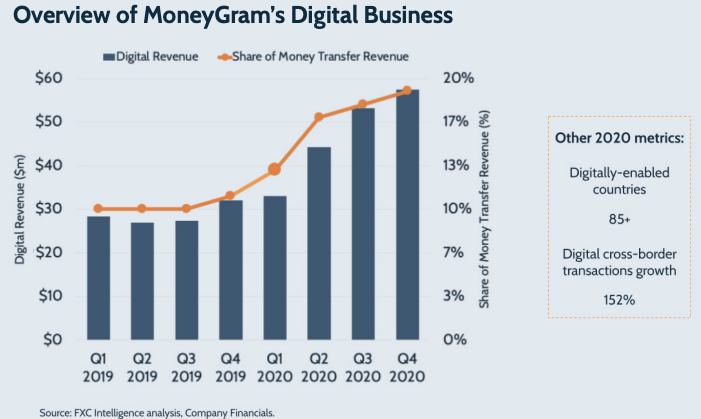

MoneyGram posted strong digital 2020 results this week against the backdrop of a challenging year. Cross-border digital transactions hit a record 152% growth in 2020. Top-level digital revenue and transactions also grew by triple digits, thanks to innovation on the pay-out side and a strong strategy for digital partnerships.

The pausing of its Ripple relationship and increased competition in retail are the primary headwinds that MoneyGram’s digital business is looking to grow through. How will MoneyGram evolve over the coming years as its targets 50% of its business to be digital?

FXC Intelligence CEO Daniel Webber had a detailed discussion with MoneyGram CEO Alex Holmes and COO Kamila Chytil to find out more.

Topics covered:

- Drivers of cross-border principal growth

- The growth in digital partners

- Account deposits as a key driver

- The Visa Direct opportunity

- Offline retail’s ongoing role

- The evolution of the Walmart partnership

- Ripple and the future of MoneyGram’s crypto efforts

- Trends in pricing

Drivers of cross-border principal growth

Daniel Webber: Let’s start with the growth on the principal side; 27% in Q4 2020. What’s been fuelling it, and where do you think you’re taking share from?

Alex Holmes:

There’s a variety of different factors in play right now. We did a survey back in December [where] about 70% of people said they were sending money back home because they thought that the receive side was suffering a lot more this year than they had historically, and whether that was for food or shelter or education, etc, it was important to them to step up and earn a bit more money.

That has been driving a lot of the principle increase in terms of size per transaction. We’ve seen, across the board, a bit of a surge in terms of how much individuals are actually sending. I think that’s pretty interesting because it’s a sharp contrast to a lot of fears that the World Bank and others had about a slowdown in remittances.

Secondly, we’ve had a tremendous success in the digital side of the business where we continue to see triple-digit cross-border growth rates and continued acceleration of that business. A lot of that business is driven by not just new customers coming in, which we’ve seen a massive increase on, but also repeat customers’ transaction frequency increasing and pushing higher customer lifetime value.

Then, third, the combination of them all brings us to this question of who are you taking share from. I do think that we continue to gain a disproportionate amount of new customers coming into the market, and we’re also seeing a lot of movement from some of our larger competitors and also some of the regional competitors as well. We’re getting a lot of intelligence that says they’re definitely coming from some of the competition that’s out there today.

Figure 1

The growth in digital partners

Daniel Webber: Talk us through what the digital partner piece is. That’s obviously growing well. We can see the numbers in the print, but what’s underneath the digital partners?

Alex Holmes:

It’s something that we started many years ago that’s actually ramped quite quickly in the last couple of years. Long ago, we used to sign physical agents around the world, and then out of nowhere, we began to see an outreach from partners that we used to call virtual agents, and what they were, in our minds anyway, were basically traditional agents, but rather than having a physical presence, they led with a digital presence.

Some of it was banks in Asia, and then sometimes you would see wallets, but it wasn’t really a tremendously strong growth market for a number of years.

A lot of these partnerships have popped up and continue to pop up in just pretty much every market around the world. A lot of it across Asia, of course. We’re seeing it in the Middle East; we’re seeing it in Europe and then back home here in the Americas.

I think it’s a trend that will continue, and I think it’s one that consumers tend to gravitate toward because they’ve already done their KYC process in many cases. They’ve already signed up for that app for a reason, and they are usually doing something in a domestic sense with that app or with that online presence in the market, and then adding remittance as a cross-border payment capability is sort of a natural extension of what those partners are doing.

