Instant payments platform Pix has transformed the payments landscape in Brazil and the country’s central bank is now seeking to facilitate cross-border linkages that could enable the use of the system abroad. We explore what has driven the platform’s growth and its cross-border potential.

Over the last few years, Brazilians have increasingly moved away from debit and credit cards and towards Pix – an instant payments system owned and regulated by Banco Central do Brasil (BCB), Brazil’s central bank.

Launched during the Covid-19 pandemic, Pix makes instant money transfers incredibly easy for people in Brazil, who are able to make payments online or in stores by scanning a QR code with their phone or inputting a code into a Pix-enabled payment or banking app. The system has since been adopted by almost 170 million users and has enabled billions of transactions, transferring more than a trillion Brazilian reals every month.

Now, the BCB is considering agreements to connect Pix with similar instant payment platforms in other countries. Various fintechs have already enabled the payment method to be used in Argentina and Uruguay, and the BCB has also expressed interest in Nexus – a project being spearheaded by the Bank for International Settlements (BIS) to develop a platform that will enable instant payments platforms around the world to connect with each other.

Pix has seen particular success in a very short amount of time domestically. But what is the impact that it could have across borders? This report explores what’s driven the success of Pix so far and its potential for overseas payments.

What is Pix?

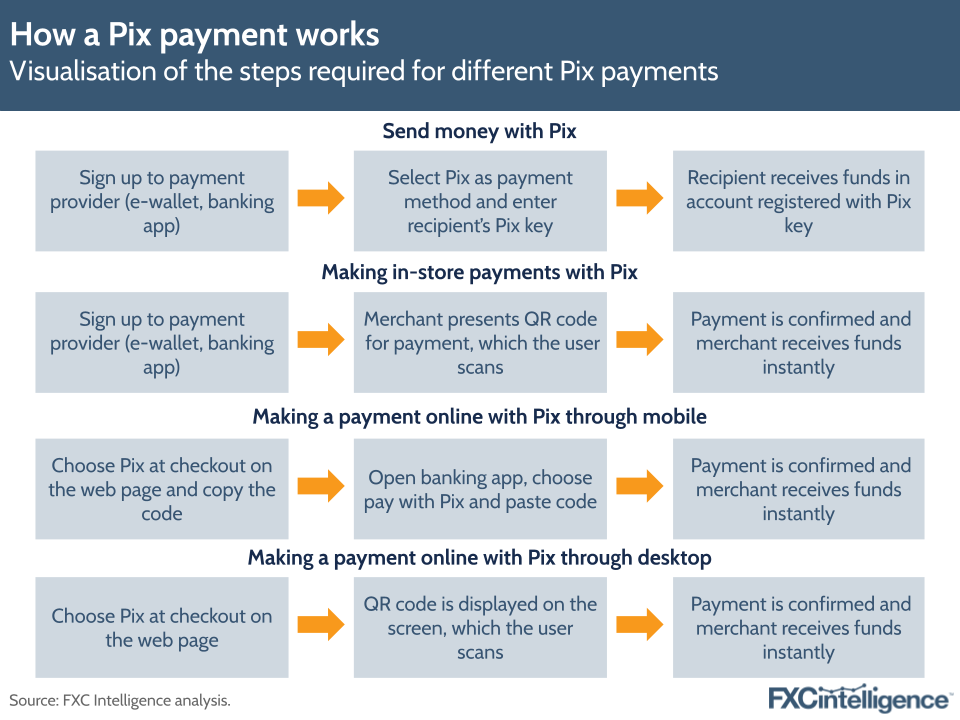

Pix is an instant payments system that settles fund transfers in seconds and is available 24/7/365. Pix can be used to make instant money transfers between users on mobile phones without the need for card acquirers, card schemes or issuers.

Instead, Pix works with the use of two systems. The first is the Instant Payment System (SPI), the BCB’s central infrastructure that settles payments instantly between payment providers. The other is the Transaction Accounts Identifier Directory (DICT), which connects user’s account info with a unique Pix ‘key’ that they can use to make payments – this could be their phone number, email address or even a randomly generated number.

Recipients can make payments to other Pix users simply with their Pix key, rather than needing to input their bank details. This does mean that for P2P payments, both the sender and recipient need to have a bank account that is registered with Pix in order to make a payment.

Why was Pix introduced?

Ultimately, Pix was introduced to enable a faster, more convenient system for sending and receiving payments. Consumers benefit from being able to receive money from others faster and at no extra cost.

It is also less costly for businesses and merchants, which are able to collect funds fast, without additional intermediaries. Pix’s benefits are similar to other instant payments systems worldwide, such as India’s UPI, the UK’s Faster Payments system and the US’s recently launched FedNow system.

Prior to Pix, Brazil had a number of traditional payment systems for money transfers. These include Transferência Eletrônica Disponível (TED), a real-time money transfer system with no limits on transactions; Documento de Ordem de Crédito, another electronic money transfer method; and Boleto, which allows users to generate a barcode that they can use to settle online payments with cash.

