Remitly exceeded expectations in Q3 2024, with record customer growth driving revenue and contributing to the company’s first profitable quarter. We spoke to CEO Matt Oppenheimer to find out what’s driving the company’s success and its strategies going into Q4.

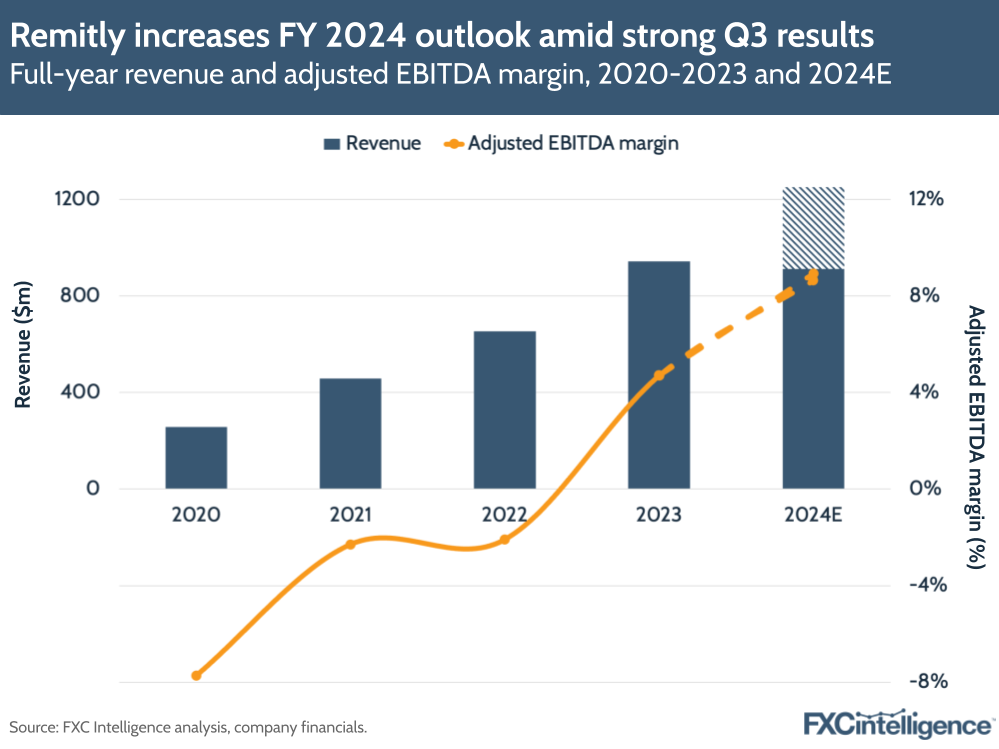

Remitly saw one of its strongest quarters yet in Q3 2024, with revenue rising 39% to $336.5m, contributing to a 345% rise in adjusted EBITDA to $46.7m – a new record for the company and a higher EBITDA than it delivered for the entirety of FY 2023. This delivered an adjusted EBITDA margin of 14%, the first double-digit margin Remitly has seen as a public money transfers player.

