Cross-border money transfers have always been extremely important to Southeast Asia. Now, a sector-wide push towards digitalisation, as well as the region’s efforts to boost interoperability to circumvent the US dollar, is changing the future landscape for money transfers.

Cash has traditionally seen heavy use across several countries in Southeast Asia, driven by a lack of easily accessible banking services. This, combined with the effects of Covid-19 restrictions, shifting migration patterns and economic challenges has driven growth of fintechs in the regions that are offering more accessible e-wallet and money transfer services via mobile apps.

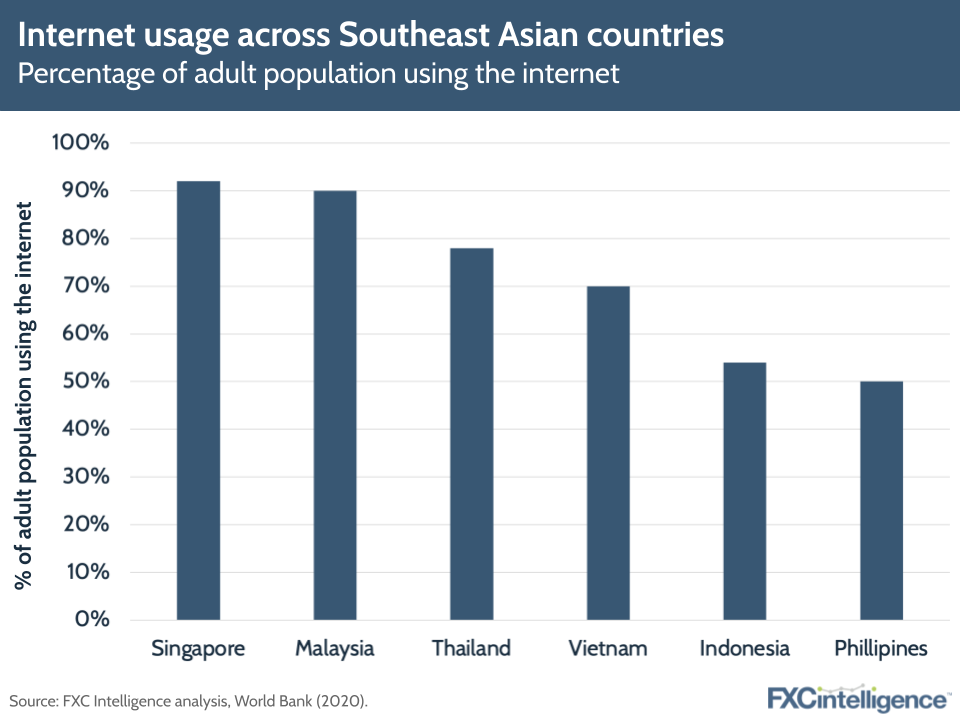

Southeast Asia is rapidly coming online, with a recent Google report stating that there are now over 460 million internet users across the principal economies of Vietnam, Thailand, Malaysia, Singapore, Indonesia and the Philippines – an increase of 100 million in the last few years. The pandemic has driven the use of more mobile apps and digital transfer services, which is shifting the power away from cash.

This report looks more deeply at the state of money transfers in Southeast Asia, examining what the key trends are now and how the landscape could change in the future.