However, as with other legacy payment systems worldwide, many of these existing payment instruments had downsides when it comes to fees, limits or transfer speeds. TED, for example, would incur fees depending on the bank and type of account and payments could only be initiated during regular banking hours.

The BCB introduced Pix with the aim of modernising payments in Brazil, reducing the reliance on cash transactions, increasing financial inclusion in the country and strengthening competition.

How has Pix grown?

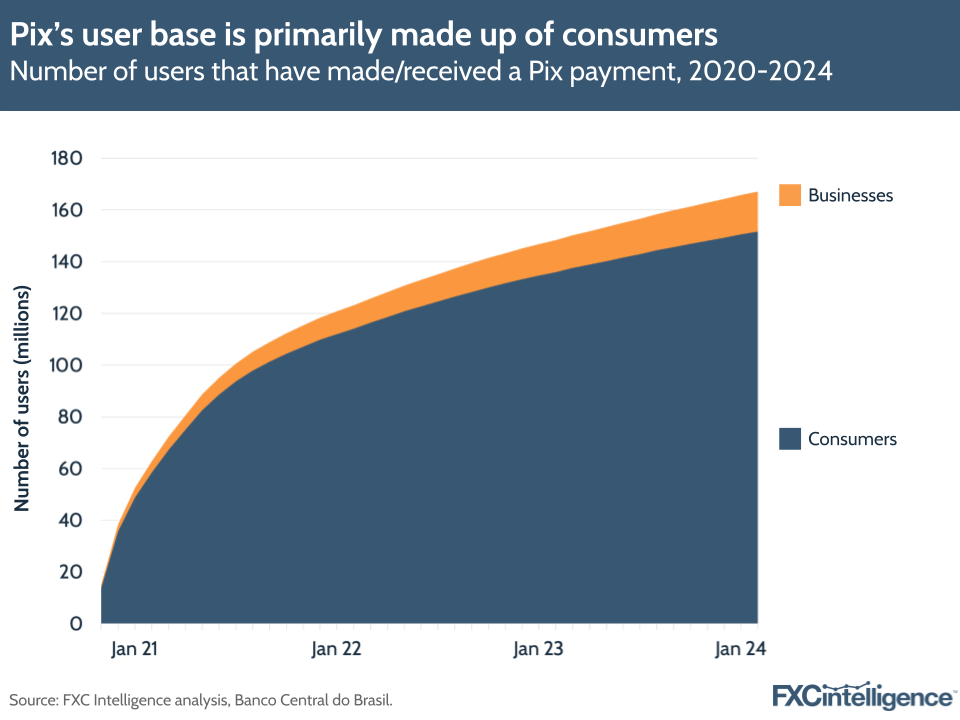

In the space of just a few years, Pix has taken over instant payments in Brazil. According to the BCB, out of around 160 million Pix users with a registered DICT key in February 2024, around 147 million of them are consumers. Looking specifically at the number of users that have made or received at least one Pix payment, around 91% of them (152 million) were consumers in February 2024.

The World Bank’s latest figures show that the Brazilian population above the age of 15 totalled around 171 million in 2022, which gives a sense of how ubiquitous the app has become.

World Bank data also shows that bank account ownership has risen in Brazil over time, from around 70% in 2017, to around 84% in 2021 (though it doesn’t note figures for intervening years). In a speech at the opening of the Brazilian presidency of the G20, BCB governor Roberto Campos Neto said that Pix had played a pivotal role in financial inclusion across Brazil.

