Following its recent analyst day, we speak to Flywire executives to find out more about the company’s verticals-based approach, future investment plans and the top trends in cross-border payments.

Since going public in May 2021, US-based payments solutions company Flywire has continued to show resilience in the face of post-Covid uncertainty.

In its latest analyst day on May 19th, Flywire revealed it has seen a 123% three-year average annual dollar-based net retention rate across its existing clients since its IPO, while adding more than 440 across its key verticals (education, healthcare, travel and B2B). It also extended services across three new countries and acquired WPM, a software provider that enables secure payments for universities and colleges in the UK.

With strong showings across its travel and education verticals in recent months, the company is enjoying continued demand for streamlined cross-border payments as Covid-19 restrictions ease. However, with the company’s stock price facing a new one-year low in June, the pressure is on to create new avenues for profitability in 2022.

Flywire is looking to expand into new markets while consolidating its strength across verticals with more investment in geographic expansion, new total addressable markets (TAMs) and a ‘strategic payables’ approach.

In this report, we speak to Flywire senior executives – including CEO Mike Massaro, VP of Global Payments Mohit Kansal, and President and COO Rob Orgel – to explore Flywire’s ongoing expansion, highlighting the key drivers for growth in cross-border payments and trends for the future in the space.

Flywire Q1 2022 earnings results highlights

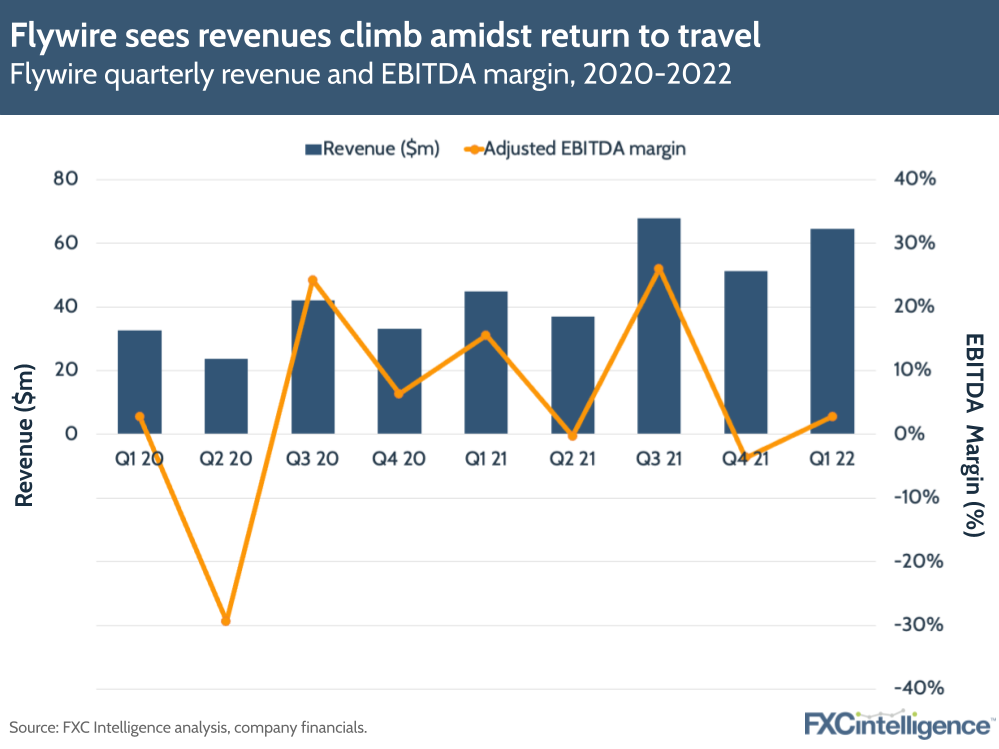

Flywire managed to beat its revenue projections for Q1, with a 43% YoY revenue increase to $64.6m in Q1 22.