You could also think about it from a competitive perspective as well that they may have some local corridors, meaning they may move money. If you’re talking about maybe a Korean fintech, they might do some money movement for countries that are near to Korea, but when it starts getting far afield, they’re looking for a broader company like a MoneyGram to help facilitate fund flows and really expand their capability so that they don’t really have to get out of market and go sign up those partners.

Because it’s really not what their business model is about, and managing back-end networks all around the world is complicated. It takes time and energy, and so for us, it’s a great extension of our business model.

Daniel Webber: How much of that do you do that’s unbranded, and can partners set their own prices?

Kamila Chytil:

It’s always unbranded. The digital partners are always the ones that control the user experience, and they are the brand that the user knows, and they use our technology on the back end. All of the new ones set their own pricing. Some of the ones that we’ve had for some time may have a pricing grid that was agreed upon in the past, but the model today is for them to have 100% flexing on pricing.

An example would be Sentbe in Korea. It’s a fintech startup. And we have several others in Asia.

Alex Holmes:

SBI in Japan is another good example as well, which is basically an online bank in Japan. They’ve been around for quite a long time, but that’s another partner that we’ve had, one of our largest partners in Japan. Almost 100% of their business is funded through transactions that initiate on their website.

Daniel Webber: How do the economics of those types of partnerships look? I assume the top line is less by definition because you’re not taking all the transaction value in, but then margins for these things can be good?

Kamila Chytil:

That’s exactly right. You hit the nail on the head. It is lower top line, but it has a very good margin for us because we get paid a fee regardless of the type of transfer it is, regardless of whether it was a newly acquired customer or a customer that received an incentive or one that had a product code or if the effect was becoming extra competitive. All of that is in the partner’s control. We receive a flat fee either way. It’s definitely a lower top line, but it’s a consistent and very good margin.

Account deposits as a key driver

Daniel Webber: Let’s discuss the account deposit. When you say account deposit, this is on the receive side, right? What’s driving the triple-digit growth for that?

Kamila Chytil:

Correct. A couple of interesting things. It definitely has a much higher probability of being a sent-to-self transaction. People that are sending home to their own accounts for investment purposes, for example, versus family or friends remittance that you’d see more exclusively in the cash space. That’s one interesting difference.

In terms of principle and frequency, it’s pretty much on parity with the digital business. Yes, it’s higher frequency, higher retention rate, and principle is slightly higher and certainly grown over last year, but not significantly higher than sending to other types, like Visa Direct, for example.

It’s very similar in that aspect and definitely very geographically concentrated. Countries that have had significant legislation around banking their populations tend to see a lot more real-time connection – India for example. Banks have obligations to post funds in real time, and the populations are used to not dealing with cash after some of the demonetisation challenges that the country has had. For example, one of our highest account deposit countries is India.

Alex Holmes:

In terms of the types of transactions, you need to break it down into the types of receive side. You have your traditional account deposit, which is into a bank account at a traditional bank typically. Those tend to be a bit higher dollar amount on send, but I wouldn’t say particularly more frequent.

You see Visa Direct is very similar in some respects to wallet transfers where you’re seeing higher frequency and probably smaller dollar amounts in a lot of those transactions because those tend to be more P2P-type transactions where I’m making a send to somebody. I think we talk a lot about value shifts in market dynamics, and a good example of this would be our partnership in Ghana with Zeepay.

We traditionally had account deposit transfer into Ghana, and we also had cash payout in Ghana. That looked a lot like a remittance transaction in terms of not super frequent transactions and that $500, or whatever it might be, traditional cash amount. Then when you switch to a Zeepay wallet, you’re seeing a lot higher frequency, but much smaller dollar amounts in the transaction flow.

It’s pretty interesting, but you need to really think about account deposit sends as being traditional bank sends and then breaking that into more of your wallet and then Visa Direct, which also has a different look and feel to it. It’s pretty fun, and it was really interesting because it definitely gives you that variety of differentiation and choice from a customer perspective.

It’s also bringing different customers to the brand for the different purposes of those sends. It’s nice to be able to break out a little bit of your traditional consumer-to-consumer remittance, and then look at also this idea about sending to yourself, to your savings for when you go home someday, or potentially paying people for higher frequency, lower dollar amount-type transactions as well in the payment space. It kind of breaks it into those variety of buckets and definitely differentiates the type of consumer.