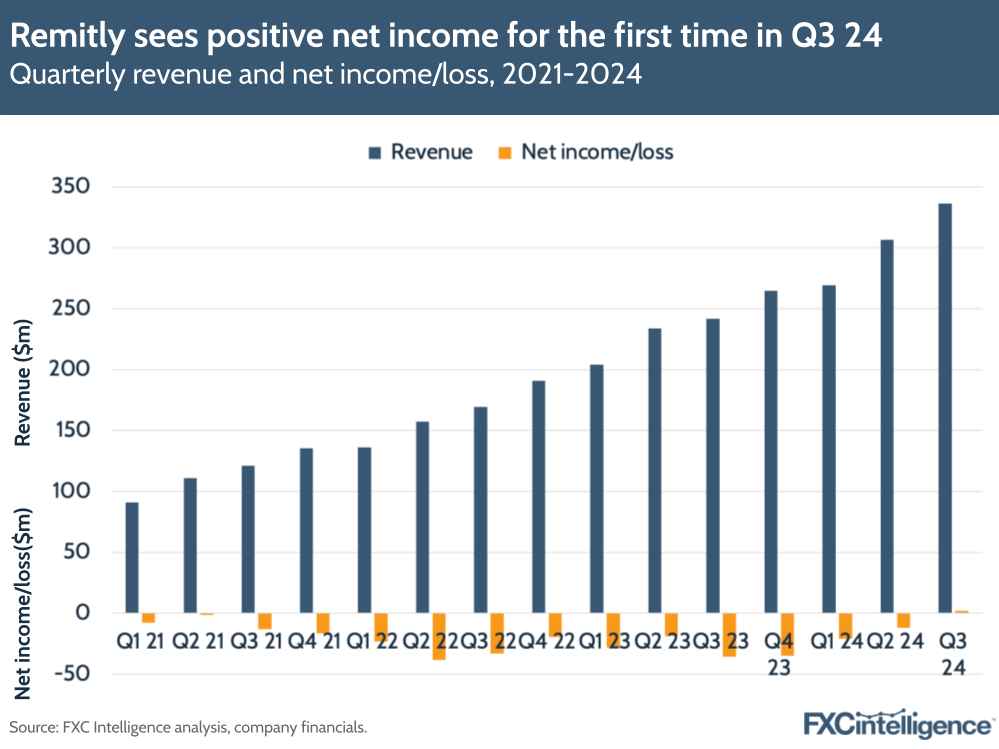

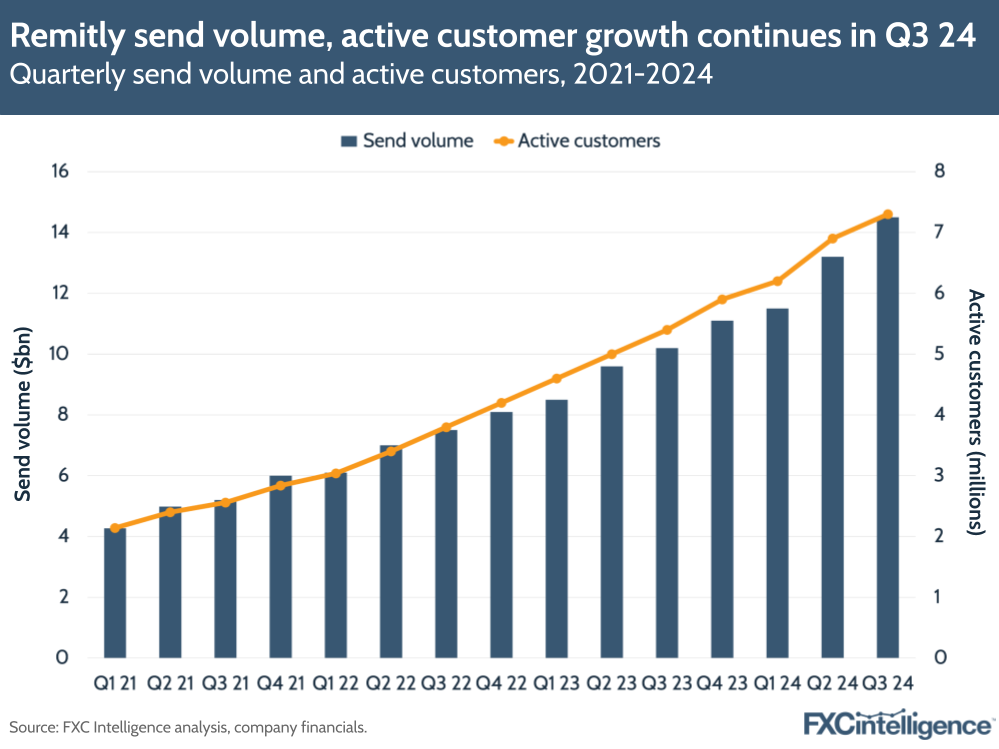

Results were driven by a record number of new customers, contributing to overall send volume growth of 40% – five times the market growth rate, according to Remitly – as well as FX tailwinds in some markets. For the first time, the company also recorded positive net income, which stood at $1.9m for Q3 2024, versus net losses of $35.7m in Q3 2023. Investors responded accordingly, with the company’s share price growing by more than 20% the day after results were announced.

Remitly attributes its continued growth to factors including its digital-first approach, disciplined corridor expansion strategy and continued focus on marketing efficiency, which is helping the company attract new customers while it retains its existing ones. As a result, the company grew its share of the $1.8tn remittances market to around 3% during the quarter, up from around 2.5% in Q2 2024.