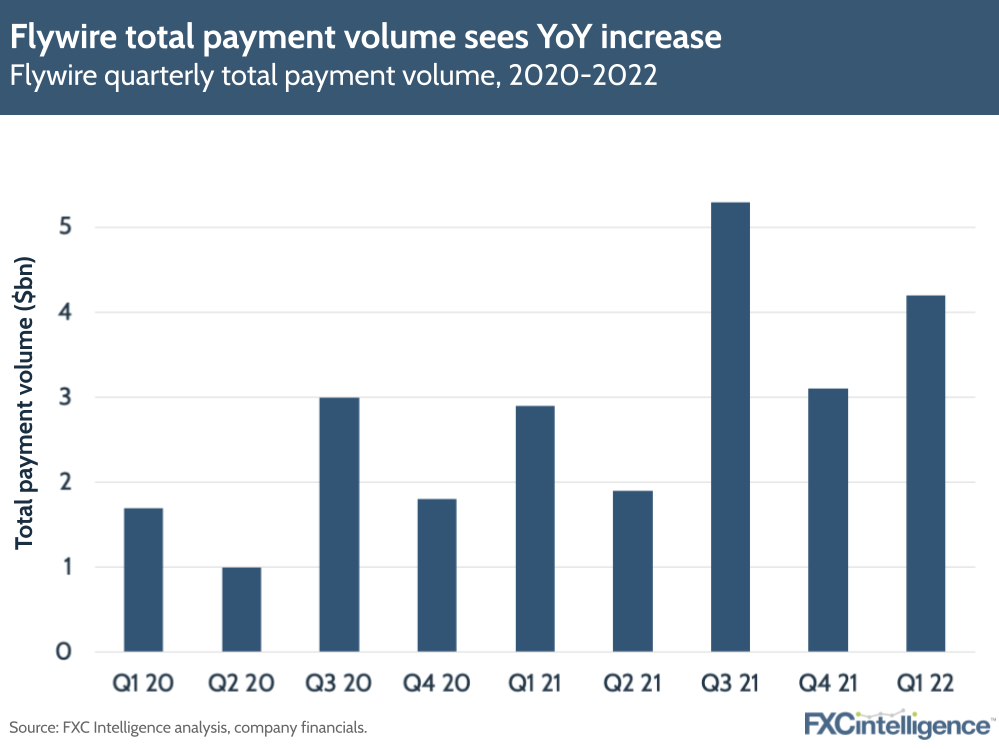

Total payment volume increased 46% to $4.2bn, with the company’s education and travel segments being key drivers for domestic and cross-border payments. This was largely attached to the easing of Covid restrictions driving higher travel spend and leading to a surge of international applications at US higher education institutions.

The company’s adjusted EBITDA declined by $5.2m (74%) YoY to $1.8m in Q1. Flywire said this was because it had increased employee numbers by over 50%, as well as increased costs from operating as a public company and travel-related costs.

The company also signed new cross-border partnerships, including with Adapt IT to streamline cross-border education payments in South Africa and the University of Connecticut to replace its legacy system for cross-border payments. It also announced a preferred payment partner agreement with Tribal Group, a leading student information system with over 1,400 universities in the EMEA and APAC regions.

Finally, Flywire also expanded its client base more than in any other quarter since it went public, adding over 130 new clients in Q1 2022 (40 of which are in the travel sphere).

Driving growth through verticals

Instead of taking a more generalised approach to the receivables space, Flywire continues to take a targeted approach across its main verticals – education, travel, healthcare and B2B.

According to the company, this allows it to tailor its payment software offering to these verticals, while building in diversification that protects the company against turbulence. Flywire says it has seen steady and diversified client growth, with no client representing more than 3% of 2021 revenue.