Figure 2

The Visa Direct opportunity

Daniel Webber: Let’s talk about Visa Direct. You just mentioned a little there on the P2P side, but where has that added a unique addition, and where’s the opportunity? How far can Visa Direct take you?

Alex Holmes:

What’s really unique about Visa Direct is if you think about a traditional account deposit transfer or even a wallet transfer to some degree, you have to have quite a bit of information about what you’re doing. In some respects, account deposit even in the money transfer space is still a little bit analogous to a wire transfer. You have to have the account number; you have to have the routing number. The sender has to set that up and deliberately make that transaction.

In the case of a Visa Direct send, you’re really asking for a debit card number to key in, and so it’s much more like a reverse payment in that sense. We’re all very used to going online, and registering, and using a card for a payment. This is actually going online and registering a card for a receive-side payment, so it’s pretty interesting because it’s allowing you to push money onto debit cards.

Then, obviously, most people around the world are looking for utilisation of the funds in a relatively quick way, so being able to post directly into a debit account is very attractive. It’s obviously a lot simpler than going and getting your account number, your routing number and communicating that information, versus just giving your 16-digit PAN on the front of the card.

Kamila Chytil:

It’s really the ease of experience that’s the selling factor here for consumers. The money arrives in real-time or near real-time, but in less than 20 minutes, which is also unusual, right?

Only a few direct bank account connections around the world still as a percentage point are actually in real time. A lot of banks still post every four hours or every 12 hours or when the banking core updates after midnight. It really depends on jurisdiction and the age of the banking system.

Visa Direct rails work exactly the way, like when you use your debit card. The balance gets pushed essentially in real time. Consumers really like that.

From a technology standpoint, it’s a simple Visa gateway, so anybody enabled becomes enabled right away. We don’t have to do something specific for every bank, and that’s really the beauty of the aggregation component. We don’t have to do something specific for every country. Visa has exchange rates, ISO messages that are consistent, so the number of data elements are not different.

What we’re finding, for example, in account deposit these days is banks are starting to get a lot more concerned about what flows are coming into the country, and they’re starting to ask for more information. They’re starting to ask for purpose of transaction or they’re starting to ask for source of funds or source of income.

There’s a lot of local regulation by central banks that’s starting to create that need for information. That, of course, creates friction in the transaction process because you have to ask yet another question from the consumer when they’re sending. With Visa Direct, none of that exists because it’s all accounted for in the compliance rules as being part of the network, so there’s a variety of components that just add a little bit less friction.

Daniel Webber: For Visa Direct customers, is that the only method that they’re using, or are they also sending to account or to cash? Does it tend to bring in a standalone Visa Direct recipient or is it a changing customer behaviour that used to be cash, and now moves to a debit card, which is easier?

Kamila Chytil:

We haven’t looked at a ton of crossover, but what we have seen is Visa has done a lot of advertising on our behalf. For example, PayMaya in the Philippines. The Philippines is a pretty large Visa Direct customer. A lot of the banks are integrated with Visa Direct rails. They did receive that marketing for us when PayMaya went live. That was supported by Visa, so we did acquire some new customers because they were really interested in what they were getting on the receive side.

PayMaya was offering them additional credit. It had nothing to do with the price that we were charging, but they were getting additional benefits on the receive side. In that instance, I would bet that the majority of the customers were brand new to MoneyGram and simply said: “Hey, send to my Visa card because I’m going to get something there”.

Offline retail’s ongoing role

Daniel Webber: Let’s talk about retail offline because it is still a significant part of the business. What are the dynamics you’re thinking about for 2021 for the retail, cash side of the business outside of digital?

Alex Holmes:

My holistic view over the long term over the next couple of years is we’re going to be pushing this organisation as hard as possible to become digital everywhere we can be. We’re almost digitised in half of our 200 countries. I think we’re somewhere in the 90s and moving really quickly.

We’re going to continue to push that, and I think that we’re nearing, if we haven’t already crossed, 30% of our transactions that are now digitised. I’m thinking we’re going to pass that quickly and move up. If we get over 50%, I think it changes the entire paradigm and really the entire view and perception of the company, and who we are, and what we do. So that’s a hugely important part of our mission here.

