Last week, the GSMA published a report discussing the potential of mobile money wallets in remittances. The organisation produced a case study on the development of the Malaysian mobile money-enabled app Valyou to send remittances to Pakistan and Bangladesh. Valyou was set up by the telco company Telenor, one of the world’s largest telecoms firms, and funded by the International Fund for Agricultural Development (IFAD).

Malaysia provided a good testing ground. According to IFAD, 15% of Malaysia’s workforce is made of migrants from other Asian countries and outbound remittance flows from the country totalled $10.8bn in 2019 (from World Bank data).

Our main takeaways :

- Mobile money wallets are helping to lower remittance costs

Valyou partnered with physical agents for cash-based operations but put a strong emphasis on educating its customers to send remittances digitally. Sending money through mobile channels is cheaper than doing so through agents (no surprise there). However, some market players might find it hard to replicate Valyou’s pricing, which was largely funded by IFAD (0.5% to send US$250-300) and still earn margins.

- New mobile data channels are opening up new opportunities

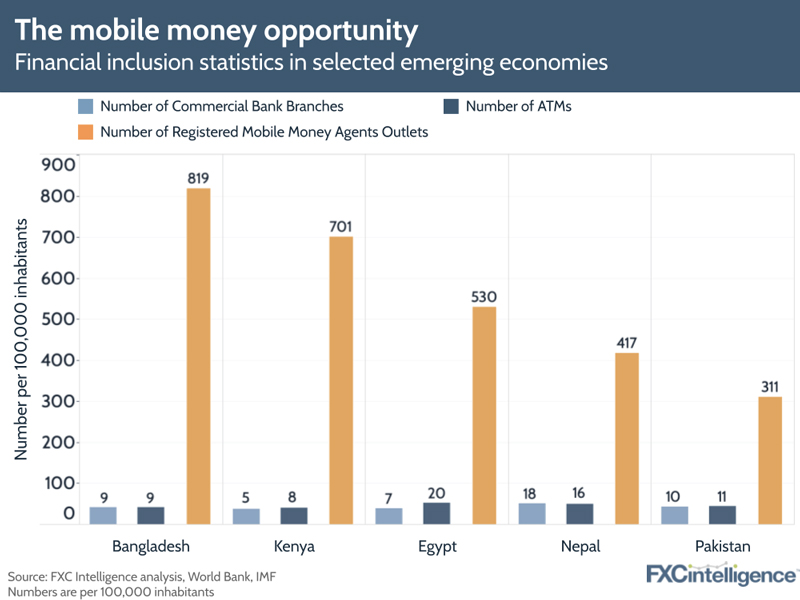

Mobile internet connection is still not available to 66% of the low and medium income countries’ population according to the GSMA. However, mobile money wallets are still accessible as funds are sent and received through the Unstructured Supplementary Service Data (USSD) channel, which works on basic cellphones. This significantly expands the potential reach of the service.

- The interoperability issue

Connecting Valyou to other Telenor-owned wallets in Pakistan and Bangladesh was facilitated by the telco. But other players might need third parties to integrate with telcos, and this might prove particularly difficult for new entrants lacking scale. The difficulty in connecting different mobile money wallets across the world is still a major barrier for the spread of such a method.

- Informal channels will be the biggest loser as mobile grows

The use of informal channels to send and receive money is still very common in emerging economies because of their proximity and due to the fact that no official documents are required. Mobile money wallets can facilitate remittances through official channels, while reducing costs and increasing certainty of delivery. Financial inclusions will also rise as a result.

Mobile money wallets are certainly a rising trend in the remittances market. However, technological and literacy barriers still exist that might limit the spread of such method and adoption is still very country-specific.

Sign up to our newsletter to stay up to date on industry developments