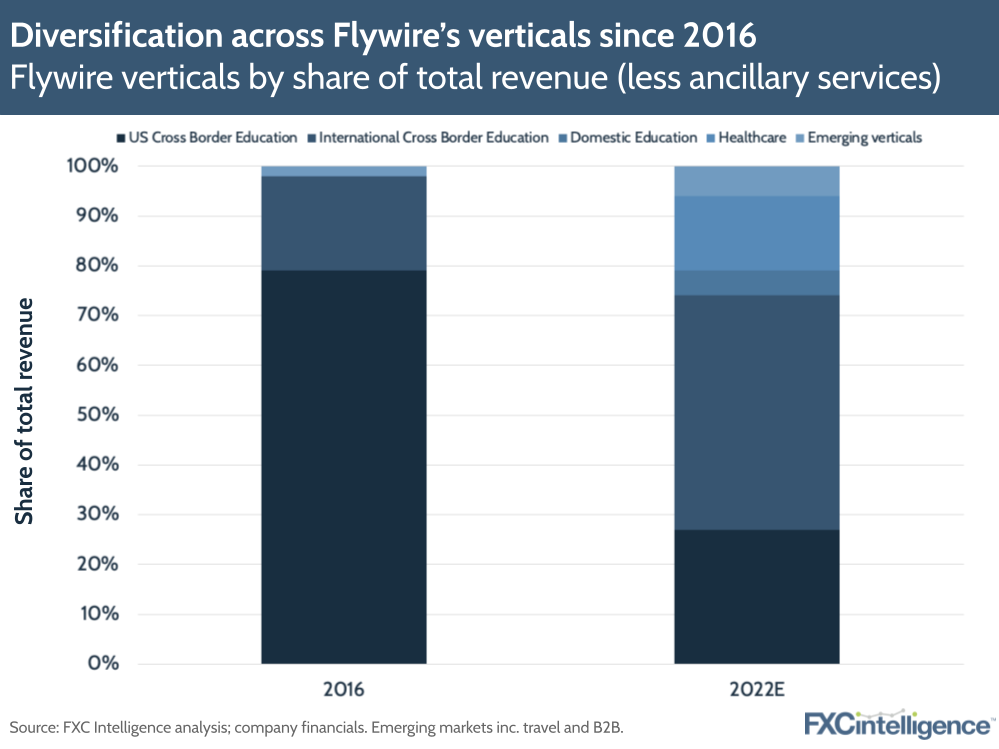

Since 2016, the company has increasingly branched out across verticals, with education going from representing 98% of revenues to an expected 79% in 2022, while healthcare and emerging verticals (including B2B and travel) are expected to represent 15% and 6% of the mix, respectively. Going forward, the expectation is that education will represent less than 50% of revenue in five years.

As well as carving out more space in healthcare and B2B, Flywire is also looking to speed up its global diversification efforts, with more than 50% revenue coming from non-US clients in 5 years. Already the company has seen its mix for cross-border education payments change, with international cross-border education expected to rise from 19% in 2016 to 47% in 2022, while US cross-border education is expected to drop from 79% to 27%.

Overall, the picture is of a company that is rolling with the momentum of markets reopening and now looking to expand its global network.

Differentiating Flywire’s payment solution

According to VP of global payments Mohit Kansal, a big part of what differentiates Flywire’s payment solution is the fact that it runs its payments software on a network that it owns and operates, without the need of an aggregator (like Stripe) to manage and process online transactions. He says this removes much of the challenges around issue resolution, allows money to move faster and has more visibility, as they are cutting out the middlemen.

The way he explains it, the network is based on “nodes”, which refer to the ways the Flywire platform is able to move money around the world (i.e. connections to bank accounts, alternative payment methods). It is these nodes that make the payments solution adaptable for both cross-border and domestic payments.

“It’s all plug-and-play,” says Kansal. “At a client level, we can decide which network node is used and which partner is used for that node. Client A could accept Euro payments through one card provider and client B could be seeing Euro payments through another card provider – same for bank accounts, same for APMs.”

COO Rob Orgel says that Flywire’s strength is that it can handle the complexity of domestic and cross-border payments, while having a proprietary platform that allows payers to pay using payment methods that are relevant to them.

“We can comply with Chinese, Indian, Korean, Nigerian [regulations] – or whatever the export currency controls are,” says Orgel. “We know how to very specifically guide a payer through whatever the requisite experience is, so that compliant payment will be successfully delivered on time to the institution of choice.”

Dealing with complexity across travel payments

According to CEO Mike Massaro, an ‘inherent seasonality’ across the company’s aforementioned verticals is driving consistent YoY revenue growth.

The company reported that it had added 40 new clients to its travel business in Q1 2022. Travel clients also delivered net revenue retention greater than 145% in the quarter, with particularly strong growth amongst European destination management clients.

“Look at the card schemes and the acquirers: everybody’s talking about the return of travel,” says Massaro. “It’s coming back quite strong for us and we really never took our foot off the gas when it came to adding more clients.”

Massaro says that the company’s focus isn’t on mass-market travel. Instead, it continues to look at those sub-segments that traditionally have higher transaction sizes for their services, such as larger rental properties, student housing and destination management companies.

Flywire is positioning itself as the payments company that helps institutions deal with complexity that arises from these high transactions, which can come with high costs, a lack of visibility or tracking and a high manual workload. Flywire says its solution can help mitigate these issues and provide a streamlined payments solution.

In addition, Flywire’s appeal is that it can offer travel clients the expertise that they might otherwise lack regarding things like cross-border payment regulations, negotiating, interchange and SLAs.