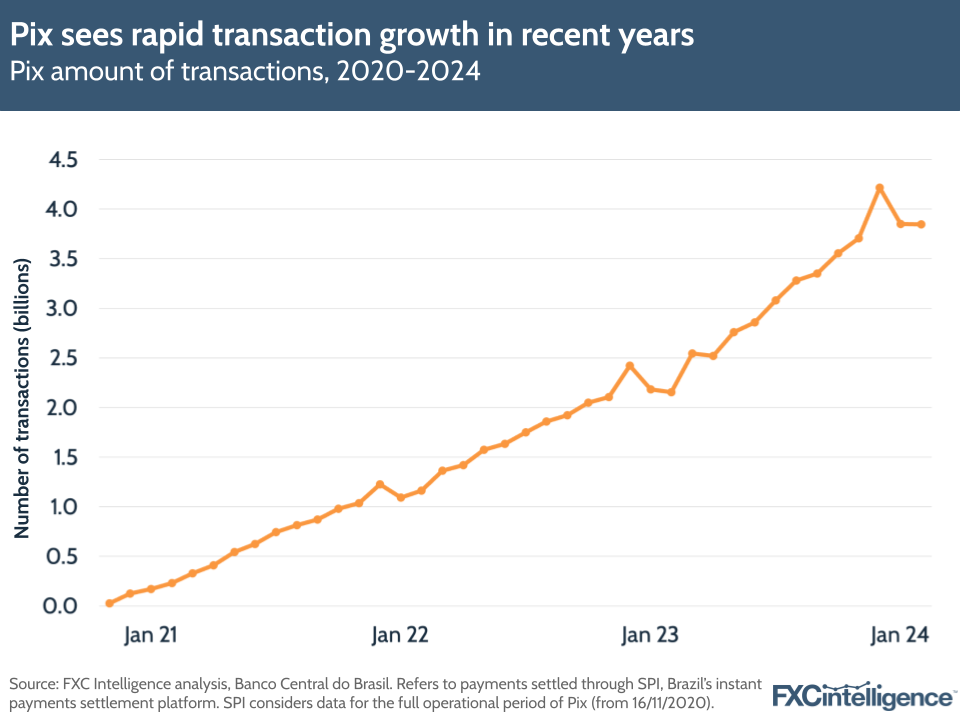

In terms of volumes, the BCB relays data from Pix transactions over two periods: Pix transactions made using SPI (i.e. the full version of Pix) and transactions made via non-SPI settlement infrastructure, which includes data from Pix’s “restricted operation” period from March to November 2020.

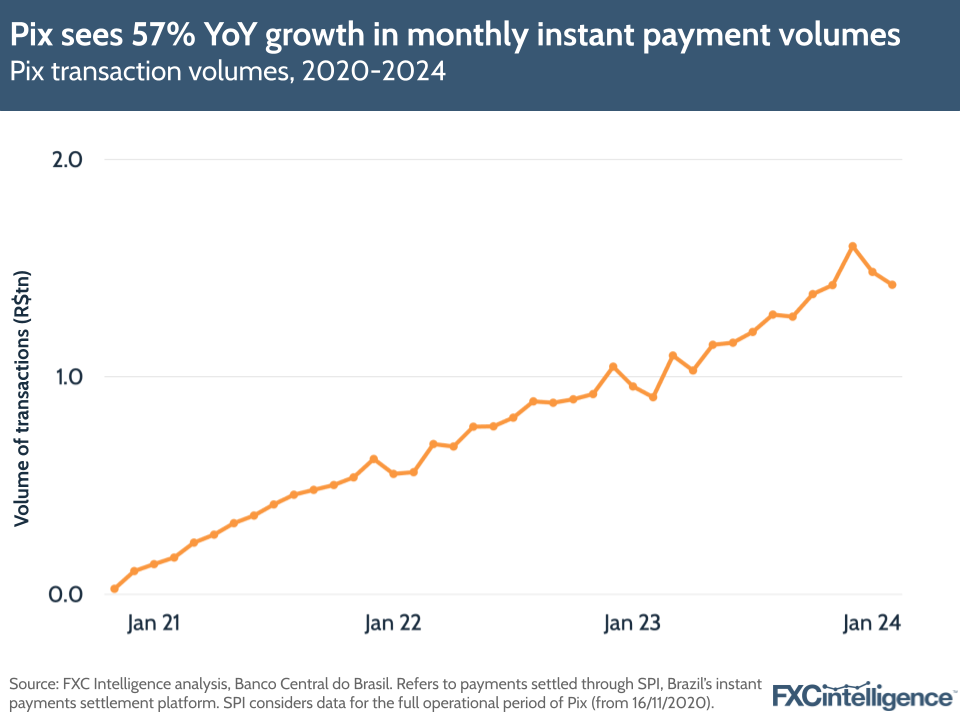

Looking solely at SPI-settled transactions, Pix continues to grow significantly, with R$1.4tn ($283bn) of volume passing through the system in February 2024, a 57% YoY rise compared to February 2023. In total, Pix saw R$14.4tn ($2.8tn) of volume in 2023.

In terms of transaction numbers, there were 3.8 billion SPI transactions in February 2024, a 79% YoY increase, while in 2023 there were around 36 billion SPI transactions in total.