I think you have to dissect the send side and the receive side differently on the cash piece of the business. I’m extremely bullish on cash payout services for the foreseeable future.

A lot of these digital partners we’ve talked about are pushing these transactions, and the customers are going online to send these transactions. A lot of them are still being picked up in cash around the world. I think that’s going to be a need that’ll be there for a very, very long time. Even as Visa Direct, and account deposit, and wallet continue to proliferate and grow, that cash received side is just going to be critical.

On the send side, I think we’re going to continue to see a migration away from large agent partners and continue to really see a narrowing of focus into the retail and smaller mom-and-pop space.

That’s probably the case in the more Westernised markets like the US and Europe. Maybe that won’t necessarily be the case around the world, because let’s say if you’re in Asia or Africa, Middle East, even Latin America, I would say that remittances are much more indoctrinated into the everyday lives of banks in those regions. It’s a little bit of a different paradigm.

If the net of all that is we can continue to grow the walk-in business in mid-single digits, that would be a reasonable outcome against the backdrop of a growing and more dynamic digital side of the business, which is pushing the growth rate hopefully into sustainable double digits. Obviously, that’s going to vary by quarter, and it’s going to vary by year, but I really think that’s how things are going.

Figure 3

The evolution of the Walmart partnership

Daniel Webber: How do you see the Walmart relationship evolving?

Alex Holmes:

We’ve been partners with Walmart for a very long time. I think both parties have done very well in the combined partnership over the last couple of decades. I’d say really for the last decade, Walmart has been doing what a lot of other retailers are doing, which is figuring out what their point of sale experience should be like, what their service offering should be like, how do they more dynamically sell services against the backdrop of an evolving digital requirement, and also against the backdrop of increasing cost for servicing, and trying to figure out how to do money centres.

With Walmart, the single most important thing continues to be how do they give everyday low prices to their customers, and so that evolution has been underway for a very, very long time. When we were the sole player and the incumbent in the location, any addition of other services is obviously going to be somewhat detrimental to our market share inside of Walmart, but it’s an understandable evolution, and it’s not really different from what we’ve seen around the world. We’ve had plenty of areas in the world where we’ve been the player coming in, and we’ve taken share from the incumbent in those stores. We’ve been very successful at that.

Also because of that established relationship and because of our presence inside of Walmart, we’re in a very strong position to continue to promote our brand, even if it’s the white-label powered by MoneyGram brand. We showed that over the past year against the introduction of the Ria outbound white-label product, where we’ve been able to really maintain our share.

I don’t think the introduction of Western Union will be any different from that experience. We’ll have to continue to work with all the associates at Walmart to educate them on the value of our product and our service. It’ll disrupt our share inside of the store, but it’s also important to me that we continue to diversify our revenue streams and continue to move away from the reliance on single, large agent partners.

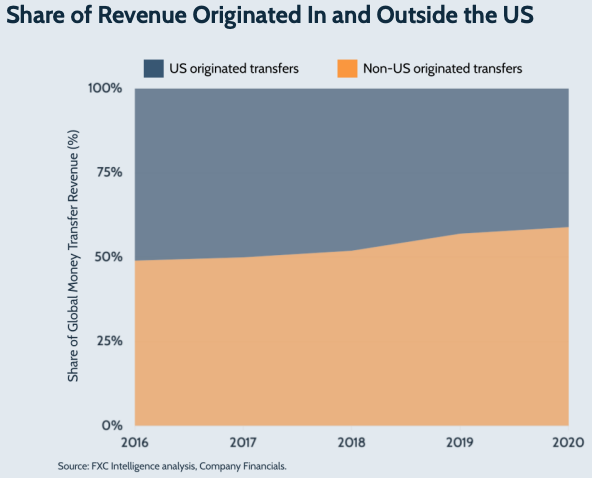

When I started here, Walmart was 36% of revenue, and now it’s below 12% – and even lower in the money transfer side – and continues to go down as the rest of business grows and Walmart diversifies. I think it’s part of the evolution, and we’re comfortable with our ability to compete. We’re looking forward to doing that.

Ripple and the future of MoneyGram’s crypto efforts

Daniel Webber: You addressed most Ripple-related questions in the earnings call, but away from the financial side, what other areas do you think may have any impact on the business in the next year if you are off Ripple’s platform?