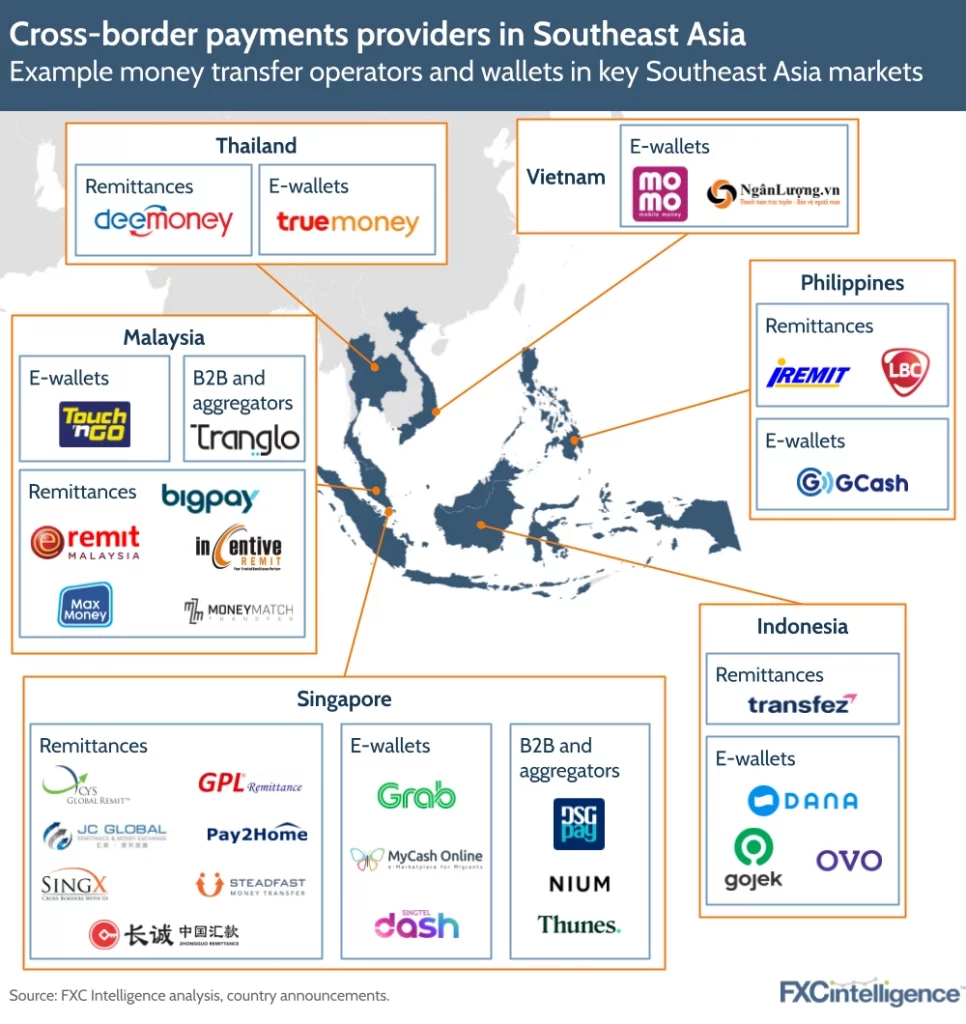

Key money transfer players in the region

The money transfer space in Southeast Asia is a mix of well-known providers and up-and-coming money transfer operators/e-wallets attempting to stake their claim on the region.

Much of the focus is based around Singapore, which is home to growing cross-border payments company Nium; B2B money transfer specialist Thunes; and mobile wallets Singtel Dash and Grab. As the region’s financial hub, Singapore has been a core focus for fintechs, but heavy migration across several Southeast Asian countries has created demand for faster, more effective transfers in the region.

Major names in the remittance space are also upgrading their products and launching new ones. For example, MoneyGram has now rolled out stablecoin-based remittances in the region, while Wise has updated its app in Singapore with a new feature that allows users to link their bank accounts, allowing them to transfer money from their account without having to leave the app.

MoneyGram, Western Union and Ria have made partnerships in the region to capitalise on the demand for remittances. For example, Western Union partnered with mobile app M Lhuillier to allow app users to receive international transfers and eventually be able to send money via the app. Visa also recently teamed up with Singapore-based Thunes to allow individuals and SMEs to move money internationally to 78 digital wallet providers, reaching 1.5 billion digital wallets across 44 countries.

Countries in Southeast Asia: The money transfer landscape

According to the World Bank, remittance flows to the East Asia and Pacific region fell 3.3% in 2021, following a 7.3% drop in 2020 (flows reached $133bn in 2021). However, excluding China, remittances to the region grew by 2.5% in 2021, and they are projected to grow by 3.8% in 2022. Meanwhile, the average cost of sending $200 to the region fell to 5.9% in Q4 2021, compared to 6.9% a year earlier.

How can FXC Intelligence’s market sizing data help my business?