Remitly is now continuing to diversify into other segments, including seafarers (which it spoke about last quarter), high-dollar transaction centres and micro businesses. Beyond raising its FY 2024 projections to 32-33% revenue growth, the company has projected a low to mid-20s revenue growth rate for 2025, which it said was based on customer cohorts, past trends and taking a “prudent view” of the company’s situation.

To find out how Remitly continues to outpace the competition on growth and elaborate further on its latest strategies, we spoke to the company’s CEO, Matt Oppenheimer.

Drivers of Remitly’s top-line growth in Q3 2024

Daniel Webber:

Your latest results are way above the growth of the remittance market. Take us through what’s driving these.

Matt Oppenheimer:

We’re really excited about our third quarter. If you start with our customers, we had 7.3 million quarterly active users just within that quarter, and the service we’re providing is incredibly important. The product that we offer to our customers is continuing to go from strength to strength in terms of reliability, speed and cost.

That resulted in 39% YoY growth to $336.5m in revenue for Q3. That 39% YoY growth is something that we’re incredibly proud of, and we’re continuing to get leverage in terms of overall profitability.

We saw our first ever GAAP net income-profitable quarter and $46.7m in EBITDA. We’re really excited about all of those things and, as we often say internally at Remitly, given that we’re 3% of the market, we’re just getting started.

Q3 was stronger partially because if you look at just the broadly developed currencies – such as the dollar, euro and the pound – these strengthened broadly compared to developing currencies.

That affects things just on the margin, but it does also mean customers can get more of their hard-earned money home back to their families, because they can buy more pesos per dollar or rupees per dollar etc. Our customers know how far those funds go in their family’s lives, and so it might pull forward a bit of demand in terms of sending more money when they perceive rates to be good.

Remitly raises projections after strong Q3

Remitly’s 39% revenue growth was consistent with previous years, but where it really saw a difference was in its record adjusted EBITDA and EBITDA margin.

On the back of its results, Remitly has now once again upgraded its guidance, and now expects revenue to grow between 32-33% to $1.250bn-1.254bn, with adjusted EBITDA expected to rise to between $108m-112m, giving a margin between 8.6-8.9%. This would be more than double the adjusted EBITDA seen last year ($44.5m) and nearly double the margin (4.7%), showing that Remitly is continuing its shift towards profitable growth.

Key to the results has been the company’s achievement of $1.9m in net income, which highlights the shift towards profitable operations, even amid growing costs and expenses for the company.

How Remitly is growing operating leverage as it scales

Daniel Webber:

You also highlighted your improving operating leverage through the metric revenue less transaction expenses (RLTE). Talk us through what you’re trying to show with that.

Matt Oppenheimer:

RLTE is an important metric because basically that’s revenue less a lot of our variable costs, and so it’s more correlated with lifetime value, which is a metric that we talk a lot about from a unit economic standpoint.

That grew 42% year-on-year because of the fact that as our business gets more scale, we have more leverage to bring down some of those variable costs. By looking at the long-term trend of RLTE, we’ve got a lot of confidence that we can continue to deliver RLTE dollars as we continue to grow the business, drive down costs and serve more customers.

Daniel Webber:

What goes into these variable costs or transaction expenses?

Matt Oppenheimer:

Some of the things that go into transaction expenses are things like how we collect funds, so that could be a bank account, a debit card or a wide range [of methods] across the 30 countries we originate funds from. There is a cost associated with us collecting those funds, which is obviously variable depending on how many customers are using our product.

Then the disbursement side has another large variable cost. Over 90% of our transactions are delivered in less than an hour.

The way that we are able to do that is because we have many partnerships that we’ve built out in our distribution network, which gives us access to five billion bank accounts and mobile wallets, as well as over 400,000 cash pickup locations. We can do that 24 hours a day, seven days a week because we’ve done direct integration with financial services institutions across the globe.

In order to deliver funds that quickly, we pay those financial services institutions a fee to disburse those funds instantly and to have a direct integration with the network we’ve built. So funds in and funds out are two of the larger variable costs.

As we get more scale, the great thing is we can drive down costs in the industry. Having done this for close to 14 years, I can tell you the deals that we got when I said, “hey, we’re going to send you 50 transactions next month” versus [those now with] millions of transactions flowing through our platform.

We can then therefore make a separate decision on how much we let flow through to the P&L versus how much we pass along savings to customers. Because that’s also an important part of our mission: to make sure that we’re offering a fair and transparent price to our customers. The good news is we can drive down some of those variable costs of funds in and funds out, which are two of the larger ones.

