With high revenue retention and travel continuing to rise, software and payments platform Flywire has had a solid end to the year. In the latest in our Post-Earnings Call Series, we discussed the latest growth drivers in 2022 and the future strategy with CEO Mike Massaro.

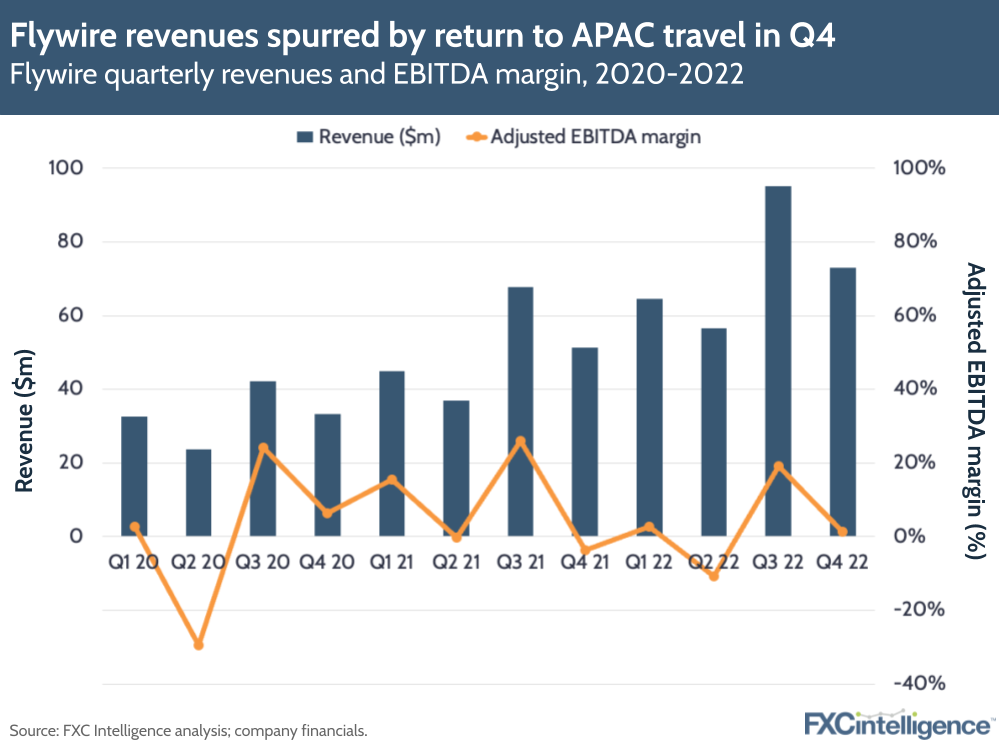

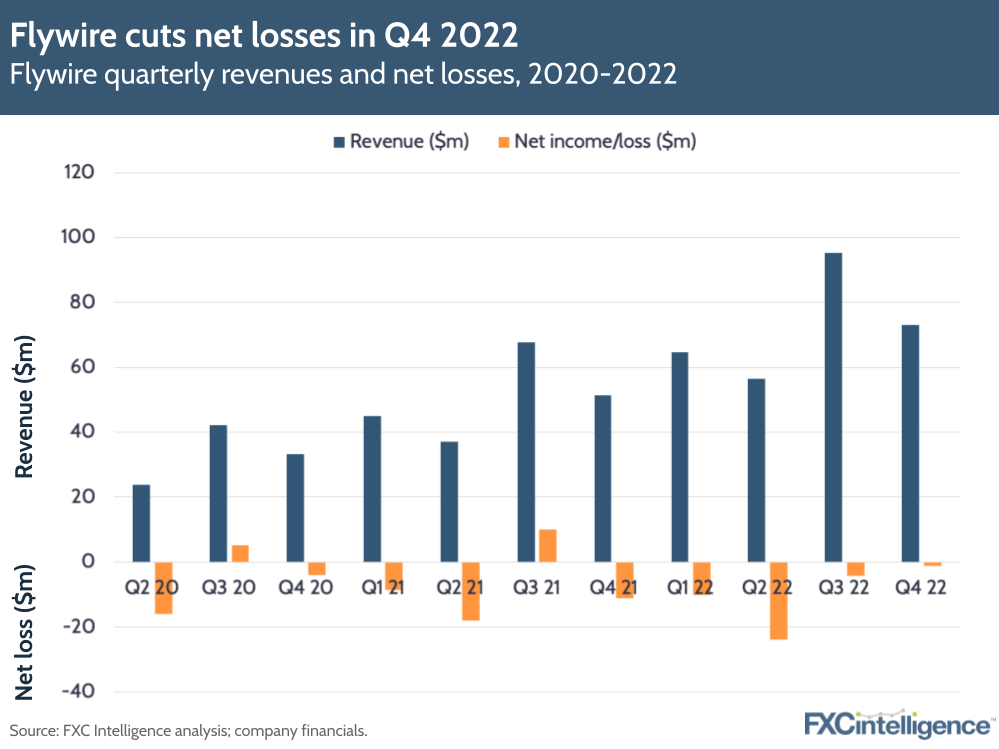

Flywire’s revenues increased 42% to $73.1m in Q4, while revenues for 2022 rose 44% to $289.4m. Nearly two years after its IPO, the payments and software company is continuing to see growth across its diverse set of verticals, which include education, travel, B2B and healthcare.

Total payments volume increased 37% to $18.1bn in 2022. This was spurred by a return to travel, particularly in the APAC region, as well as education, which Flywire continues to scale through its integration of student payment platforms Cohort Go and WPM.