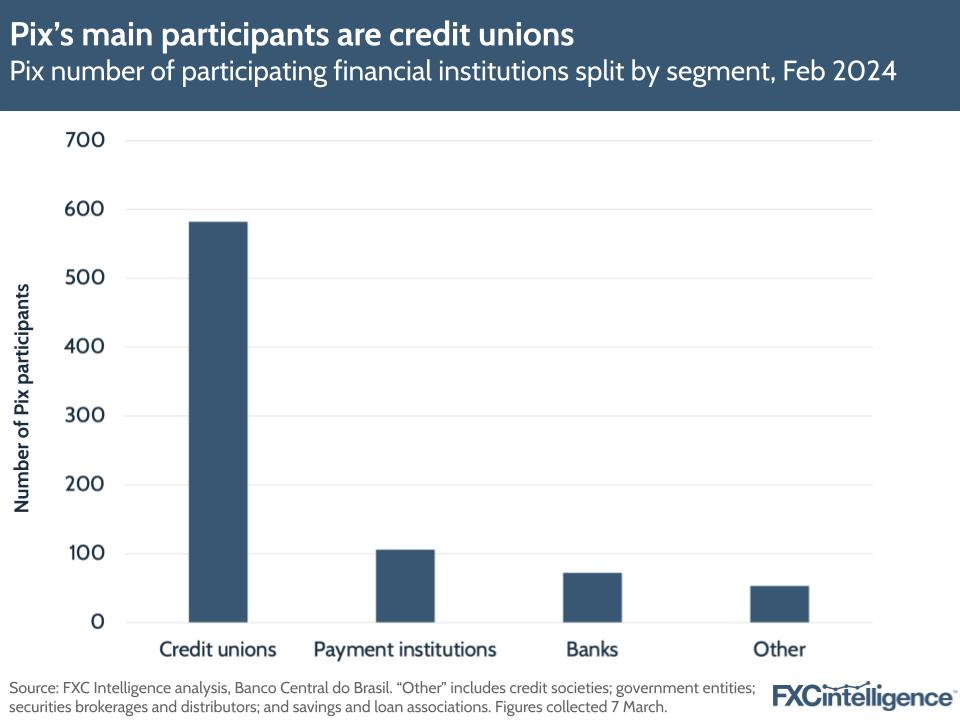

Pix has also seen significant buy-in from financial institutions, including banks, credit unions, payment institutions and a variety of other organisations, with over 800 being either a direct participant in Pix (meaning they have a specific payment account within the SPI that allows them to settle Pix transactions) or an indirect participant (meaning that they need to route payments through a direct participant). In order for consumers or businesses to use Pix, they need to have an account with one of these institutions.

With regards to these participating organisations, credit cooperatives and banks make up the largest share, though payment institutions account for around 13%. While traditional financial institutions are pushing the platform, a sizeable number of fintechs have also adopted it.

Which segments are transacting through Pix the most?

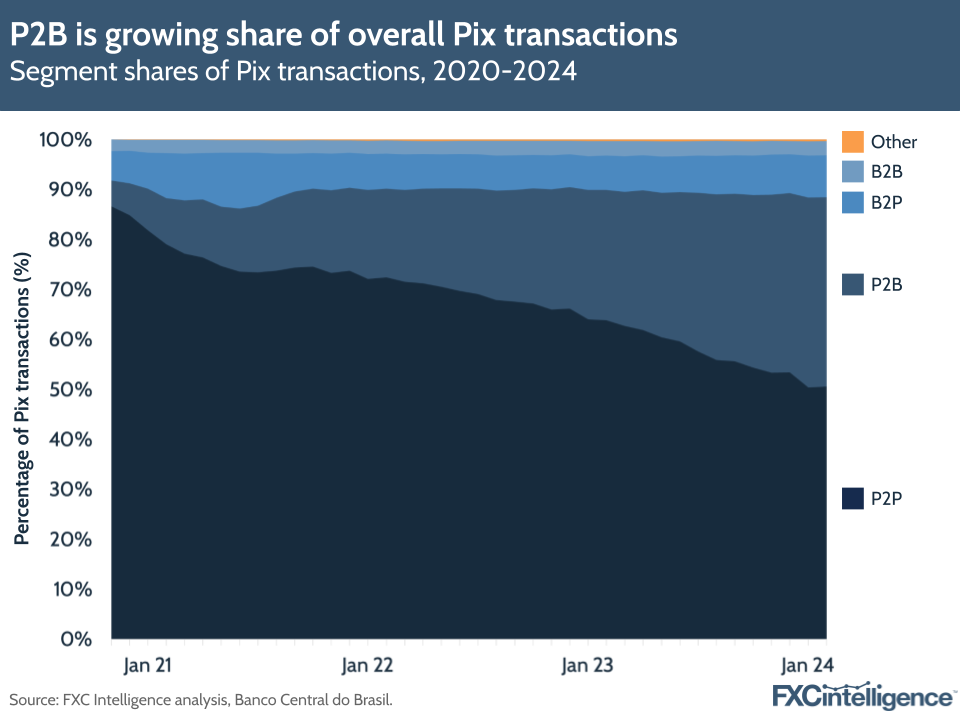

Pix’s current user base is still primarily made up of consumers, who are making the majority of transactions on the platform. However, the volume (i.e. total amount sent) and number of transactions that businesses are sending through Pix has grown significantly in recent years.

Looking at transactions posted by the BCB , P2P payments accounted for 51% of Pix transactions in February 2024, though this has consistently declined since February 2021 (a few months into Pix’s operation, thus giving an idea of its early stages), when P2P payments accounted for 79% of transactions.

However, person-to-business (P2B) transactions (which includes merchants) now account for a significantly higher percentage of transactions overall at 38%, compared to 9% in February 2021.

Government transactions to and from businesses and consumers (encapsulated in the ‘other’ category in the above graphic) have also grown in number but their share of transactions hasn’t changed significantly. The same is true of B2B payments.