Remitly sees positive net income for the first time

Remitly has seen its first profitable quarter in terms of net income, which reached $1.9m in Q3 2024, compared to a net loss of $35.7m in Q3 2023. The company’s successful revenue growth has outweighed its total costs and expenses, despite these rising 21% to $336.2m.

Of these, the biggest costs to Remitly are transaction expenses, which rose 35% to $115.6m in Q3 2024 and account for 34.3% of costs and expenses overall. However, the company noted that RLTE grew 42% to $221m, outpacing revenue growth and showing the impact of this expense on the company’s profitable growth.

Looking forward, Remitly believes it can continue to drive down the cost of transactions as it continues to scale, aided by decreased costs and faster payment methods on the acceptance and disbursement side. It also continues to mention the benefits of AI on costs, particularly those associated with customer support.

Building direct connections to speed up transfers

Daniel Webber:

You mentioned direct integration, which not everybody has. Where do these direct connections come from and what’s the value of that for your business model?

Matt Oppenheimer:

We haven’t shared the specific number of direct connections, but this is another part of our flywheel. If you think about the scale that we have, the number of direct connections we can do per quarter versus when we were a tiny startup is so much better now.

What that means for customers is faster transactions with less friction. Over 95% don’t have to contact customer support.

Let’s take a customer that’s sending money from the US to HDFC, which is a bank in India. When we started, we might not have had a direct integration with HDFC: we would’ve had to have several different steps to send money to that disbursement partner.

With the scale and size that we have now, we’ve done multiple direct integrations, so that if there’s any sort of delay or issue, we’ve got a direct connection and can resolve that much faster and easier than when we had a bunch of intermediaries. Obviously, it also brings down the costs too because there aren’t as many intermediaries as well.

The impact of the US Affordable Remittance Act

Daniel Webber:

The proposed Affordable Remittance Act (ARA) was introduced in the US House of Representatives at the end of October. What benefits are you hoping to see from that?

Matt Oppenheimer:

We’re really excited about the ARA. It’s a legislative proposal that aims to grant us and other non-bank remittance providers like Remitly direct access to the Federal Reserve’s FedNow payment service.

This access would play a role in reducing collecting funds and domestic transaction costs, as well as help improve transparency and enhance services because it’s faster than a bank-to-bank transfer like ACH in the US, which is slower than a lot of other countries. So we’re excited about that.

There’s a lot of benefits if non-bank remittance companies can get access to FedNow. We’re grateful to Representative Torres for sponsoring that bill.

Remitly grows customers and send volume

Despite predicting lower sequential change for Q3 in last quarters’ earnings, Remitly still saw active customers grow 35% to 7.3 million, contributing to 42% growth in send volumes to $14.5bn.

Customer growth is rising as Remitly’s expansion into new markets continues. On the send side, Rest of World revenues growth accelerated to 58%, faster than 36% growth in US revenues, while on the receive side revenues from regions outside Remitly’s historically top-three markets – India, Mexico and the Philippines – rose to make up more than 50% of total revenues this quarter.

Overall, Remitly’s expanding network means that it now serves people in 30 send countries and more than 170 receive countries, with payments supported across more than 5,100 corridors.

Remitly’s approach to brand marketing

Daniel Webber:

How are you approaching your marketing spending and driving efficiency with it?

Matt Oppenheimer:

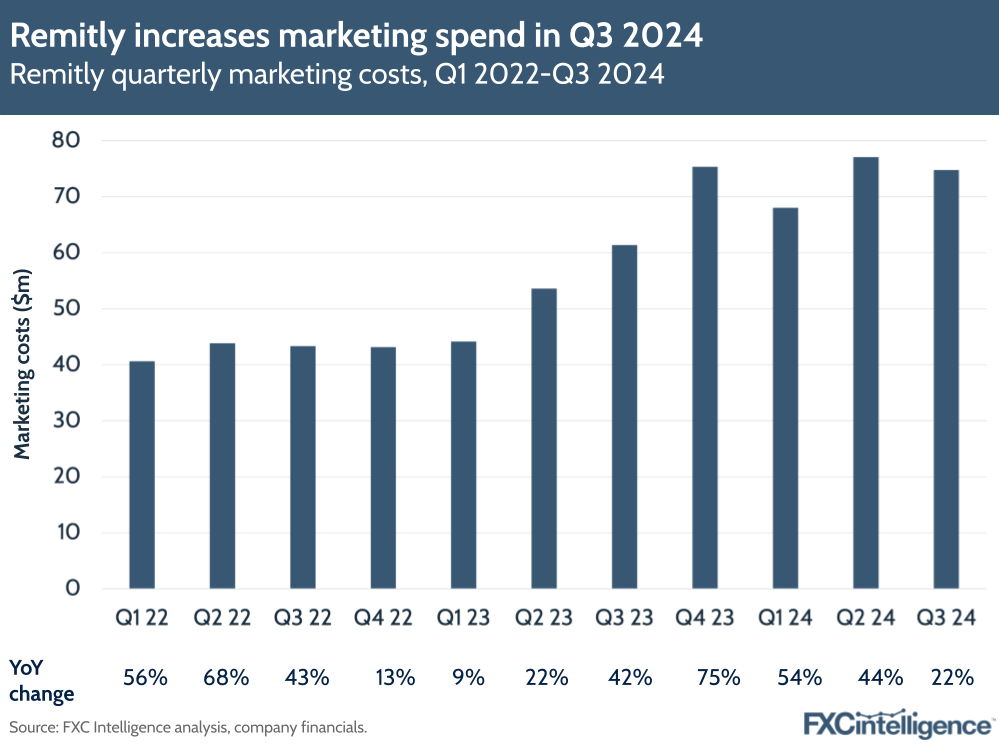

We added a record number of new customers again in Q3, and that’s indicative of the very effective and measurable marketing spend that we deploy.

My definition of brand is a promise, when delivered, creates a preference. Sometimes when folks think of a brand, they think of brand marketing, and that is a way to amplify a promise, when delivered, that’s creating preference.

Brand is owned by everybody in the company, but it starts and ends with the customer experience, and our product just continues to get better. We talked on the call about a customer named Sergario, and after she used our product, she shared it with five of her friends.

We’re seeing leverage from a P&L standpoint on our marketing spend, partially because we’ve spent the dollars to build a well-known brand, but foundationally because our product continues to get more and more differentiated. With that comes the word of mouth and positive brand halo that comes with having a differentiated product.

Remitly’s marketing spend growth

Remitly’s significant marketing focus saw costs rise again in Q3 2024 by 22% to $75m, though this was slower than growth during the same period last year. Remilty is taking steps to streamlining its approach by optimising its local digital marketing and carrying out targeted campaigns, but it also continues to report benefits from word of mouth marketing as the brand scales up.

The company noted that on a non-GAAP basis, marketing spend was $70.3m, which accounted for 20.9% of revenue – an improvement of 260 bps YoY. When tracked against active customers, marketing spend per quarterly active customer declined 8.5% YoY to $9.61.

Seasonally, Q4 sees higher investment in marketing from the company than other quarters, and the company expects this to be the case again this year as it targets customer acquisition in line with its 2025 goals.

How Remitly is using AI

Daniel Webber

You also mentioned AI on the call – what impact is AI having on Remitly and how are you thinking about leveraging it?

Matt Oppenheimer:

It will start and end with the customer, which may sound cliche, but it’s truly the way that we approach any sort of technology, which sometimes can get lost. There is definite applicability too in terms of how we can improve our service and our product for our customers with AI.

I mentioned our virtual AI assistant that is incredibly fast and effective and gets really good reviews from our customers, so we’re expanding the use cases, including adding additional languages like French and Spanish in addition to English, which has already been launched for a while.

If you look at our marketing, we have to market across over 5,000 corridors, 18 languages and 170 countries. Not only language, but the localisation of what it means to advertise and build creative across all these geographies is complex. We have used some AI tools that have increased the efficiency and effectiveness of our marketing deliverables.

Those are a couple of examples, but there is lots of opportunity and the team’s focused on it.