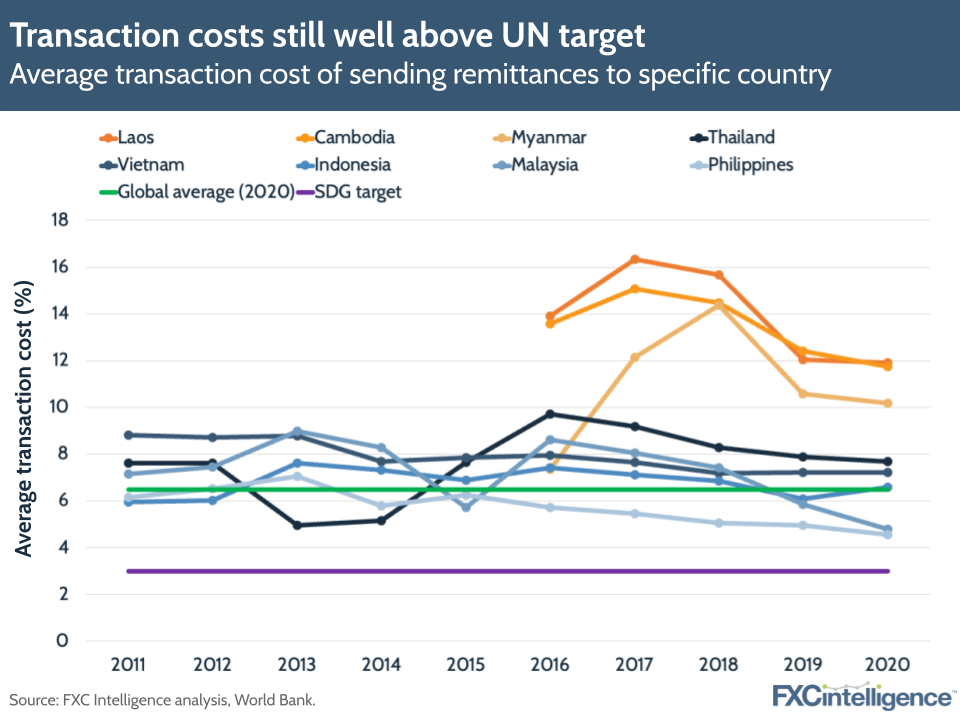

A key challenge for remittances will be high transaction costs. The global average transaction cost for sending remittances stood at 6% in 2021, which is well over the sub-3% being targeted by the UN’s Sustainable Development Goals. Costs are being driven up by standard banking channels for remittances, which have many intermediaries requiring fees in the process. As the graphic below shows, sending prices for remittances have been declining, but are still well above the 2030 target.

Learn how FXC Intelligence pricing data can drive your strategies

Another issue in the space, as it is elsewhere, is reducing the time it takes for consumer remittances to reach their destination. Transfers in some areas and with certain providers can take up to five days to reach recipients, and so much of the movement in the space (particularly with regards to crypto) will be about making remittances faster.