The company’s adjusted EBITDA declined 34% to $14.9m. This gave an adjusted EBITDA margin of 5.15%, down from 11.29% last year, but still in line with Flywire’s revised projections.

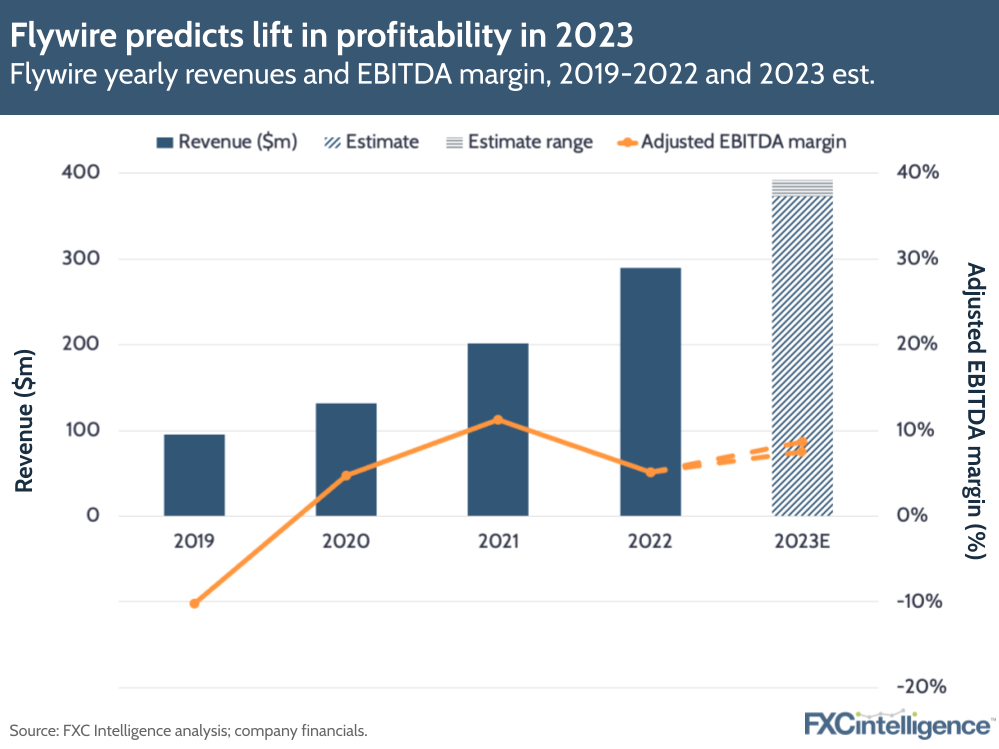

Executives predicted that FX headwinds won’t have the same impact on revenues in 2023, which will see the company invest more in its go-to market strategy and tech partnerships. Flywire is expecting an annual revenue of $373m-392m and an adjusted EBITDA of $28m-34m, giving an EBITDA margin of around 8-9%.

Daniel Webber spoke to CEO Mike Massaro to find out how Flywire is planning to achieve these goals in 2023, as well as how it is positioning itself as a public company.

Flywire revenue growth drivers in Q4 2022

Daniel Webber:

What were some of the key drivers for revenues in the last quarter?