Alex Holmes:

We’re doing a lot in the background on new payment forms and applications, and crypto is obviously an important aspect of that. I think the one thing that we particularly enjoyed about the Ripple relationship outside of the financial side of it was the learnings and the ability to test new things, and figure out what was happening. If that ability is not there, then that is something that we’re going to look to other areas to expand upon. Crypto is going to go through an evolution in the next five to 10 years, but I do think it’s here to stay. The question is in what form, and how does that play out, and what that does look like?

MoneyGram has been a leader in blockchain. We’re the first company in the payment space to use it at scale for a variety of different applications. We have a number of different projects underway that will allow us to play in this space in a variety of different ways, and so we’re excited about that. With or without Ripple, we want to continue to be a leader in crypto and in blockchain and be viewed as a payment company that’s differentiating itself through that capability.

More to come on that in the coming months, but definitely look forward to where we can go. We want to continue to be on the leading edge of new technologies, and that’s one of the most exciting things about our digital transformation: that we’re able for the first time in a long time to do some things very differently than we ever have before. We’re going to look to leverage that as we move over the next one to five years.

Trends in pricing

Daniel Webber: Finally on pricing, what’s your long-term view, particularly on digital?

Alex Holmes:

I have an ongoing joke with Larry, our CFO, about what we need to do to get a billion dollars of revenue. Larry would prefer to do one transaction worth a billion dollars, and I keep joking that we’re going to have to do a billion transactions for a dollar, and we need to be positioned to do that.

Technology has broken down a lot of barriers in a variety of ways. I still think cross-border currency management is one of the most complicated things in the world, and I think it’s going to continue to be that way because every sovereign, domestic market anywhere in the world, every country wants to protect its currency and wants to protect the value of what it does, and it wants to keep its borders safe.

So moving money cross-border is going to continue to be a monumentally complicated thing to do. On the flip side, we’re lucky to be a company that’s extremely good at that. I think we’re going to continue to pivot and push the envelope there. Technology is enabling us to do things faster, better, smarter, and at scale, right?

When you start to think about consumer direct, when you start to think about partners like different wallets, different digital partners, when you think about different applications of account deposit or you think about Visa Direct, think about crypto, blockchain, there’s a variety of different ways to approach it and a variety of ways to think about it.

Competition has increased. Non-exclusivity is on the rise, so you have to present your product, and you have to differentiate yourself in the customer experience. That there is an opportunity over time to price value into that. In the short term, prices coming down is forcing companies to change the value proposition to consumers.

That’s part of the evolution of what we’re seeing. I don’t think it’s going to go to zero and disappear. I think what happens is prices have to come down to a point where there’s a value-creating opportunity for consumers that they can understand and adapt. Then you can grow back.

It’s very similar to what you saw, in some ways, in telcos. It’s what you saw a little bit in phones and things in the beginning.

It was this expensive side of it, then there was this push down to almost free, and then you’ve grown back into, wow, it’s actually pretty expensive to have a phone. I remember the days when it was like you were going to get a free plan for years, and they’d throw a free phone at you. That stuff is dissipating now.

I think our industry’s going to do the same thing. What you think about the traditional cost of a remittance experience, is going to dissipate, but I do think there’s going to be value-added services that’ll lay on top of that, that’s going to then begin to add that value back. I think that evolution is underway, and I think we’ll see the outcome of that. It probably won’t be for the next five to 10 years, but I definitely think it’s part of that evolution and part of that forward flow.

The net of that is I think pricing will remain very competitive. I think it’s naïve to say pricing is stable. I don’t even know what that means. It’s confusing to me because there’s no market anywhere where prices are stable. I mean it’s not the nature of how business models work. It’s not how things evolve, and I think it’s a very self-serving statement that I just disagree with.

Daniel Webber: Alex and Kamila, thank you. A very nice conversation as ever. Is there anything else that you would like to add?

Kamila Chytil:

It’s definitely an exciting time. I always say that we just recently caught up and are now gaining share. When we do a customer survey, we know exactly where they’re coming from, and we know exactly why they’re picking up. It’s really around that customer experience, price and the value that they’re getting for their money. We know it’s working, and we’re in a bigger acquisition mode to really refine our marketing and make sure that we continue to fuel that growth, because we know what has worked over the last 18 months.

Daniel Webber: Great, thank you for the time.

Alex Holmes:

Thanks.

Kamila Chytil:

Likewise. Thank you. Take care.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.