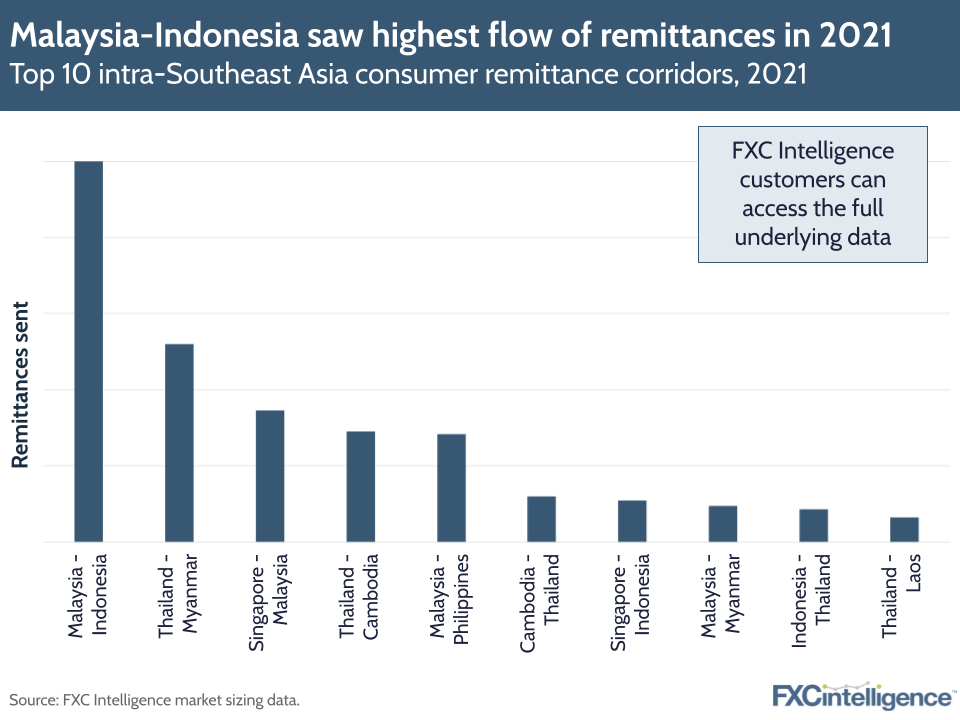

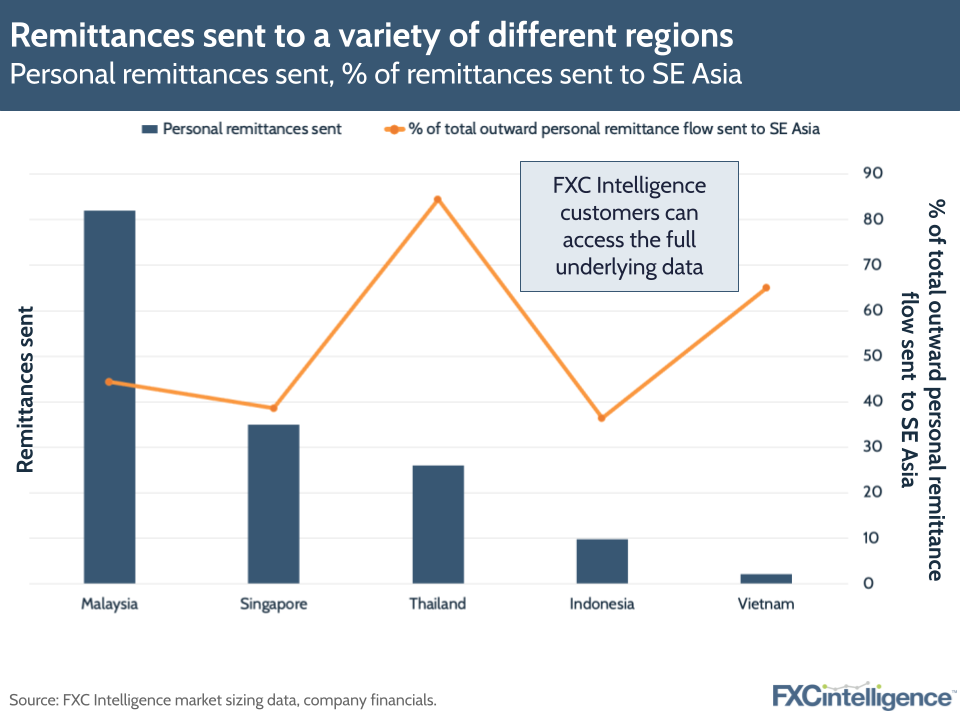

Remittances are also being sent to a variety of different regions for different reasons. Thailand, for example, sees 84% of its total outward remittances going to other countries in Southeast Asia, while for Singapore the number is 39%, according to FXC Intelligence data. Thailand, in particular, is a country that sees high amounts of migration from other Southeast Asian countries, particularly neighbouring Myanmar, which is its largest send location.

Access FXC Intelligence’s full data on remittance flows

Below, we’ve included key remittance figures and an explanation of the payments landscape in core markets in Southeast Asia, including Singapore, Indonesia, the Philippines, Malaysia, Thailand and Vietnam.

Singapore

In Singapore, digital payment methods are both accessible and highly favourable. Within digital payments, although traditional bank transfers and card payments have retained popularity, digital wallets such as GrabPay are seeing rising adoption in Singapore.