Mike Massaro:

We saw really great performance across all industries. We talked about some pretty amazing statistics, including tripled revenue growth in our travel business last year. With Asia opening up, not only are travellers from Asia able to move around the world a bit more, but destinations in Asia where we have a lot of clients for travel started to come back in Q4. It sets us up well for 2023.

We finished the year strong, with really strong numbers across the verticals, and we also talked about WPM in the UK, which has over 40 clients signed. We really exceeded expectations around the number of clients that would’ve signed on for the integrated solution in year one, which is another big area of growth for us.

Measuring Flywire’s success

Daniel Webber:

What’s the right profitability metric for your business? You have a mix of software and payments, which is not always easy to compare to others.

Mike Massaro:

We continue to tell people to focus on that revenue growth number, [where you see we have] 30%-plus organic compounding growth. As you look at gross profit, which is again a 30%-plus percentage, that’s really a way to focus.

If it’s adjusted gross margins, those become an output to the payment methods and the industry mix will move those numbers around slightly. But we really focus on great gross profit in driving revenue growth, which obviously leads to the strong adjusted EBITDA that we’ve put forward as well.

Trends in education payments for 2023

Daniel Webber:

What trends are you seeing on the education side of your business?

Mike Massaro:

You’re starting to see a return to normalcy, just because there’s different parts of the world still coming back. You’re starting to see some countries get to pre-pandemic levels of international student numbers. You’re seeing Australian universities open back up again. That’s been a really positive trend just around Asia.

As more people are moving around in Asia than they were last year, 2023 is going to be a big year for both education and travel inside Asia. I mentioned the WPM integrated solution, with 40 [clients] being an exceptional number last year. Now it’s about getting all those clients live and getting the value driven through the integrated solution this year. Of course, we’ll add more and get more live. But it’s really a shift from educating our clients about the integrated solution to now delivering it and driving the value that we know the software could drive.

You’re also seeing continued strength in India and some improvement in China, if you look at visa numbers from those two countries. Those are encouraging even though, obviously, there’s a lot of macro challenges still going on in the world.

Increasing spend for existing customers

Daniel Webber:

Your average annual dollar-based net revenue retention (NRR) was 124% in 2022. How will you continue to evolve your product offering to drive that moving forward?

Mike Massaro:

NRR strength is due to the confidence we have in all the different ways in which we can do more with our customers. It could be geographic expansion; it could be sub-sector expansion within a client; it could be deploying a new product, such as going from just cross-border to domestic. It can be deploying the Agent Platform, which is another big product advancement that we have.

It’s coming from the core functionality that we have and our ability to identify areas of new use cases. For example, we continue to hear about overdue receivables, where companies have got to go back and try and collect funds they’re owed, but maybe 30, 60 or 90 days late. It’s amazing to hear about all the different processes that clients have for how that is handled and why it’s so different to how they normally get paid in their accounts receivable (AR) process. So, we keep finding opportunities where you can take the same functionality we have, make it available to a different team and a client and help them collect back hundreds of thousands of pounds.

As you hear more of those case studies, the NRR becomes more tangible. People realise you have new products and get new verticals, new industries and year-on-year growth. You have all these things that are helping drive clients doing more and more with Flywire.

Flywire’s growing travel segment

Daniel Webber:

How is your travel segment evolving? And how is that different to education?

Mike Massaro:

In some ways it’s similar to global business. There are 30-plus countries where we have clients, and it leverages our ability to process payments and the network that we have that’s accessible to all the verticals, so in many ways it leverages a lot of the same assets.

But the go-to-market model is focused on the three sub-sectors: accommodations, luxury tour operators and destination management companies. That’s a big shift in just travel in general. If you think of how our parents would’ve booked travel, it would’ve been with a travel agent down the street and they would’ve worked with them to set up their whole trip. Now, you’ve got all these places around the world and all these unique experiences, and the experts are actually not down the street anymore. They’re in the country that you’re going to explore.

So, we have to target those types of relationships digitally, whereas our core education business or healthcare businesses are more of an in-person and a conference go-to market sales motion. You’re typically building somewhat complex relationships, where you may have five or six or 10 different people inside a university that know about your solution who you need to help educate. It’s the same with hospitals.

Inside a lot of these travel companies, you may end up meeting the owner, or a director of finance or someone that’s on the AR side, and they may have the full authority to make that decision, implement the software and move quite quickly. The way in which we build the pipeline is a little more digital, similar with B2B, and the beauty is the speed in which we can build that pipeline, sign up customers and get those customers live.