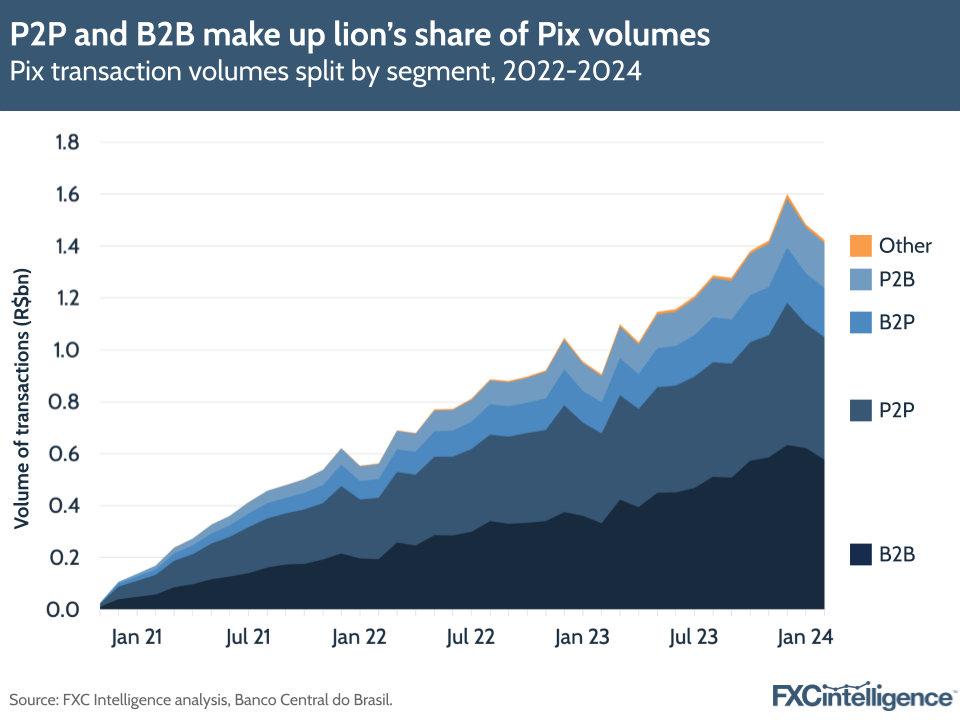

However, looking at Pix volumes, over time B2B payments have overtaken P2P payments in terms of total volume share. Out of a total R$1.4tn of volume in February 2024, B2B payments contributed 41% – up from 34% in February 2021. By comparison, P2P payments still made up a large share, at 33%, but this was down from 45% in February 2021. Also in February 2024, P2B payments accounted for 12% of volumes, while B2P payments accounted for 13%.

“A unique aspect of Pix is its widespread acceptance among businesses of all sizes,” says Liber Fernández, Chief Commercial Officer of embedded finance platform Inswitch. “From large retailers to small local vendors, Pix is widely embraced across Brazil, making it a versatile and universally accepted payment method.”

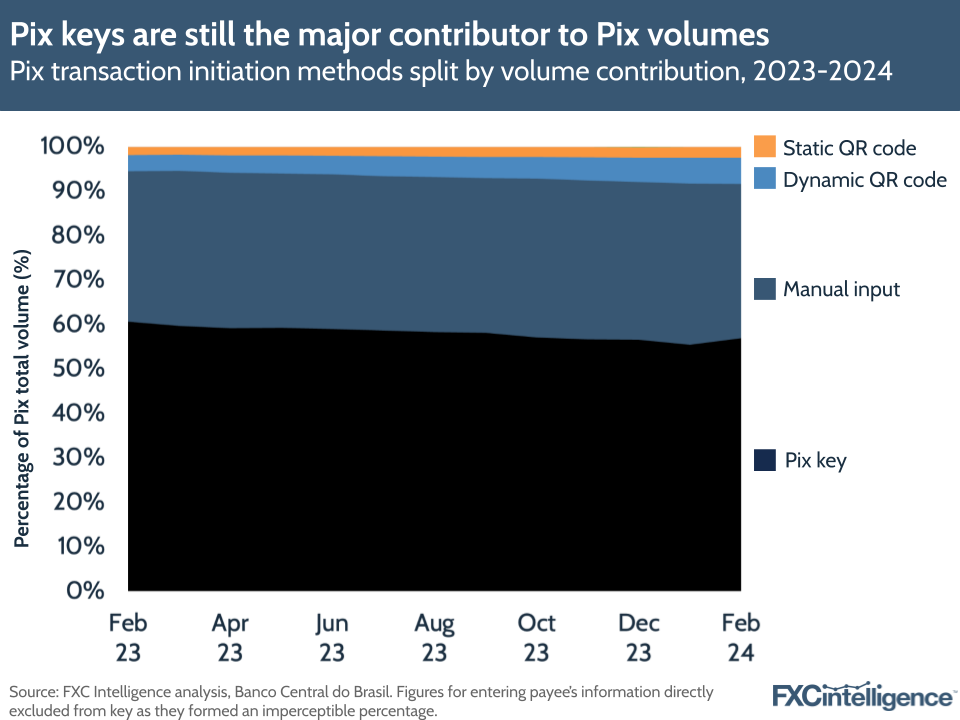

Looking at which methods are actually driving the platform, we find that Pix keys are still very much the driving force behind Pix payments, with 57% of transactions in February 2024 made via Pix keys and 35% made by manually inputting codes.