“Our clients want Flywire to deliver great software and take away the complexity around payments that nobody has previously helped them with,” says Massaro. “They don’t want just a credit card pay button. They want something that works for all methods, all countries and something that just offloads the complexity from them.”

The next evolution of education payments

Despite moving into other spheres through the years, Flywire still sees education as the key driver in 2022. In its analyst day presentation, the company confirmed that it has served 2,000 institutions and facilitated more than 50 partner and tech education integrations, while over 350 global education agent organisations use and refer Flywire to students.

According to Flywire, education institutions are often faced with many challenges and a fragmented marketplace when choosing payments providers. Flywire wants to solve the challenges that education institutions face when processing domestic and international payments, as well as inefficiency caused by multiple layers of student-facing applications.

At its analyst day, Flywire showed how it wanted to expand in various areas, moving towards supporting global agent organisations, as well as non-client receivables (for example, supporting payments for 529 plans, which offer tax savings on money sent towards future higher education expenses).

Moving forward the company is investing in new areas of education, one of which is a new pilot for living expenses for international students. Orgel suggests that these more payer-focused services could be expanded in the future to also include payments for things like student insurance, visas and travel related items.

“There’s an awful lot for us to do that actually is very helpful to the payers,” he says. “Because we’re trusted and we have their payment information, we can do two, three or four things for them at once. From the perspective of the lifetime value of that payer, it’s very good for us.”

Regarding upcoming trends in education, Massaro notes that lots of countries are continuing to modernise their payments experience, particularly in terms of KYC. Payments are moving online faster than ever, but regulations differ between countries and types of payment – for example, a P2P payment being sent from China might be different to one being sent to an educational institution.

Massaro says that this difference shows the benefit of having a payments solution tailored to education, as opposed to a generic payments solution that might be offered by another company.

“You actually have to have teams that understand those regulatory changes or that infrastructure type change in those countries and then adapt the software,” says Massaro. “Frankly, that’s what our clients expect us to be doing.”

Another trend Massaro mentions is affordability – with cost of living becoming a more pressing concern, the company is expecting to see more demand for software capabilities built around flexible payment plans and people with overdue balances.

Lessons for Flywire’s B2B expansion

When it comes to B2B, a key focus for Flywire is to integrate into client systems more easily.

Massaro says that although Flywire’s solution is built with vertical-specific software first and foremost, the platform’s components (e.g. single-sign on of existing platforms, all payment methods, banking infrastructure enabling cross-border payments) is shared between every vertical it serves.

The company is exploring the interface points across B2B, the systems being used by companies and how Flywire can minimise deployment costs and make it more seamless to integrate into those platforms.

“Similar to what we did in healthcare and education, I think spending the time and effort on having those system integrations is really important,” says Massaro. “Then you go into a client saying, ‘we know that system, we know how to get you live quickly’, and that’s a huge confidence booster versus just dumping it on them.”

B2B payments is still a fragmented space, with legacy systems that make payments longer and inefficient. Massaro says this is because much of the innovation in B2B has focused on enterprise resource planning (ERP) and digitisation, but payment experiences are still simplistic.

Massaro points to results in the company’s recent survey, which showed that 88% of businesses said the complexities of collecting cross-border payments impacts their ability to grow internationally.

“That to us is really encouraging,” he says. “It means it’s not just a cost priority for finance teams, but it’s actually an imperative for businesses to be able to go global, faster, sell other products in different places and get paid in different markets. We see a lot of businesses saying that slows them down if they don’t have a good way to get paid.”

When it comes to Flywire’s approach to targeting businesses, Orgel says that Flywire is mostly focused on technology and manufacturing-type companies with some level of cross-border payments in their mix, as that is where the company has a specific advantage.

“We tend to be looking in the hundred million to two billion range for revenue,” he adds. “So [they are] big enough to matter, but not so big that they figured it all out.”

Future investments for Flywire

Looking forward, Flywire is looking to further bolster its expansion efforts, increasing the size of its go-to-market team with the addition of more sales reps and relationship managers.

“We’re investing in the delivery teams and R&D to support our ambitious growth plans for the year ahead,” says Orgel. “There’s an incredible opportunity to fill in the go-to-market team across all of these attractive markets for us in Latin America. The story wouldn’t be very different if you looked across Asia Pacific, but we’re still early as we talk about covering AMEA.”

The company is also suggesting it wants to move from facilitating payments between payers and clients, to powering full vertical ecosystems, supporting strategic payables, non-client receivables and new payer services.