Singapore is rapidly moving towards a cashless future, a shift which has been building since the 1980s. The development of accessible digital payment systems, such as the local real-time payment platform PayNow, and involvement in Association of Southeast Asian Nations (ASEAN) QR cross-border payment linkage schemes, will further decrease cash use while increasing the adoption of digital payment and transfer methods.

Indonesia

Although traditionally cash-reliant, Indonesia is projected to be a key centre of growth for digital payments. Aided by a young, mobile-only population, mobile wallets are gaining widespread popularity in the country.

The banked population remains relatively low, and the introduction of the BI-FAST real-time payment infrastructure has amplified the accessibility of and movement towards digital payments. These factors are creating highly favourable conditions for mobile wallets, which could dominate the space in the future.

Philippines

Due to its large unbanked population, the Philippines has been heavily reliant on cash in the past. However, consumers are now moving in favour of digital payment solutions and mobile wallets, driven in part by Covid-19.

Although cash will likely remain popular, mobile wallets enable the unbanked population to gain new access to digital payment methods. In 2021, the Philippines was the fourth largest remittance recipient in the world. Rapidly growing mobile wallets, such as GCash, will increase the accessibility and speed of incoming international transfers, driving consumers further towards digital payments.

Malaysia

As one of the fastest-growing Southeast Asian economies post pandemic, Malaysia is highly receptive to technological innovation, an attitude which also applies to payments.

Malaysia has seen a recent and stark move away from cash, powered by a rapid growth in real-time payments transactions; between 2019 and 2020, the number of real-time payments transactions processed rose by 864% to 68 million. This increase was driven by the national programme DuitNow, which allows domestic transfers to and from mobile numbers.

Thailand

Digital payments in Thailand have seen substantial growth in recent years. The government payment project PromptPay, a real-time payment scheme adopted by various Thai banks, enables transfers via various e-channels using Citizen IDs or mobile numbers. This project has provided people in Thailand with easy and fast transfers, subsequently securing the place of digital transfers as a preferred payment method.

Mobile wallets have also seen sizeable uptake, aided by the country’s particularly high mobile penetration rates. The importance of cash for Thailand’s underbanked population persists, but digital payments and mobile wallets will continue to rise in adoption as these methods become increasingly accessible.

Vietnam

Vietnam’s underbanked population has historically led to cash dominance, with this popularity even reviving following Covid-19 restrictions. However, Vietnam’s young and highly receptive population has created a growing demand for digital payment solutions.

Mobile penetration has seen rapid growth in recent years, which has in turn caused an increase in mobile wallet adoption, particularly the e-wallet MoMo. In addition, the National Payment Corporation of Vietnam’s payment infrastructure has made digital transfers easier, more accessible and more popular.

Learn how our market sizing datasets can help your business

Money transfer trends in Southeast Asia

When it comes to money transfers, a number of trends are having an impact on the speed, cost and demand for money transfers in Southeast Asia, not least migration, the movement towards cash over remittances, digitalisation, cryptocurrencies and better interoperability around payment systems to support dedollarisation.

The role of migration

One of the biggest forces driving remittances in Southeast Asia is migration to other countries. Several Southeast Asian countries are on the World Bank’s list of low and middle-income countries, meaning migrants often seek out employment in countries with higher growth economies, more job opportunities and more stable local currencies that they can send back home.