QR codes still make up a smaller share of Pix payments by comparison, with 2% of payment initiated through static QR codes (which merchants ask users to scan and input the amount they are paying) and 6% of payments initiated using dynamic QR codes (which can be changed by merchants to enable payments of different amounts). However, both of these payment methods have also grown their share of transactions initiated over time.

The number of Pix transactions significantly outnumbers credit and debit card payments. Instant payments specialist Matera revealed in a recent report that the number of Pix transactions was 13% higher than credit and debit cards combined as of Q2 2023 (the most recent data available), when there were 9.4 billion Pix transactions, versus 4.4 billion card and 3.9 billion debit transactions.

Explore capabilities for cross-border payment companies with FXC Intelligence data.

What factors are driving Pix’s growth?

A number of factors are driving the success of Pix, with the simplest being the speed and lower fees that Pix offers versus other payment methods.

Pix is free for individuals to use, with costs only arising from using in-person services/phone support when there are electronic channels available. Businesses can be charged for using the service for paying or receiving payments, with the BCB reporting that these fees can be ‘freely established’ by financial institutions providing these services.

Having said this, because the BCB runs the infrastructure for Pix itself, this has prevented big companies from rapidly gaining market share – a parallel is currently being seen in India, where the government is attempting to curb the activity of Google Pay and PhonePe, which hold the largest stakes in UPI payments. While the system encourages competition in the market amongst key institutions, the lack of intermediaries means that costs have been lower than other methods.

According to a report from the IMF from July 2023, Pix payments take around three seconds to settle on average, versus two days for debit cards and 28 days for credit cards. Meanwhile, the average cost of transactions for firms/merchants is only 0.33% of the transaction amount, against 1.13% for debit cards and 2.34% for credit cards. In terms of limits, participants are also free to set these with a mind to addressing their core customers.

Pix is more accessible and convenient for customers than other methods that either aren’t always open or have rigid limits. The method also has a standardised UI that financial institutions have implemented, making it much easier for customers to pick up and use no matter what app they are paying with.

It also helps that Pix arrived during the Covid-19 pandemic, when contact-free, seamless payments were a hot topic. “[Pix] encouraged social distancing and reduced the need to handle cash or rely on bank hours,” says Fernández.

“The platform’s seamless integration into existing banking infrastructure and its focus on inclusivity – allowing users to make transactions through various channels – have also contributed to its rapid adoption,” he adds.

Pix adoption has also been spurred by the fact that larger institutions (to be specific, ones with more than 500,000 customers) have been required to adopt the system.

“This meant that everybody would integrate it, because if you don’t do it, you would be out of the market,” says Ralf Germer, CEO and Co-Founder of Brazilian payment processor PagBrasil.

Not only are institutions required to add Pix as an option for customers, but they are required to adhere to some strict rules and regulations on KYC and compliance. This includes tagging and holding suspected fraudulent transactions in the DICT platform.

“Pix prioritises security for its users, implementing robust authentication measures and encryption protocols to safeguard transactions and sensitive information,” says Fernandez. “This commitment to security enhances user trust and confidence in the Pix method, further solidifying its position as a leading payment solution in Brazil.”

All this is the result of a well planned out approach to digitalising payments, which, Germer, is the result of the BCB looking at other instant payment systems worldwide.

“[The central bank] travelled around the world – to the US, to China to look at Alipay and WeChat, to India to look at UPI, to Europe to look at the SEPA system,” says Germer. “They took what worked well and avoided what didn’t work from all these countries.

This, alongside public consultations, allowed the system to define strong regulatory standards early. Pix is also subject to dialogue between public and private stakeholders via Pix Forum, a permanent advisory committee coordinated by the BCB that helps establish rules around how it is used.

How can I track speed and pricing data across Latin America?

How Pix compares to other instant payment systems worldwide

Pix came after other instant payment systems, but has had a major impact in a short amount of time. According to an ACI Worldwide report released in March 2023, Pix represented 15% of instant payments globally in 2022; compared to similar systems worldwide, Brazil’s system stands out due to its low transaction fees and its lack of limits.

Pix is most often compared to UPI, as the two systems bear similarities in their reasons for introducing instant payment systems, the way their payment systems operate and the way they have proliferated across their respective countries. However, there are some crucial differences.

For example, Pix is regulated and supervised by the BCB, while UPI is owned and operated by NPCI, a private payments company with the involvement of the Reserve Bank of India (the country’s central bank) at the board level. This has likely had an impact on mandating adoption amongst financial institutions across Brazil, which in turn has led to the massive boost in customers.

In 2022, Brazil’s population was 215 million while India’s was roughly six and a half times bigger at 1.4 billion, yet Pix has grown its user base significantly compared to UPI. In a report on UPI in December 2023, the NPCI said the platform had more than 390 million users (the most recent figure available), while in the same month Pix had 160 million users. This shows the speed at which Pix is growing and has penetrated Brazil’s population compared to UPI, which launched in 2016.