While expanding and consolidating strength in existing verticals will be Flywire’s short to medium-term goal, in the longer term, Orgel says, Flywire will be dipping its feet into the payables market in a strategic way.

He stresses that the company is not trying to compete with general payables companies, but instead looking at using Flywire to get ‘involved’ in the process where money moves ‘in both directions’ i.e. with commissions being taken on travel/education payments. He gives the example of a tuition payment that might be associated with a commission payment that goes back to the agent that helped facilitate a student’s experience.

“In travel, you may pay $10,000 to the destination management trip that helped arrange your trip to Iceland, but there’s going to be a thousand dollars going back to the host agency that actually put that trip together for you,” he explains. “Another $8,000 may go paid out to various suppliers that will help actually deliver that trip for you.

“We are trying to help move the money both ways, leveraging our software, client relationships and payment network, to be able to move the money in both directions.”

Cryptocurrencies and open banking

Kansal talks about how crypto presents an opportunity for the company, as it forms another payment rail, or ‘node’ that the company could add to its network.

If cryptocurrency does see more use in payments, there will be a number of issues that will need Flywire’s expertise, he argues – for example, integrating crypto payment systems with a client’s ERP, or invoicing crypto payments. Kansal says the company has already had long discussions about crypto and how to bring it onto the platform.

“Client and customer demand will decide when we put it on the roadmap, but we’ve gone into pretty deep conversations on how to do it,” he says. “What part do we want to do? What part do we not want to do? We’ve done quite a bit of research behind the scenes.”

Another trend Kansal mentions is open banking, which he sees as being driven by increased cost of living spurring increased interest in methods with low/no bank charges.

He also says that some clients (particularly those requiring cross-border payments) have been generally less focused on the different payment methods that are being enabled, and more how customers experience the payments process. In particular, being able to resolve payment issues fast has been a top priority.

“What most clients don’t do, at least for cross border payments, is to say, “My customers want this method in this country” he said. “I think for clients it’s the experience of the payment versus the payment itself.”

As Orgel sees it, the company has two main focuses for investment in the short-to-medium term: expanding the company’s global payment network, and investing in R&D.

“We’re building out things like the global payment network [to find out]: what does it take to be able to serve a South African client, be able to pay out properly in rand? That’s what we can continue to invest in so that we can take advantage of the global payment network and the products we have.”Orgel explains how Flywire will aim to further spread its travel, B2B and education business, all of which have huge TAMs that are still barely penetrated by the company. For example, education: with an estimated TAM of around $660bn, the company says it has only seen 7% penetration across 18,000+ colleges and universities.

Going public: Growing profitability moving forward

With all this new investment, what will this mean for the company’s profitability moving forward? Being a public traded company comes with additional pressure from investors to continue to show year-on-year performance, which can require a careful balancing act.