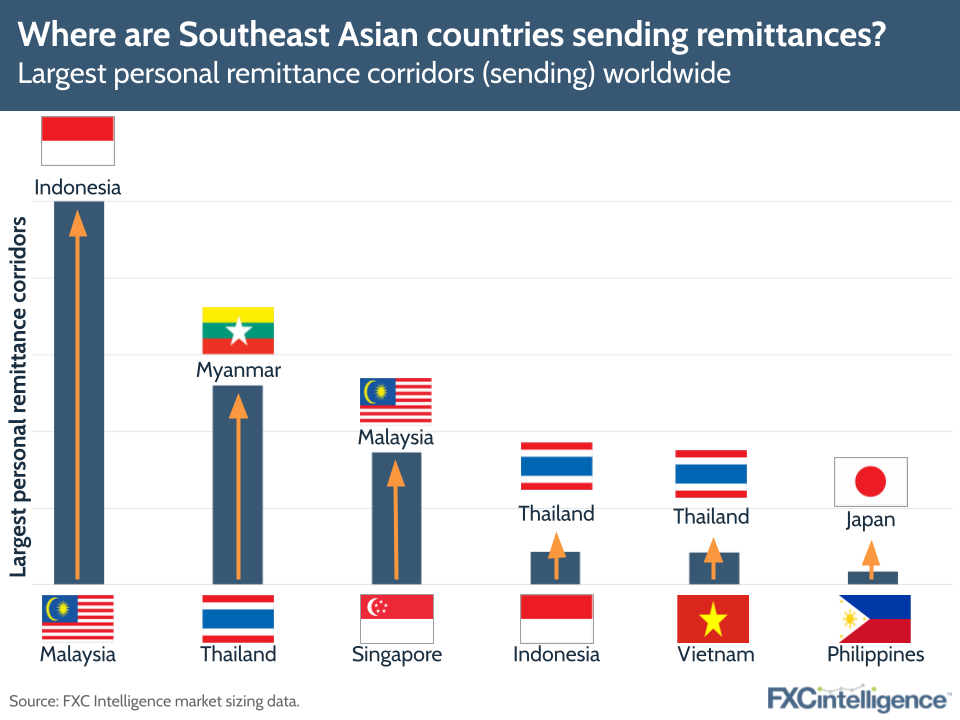

Movement between nations propels more inbound remittances and the growth of digital remittances is helping to make it easier for people in the region to send money back home. The Philippines, Indonesia and Thailand – all of which have high numbers of immigrants worldwide – are all included on our list of top 20 recipient countries/territories for international remittances for 2021, which was created using FXC Intelligence market size data.

Meanwhile, the Philippines, Timor-Leste, Cambodia and Vietnam are in the top 20 Asian international remittance recipient and source countries by share % of GDP (inflows). According to the World Bank, in 2021 remittances to the Philippines benefitted from job creation and wage gains in the US, which accommodates many Filipino migrants.

Aside from work reasons, some Southeast Asian nations see a higher proportion of movement due to the prevalence of national disasters and conflict. The Philippines, Indonesia, Cambodia and Vietnam were in the World Bank’s top 20 Asian countries by new internal displacements (disaster and conflict) in 2020.

Southeast Asian countries that depend on remittances actually see resilience in this sector during disasters and recessions. For example, across wider South Asia (excluding Vietnam and Singapore), remittances increased by 4.2% in 2021, despite the ongoing effects of the Covid-19 pandemic, according to FXC Intelligence’s market sizing data.

Lack of financial inclusion

Financial inclusion – i.e. the availability and accessibility of financial services – is a mixed bag across Southeast Asia. On the one hand, over 70% of Southeast Asia’s population is unbanked (with no access to basic financial services) or underbanked (underserved and face problems such as an inability to get credit cards, loans or adequate insurance).

On the other hand, the growth of financial services in some countries has led to much higher levels of bank account use. Singapore is one of the most financially inclusive markets in the world, with 97.55% of adults having an account with a financial institution, while this percentage is much lower in Indonesia (51.76%) and the Philippines (51.37%).

Due to a lack of financial inclusion, cash has traditionally seen heavy use in several Southeast Asian countries. Prior to the current digitalisation boom, many remittances took place informally, whether this is in handing cash to family members/colleagues/friends to bring abroad in person, or via organised informal money transfer systems outside traditional banking or remittance channels, such as the Hawala system.

Originating in India, Hawala refers to a system of payments made between a series of money brokers. The sender gives cash to a broker in one country, who pays it out to an intended recipient in another, with the broker in the originating country then indebted to the broker in the receiving one. However, the whole process is based on trusting particular individuals to pass money along the network, rather than banks or money transfer providers. In some areas this may make the process cheaper, but it also makes it less secure.

While banks might operate in the greater region, these may be particularly expensive due to the cost of correspondent banking. Meanwhile, some banks in the region are de–risking, i.e. closing their accounts with money transfer operators to reduce their risk of not complying with anti-money laundering regulations and combating the financing of terrorism standards.