So it is a different sales motion, but it’s that same digital demand gen aspect that we’ve refined inside travel and B2B, and which is going to help us strengthen the education market over time, because you’ll see buyers in that market look to digital as a way to get educated on new products, offerings and capabilities.

Penetrating the fragmented B2B payments market

Daniel Webber:

The B2B market is still fragmented. Where do you see your product fitting in on the B2B payment side?

Mike Massaro:

We’re on the receive side, which differentiates us a lot in the B2B payment sector. We announced a deal with FranConnect, which is franchise payments, and when you hear about it, it’s so clear why somebody like Flywire would be successful in that type of subsegment.

Again, you have an annualised or quarterly invoicing process occurring. FranConnect has a technical solution, almost like a CRM ERP-type system of record, and our ability to enable that with payments means that you can connect clients and automate global franchising businesses from an AR perspective.

It’s a great example of exactly what we do: find technical partners or channel partners like Bank of America or Huntington Bank, and really put our solution in front of clients that are already experiencing the pain of getting paid all around the world and how difficult that is to manage. The direct team, the channel team and the technical integration partners – that’s really our model, all focused on the AR side.

Daniel Webber:

So normally the customer looks to their traditional bank to solve that problem, rather than a fintech?

Mike Massaro:

That’s right. The bank can either help them find a solution that can solve this problem or they’re going to look outside the bank.

Bank of America’s one of our banking partners. We’re an infrastructure player that they can leverage, where they may not have a footprint in many of the markets around the world that their clients are trying to collect funds. With Flywire, they know that they’ll keep it inside their ecosystem and deliver value for their customer, so it helps strengthen that banking relationship when they bring in a solution that can actually solve a real problem.

Instead of that business having to go and find another bank, they can leverage the Flywire solution partnered with their primary bank to enable them to collect money in more locations.

Positioning Flywire in the public market

Daniel Webber:

You don’t have a straightforward competitor. How are you helping investors think about how to position Flywire within the public markets and others you want to frame against?

Mike Massaro:

Coming up on our two-year anniversary of being public, we knew the education process of a public company is anywhere from 12 to 24 months. And we feel like we’ve been out there doing a lot of education. We’ve seen a lot of the investor base turnover and we have a great set of public market investors that have realised that we have a unique offering.

We’re quite comfortable having public market investors need to get to know us and then understand the revenue model and that balance between transactional and platform-based revenue. The more people see us grow profitably, the more they understand the power behind the model and the earnings potential that this business has in multiple years. The more investors are educated about that potential and see us execute quarter-on-quarter, the more good things will happen. It’s about telling the story.

For us, we’re fortunate. In many ways, the grow-at-all-cost model was never who we were as a business. The strength of the model is in this compounding growth and in revenue growth you can get from the existing customers. It fits really well with what investors are looking for, which is someone that can grow with strong adjusted EBITDA and can go after a global total addressable market. There’s so many companies that can’t do that.

People can look at Flywire and see that we’re already in 30-plus countries. We’ve proven we can go after the global total addressable market for our verticals, and we’ve had strong numbers, with 47% growth in revenue less ancillary services last year (57% constant currency growth). To do that with adjusted EBITDA and margin expansion, which we guided to for this year, hopefully people understand the earnings potential that is there in the future.

Impact of the current macroeconomic environment

Daniel Webber:

What are your thoughts about the macroeconomic environment?

Mike Massaro:

When it comes to the macroeconomic environment, our industries are traditionally more defensive in nature and less tied to direct consumer spending. Even the travel sector’s a bit more of a luxury experience, rather than ad hoc travel that may be impacted by changes in certain economies. It’s stuff that’s often planned ahead of time and often by people with the means to make it happen. So we’re not overly impacted on the macroeconomic side.

Obviously, our team’s impacted. As inflation increases around the world, you get FlyMates who are impacted with different macroeconomic or geopolitical challenges, and so we’re not immune to those things. We have 40 nationalities within the company, so we get people experiencing a lot of different things on a daily basis.

When it comes to other things that can have an impact, it’s really the movement of people across borders. The travel and the education aspects to it are the macro things outside of our control, but which have the ability to impact our business.

Daniel Webber:

Anything else you’d like to share?

Mike Massaro:

We’re still hiring, which is probably a bit rare. We’re always very selective in bringing new people into the company, but in a time in which you see a lot of companies shrinking significantly, we’re being smart and very targeted about how to bring new FlyMates into the business to keep growing and investing in the right area.

Daniel Webber:

Mike, thanks very much.

Mike Massaro:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.