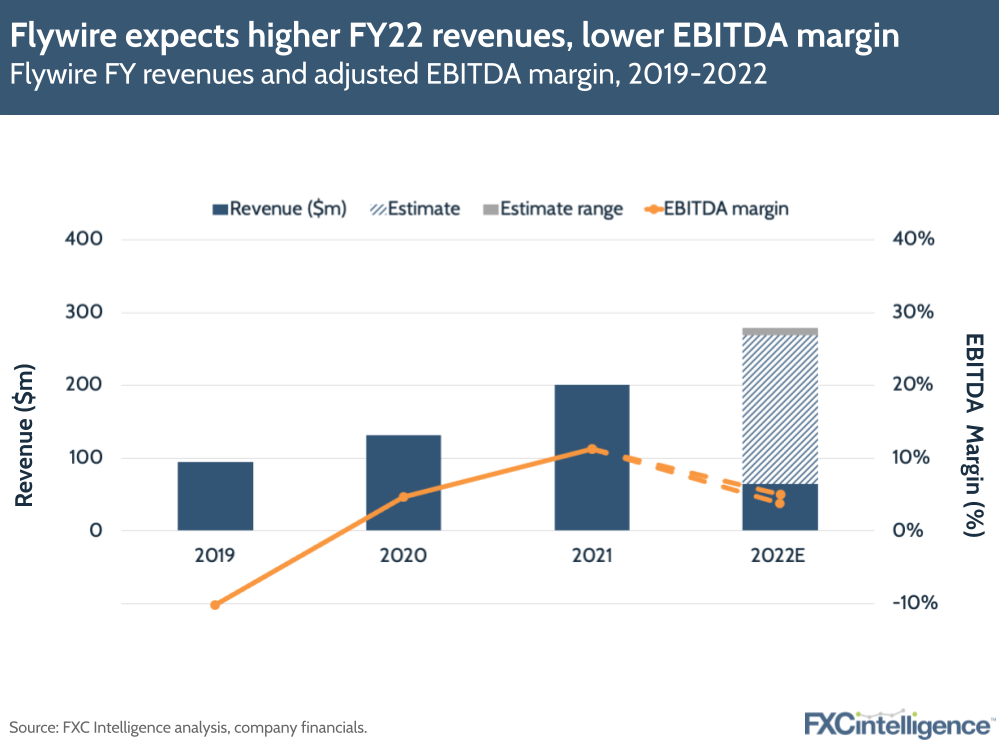

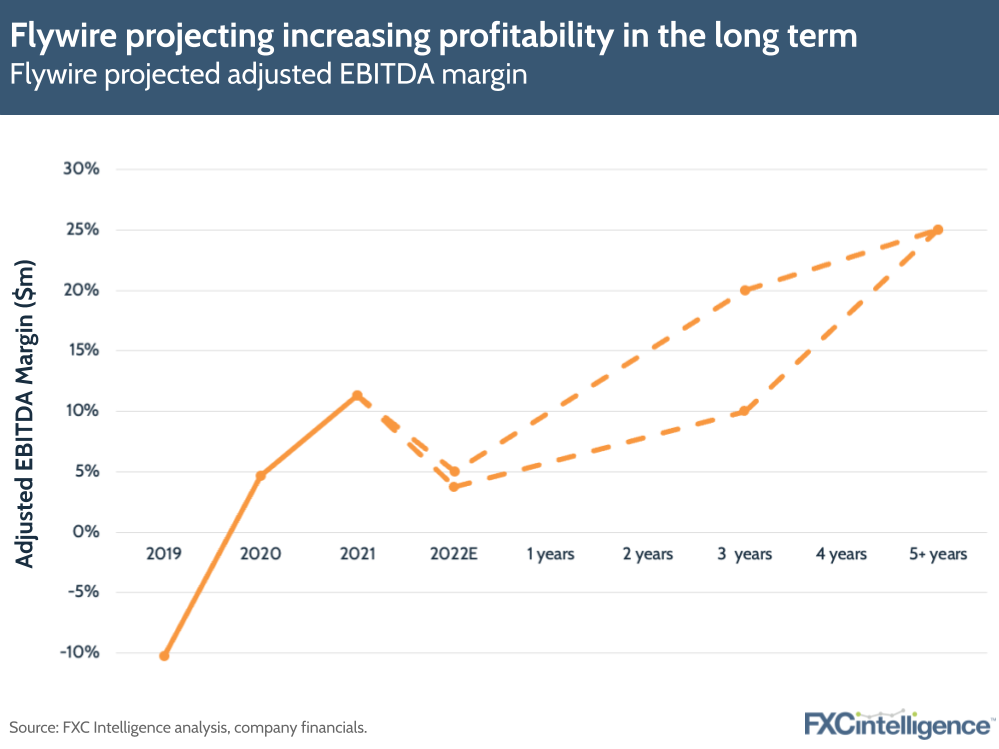

In terms of Q1, Flywire’s EBITDA margin has decreased from 15.8% in Q1 2021 to 2.8% in Q1 2022. In its Q1 results, the company has pitched its expected revenue at $269m-279m and adjusted EBITDA at $10-14m – this means the company’s expected adjusted EBITDA margin is sitting between 3.7-5%, lower than 11.3% in 2021.

However, looking forward, Flywire expects momentum to build as it strives to “build a global payments and software leader”. The company is expecting to yield a 10%-20% adjusted EBITDA margin in the medium term (2-4 years) with this rising to more than 25% in the long term (4-5+years).

Massaro says that even though the company is moving towards investing, he is not tonedeaf to the shift in markets to showcase growth. He says that he believes the company can keep spending tight while continuing to grow profitable.

“We’ve never been a company that aggressively spends or has to spend to grow, right. We’ve got a really good financial model, and so we’ll be smart with our investments, but want to invest throughout the years,” he explains.

“That’s why we’re here: not to run the business on the priorities of today, but really trying to focus on running a really good company with great financial metrics, but also one that grows.”

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.