This is where digitalisation comes in. The increasing penetration of mobile apps is decreasing cash use across payments, which could in turn help drive digital money transfers in the region. According to a McKinsey report, cash use fell from 97% of transactions in 2010 to 71% in 2019 across Asia more widely, and this trend is likely to continue even further, in Southeast Asia specifically, as digital wallets such as Alipay and QR codes become more normalised.

More could be done to overcome the hurdles presented by financial inclusion in affected countries. In particular, potential solutions revolve around designing outreach programmes for specific groups that are reluctant or uncertain about moving to digital methods. These programmes would focus on helping people understand how digital financial services work, as well as potential risks and how to manage data privacy. Work is already underway in this respect, with the ASEAN setting up a working committee to support financial inclusion initiatives in the region.

Increasing adoption of mobile money

The ease and accessibility of digital money payment and storage methods, as well as supporting regulatory initiatives, is driving the growth of mobile money apps in Southeast Asian countries. The GSMA reports that, across East Asia and the Pacific, 68% of the population was connected to mobile internet in 2021 (up from 41% in 2014).

The movement away from cash and towards digital is not only streamlining remittances for people in the region, but also creating more competition amongst digital players, which could help to reduce costs for money transfers.

Remittances via mobile apps are increasing as mobile phone penetration in Southeast Asia continues to outpace credit card and bank account penetration. Rather than receiving cash in person, users in Southeast Asian countries can receive money directly to their mobile wallets. For example, WorldRemit facilitates immediate transfers to OVO, LinkAja, GoPay and Dana mobile wallets, some of the leading mobile wallets in Indonesia.

Mobile apps for money transfers can also help to drive more reliable, easier and less costly remittance services for migrant workers sending money from Southeast Asia back to other regions. The impact of this was measured in an IFAD-funded experiment through Malaysian remittance app Valyou, which piloted an app tailored to migrant workers from Pakistan and Bangladesh between 2017 and 2020.

The Valyou app reduced the cost of sending remittances to rates significantly lower than the UN’s Sustainable Development Goals’ 3% target, and also reduced the use of over-the-counter remittances by three times.

The growth of superapps in the region

Asia has seen a rise of so-called ‘superapps’ in recent years; payments and spend management apps that run the gamut of financial services, from money storage and remittances to insurance and ecommerce payments. Integrating remittances within a ‘one-stop-shop app’ is powerful and could speed up the transition of many consumers in the region to digital money transfers.

The biggest example has been Chinese superapp WeChat, which began life as an instant messaging and social media app. Mobile payment platform Alipay, owned by Chinese financial services giant Ant Group, has partnered with southeast Asian fintech Tranglo to enable cross-border remittances through the app, in a bid to assist migrant populations in Southeast Asia.

Several mobile apps, including Singapore-based cab-hailing app Grab, are now expanding their offering to include remittances and other financial services. Some of the key examples of upcoming mobile wallets in Southeast Asia are included below.

Rising use of digital currencies

The move towards digitalisation in Southeast Asia is also spurring increasing use of digital currencies in the region. With regards to payments, Thailand, Vietnam and Indonesia currently do not allow crypto for payments, while Singapore has licensed some companies to use it. However, other factors are driving the adoption of digital tokens.

For example, Vietnam has the highest crypto adoption rate in the world, partly because crypto is not yet legal tender in Vietnam, meaning it is not taxed in the same way. Additionally, volatility in the Vietnamese currency (relative to cryptocurrency) means some are investing in it as a way to hedge against inflation.

Across unbanked nations, many of which rely heavily on remittances from migrants and are increasingly turning to mobile banking, crypto remittances could become a growing trend in years to come. Theoretically, blockchain technology could enable faster, cheaper and more secure remittances in the region, without banks or middlemen adding additional margins or exchange rates. Because a central clearing authority is not required (e.g. local agents), it’s predicted that crypto remittances could be faster and cheaper.