UPI is processing substantially more transactions than Pix, with more than 12 billion transactions passing through the platform in February 2024, compared to around 3.8 billion through Pix on the SPI infrastructure. Again, it should be noted that UPI has been around substantially longer. Three years after the launch of UPI (in April 2019), the system had processed 781 million transactions, while three years after the launch of Pix it was processing 3.7 billion transactions, which again demonstrates the speed of adoption of Pix.

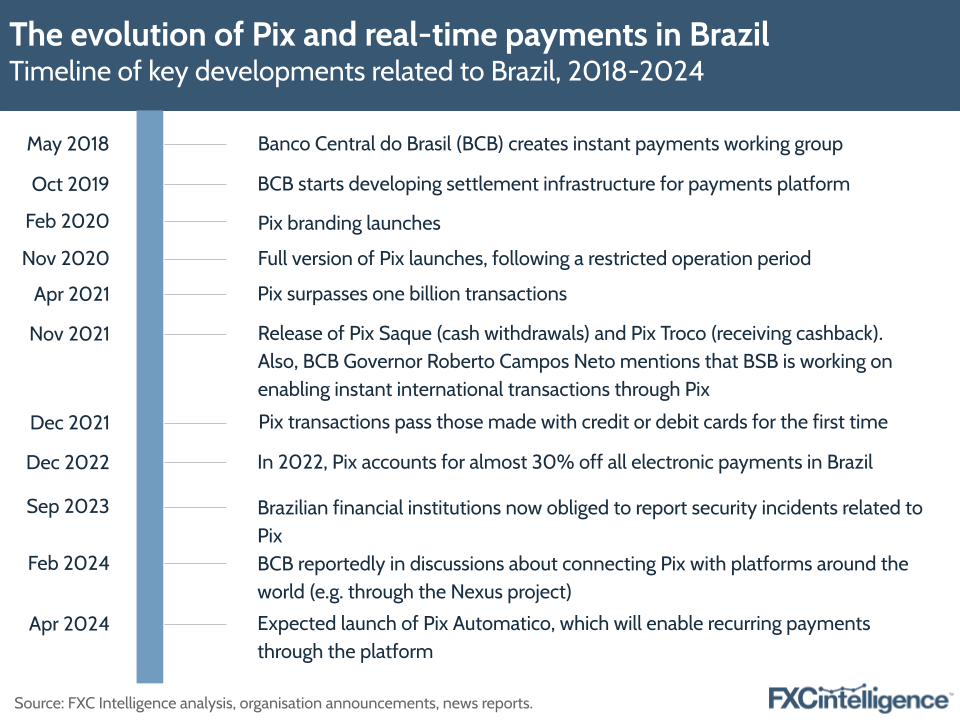

In order to increase its usability and spread its reach to more applications, the BCB has introduced new features to Pix over the years, such as the ability to withdraw cash with Pix (Pix Saque) and obtain physical cash for digital transactions (Pix Troco). A number of additional features are in the pipeline, including a buy now, pay later product (Pix Garantido); a solution for recurring payments that could be used for things like paying bills and subscriptions (Pix Automatico); and Pix payments using NFC technology.

Another feature that has been repeatedly discussed, but not yet formalised, has been the potential of linking Pix with other instant payments systems worldwide.

Pix’s cross-border potential

The success of Pix in a short amount of time has led to speculation about the payment system’s expansion beyond borders and enabling cross-border linkages with other countries – similar to UPI and a number of other systems in Southeast Asia.

Many countries that have already enabled cross-border payment linkages have looked to enable fast instant payments across borders using local currencies, thereby reducing the need to convert to USD, which in turn reduces transaction costs.

Last year, Brazil signed a deal with China to drop USD as an intermediary currency for exchanges. It also revived discussions about creating a common currency with Argentina. A cross-border Pix model could therefore align with Brazil’s ambitions to reduce the power of the US dollar over its economy – an ambition it shares with the other members of BRICS (Russia, India, China and South Africa).

Pix is not currently able to enable instant cross-border transfers through its infrastructure; payments are deposited in Brazilian real and are available through Brazilian banks and financial institutions. Having said this, several fintechs have filled the gap by enabling Pix payments to merchants based in other countries through their own infrastructure, with one example being PagBrasil. Sending money to recipients in Brazil via Pix is possible from other countries but requires the assistance of specialised payment providers, such as Wise, Paysend and Remitly.

However, the Governor of the BCB, Roberto Campos Neto, has repeatedly spoken about the fact that the bank is working on developing Pix international transactions and bilateral linkages with other countries. The BCB is also one of more than 60 central banks that are currently part of Nexus – a project from the BIS that aims to create a single platform through which instant payments across the world can sync up in order to easily create a link with another country. The platform is currently being tested in five Asian countries.

One motivation for this will be enabling Brazilian travellers and tourists to use Pix in other countries, similar to Alipay, which Chinese travellers are now able to use to make payments around the globe.