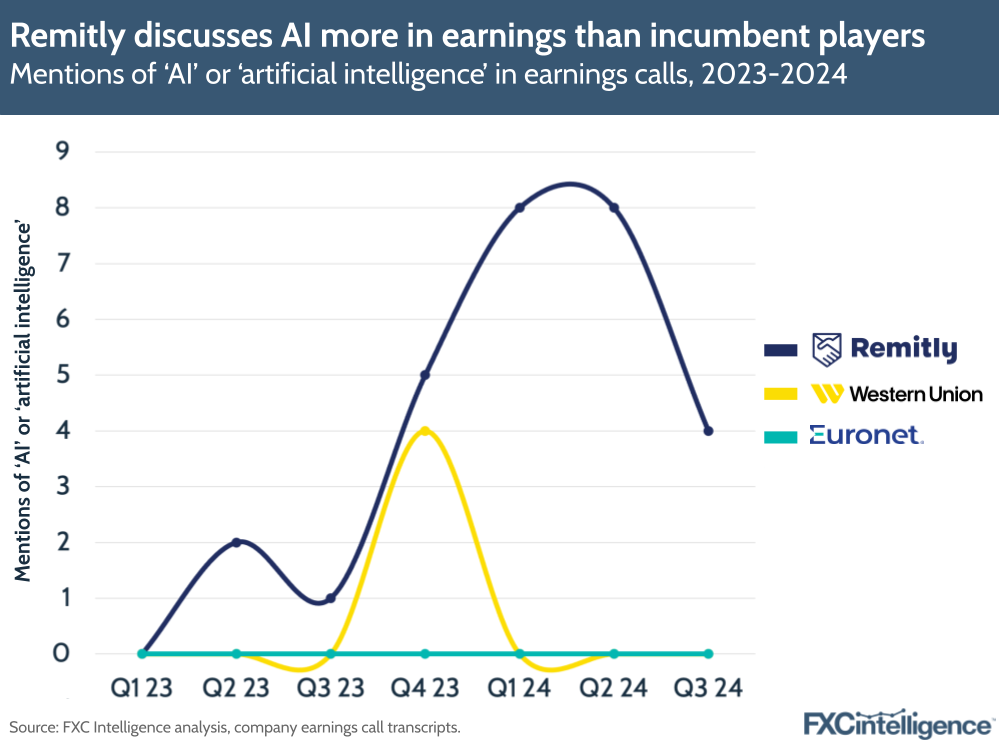

How often is Remitly talking about AI compared to other players?

While earnings calls don’t cover all initiatives in a company, it is notable that Remitly continues to champion AI during its calls, while other publicly traded remittances players aren’t mentioning it nearly as frequently, if at all.

Remitly mentioned AI or artificial intelligence four times in its Q3 2024 earnings call, whereas two other major money transfer players, Western Union and Ria parent company Euronet, didn’t mention either of these terms in their Q3 calls.

Hype around generative AI has led to a boom in interest in the technology, but in some cases this hasn’t yet yielded actionable results. However, Remitly has already begun to use the technology to assist with customer service, as well as in some marketing applications.

Remitly’s strategy going into 2025

Daniel Webber:

How are you looking at 2025?

Matt Oppenheimer:

We’re excited and in some ways, I’m already thinking up to 2030. We actually used one of the stats that FXC Intelligence shared, which is that the consumer cross-border payments market is expected to grow to over $3tn by 2030, so 2025 is another step towards that.

There’s lots of room to grow in markets we’ve been in for 14 years, and those geographies are still growing.

We probably don’t talk enough about how much room there is to grow in markets that I’d categorise as “relatively recently launched”. Sub-Saharan Africa is growing, and our quarterly active users there grew 50% year-on-year. So that’s exciting and there’s lots of opportunity in that region, but we’re already in that region. It’s about growing from a strong base.

We just launched in lots of countries and we’ll continue to launch new corridors. We’re excited as ever about our broader vision of cross-border financial services, and looking at how we can deepen the relationship with our existing remittance customers. The team’s already hard at work because the things we’re doing now – and have been doing for the last several quarters – are what will deliver 2025, just like the things that we delivered in Q3.

We did a lot of great things in Q3, but it was really due to the foundation that we laid in prior quarters and years. We’re excited, based on what we’re seeing, about 2025 and beyond.

Daniel Webber:

Anything else you’d like to cover?

Matt Oppenheimer:

I’m always going to bring it back to the customer. As a founder going back 14 years, the reason businesses exist full stop is because of how well they serve their customers. We have the privilege of serving customers that are inspiring, that make amazing sacrifices and journeys to support their families and loved ones, and historically have been underserved because of the complexity of this industry.

Even though I would say a lot of folks in this space have good intent, it’s a really hard industry to really reinvent cross-border P2P payments. We’re excited to do that, specifically because of our customers.

Daniel Webber:

Matt, thank you.

Matt Oppenheimer:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.