One company that has been increasingly expanding its presence in Southeast Asia is B2B crypto specialist Ripple, which recently partnered with Japan’s SBI Remit to allow instant transfers for Thai nationals working in Japan. The company is aiming to expand the reach of its On-Demand Liquidity product, which enables remittances using its XRP cryptocurrency over a blockchain network. Another example is cross-border tech company Velo Labs, which partnered with leading Asian fintech Inception to enable blockchain-based remittances across Indonesia, Malaysia, the Philippines and Singapore.

In a bid to formalise cryptocurrencies, some countries in the region are also looking to central bank digital currencies, creating a fiat-backed version of a digital currency that doesn’t need to go through the expensive correspondent banking system, and thus greatly reduces the cost of remittances. Such a system has been pitched by the Monetary Authority of Singapore in October, and similar schemes have been covered in FXC Intelligence’s recent report.

Dedollarisation and interoperability

Investors see the US dollar as the world’s reserve currency, so tend to flock to it during periods of economic uncertainty, selling assets held in other currencies and thus depreciating their value. This has an impact when sending cross-border remittances between Southeast Asian countries, as money is converted into US currency and then sent over and converted again into the native currency in other countries, leading to additional fees.

In recent years, some Southeast Asian countries have been taking steps to try to boost interoperability between their payment systems, thereby avoiding conversion to the dollar altogether so that they are not as badly affected by currency volatility. The biggest example is Singapore’s PayNow, which allows users to instantly transfer funds from one bank account or e-wallet in Singapore to another just by using their mobile number.

In April 2021, PayNow was connected to the Bank of Thailand’s PromptPay system, allowing people in both countries to send money between each other as if it was a domestic transfer. Prior to this arrangement, remittances would have to be sent via a wire transfer requiring the recipient’s bank details and account number, and could take up to three working days. However, with the new system, money can be transferred instantly using just a mobile number. Money is taken directly from the sender’s account in their local currency – this forgoes the conversion process, thus avoiding the FX fees involved with the transfer.

Similarly, ASEAN countries are working together to achieve greater interoperability in payments. A new partnership aims to allow users across Indonesia, Thailand, Singapore and Malaysia and the Philippines to pay via a QR code at participating retailers. The money would come out of the payer’s local account in their local currency and be settled in the merchant’s local currency – this could potentially lead to a more competitive exchange rate, as they are not relying on US currency. It also means cross-border transactions become straightforward, fast and simple.

In the past, increasing remittances in Southeast Asia has been difficult as countries in the region may have different regulations and systems around money transfers. For example, they may have different requirements for senders, or certain restrictions on payments from non-bank remittance providers. Encouraging greater interoperability between payment systems could help remove regulatory barriers and make it easier to send money between Southeast Asian countries.

Conclusion: Challenges ahead

The future money transfer landscape in Southeast Asia looks to be dominated by further movement towards digitilisation, with new and incumbent players already benefiting from partnerships with major money transfer players. The ongoing adoption of mobile wallets, driven by Covid-19, will likely continue as several key players in the region vie to be the next big ‘superapp’.

Southeast Asia is currently a hotbed for crypto adoption, but whether this takes off for remittances remains to be seen. Having said this, countries in the region want to better link their payment systems in a bid to remove their reliance on conversion to the dollar and create easier, faster and less costly transactions across their borders. This move could have important implications for money transfers in the region.

However, a number of key challenges remain for policymakers in Southeast Asian countries, including:

- Building financial inclusion and awareness of mobile money in areas where this is currently lacking to drive further use of digital methods and lead more people to step away from cash. While digital banking has seen strong adoption in countries like Singapore, there are still considerable gaps across rural areas of Indonesia, Thailand, Vietnam and Malaysia.

- Ensuring better regional coherence on strategies and policy around digital payments. In order to build more interoperable payment networks that will in turn enable easier money transfers, governments in the region need to have uniform policies to support these initiatives. For example, introducing common standards on data sharing, KYC regulations and fraud protection.

- Building data on remittances. Information on remittance flows in the region is difficult to ascertain, particularly as cash is still king and informal remittances are often difficult to track.

Money transfers will continue to be vital to markets in Southeast Asia, which is why it will be important (particularly amidst economically difficult periods) for countries in the region to work to reduce costs and transaction speeds. Doing this will involve a combination of regulatory changes, inter-region collaboration to drive competition and better reap the benefits of digitalisation.