It could also be extremely beneficial for sending and receiving money from other countries.

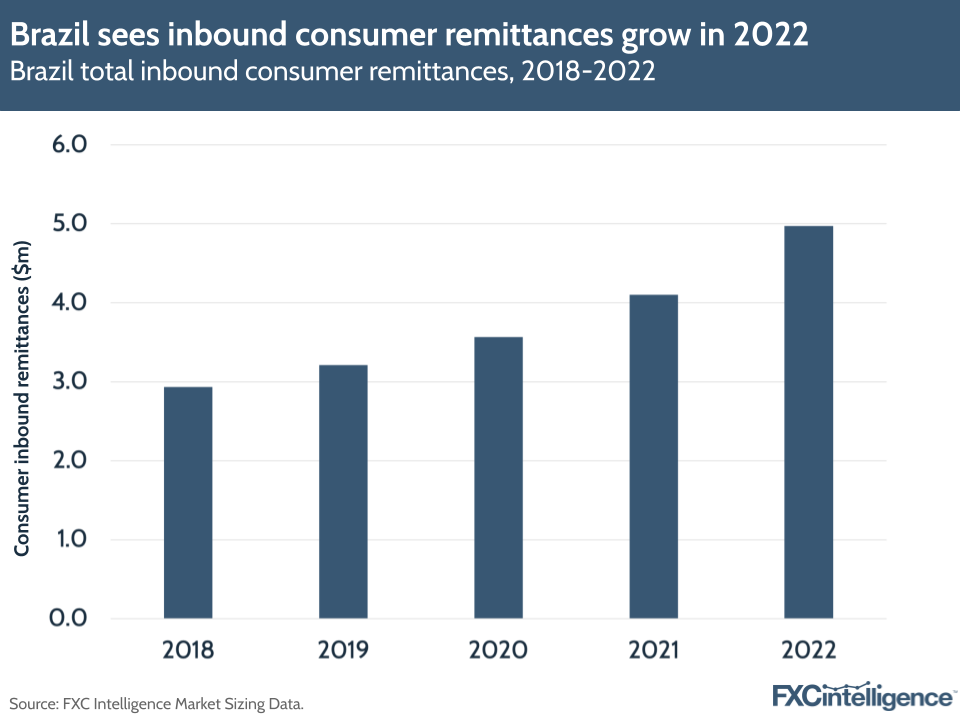

FXC Intelligence data shows that inbound consumer remittances into Brazil grew by 21% in 2022, with some of the biggest source countries being the US, Japan, Portugal, Italy and Spain.

Enabling faster payments across borders will benefit not just remittances into and out of the country, but also growing B2B payments in and out of the country, which FXC Intelligence has also mapped out not just across Brazil but also worldwide.

The internationalisation of Pix through cross-border linkages could be a natural progression for the platform. In the meantime, fintechs have already enabled the use of instant Pix payments to merchants abroad through a series of partnerships in local countries.

For example, PagBrasil has launched International Pix, with an initial focus on locations with significant tourist inflows, such as Uruguay, Argentina, Chile and Florida. International Pix is an instant payment method with real-time currency exchange, and it enables merchants to generate QR codes that Brazilian customers can scan with their app or e-wallet.

It should be noted that this is specifically a browser-based checkout experience, rather than P2P. It works in the same way as making a Pix payment online from Brazil, with an FX currency conversion element attached – however, the exchange rate is much lower than credit card transactions.

“The total revenue from the countries in which International Pix is operating – Argentina, Chile, Mexico, and Uruguay – already accounts for 1% of PagBrasil’s total payments volume,” says Germer. “Since its launch ten months ago, it has become the fastest-growing solution for our company. In February, International Pix’s TPV rose 80% over January, and we expect it to grow 60% in March from February.”

Meanwhile, alongside Banco Itaú, Inswitch has also launched a solution (Pix No Mundo) that enables Pix payments to be made by Brazilians to merchants in Uruguay, with a vision to introduce the solution in Argentina, Paraguay and Chile. However, according to the company, merchants receive the payments in three business days, not instantly.

According to Germer, the BCB has been very supportive of PagBrasil’s move to take Pix across borders with its solution. This could be because, while cross-border payments are on the agenda for the central bank, there are other priorities that need to be addressed first and present difficult challenges.

“From what I can see, there are more important things [coming up],” he says. “Enabling contactless payments with Pix or having Pix Automatico for subscriptions or recurring payments. Such a complex project takes more than a year to be completed.

How can I find out more about inbound and outbound remittances to Brazil?

Conclusion

Pix has been an example for other instant payments systems to follow, particularly in terms of driving adoption, enabling security and highlighting the benefits of its system.

The cross-border potential of the system has not escaped the notice of the Brazilian central bank, particularly when it comes to supporting Brazilian expats and tourists and enabling faster payments. Germer refers to “Pix fever” spreading across Brazil and to other neighbouring countries.

It will be interesting to see how the country supports ongoing global cross-border initiatives going forward. However, with other features more immediately in the pipeline, for now it will be a case of watch this space.